The Weekly #240

The Weekly #240

Flurry of more constructive headlines are now offsetting the negativity that was dampening valuations previously. Bitcoin strength remains in focus for investors.

Join the 1000’s founders, investors, crypto funds, brokerage firms, and developers in getting free cutting-edge crypto research by subscribing below:

Turning on a Dime

It’s as if last week was the mirror image of the previous. Sentiment within the cryptoasset market has turned positive.

What was a once severe capitulation, driven by an onslaught of hostile regulatory headlines within the US, is now being offset by more constructive news, particularly around the filings of spot ETFs from large AMs.

Zooming out, we can see a $988B-$1T was the local floor in prices put in by investors after the SEC went after the two largest crypto exchanges - Binance and Coinbase.

Last week, the cryptoasset market gained 11%, reversing and surpassing valuations during this largely negative week. What’s more, the upwards channel looks to have resumed with the SEC headlines driving prices to temporarily break to the downside.

A flurry of more constructive headlines turned the tide (markets can be very reflexive…). News around Blackrock filing for a BTC spot ETF and the launch of EDX exchange helped drive BTC and ETH to their strongest weekly gains since March 13th.

Investors also likely realize that SEC reg enforcement or securities law isn’t negative in and of itself. They also realize there are more jurisdictions exploring cryptoassets constructively outside of the US.

Now clients of HSBC can buy BTC and ETH RTF directly from their banking mobile.

BTC rallied 26.73% from its June low to reach a high of ~$31,458. Meanwhile, ETH fell just shy of the $2k mark at $1,930 last week.

BTC’s main resistance zone is $30k-$31k which marked the high of April 2023, June 2022 and the bottom for May-July 2021. BTC will also look to hold $30k as support.

Technicals point to overbought levels currently with near-term correction as being more likely. However, the rally has shown that the worst has likely been behind us with $30k-$31k BTC/USD acting as a sticking point once again.

We also note BTC/USD bouncing 4% above its 200d MA in a signature constructive move on the 14th of June 2023.

In other words, the hostile US clampdown on crypto was not priced by investors to the same degree as the collapse of FTX when fear and contagion were at their peak (marked by the bottom in valuations).

All eyes remain firmly on BTC (for now)

The filing of BTC spot ETF by Black (and then subsequently others) meant that BTC remained firmly in the investor spotlight.

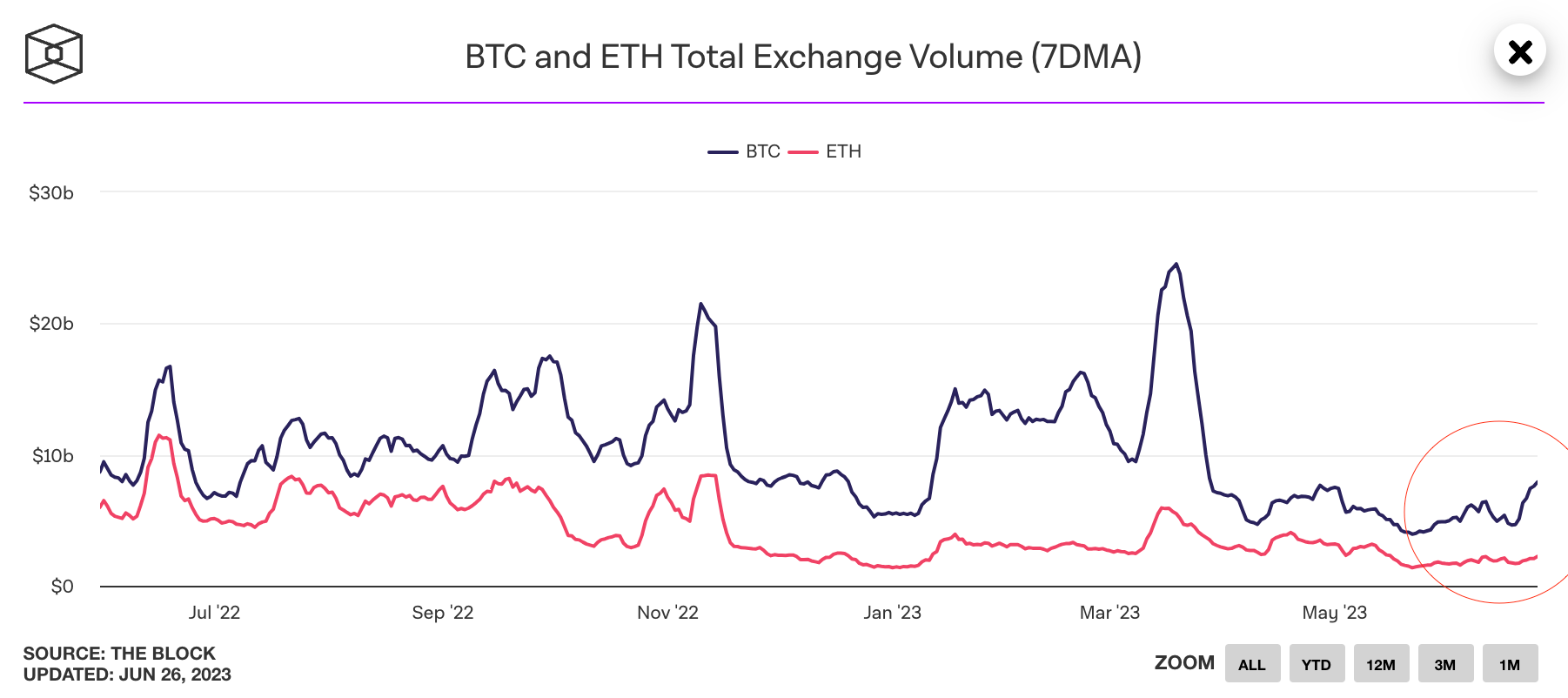

BTC spot volumes have effectively doubled in June vs. ETH which has stayed relatively flat.

The realized vol spike for ETH/BTC that we said was imminent finally came, and the direction was to the downside.

We see ETH/BTC short-term as recovering from oversold technicals but still pulled down vs. up. At the point in which a Bitcoin spot ETF is approved, ETH/BTC may then be more constructive which may come in the 0.05-0.055 zone.

Bitcoin dominance measures have broken to new highs since April 2021 (51.5%) and have also broken out of its sideways channel. Remember, BTC dominance was already strong leading into the Bitcoin spot ETF news. A 48% dominance acting as a sticking point was the hint that something was brewing…

As we’ve mentioned many times this year, a break out to the upside would mark a new regime change of prolonged BTC strength.

We also note that BTC relative strength often comes in the first innings of a bull market prior to lower cap names starting to outperform once retail enters the market in numbers.

US regional banking indices which have been inversely correlated with BTC dominance may add further fuel to BTC relative strength.

Bitcoin’s strength has also come at the expense of ETH and alts losing dominance as well as stablecoin dominance. Therefore, we see the current rally as not representing a ‘classic’ reflexive risk continuum environment (BTC does well, ADA does better).

L1/BTC ratios is another way of showing this too with SOL/BTC and NEAR/BTC yet to show meaningful momentum swing to the upside compared to the past 2 years.

And your classic consensus high beta plays on ETH are now diverging from ETH itself. RPL/ETH has reached <19 on its daily RSI - a dynamic that will make some investors excited while causing concern for others.

This is not to say sectors like DeFi haven’t performed well over the past week. They have. But these large moves are more indicative of short coverings against an increasingly illiquid market.

Zooming out, DeFi’s rally last week took its ETH ratio back to resistance once previously support (18%). The default momentum still looks to be down unless suggested otherwise.

Macro Cocktail of the Month:

1 part - Regional bank pressures mounting

1 part - increased liquidity

1 part - disinflation

1 part - softening labor market

Investors are now placing a 72% probability of a further 25 BPS rate hike in the next FOMC meeting following other central banks like BoE that continue to battle against sticky core inflation.

Troubled regional banks are now facing the prospect of even higher nominal rates and a 2-10 yield curve that is looking to make a new low this cycle. Coupled with concerns about CRE exposure and investors are starting to worry once again.

Bitcoin, born out of the 2008 financial crisis, has the narrative behind it: an alternative value-transfer system + hard asset against liquidity facilities aimed at propping up financial markets.

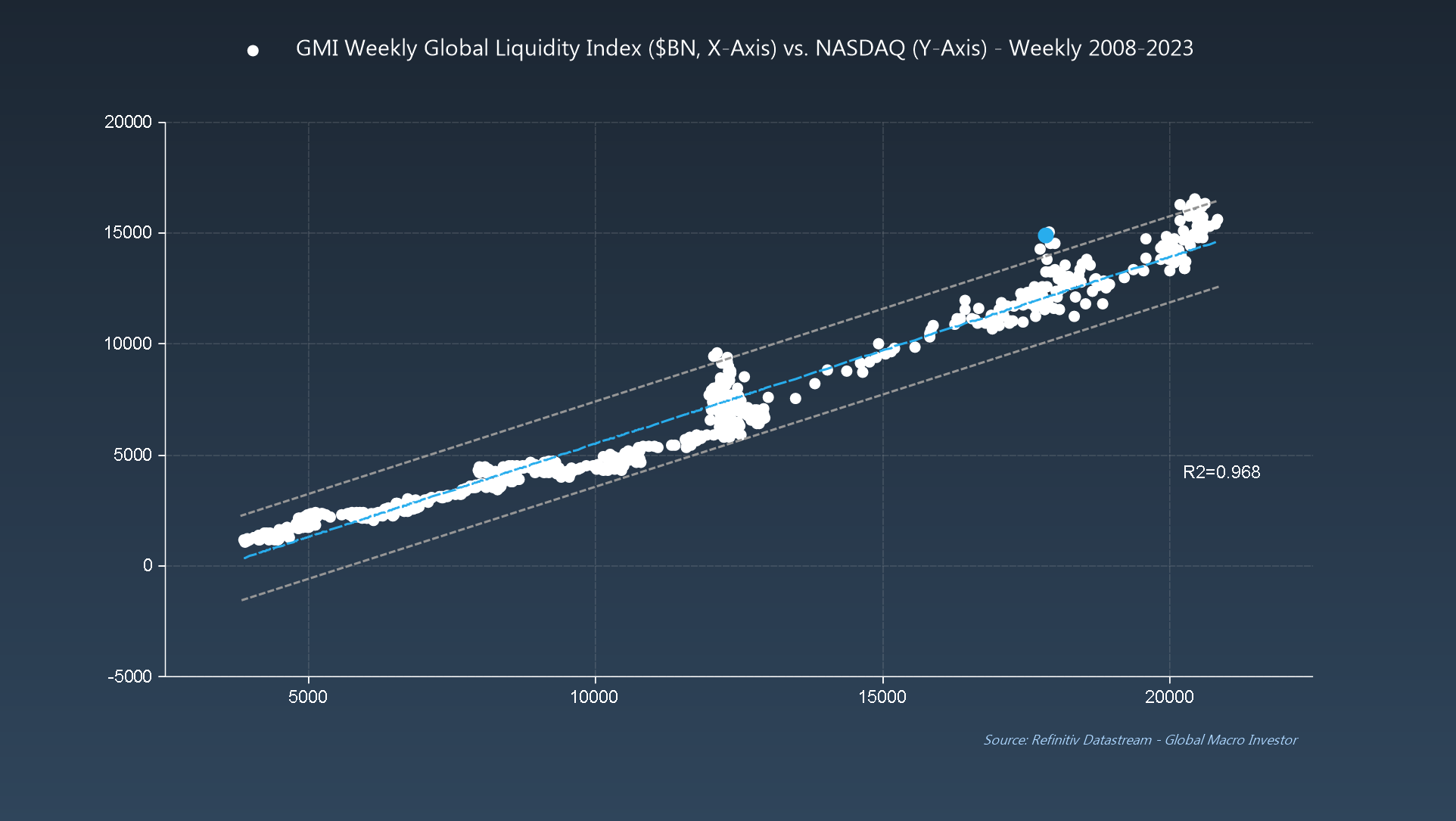

And speaking of liquidity, US domestic measures are positive even after the TGA rebuild. Of course, net liquidity can fall from here but we don’t think the Fed or the Treasury can afford to measures fall below key levels (e.g. $3T bank cash behind the $17T+ bank deposits).

As has been the norm, the Fed will be slow to act in response to the softening labor market with further rates hikes ironically accelerating the time to cut rates in the future should financial market stress ensue.

The other piece of the puzzle is inflation. US inflation is falling sharply (both headline and core). We have written extensively about the likelihood of strong disinflation (base effect) and a small probability of outright deflation.

And this is what the market (as forward-looking measures) is pricing in today.

NDX is now up 43.3% from its 2022 low vs. SPX at 24.4%.

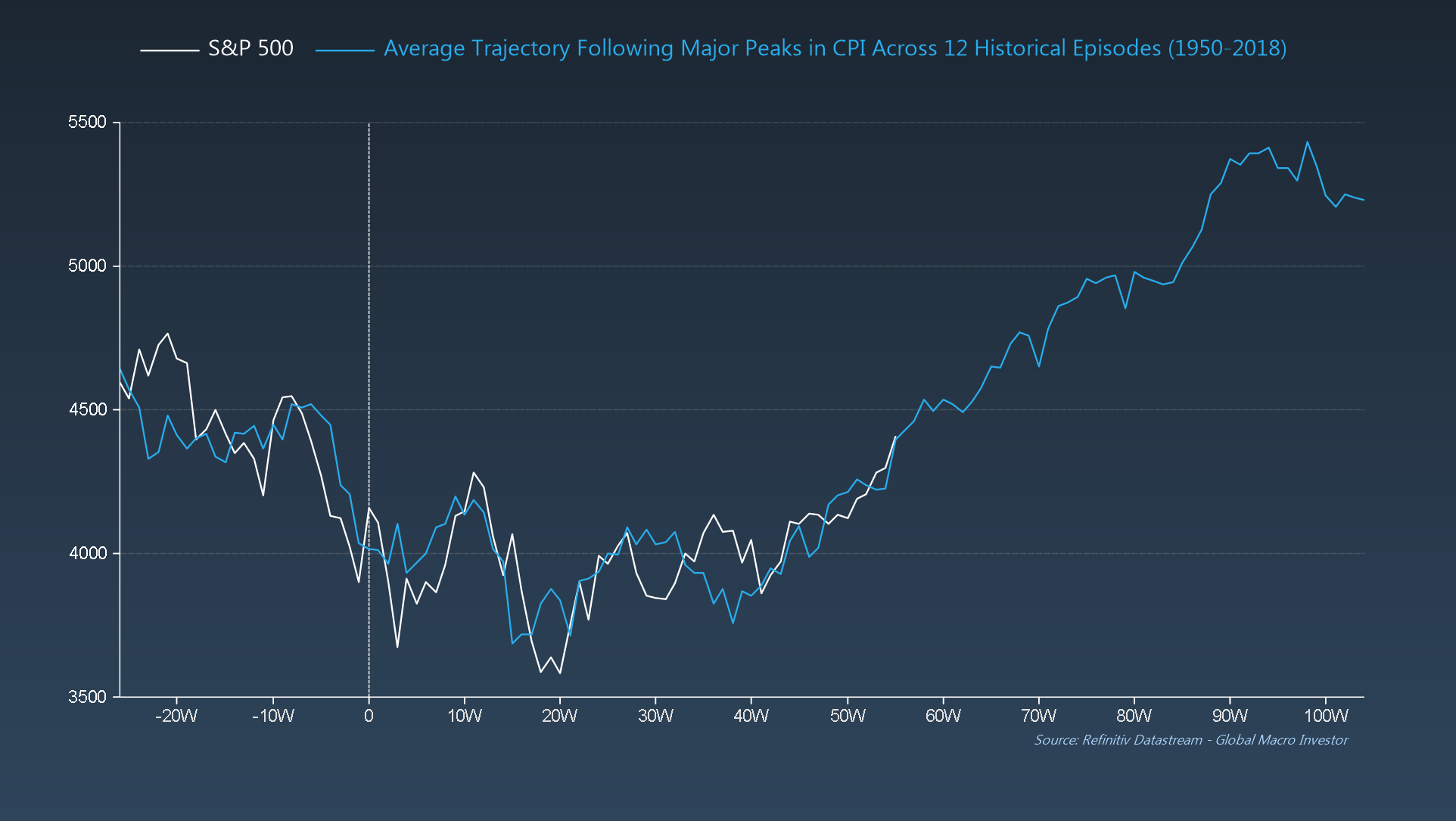

After all, it’s the rate of change that matters and the peak in CPI carved out the opportunity for equities to do well…

Near-term, equities may be in need of a correction with NDX being overbought relative to liquidity conditions globally. So although liquidity has improved, NDX may need to be pulled back a bit.

So when it comes to crypto vs. other risk assets like equities, crypto still has some catching up to do after NDX’s tumultuous 40% rally off the lows.

The idiosyncratic risks and headlines pertaining to the crypto markets have meant BTC has been discounted relative to NDX but without these discounts, BTC should be trading closer to $35k-$36k.

BTC also appeared to put in a local bottom to NDX on June 14th right on cue…

So to conclude, investors are reminded that things can turn on a dime. The SEC news didn’t lead to investors discounting the market more than with the collapse of FTX. The collapse in inflation, the rise in liquidity out of necessity, and the pricing in of a severe recession in Q4 2022 have paved the way for positive risk asset performance not without a near-term correction.

BTC strength seems to be unhindered for now but we will likely see pockets of outperformance elsewhere down the risk curve. However, it would be the approval of a BTC spot ETF or a $35k-$40k as the likely catalysts for the alt coin market to carve out its bottom. For now, its business as usual.

Decentral Park Market Pulse

Want real-time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

ICYMI: On Bitcoin’s Valuation

Global Market Cap

$1.14T; Rallied 17% off its June bottom with $900B acting as support. Resumption of the upwards trend within the channel with $1.17T as next resistance to break.

DeFi

$40.9B; A 20% gain from the June's bottom reaching 40B (200d MA) as resistance. As an alt sector, DeFi has a lack of institutional (regulatory) and retail buyers (higher prices needed for participation) as its current headwinds.

DeFi/ETH market cap ratio now using 18% as support-turned-resistance as the longer-standing, higher quality names get relative bid by investors.

Trader Positioning

BTC OI weighted funding rates remain positive (0.01) as BTC hovers above the $30k key level. Traders maintain their bullish stance overall.

Aggregate funding rates are more volatile for ETH compared to BTC but are currently positive at 0.0062. Traders may be less consistently bullish on ETH vs. BTC over the past week.

Pick up in IVs for BTC and ETH across the board over the past week. Higher IVs for longer tenors 90-180.

Grayscale Trusts

GBTC discount to NAV narrowed significantly following the filing of a BTC spot ETF application by BlackRock (30%).

One framing is to think about the discount as the probability of an unsuccessful redemption of GBTC close to NAV (whether Reg M or ETF conversion). Investors placed a 45% probability of investors not being able to redeem through a mechanism. Now that probability stands at 30% and BlackRock’s filing could change the game for Grayscale’s Lawsuit Against the SEC.

ETHE discount to NAV narrowing too (47%) but to a lesser degree than GBTC. This likely reflects the stronger likelihood of a GBTC ETF conversion than ETHE but investors may still price in some growing likelihood of an ETH spot conversion longer-term (once an ETH spot ETD is filed in the future).

CoinShares’ crypto fund flows shows last week saw $200m inflows - the largest weekly inflows since July 2022. BTC funds represent 94% of fund flows reflecting the stronger interest by investors compared to other assets including ETH.

BTC/USD Aggregate Order Books

Order books look slightly heavier on the bid side. Heavier resistance up to $31k.

Miners

Bitcoin hash has stalled briefly at 375m TH/s (30d MA) but overall uptrend looks intact.

Hashprice has collapsed as prices outpace resource commitment. Our prediction this year of a hashprice collapse since the top in January 2023 is playing out and supports miner capitulation as completed towards the end of Q4 2022.

Revenue from BRC-20-related activity for miners has become non-existent at just 0.1 BTC/day.

Bitcoin-related assets listed on EDX among top performers while BNB losing investor interest following the SEC charge against Binance:

Top 100 (7d %):

Bitcoin Cash (+80.3%)

Pepe (+66.2%)

Bitcoin SV (+46.3%)

Radix (+33.8%)

Kaspa (+33%)

Bottom Top 100 MCAPs (7d %):

Rocket Pool (-4.8%)

BNB (-2%)

Sui (-1.8%)

XRP (-1.6%)

Trust Wallet (-1.4%)

> Chris Rothfuss on Wyoming’s Blockchain Strategy & the WY Stable Token [On The Brink]

> The Chopping Block 510 [Unchained]

> Why the New Bitcoin ETF Proposal is Different [Stacks]

> How AI Will Change Web 3 Forever [Block Crunch]

> Trading Reflexive Markeets [1000x]

> ProShares' Bitcoin Futures ETF Racks Up Biggest Weekly Inflow in a Year [Coindesk]

> U.S. Has Room for a Compliant Crypto ETF to Grow Market Share as a Bitcoin On-Ramp: Bernstein [Coindesk]

> Crypto funding: Firms concentrated heavily in DeFi sector raise $50M [Blockworks]

> BlackRock touts the 'monumental' impact of tokenization, even if it arrives slowly [The Block]

> TradFi warming up to BTC [Jason Choi]

Key Decentral Park Links:

> Decentral Park Research Hub

> Decentral Park Market Pulse

> Decentral Park Website

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.