The Weekly #238

The cryptoasset market remains resilient but dollar strength weighs on prices. ETH gains relative momentum to BTC from narrative strength shifts.

Join the 1000’s founders, investors, crypto funds, brokerage firms, and developers in getting free cutting-edge crypto research by subscribing below:

Consolidation with an upwards bias

The cryptoasset market pulled back last week (-1.4%) in what seems to confirm our consolidation outlook for price. Global market capitalization stands at $1.098T today.

We can see the support and resistance slopes that are forming the wedge (higher lows, lower highs). We see $1.123T as the key resistance to break above and $1.052T as the key resistance to break below.

As a beta asset, we see the same set-up for BTC with $25.8k as being strong support…

The ongoing strength in the dollar has ensured rallies have been capped. DXY breaking into and above ~105 may signal a more prolonged period of dollar strength.

The currency remains 15% above its post-pandemic low but overall we see the end Fed rate increases as taking the wind out of the greenback’s sail.

Dollar bearishness is a crowded trade, however, and the transition period from a bull to a bear may be messy and frustrating. The implication likely is a more choppy upside bias for crypto.

On ETH vs. BTC

As we’ve mentioned over the past few weeks at Decentral Park, the key ratio to watch is ETH/BTC.

We noted that realized vol spread between BTC and ETH was signalling a significant move and seems to now be forming.

The last two times the spread was this low we had both bearish and bullish vol spikes. But the key thing here is we often see the direction of the move as realized vol spikes up from its multi-year lows.

The extent of the move so far is noteworthy. ETH/BTC has not only breached its 2023 resistance lines but has also now breached its 200d MA for 4 days - the longest time above the long-term momentum indicator since mid-January 2023.

Last week, we also noted the intense relative performance battle between BTC and ETH and attributed these two competing (and compelling) narratives on both sides.

One narrative on the Bitcoin side was the bet against US domestic bank instability. Bitcoin dominance and regional bank indices (e.g. KRE) have been effectively all one trade in 2023 - Dominance (white) climbs as KRE falls (orange; inverted).

Strong recovery in the regional bank stocks has reflected greater optimism by traders while others are pointing to Commercial Real Estate (CRE) as being the next shoe to drop for these smaller players. Therefore, we see Bitcoin dominance as remaining elevated relative to its 3-year lows but see the path of least resistance being lower over the next 6 months.

For Ethereum, one of the key narratives we highlighted was ‘sound money’, fueled by the net negative issuance of ETH.

The total circulating supply of ETH has fallen ~570k from its peak of 120.5m.

It seems compelling that ETH/BTC’s recent strength in its technicals comes at a time when ETH’s net negative supply has accelerated and is something we monitor.

Therefore, it seems you have a strengthening regional bank backdrop for Bitcoin while having a strengthening ‘sound money’ narrative backdrop for Ethereum.

The Broader Cryptoasset Market

For Alternative Layer 1 and Layer 2 blockchains, SOL continues to take the lead over the past month (-1.5%). OP has underperformed significantly (-28.8%) due to a 386m OP token unlock on May 31st.

SOL/USD trades at $21.6, continues to look constructive and is keeping above its 200d MA. We see the bottoming effect of the MA (which we are now seeing) as helping to put in $20 as the core support line for SOL.

On a relative basis to BTC, SOL is once again testing its 200d MA which has acted as clear resistance for the pair since Q1 2022.

Charting the distance from the 200d, something becomes much clearer. The ratio has been gravitating towards its 200d (despite the nominal slope downwards) since June 2022.

We will see if SOL can break above it for this test but overall we think the SOL/BTC bottom was put in 2023 EOY.

From the Micro to the Macro

What may get these alternative assets higher is the conducive macro environment. Let’s break down the latest.

Broader economic data in the US continues to point to a softening labour market. US jobless claims increased modestly last week with private employers hiring more workers than expected in May pointing to an overall tight labor market. Unemployment also rose to 3.7% in May.

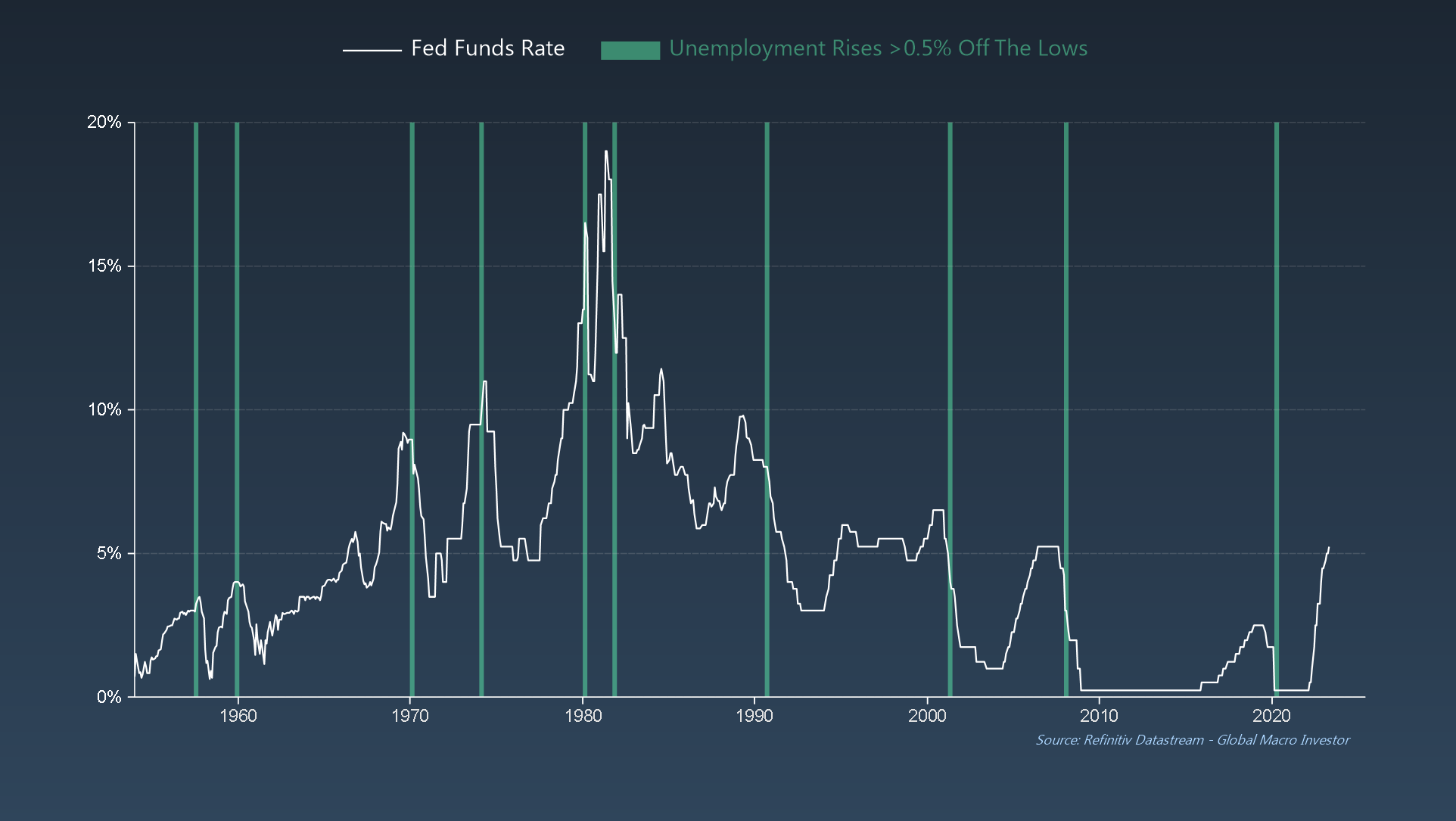

However, the trend and direction within the business cycle are what matters. Jobless claim spiking (orange; inverted) is what eventually leads to Fed fund rate cuts (blue).

Data from 1967 shows that Jobless claims lead unemployment figures off their lows. The Fed cuts rates before or during the unemployment rate rises above 0.5% from the lows.

The key headwind for risk assets nearer term is the potential negative liquidity growth due to the TGA rebuild. However, we see a significant rebuild with nominal rates at 5.25% as being unlikely with the Treasury and Fed likely resolving financial instability with more liquidity measures or workarounds.

Financial condition analysis points to global liquidity measures growing ~20% by Q4 2023. This lines up with our view that US domestic liquidity has a floor where fractures form in the financial system which become forcing functions for more accommodative central bank responses.

In our latest Bitcoin Valuation research report, we note the importance of Global Liquidity as being the slow but forceful director of BTC’s price action overall.

Spotlight: zkSync Era

Over the past few weeks, we have seen significant development focus and growth on a number of key headline metrics for zkSync Era.

After the launch of Optimism and the subsequent launch of Arbitrum in 2021, scaling networks have focused on optimistic rollups (fraud-proof-based designs). With the launch of zkSync Era, validity-proof designs have started to enter the arena promising to provide a more elegant solution for low-cost transactions.

zkSync daily active addresses are now starting to overtake Arbitrum and are on track to do the same with Solana.

zkEra’s TVL is still <10% that of Optimism’s and Arbitrum’s but its small growth marks an emerging trend. The dominance of validity-proof-based scaling networks growing over their fraud-proof counterparts.

The ongoing porting of applications (now standing at 58) including Rocket Pool and Storj over to ZKSync in the past week will only likely fuel this market dominance further over the coming months.

Decentral Park Market Pulse

Want real-time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

ICYMI: On Bitcoin’s Valuation

Global Market Cap

$1.01T; Consolidation price action. Markets are still within the upwards channel with the April-June resistance line forming a wedge. Support at $1.052T with ~$1.14T as being the next target to break.

DeFi

$42.7B; DeFi sector still chopping around its 200d MA. The sector has struggled to break above the $60B mark since May 2022.

Investors remain focused on higher-cap, high-quality names at the expense of the sector broadly. DeFi/ETH touched support last week after it broke the 21% level in late April.

Trader Positioning

BTC call OI for 30JUNE23 highest $35k ($240m) while the highest put OI between $22k to $27k. Net max pain $24k.

BTC OI weighted funding rate positive (0.009) with an overall weekly range of 0.003-0.01. Traders are taking a predominantly bullish stance overall.

BTC and ETH implied vols are collapsing across tenures providing traders an attractive period for cover shorts or enter long vol strategies.

Grayscale Trusts

GBTC premium narrows slightly to 41.6%. Key driver remains spot price action, especially around high vol periods.

ETHE discount is still much wider than GBTC’s at ~52.7%. We may see the delta between them narrow if ETH starts outperforming BTC over a positive period on their USD ratios.

Estimated revenue from GBTC and ETHE revenue likely coming in ~$40m in May.

Grayscale’s SOL trust, GSOL, saw a premium spike to 200% but is a highly illiquid asset (<$50k/daily volume) due to limited shares available on the secondary market.

More broadly, digital asset fund flow analysis shows a 7th consecutive week of net outflows. CoinShare’s believes this reflects profit-taking by investors rather than a structural downshift in sentiment for select assets.

BTC/USD Aggregate Order Books

Order books look heavier on the bid side. Heavier resistance up to $27k.

Miners

Bitcoin hash continues to climb higher with 30d MA climbing 46.3% YTD (367m TH/s).

Hashprice appears to have put in a lower peak and lines up with our view that hashprirce has started its cyclical downtrend after miners capitulated towards the end of Q4 2023.

Revenue from BRC-20-related activity for miners has collapsed to just ~2 BTC. Our outlook since early May was this climb in BRC-20-driven fees was just the latest craze in the playground and was likely to do little to impact miner top line sustainably.

We can identify potential drivers for best and worst-performing assets over the past week:

Top 100 (7d %):

XRP (+11.4%) - update on the Ripple vs. SEC case June 5th

The Sandbox (+11.1%) - Metaverse play prior to Apple announcing its VR headset

Lido DAO (+7.1%) - following the launch of V2

Decentraland (+7%) - metaverse play prior to Apple announcing its VR headset

Quant (+6.5%) - company involved in the development of CBDCs

Bottom Top 100 MCAPs (7d %):

Coinflux (-20.6%) - declines from recent rally related to Tencent Cloud news

Pepe (-18.8%) - meme coin traded out into alternative assets

Gate (-15.1%) - rumours of bankruptcy/insolvency issues

Sui (-14.1%) - token unlock

Optimism (-11.4%) - token unlock

> Will Modular Blockchains Win? [Unchained]

> Uniswap Fee Switch, Lido FUD, Endgame Craziness [Bell Curve]

> Exploring Nigeria’s payments landscape and CBDC eNaira’s adoption [The Fintech Blueprint]

> The State of ZK [Zero Knowledge]

> Bitcoin Prehistory and A Warren Buffett AI Bot [The Breakdown]

> Bitcoin Diminishing Marginal Returns [Coindesk]

> The latest on Rollups [0xguni]

> FTX Challenges Genesis’ Zero Debt Claim [Blockworks]

> zkSync Era Welcomes its First Liquid Staking Protocol [Blockworks]

> JPMorgan, 6 Indian Banks to Settle Dollar Trades on Onyx Blockchain System: Bloomberg [Coindesk]

Key Decentral Park Links:

> Decentral Park Research Hub

> Decentral Park Market Pulse

> Decentral Park Website

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.