The Weekly #235

Crypto bounces back as technicals suggest but resilience within the market is found most in Bitcoin.

Join the 1000’s founders, investors, crypto funds, brokerage firms, and developers in getting free cutting-edge crypto research by subscribing below:

Resuming the Momentum

Not much action occurred last week with markets rebounding 1.4% after declining 4.5% the week prior.

Global MCAP broke slightly below our $1.1T support formed since March 2023 but zooming out it’s clear the market is in an upwards-sloping range since January 2023.

The market hit the bottom of this range last week at $1.087T and we could now be looking at a more constructive period.

We are still above our 200d MA. We can also draw parallels to when the cryptoasset market broke its 200d MA in the past and looked for support upon corrections.

We often see an 11%-13% drift above the 200d MA which we are lower today. Given the range analysis, we take a more constructive view.

A move closer to this longer-term momentum indicator suggests a more intense battle by the bears is playing out. A break below it, and the bears will dictate price action for potentially a long time.

BTC broke out of its range to the downside only to return a few days later. We see $28.5k as the next target to reach.

When there’s less liquidity, price can swing aggressively in either direction.

ETH still can’t get anywhere relative to the orange coin, putting in lower highs so far in 2023.

Realized vol spread between the two assets suggests a big move may come in the coming days or weeks.

When the spread has been this low, the ensuing spike in vol has often been to the upside. Still, the 200d MA has been used as resistance to put out the rally so far in 2023.

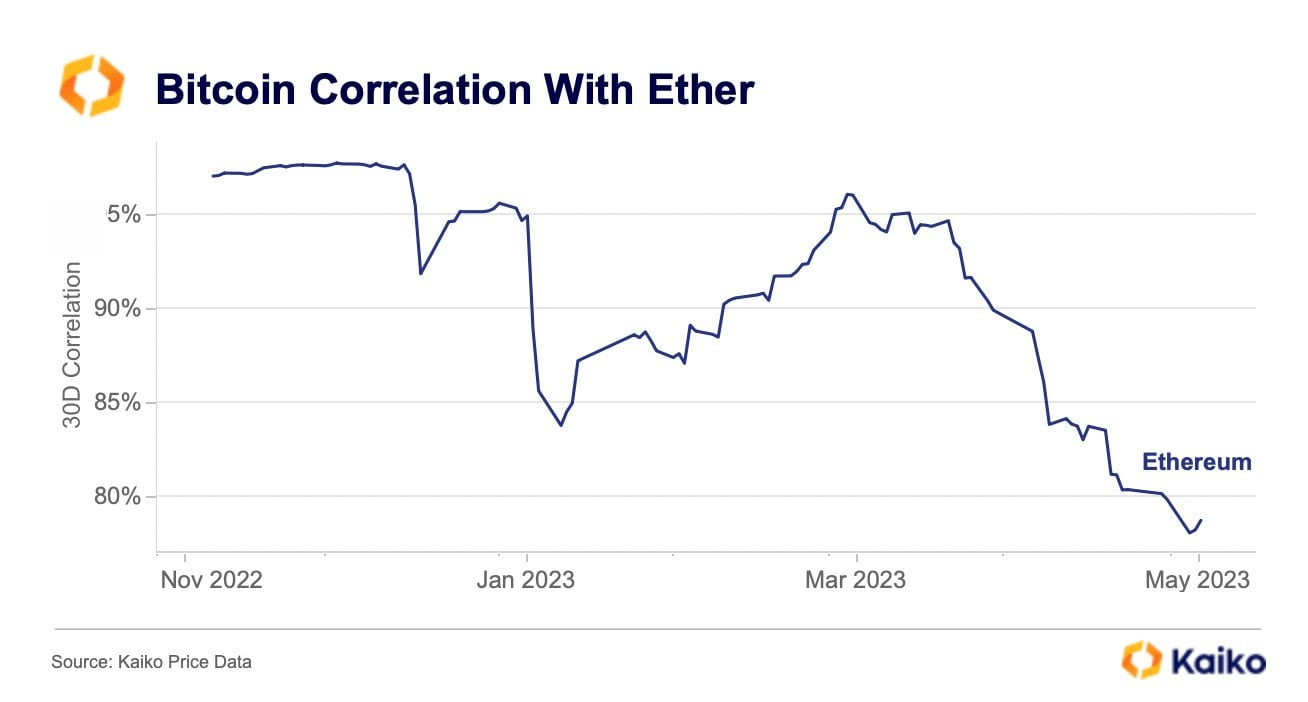

Bitcoin is becoming less correlated with Ether too with 30D now dipping below 80% for the first time in 18 months.

Bitcoin’s relative strength also comes as investors start thinking about positoning around the halvening. Although the event is known (it’s prescribed in the code), the playing the ‘event psychology’ remains a factor for investors.

The market has historically rallied either into (2nd halvening) the event or rallied and cooled off into (1st and 3rd halvening) into the event.

The DeFi sector remains unloved, unable to break out of its $40B market capitalization oscillation. For the bulls, this may be a good time to get constructive…

The problem, however, is the relative performance of the sector. DeFi dominance broke out of its downward-sloping range to reach new lows since January 2021.

Widening the basket and we can see this isn’t a DeFi-specific problem. Alt assets seeing any net inflows of capital. Worse, the slope appears to be getting steeper since Jan 2021.

So where are investors parking their capital at the expense of alts?

Bitcoin and Ethereum - but mostly Bitcoin.

Large-cap L1s are holding steady but yet not growing (yellow) which implies it’s the flight to quality, long-standing names that are receiving the most love. Not just the high-cap names.

We can look to the broader landscape to understand this flight to quality.

The regional banking crisis is still not over with nominal rates still at new cycle highs and inversion across different yield spreads continuing to create a negative interest income growth environment which hurts the smaller banks much more.

We see a continued approximate negative relationship between Bitcoin dominance and regional bank health where dominance remains elevated above 46-47% when the crisis for banks started gaining momentum (March 2023).

Short-term holders are remaining constructive. SOPR is now at the same level seen on March 10th when BTC started its move from $20.3 to $28k…

BRC-20s

Right now, Bitcoin miners are enjoying a surge in non-issuance fees due to the transactional activity related to BRC-20s. Over 14.3k tokens have now been minted with a combined market capitalization of $550B.

Positively, miners have seen their non-issuance fees surge to $17.5m/daily at a time when their income is coming under pressure in a competitive landscape as well as the 2024 Bitcoin halvening where issuance will be cut by 50%.

On the flip side, the Bitcoin mempool is now clogged with Bitcoin developers now contemplating labelling BRC-20s as ‘spam’.

The most important signal however is the reduction in fees paid to miners since the initial spike. Bitcoin users have been spending $35m in inscribing data onto sats and we see this as likely losing steam over the coming weeks by being the latest playground craze.

On Alternative Corners of the Market

Alternative L1s are fighting off Bitcoin strength with differing success.

NEAR/BTC has printed new lows since the summer of 2021 while SOL/BTC has found 0.0007643 as a sticking point.

Both ratios have been unable to break out above their 200d MA. SOL/BTC will have to decide by the next month which direction it wants to break out to.

Macro Signals

The macro signals also seem to be improving or more conducive to cryptoassets.

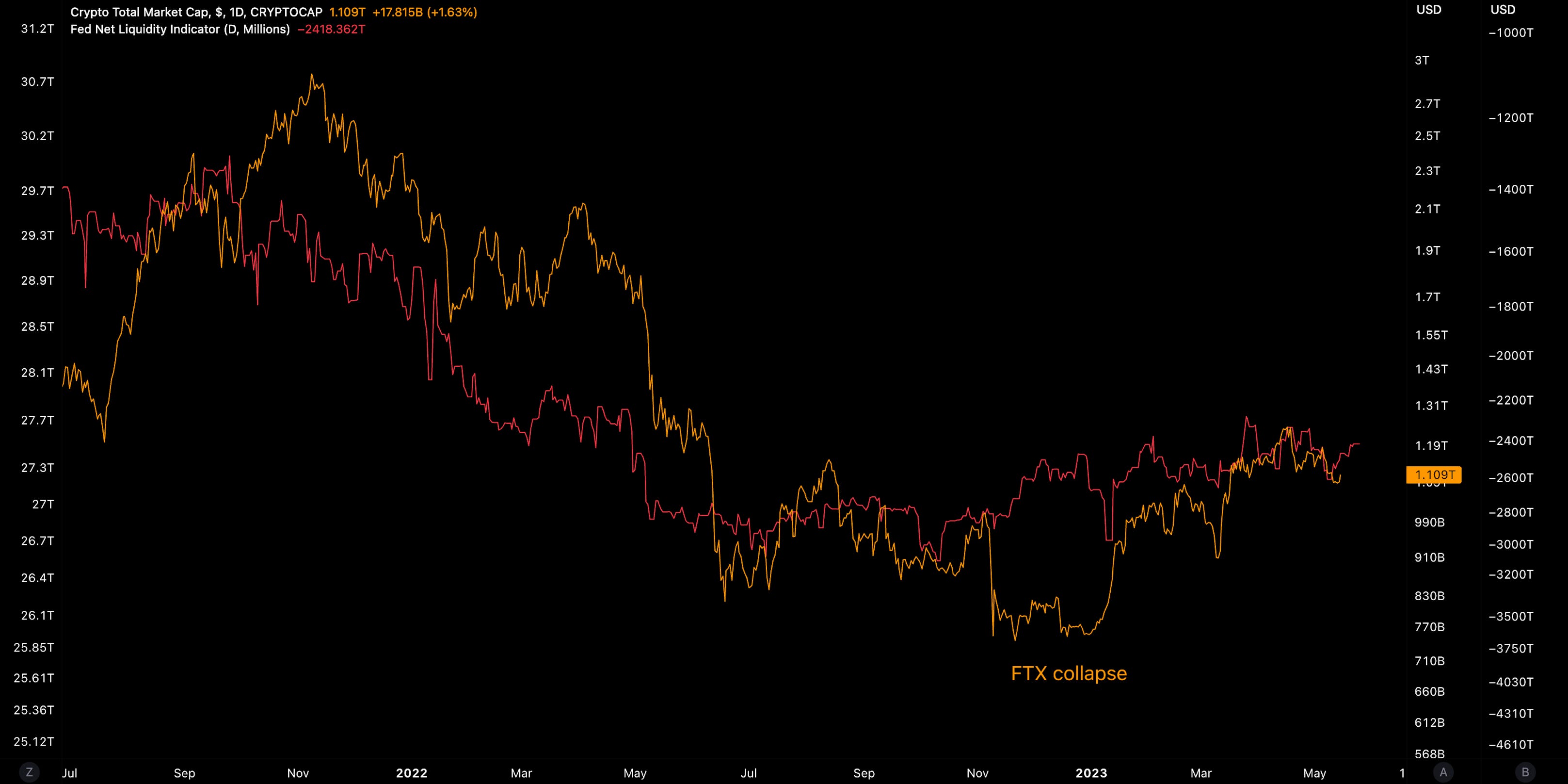

As we highlighted last week, Fed net liquidity has ticked higher for the next few days - aided by the Treasury drawing down from their TGA.

With the TGA shrinking to just $197B, the need to find a debt ceiling resolution within the month is critical for the US to avoid a national default.

Talks are improving and the issues on the table in the talks have narrowed.

When the debt ceiling is reached, liquidity is expected to fall as the running down of the TGA is stopped while quantitative tightening remains as is. Tighter liquidity will be a key headwind for cryptoassets.

When we look at raises in debt limits in the past, crypto has done well apart from the end of the 2021 market cycle (which doesn’t apply to now).

Crypto likely responds due to the market sniffing out the printing of more money in order to service that debt, which ultimately leads to capital inflows into more risky assets.

Of course, the problem here is the quantitative tightening - the Fed is no longer buying bonds. But this could be the very reason why an eventual flip to easing may be coming. A deflationary recession may be the most likely outcome this year that will force the hand of the Fed.

We’ve already started to see the signals of disinflation with US PPI coming in below consensus expectations in April (2.3% YoY vs. 2.5% exp.) and we may be looking at CPI heading towards 3-4% within the next few months. Disinflation is also seen for other countries, including Norway and Brazil.

For Italy, deflation is the story with PPI coming in -1% in March.

And it’s the nearing of the tightening cycle that matters here. The crypto market has only seen one tightening cycle before but we glean that markets bottomed prior to the terminal rate and reversed as the Fed Funds moved from its peak to lower levels.

Decentral Park Market Pulse

Want real-time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Revisiting Oracle Network Valuations

Thanks for reading Decentral Park Research! Subscribe for free to receive new posts and support my work. This article is an update on Oracle Network Valuations: The VSPT Ratio - first published on January 29th, 2022.

Global Market Cap

$1.107T; Rebound in the markets after finding support at $1.087T (upwards slope support). Still remains above 200d MA which is -11.7% below current levels.

DeFi MCAP

$43B; DeFi sector remains above 200d MA but may now be using 200w MA as resistance to break. Underperforming vs. higher cap names specifically beta names. Possible we see a bounce in dominance given range since early 2022.

Trader Positioning

We saw a full reset in BTC funding in the perpetual market on Monday with funding now slightly positive.

Short liquidations are now helping to drive spot higher just as longs were helping to drive prices down earlier in May.

Grayscale Trusts

GBTC discount to NAV widening to 40.85%. Discount has been intensifying in the last few sessions likely due to Grayscale launching a new trust - Grayscale Funds Trust while also filing a registration statement with the SEC for new ETFs including a ‘Global Bitcoin Composite ETF’.

Investors may be taking this as a signal of a weakening or long-standing battle that is unlikely to get resolution anytime soon. BTC moving lower from $30k also likely helped drive the widening given GBTC remains a high beta BTC play overall.

GBTC volumes (30D) are dropping to 3-year lows (2.398m) with little interest in the product by investors who do not want to take premium/discount risk on BTC.

ETHE’s discount to NAV also widening and is now at 53.23%. Same story as above with investors now possibly being able to trade an Ethereum futures ETF.

BTC/USD Aggregate Order Books

Order books look slightly heavier on the ask side. Heavier resistance up to $28k.

Miners

Bitcoin hash rate continues to edge higher once again (350m TH/s for 30d MA) with miners committing more resources to the network.

Bitcoin hashprice surges as hash rate outpaces BTC/USD but our bias is a rolling over of hashprice near current levels with the broader outlook being we are past the end of the miner capitulation cycle.

Miners have seen their non-issuance fees surge to $17.5m/daily due to on-chain activity relating to BRC-20s.

The highest-performing assets over the past week have largely been mid-cap names (34-90 MCAP ranked). Meme coin PEPE largest loser as fails to sustain its >$1b valuation.

Top 100 (7d %):

Kava (+40.6%)

Bitget Token (+22.7%)

Lido DAO (+22.5%)

Bitcoin SV (+16.9%)

Rocket Pool (+12.3%)

Bottom Top 100 MCAPs (7d %):

Pepe (-24.9%)

Klaytn (-19.1%)

Stacks (-17.1%)

WOO Network (-10.8%)

Radix (-9.2%)

> The Chopping Block: Do Aragon Association Members Get ‘Fat Salaries’ With ‘Zero Accountability’ [Unchained]

> Bullish on Crypto and AI [Real Vision]

> How to Value Crypto Tokens [Empire]

> Meme Mania [1000x]

> Building an $800m blockchain infrastructure company with Quicknode COO [The Fintech Blueprint]

> Ethereum staking queue [Marc Zeller]

> SEC Seeks to Slash $22M Fine on Crypto Firm LBRY to $111K [Coindesk]

> Going Full Bitcoiner: 1 Million Addresses Now Own 1 BTC or More [Blockworks]

> Diving into Sui [Messari]

> On Litecoin halvenings [Theiccythot]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.