The Weekly #232

Bitcoin breaches $30k as the orange coin leads the market once again heading into Ethereum's Shapella upgrade.

Join the 1000’s founders, investors, crypto funds, brokerage firms, and developers in getting free cutting-edge crypto research by subscribing below:

Investors Awaited Direction and They Got It

For several weeks now, we have highlighted the likelihood of crypto markets consolidating with breaches of key targets to the upside as confirming the resumption of the bullish momentum. We also highlighted the positive seasonality for the April month - both for crypto and risk assets in general.

The April-May 2019 Framework

It seems the above has played out right on cue with the crypto finally breaking the $1.15T on the global MCAP index after 26 days of battle.

This break could echo the April-May 2019 period when crypto tried to break above the 180B mark for 35 days before gaining 100% 49 days afterward (red).

With this move, BTC broke $30k to reach a high of $30.4k. We see the next real resistance at the $34k level (Jan-Feb 2022 support).

For ETH, a smaller gain to $1938 was put in with the next resistance at the $2040 level.

So what changed recently?

One potential driver was the warm reception of Web3 innovation in Hong Kong - specifically by its Finance chief, Paul Chan. Late on Sunday, Chan wrote in a blog post that despite crypto volatility, it is the “right time” to push Web3 adoption in the Chinese administrative region.

“In order for Web3 to steadily take the road of innovative development, we will adopt a strategy that emphasizes both ‘proper regulation’ and ‘promoting development,’” said Chan. “In terms of proper supervision, in addition to ensuring financial security and preventing systemic risks, we will also do a good job in investor education and protection, and anti-money laundering.”

This marks a stark contrast to the US crypto clampdown that had gained momentum in 2023 which has led many to reconsider who the net new buyers are for cryptoassets over the coming quarters. Therefore, the Hong Kong headlines are the counter signals the market may have been looking for all this time.

We can also see that other markets are unlikely to have acted as a catalyst either. NDX ended Monday -0.09% while precious metals like Gold printed a 0.81% decline.

The other angle is broader market liquidity. We highlighted the uptick in Fed net liquidity last week in our Market Pulse channel which has historically impacted crypto positively. The Fed’s QT efforts are being outpaced by the repo market and the TGA. It’s therefore some combination of higher liquidity (the enabler) and regulatory headlines (the catalyst).

Liquidity, liquidity, liquidity

As we’ve also mentioned before, the illiquidity of the market within crypto has helped exacerbate price action. In this case, thin order book depth has accentuated the price to the upside and it will be necessary for investors to monitor how liquidity measures evolve over time with potentially higher market values.

Net outflows of stablecoin supplies appear to be slowing down with USDC supply holding more steady at the 32B level.

Coming back to the April-May 2019 period that we could be re-enacting, investors will need to look for those overbought signals.

The market run-up to $390B market capitalization coincided with a bearish regular divergence on the weekly. Investors could also take note of the 200% price/MA ratio (200d MA) for that period although larger values have been printed. This is where each rally will need to be contextualized with the identified drivers.

One driver on the macro side is disinflation, especially in the US. March’s CPI released on Wednesday is expected to show a 5.2% slowdown from February’s 6% annual gain according to Bloomberg.

If realized this would mark the slowest annual increase in consumer prices since May 2021 despite still being above the Fed’s 2% target. Investors are now pricing in a 70% chance of a further 25 BPS rate hike despite ongoing signals that widespread recession is becoming ever more likely.

Lower rate hike expectations are now pulling the dollar down with anti-dollar assets like commodities, precious metals, and Bitcoin all likely to benefit.

Along these lines, the flight to quality continues in the crypto markets with BTC leading the charge once again.

After a brief pause, Bitcoin dominance edges higher towards 49% - the upper end of the resistance zone since May 2021.

We note the potential bearish divergence being set up where we become more cautious on further gains for the index.

That said, a clean break above the 49% mark, especially after a potential retrace, would signal a structural shift in the market. That too would be an important signal.

This is either the start of a broader capital rotation or the beginning of a new market regime - both are significant outcomes.

Shapella Is Coming at Prime Time

This comes as Ethereum is scheduled to undergo its Shapella upgrade - the combination of Shanghai (hard fork at the execution layer) and Capella (consensus layer upgrade).

The concern some investors have is the impact of unlocked ETH on the market especially when the market has become illiquid as we mention above. However, there will be restrictions on the withdrawal count per block (16 max).

Ethereum validators can queue up and exit now ahead of the upgrade itself in order to have their ETH ready to sell when unlocks happen. Over the past week, the net change of validators has been +925. If a long list of validators had the intention to exit, it’s likely that we would have seen this intention on-chain.

We are still seeing a good level of staking commitment with 120k ETH being staked daily. Liquid staking providers are also consistently seeing more inflows than CEXs with exchange risk appearing to be a concern for holders since the events in 2022.

A more favorable liquidity backdrop both outside and inside of crypto may also mean investors are more constructive.

Options markets indicate that traders may be hedging downside risk with more puts (vs. selling ETH spot) too.

The ETH/BTC ratio also shows how ETH wants to start catching up with BTC but can’t find the strength. The ratio rallied 7% between Monday-Wednesday before giving up all of the gains by the end of the week.

It may be that investors are being led by more pessimistic headlines about supply unlock headlines which are driving a sell-the-rumor, buy-the-news dynamic.

We still see a strong dip in buying at the 0.063 level.

Layer 1 blockchains are also gaining (slowly) over the past month relative to the broader market. Since March 20th, the select L1 market dominance index has gained 5% and will test key levels likely sometime in April or May.

The gain signifies some capital rotation at play but the magnitude is more muted than in previous bullish periods as the availability of liquidity is much lower than it once was.

The recent buyers of BTC may also be unwilling to give up their investments which are starting to provide the best absolute returns alongside attractive risk-adjusted returns.

This may not last though. SOL is now breaking its resistance to the upside. More broadly, longer-term investors are likely now paying attention to these high-cap names that remain 90%+ down from their ATHs.

For DeFi, the sector has received some love from investors but continues to lag the broader market. Sector market capitalization now diverges from market dominance marking a relationship that is rarely seen historically.

This is not your ordinary bull market dynamic - but nothing over the last 2 years has been ordinary.

Decentral Park Market Pulse

Want real-time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Global Market Cap

$1.12T; Broken through $1.15T resistance with technicals not yet suggesting overbought levels.

DeFi MCAP

$50B; DeFi sector remains above its 200d MA and potentially breaking out of wedge to the upside. Sector has lagged broader market with higher-cap names leading the market as a whole.

Trader Positioning

BTC OI weighted funding rate has climbed to new monthly highs (0.012) as traders add to their bullish bets.

BTC pushing over the $30k level caused heavy losses for shorts. Over 87% of all future trades were short with total notional liquidation loss being $145m.

Digital asset investment products saw $57m inflows last week, bringing flows back to a new inflow position YTD. Concentration of flows was Bitcoin-related (98%) while overall volume was low at $970m (25% of YTD average).

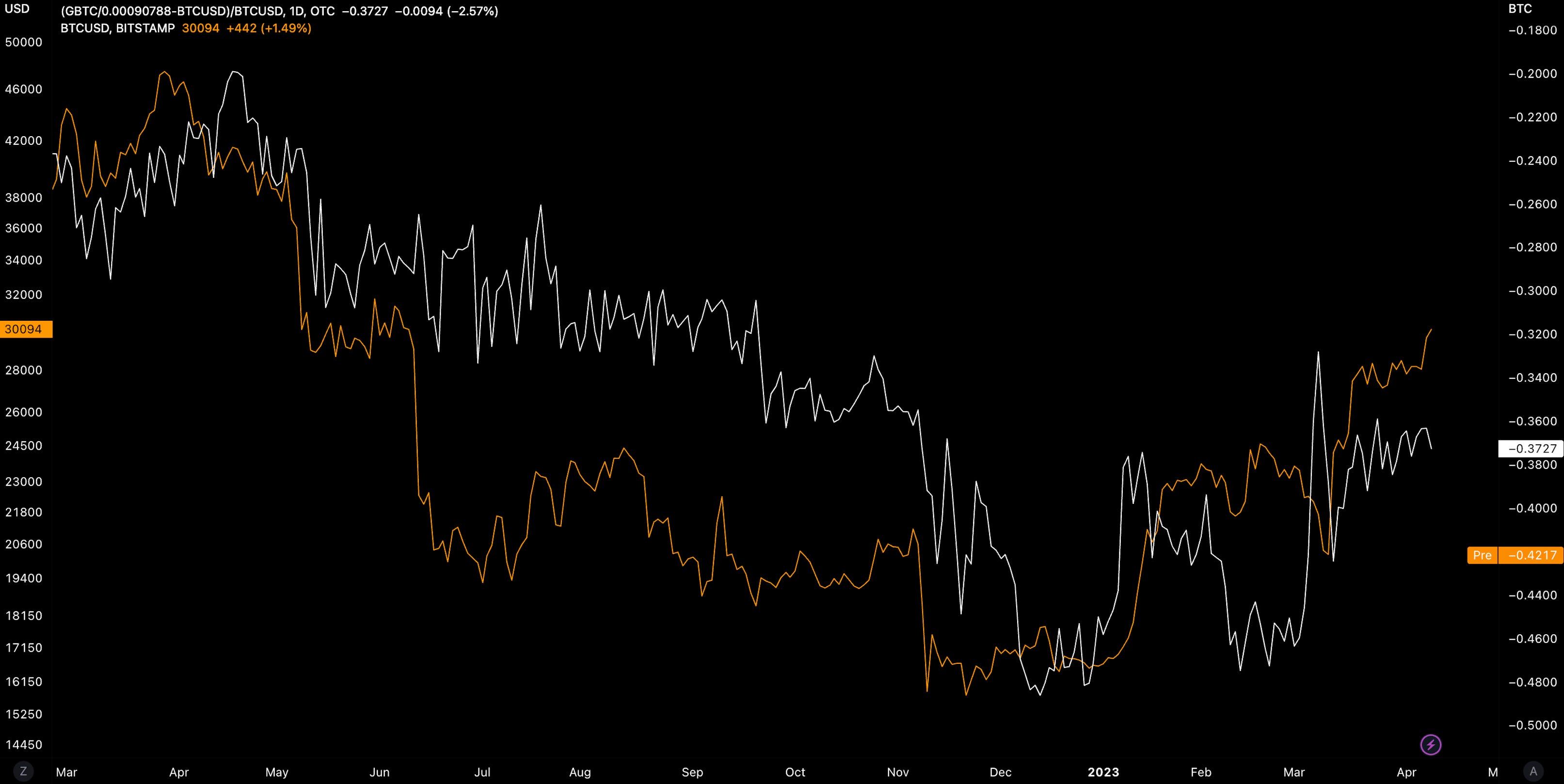

Grayscale Trusts

GBTC’s discount to NAV continues to steadily increase from its 48% with discount now standing at ~35%. The trust remains a high beta play on the underlying with the discount likely still being directed by spot moves.

ETHE discount to NAV is also narrowing following spot moves (47%). ETHE still lags GBTC in terms of nominal percentage discount by ~12%.

BTC/USD Aggregate Order Books

Order books look fairly even on the ask side with relatively heavier resistance up to $31k.

Miners

Bitcoin hash rate (7d, 30d MAs) continues to climb to new ATHs - 350 EH/s. The climb in resources has likely been driven by more machines coming online at a more profitable price level.

Miner revenue has climbed nearly 70% YTD with profits up 27% in the past month alone.

Bitcoin mining difficulty has increased to 47.89 T (all-time high). We now see confirmation of Bitcoin hash price falling and become more cautious as hashprice reaches the 325 level. This coincided with the local top in April-May 2019 after BTC broke through its consolidation range of ~$5.1k.

BTC has now breached firmly above its production cost. Previous breaks above this indicator after falling to its production cost floor (April-May 2019) is positive for medium-term direction.

Top performers over the past week have been broadly mid-cap names with $400m-$800m MCAP:

Top 100 (7d %):

Radix (+21%)

Render (+18.5%)

Coinflux (+17%)

Bitget Token (+14.8%)

Casper Network (+12.5%)

Bottom Top 100 MCAPs (7d %):

Dogecoin (-11.6%)

Kaspa (-4.6%)

Hedera (-2.2%)

LEO Token (-1.7%)

Stella (-1.4%)

> On Staking and the Ethereum Shanghai Upgrade [On The Brink]

> Leaving Web2 with Sriram Krishnan [Bankless]

> Hugh Henry on Markets [Bloomberg]

> Building a sovereign, privacy-first, programmable, economic infrastructure [The Fintech Blueprint]

> The Psychology of Entrepreneurship and Reimagining Collaboration Behind Web3 Analytics [The Fintech Blueprint]

> Blockchain Valuations [Lewis Harland]

> ROOK Token Surges Ahead of $50M Treasury Split Between Community and MEV Tech Builders [Coindesk]

> Adoption of Ordinals Analysis [The Defiant]

> Fed-issued CBDC Is a Hot Topic This Campaign Season [Blockworks]

> CBDC and Bitcoin [Chris Burniske]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.