The Weekly #231

ETH looks to regain ground against BTC as part of a broader capital rotation play with crypto likely benefiting off broader equity rallies heading into a historically bullish month.

Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting-edge crypto research by subscribing below:

A Strong Quarter, Strong April Seasonality

It was another week of consolidation in the crypto markets last week with the global MCAP index chopping around the $1.15T level. It appears we have formed a range between $1.12T and $1.18T.

MACD measures point to a more bearish outlook while RSIs (daily) are more neutral. BTC continues to chop at the $28.3k level while ETH hovers just above the $1.8k level. As Q1 comes to an end, Bitcoin ended up having its best quarter in 2 years.

Disinflation is a a friend for risk assets

One of the drivers of performance has been the positive sentiment that has boosted risk assets in general.

Key measures of US inflation helped buoy the mood with the Fed’s preferred inflation gauge rising 0.3% in Feb (excl. food/energy) - slightly below the median estimate. Investors read that as the central bank nearing the end of its rate-hiking campaign.

It’s the disinflation that is key and it’s the decline that should be positive for risk assets. The competing view is market bottoms occur 11 months after a recession starts and that the catalyst for why the Fed needs to cut rates has not yet been realized (i.e. inducing a mild recession).

As we’ve mentioned before, the ultimate question is to what extent have equities or, more importantly, crypto already priced in this outcome? Crypto bottomed before the Fed cut rates in the last tightening cycle but also put in a new local bottom in March 2020 (brief recession from COVID).

Tech stocks printed a weekly jump of 3.25% vs. crypto’s 0.43% gain.

We can point to some potential drivers of that delta with crypto currently facing its own set of internal challenges. We see the top 2 factors as being:

Regulation

Liquidity

Net outflows of stablecoins remain negative with stablecoin supplied falling 21% from their November 2021 highs

Zooming out on the NDX/Crypto chart, this relative outperformance of NDX is just a blip of a possible retreat in the index.

The month of April has also been historically good for risk assets going back to 2012. Seasonality is on crypto’s side.

This would also come at a time when the mid-Bitcoin halvening cycle ‘pull’ upwards usually starts based on the previous cycles. Others take a more cautious approach to halvening analysis arguing that patience will be needed before seeing any meaningful performance.

Short-term holders are also staying more constructive overall as we’ve highlighted before with measures like STH-SOPR…

The crypto market having low liquidity may also exacerbate price swings but it’s a double-edged sword. Traders may also be worried about the cost and slippage in a worsening liquidity environment.

The bid-ask spread can change during the trade fill due to insufficient order-book depth. This is particularly challenging for larger traders. The retreat in institutional liquidity providers and brokers following the collapse of 3AC and FTX has continued with the US operation choke point 2.0 only worsening the problem for market participants.

As we’ve mentioned in previous editions, one possible tailwind for altcoins is a Ripple win vs. the SEC.

XRP’s 43% jump in March reflects a market that believes a win is plausible with the outcome of the legal battle likely flavoring the appetite of lower cap names for investors over the coming months.

Capital Flows Down the Risk Curve?

This comes at a time when DeFi has been relatively neglected by investors over the past month. DeFi dominance fell to its strong support at 4% but is now gaining momentum to the upside right on cue.

The sector’s dominance may have another 14-15% until it sees the next resistance.

Bitcoin dominance is also at overstretched levels both on nominal levels and RSIs. A timely rotation down the risk continuum may be at play.

The ETH/BTC realized vol spread is also falling back to a multi-year low with volatility spikes for the ratio more likely to occur at these levels. The outcome of the Ripple case may very well be that volatility catalyst.

Another catalyst could be Ethereum’s Shanghai upgrade which will likely be implemented on April 12 although it’s likely the market has been pricing in a large part of the upgrade given it’s been on the calendars for some time. Shanghai will allow stakers to withdraw their staked coins (but not all at once).

Scaling is still a leading narrative for the market. Polygon's active user base continues to climb but the price has yet to respond. MATIC often catches up to these spikes in network usage.

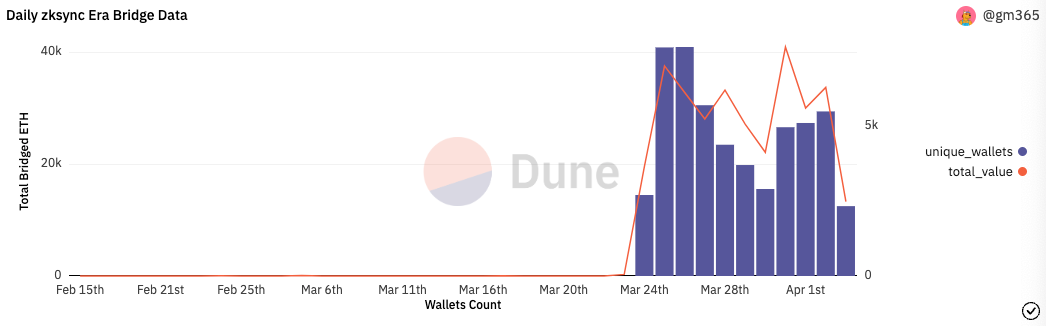

ZkSync Era is also coming in strong with 30k unique wallets being bridged from Ethereum. This comes as ZkSync became the first network to release its first zkEVM with a number of speculators likely looking to farm future ZKS tokens (launching in 1 year’s time).

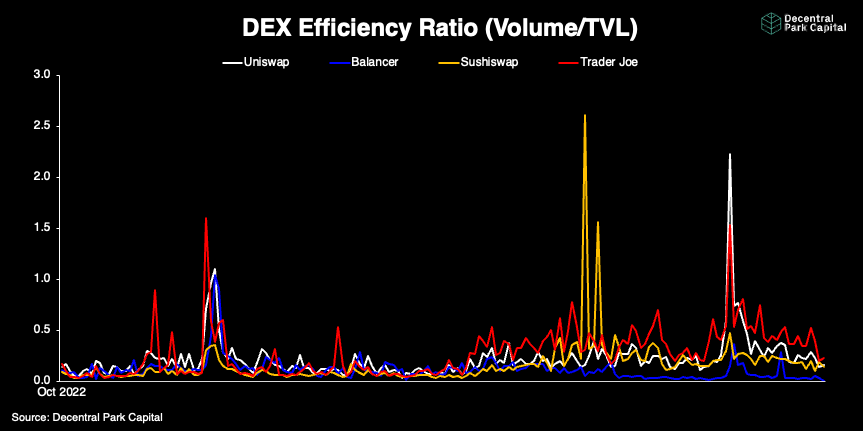

Another area of interest has been Decentralized exchanges. In particular, Trader Joe which has seen volume outpacing the growth of TVL and become more efficient than its peers including Uniswap.

The market soon began to price in this efficiency with JOE gaining 83% over the past 2 weeks.

Trader Joe’s has a series of V2.1 catalysts that were largely missed by the market which include upgrades like liquidity management automation, permissionless LB pools, and limit orders.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Global Market Cap

$1.146T; Weekly gain of 0.4% and testing key resistance. Possible range of $1.12T and $1.18T.

DeFi MCAP

$48.4B; DeFi sector remains above its 200d MA which appears to be acting as a good support zone for the sector. Technicals remain relatively neutral.

Trader Positioning

BTC OI weighted funding rate is slightly negative -0.00169 as traders become predominantly bearish which may be more constructive for price. Every negative funding rate period has preceded more constructive price action for BTC/USD as traders are reset in their position.

Ratio of long/shorts for BTC is also echoing the same reset pattern too…

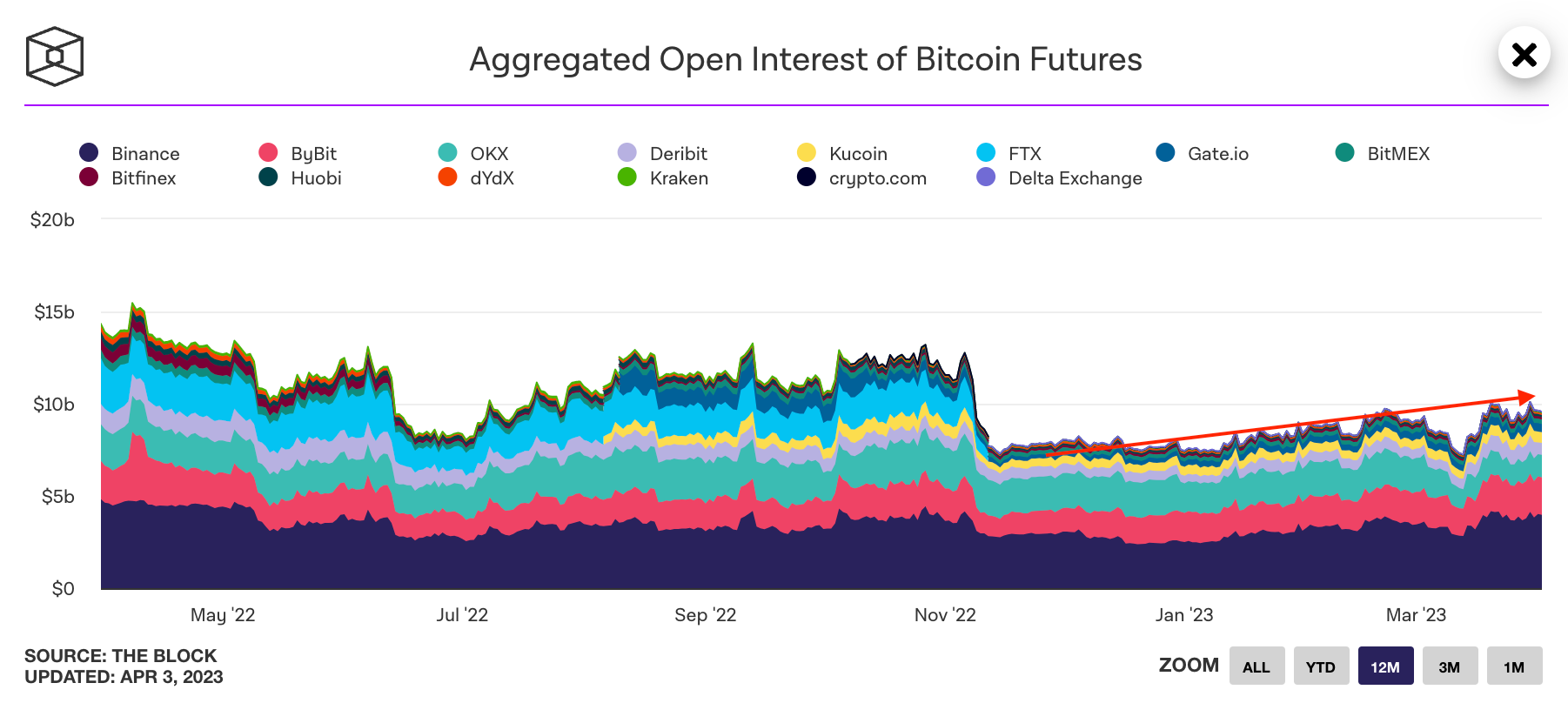

Aggregate futures OI has also been steadily increasing over the past 5 months and hovers just below the $10B mark.

Grayscale Trusts

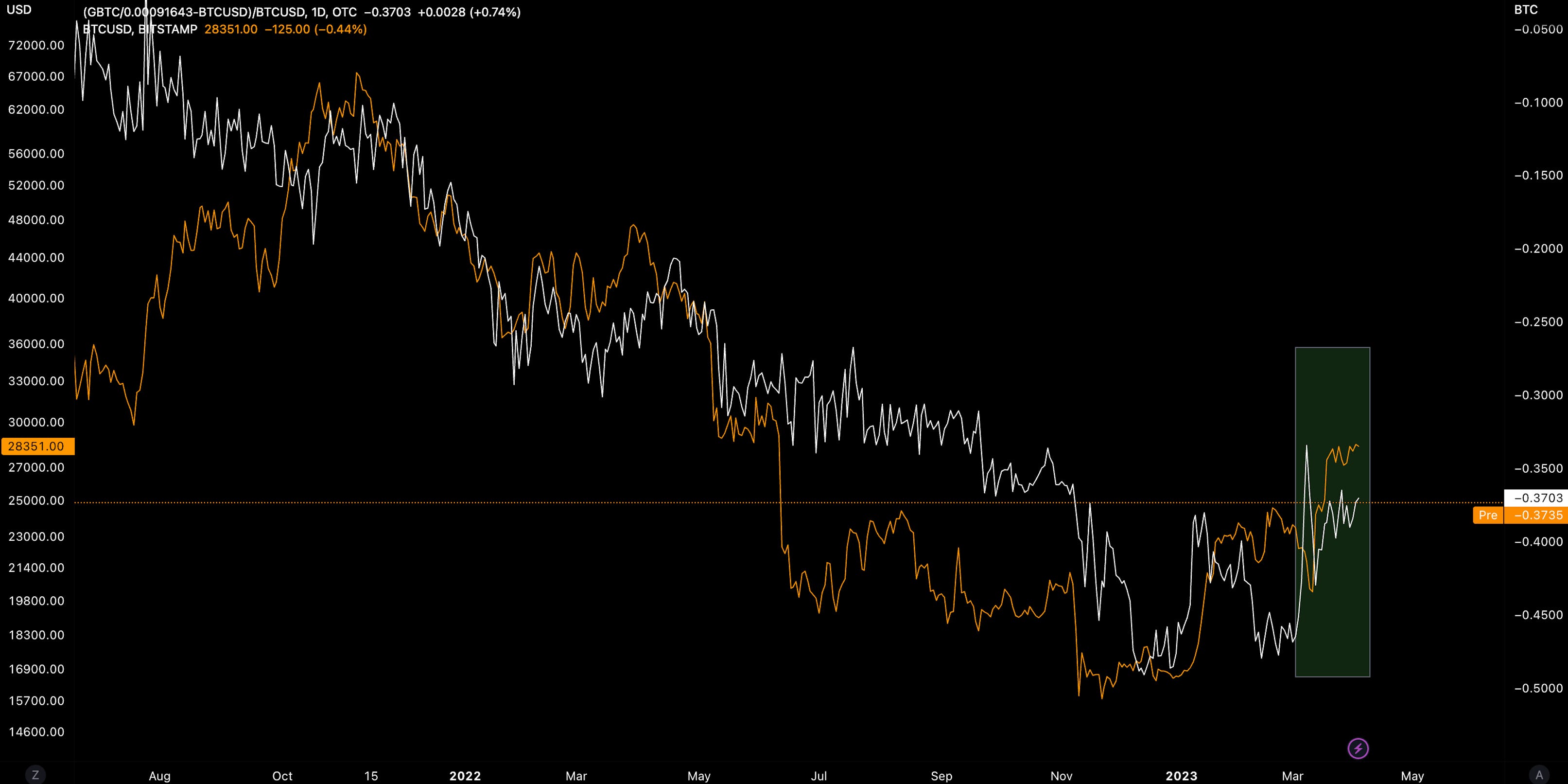

GBTC’s discount to NAV has been steadily increasing from its 48% floor and now printing in at 36.7%. The trust remains a high beta play on the underlying with the discount likely still being directed by spot moves.

ETHE discount to NAV is higher at 52% likely driven by a combination of 1) spot market dynamics (BTC outperformance vs. ETH) and 2) the market now considering the likelihood of a successful GBTC spot ETF transition.

BTC/USD Aggregate Order Books

Order books look heavier on the ask side with heavy resistance up to $30k.

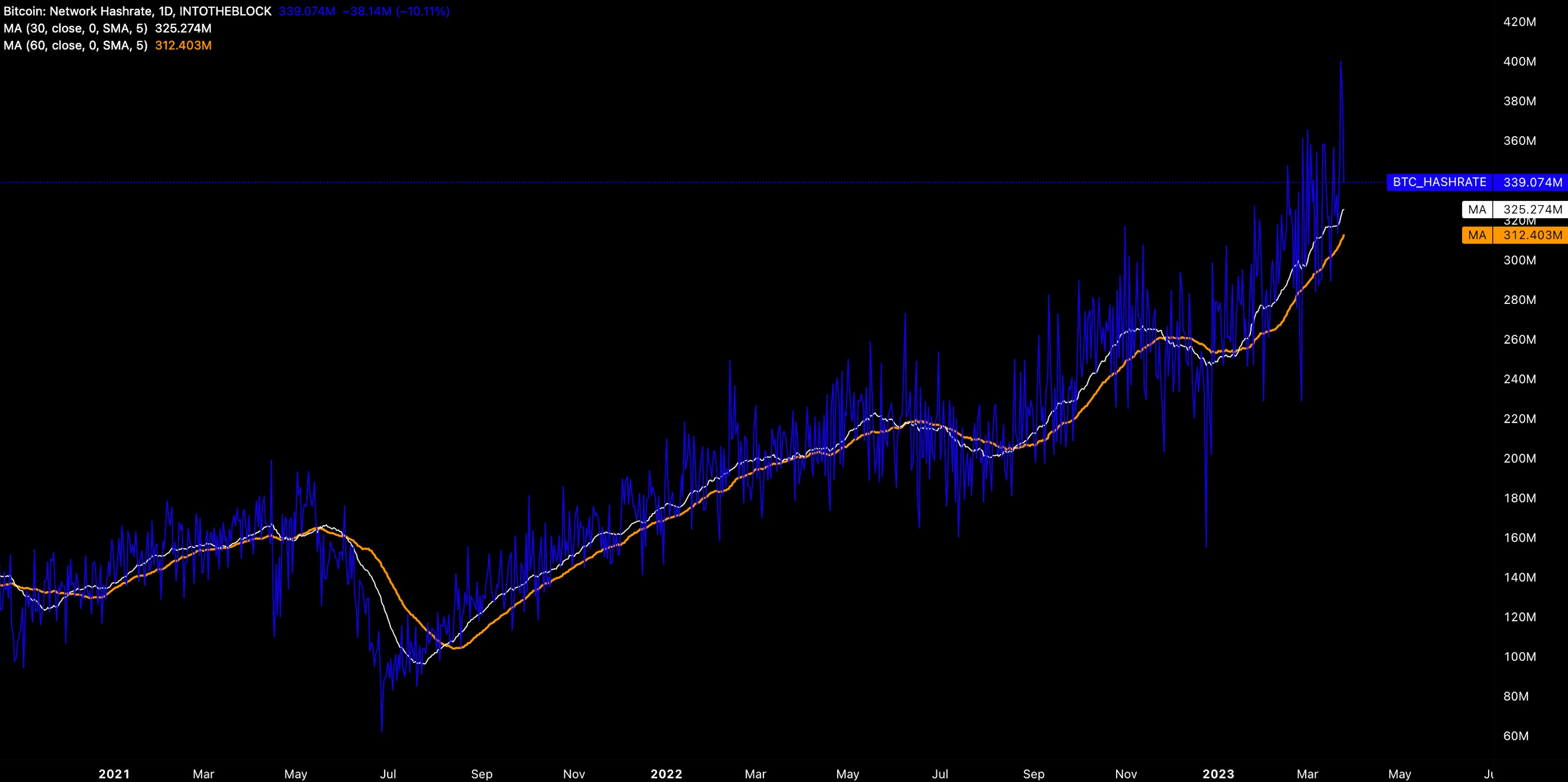

Miners

Bitcoin hash rate (7d, 30d MAs) continues to climb to new ATHs - 340 EH/s and up 36.7% YTD. The climb in resources has likely been driven by more machines coming online at a more profitable price level. New ASIC inventory was possibly sat idle at lower market prices.

The commitment by mining companies like Marathon and Riot means that the miner capitulation phase was finalized last year. Ratios like hash price peak in line with previous cycle bottoms with the ratio now trending down.

Core Scientific leads the pack for hash rate dominance controlling 16.7 EH/s (by Feb 2023).

Top performers have been dominated by longer-standing L1 blockchains. Stacks, the largest loser, maybe starting to stage a recovery after shredding 33% off its March highs ($1.31):

Top 100 (7d %):

SXP (+190%)

Kaspa (+114%)

Stellar (+18.3%)

Hedera (+16.6%)

Frax Share (+16.4%)

Bottom Top 100 MCAPs (7d %):

Stacks (-9%)

Mina Protocol (-8%)

SingularityNET (-7%)

KuCoin (-6%)

Arbitrum (-5.1%)

> What Can Be Done about Operation Choke Point 2.0 [On The Brink]

> Moody’s Head of DeFi Analytics unpacks the risks of stablecoins and CBDCs [The Scoop]

> A Wolf In Sheep’s Clothing [Bell Curve]

> Building a sovereign, privacy-first, programmable, economic infrastructure [The Fintech Blueprint]

> Be Careful What You Wish For [Thoughts on the Market]

> Arbitrum Foundation Pledges New Votes, No 'Near-Term" ARB Sales Amid Community Revolt [Coindesk]

> USDC's Depeg Laid Bare the Risks Traditional Finance Poses to Stablecoins [Coindesk]

> Tracking Unclaimed Airdrops For Arbitrum [Dune Analytics]

> Recession and market bottoms [@MacroAlf]

> Unpacking a major MEV event [Hudson Jameson]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.