The Weekly #180

Liquidations lead soft crypto markets to tumble further. DeFi dominance climbs to new ATH as fundamentals drive protocol value in several cases.

Hard Pill To Swallow In A Soft Market

We’ve seen a 13% fall in the crypto market over the past week as interest from investors continue to wane. BTC failed to break above $48k while ETH couldn’t find the momentum to get above $4k.

Cryptoassets have, generally speaking, fallen from their 2021 peaks by the same degree:

Crypto MCAP: -35%

BTC: -40%

ETH: -36%

Where we stand now is a slow moving market with oversold assets as indicated by daily RSIs now hovering at 40 or below across the board.

We are not out of the woods though. BTC’s 50-day exponential moving average is on track to cross below its 200d moving average (death cross) and could signal further bearish momentum ahead.

There may be merit to this thinking too. BTC fell a further 28% in June 2021 over 36 days before reversing course to $53k.

We don’t have to look far to see how interest had plummeted. Global exchange volumes fell further to reach all-time-lows since summer 2021.

Note, on-chain metrics like Bitcoin’s STH-MVRV also signalled bearish price action (see Weekly edition #179).

Liquidations Go Brrr.

The risk here is the development of a soft spot market relative to growing interest in the futures market. Specifically, long liquidations coming in force creating a cascading effect on cryptoasset prices.

Last Thursday, BTC broke the $43k resistance leading to nearly $800m total long liquidations occurring over 200k positions. We can see that the total liquidation amount was less than 50% of the levels seen in early December 2021.

One reason is the reduction in open interest (OI) within the futures market compared to that period which stood near all-time-highs of 400k BTC as we can see in the below graph.

However, comparing the overall trend in OI with futures volume we could also see the problem emerging since October 2021 - Futures volume fell ~50% while OI increased 66% in BTC terms.

As highlighted in last week’s Weekly:

“Reduced futures volumes against rising OI from here can favour a localized leverage squeeze so it will be important to pay attention to these metrics over the coming days/weeks.”

Driving Macro Forces

Only a few days into the new year and the Fed have ignited strong reactions from investors globally. After minutes of December FOMC meeting were released on Wednesday, it became clear the Fed were increasingly concerned they were behind the curve in fighting inflation. Two key things to note:

Rates could be increased as early as March

Begin to reduce balance sheet (quantitative tightening)

Just this week, Goldman has adjusted its 2022 rate hike prediction from 3 to 4.

Many will be watching how inflation subsides over the coming quarters. With CPI forecasts for December expected to rise 5.4% annually, hotter-than-expected inflation will only confirm expectations of aggressive tightening from the Fed.

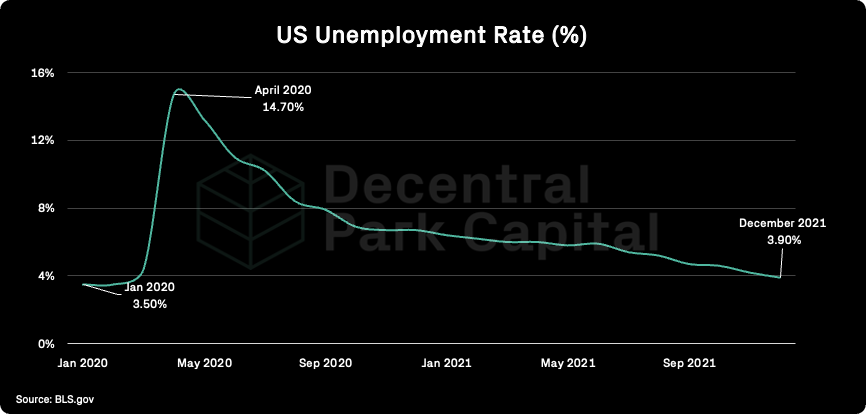

This is also true of US unemployment rate which has fallen to pre-Covid pandemic levels (~3.9%) which the Fed will see as a very positive sign to scale back.

Cryptoassets which are positioning at the furthest end of the risk curve face potential headwinds from this dynamic as investor look to risk-off assets. Equally, what matters is the period after long Fed hikes where recessions typically occur.

Even in the equity markets, investors will be looking for those that demonstrate good profitability in a raised-rate environment. It is reasonable to use a similar framework for protocols heading into 2022 and beyond.

This is especially the case for DeFi - a sector is now printing new highs in dominance against overall market weakness.

Protocol fundamentals will become increasingly important for ‘legacy’ equity investors analyzing protocols and their financials over the coming years. The ‘institutionalization’ of DeFi and Web3 will likely cement this even more.

In the next section, we show just 3 examples protocols where we believe fundamentals have enabled the respective cryptoassets to buck the wider market trend.

Pocket Network

Pocket Network is a blockchain data ecosystem for Web3 applications - your decentralized Infura.

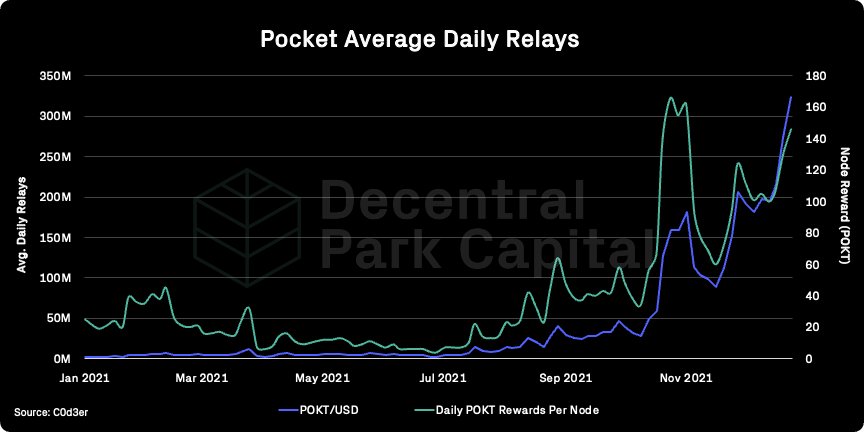

Relays (API requests) serviced by nodes to applications is hitting all-time-highs (>300m). This is directly translating to substantial daily yield from protocol revenue (1%+) for service nodes. Monthly revenue for Pocket passed $30m for December.

We can also see a clear positive relationship between average daily relays on Pocket and the average OTC price of POKT since September 2021.

FRAX Share

Increased regulatory clampdown on centralized stablecoins has paved the way algo stablecoin monetary expansion.

One valuation mental model for Frax Share is its fully-diluted value relative to the monetary supply (MS) it governs. Since November, FRAX’s MS surged by 1.3B units (~$1.3B). Frax Share has historically used the MS as a price floor.

FXS is up 95% since December and trading at a nearly a 2x premium to its MS.

Convex Finance

The Curve staking protocol has seen cumulative revenue pass $400m. Forecasted annualized revenue for the month of January is over $2B and the largest holder of the CRV token.

Becomes more reflexive as more users join and stake their CRV through the Convex. CVX is up 85% since the start of December 2021.

Top performing assets are centred more around Ethereum DeFi. Note - DeFi top performers have been the global top performers.

Global (7d%):

Dopex Rebate Token (+103%)

GMX (+28%)

Chainlink (+22%)

Tokemak (+19%)

Osmosis (+18%)

DeFi (7d%):

Dopex Rebate Token (+103%)

GMX (+28%)

Chainlink (+22%)

Tokemak (+19%)

Osmosis (+18%)

Votium.app bribes to veCVX holders are coming to an average of $0.70 per locked CVX, making bribing APY around 50%. In order to be eligible holders need to lock CVX for 16 weeks and delegate voting to Votium.

Pika Protocol, perpetual swap on Optimism, is launching a new version. Vault fund lock time is reduced from 7 days to 1 day, fee rewards can be collected separately apart from deposits and token is hinted. Vault APY exceeds to 100% since launch.

Futureswap, perpetual swap on Arbitrum, updated their incentive program. Trading, open interest, and liquidity provision are rewarded with FST. Learn more here.

Tokemak launched MIM reactor, LPs can deposit MIM for 25% and TOKE for 17%.

Enforcement by regulation is expected to be the thorny theme of 2022. In the US, the SEC and CFTC are moving quickly to carve out authority as part of a competitive agency land grab under the Biden administration. Ethereum site Polymarket hit with $1.4M fine: CFTC (Decrypt).

The crypto lobby continues to garner strength and reach with governments, ramping up lobbying efforts in the new year after several incumbents (Ripply, a16z, FTX) proffered proposed regulatory frameworks. Dapper Labs becomes the first NFT company to register to lobby with the US government (Cointelegraph).

Crypto regulation concerns make decentralized stablecoins attractive to DeFi investors (Cointelegraph).

Global market cap: $2.07T; Global market cap has fallen 13% over the past week.

DeFi: $140B; DeFi market cap has fallen by 10% - slightly less than the wider market. DeFi dominance at new all-time-high of 6.7%.

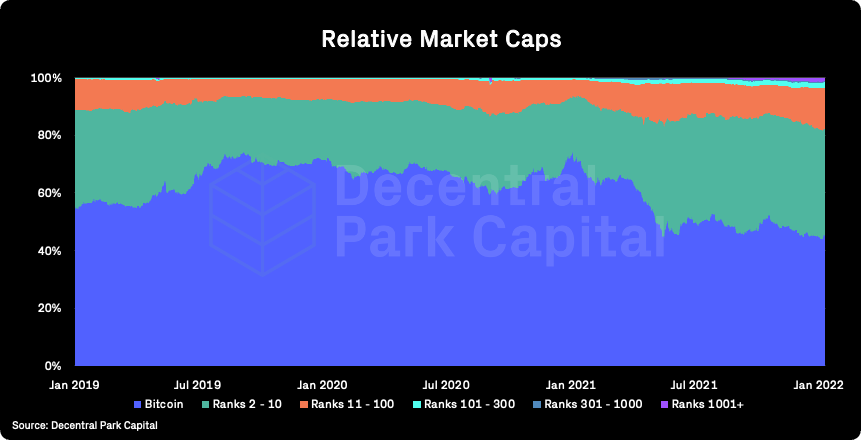

Market shares; Bitcoin dominance increased slightly over the past week (44%) as high and mid-cap name performance bleed out more in aggregate relative to the orange coin.

BTC/USD and ETH/USD (D)

ETH/BTC (D)

Price action; BTC and ETH support found at $40.5k and $3k respectively. ETH show relative weakness to BTC potentially oversold and indicated by all daily RSIs prints.

Volatility (BTC & ETH); BTC and ETH 30D vol continues to follow on overall declining trend. 3-month implied volatility for ETH are falling to yearly lows.

Combined order books; Order books much heavier on the bid side. Heavier resistance up to $42.1k (Source: Bitcoinity).

Crypto vs. SPX; Crypto market’s correlation to equities is increasing as both tumble after the Fed’s December FOMC minutes release.

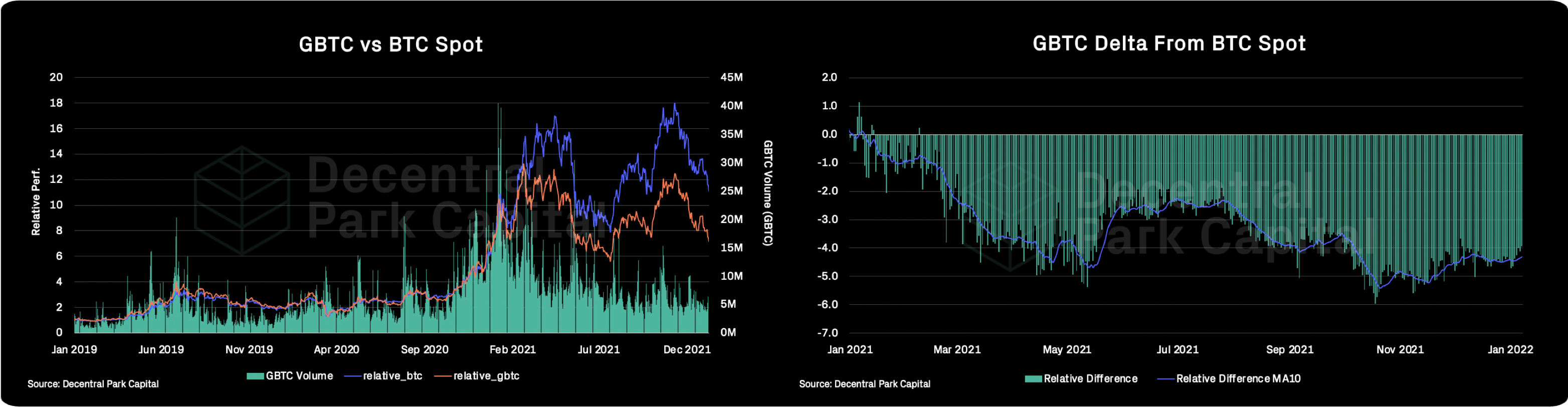

GBTC premium; GBTC discount at an all-time-high (21.3%). 30D volumes still showing month-on-month decline indicating overall limited demand on secondary market for GBTC.

ETHE premium; ETHE discount at all-time-low (13%). ETHE volumes also showing month-on-month declines.

Bitcoin Mempool activity (Size in MB); The mempool size remains low since last week indicating a relatively low network congestion.

On-chain real (BTC) & off-chain volume; BTC on-chain volume has kept flat over the past week. BTC and ETH spot volumes (7d MA) have increased 15% and 41% respectively for the same period.

Hashrate & Difficulty; Bitcoin hashrate slightly below all-time-high levels. Bitcoin has fully recovered from its 50%+ drop in hashing power driven by the Chinese mining ban. Difficulty adjustment increased 0.4%.

Active addresses (BTC); Active addresses (30d MA) has fallen 2% over the past week.

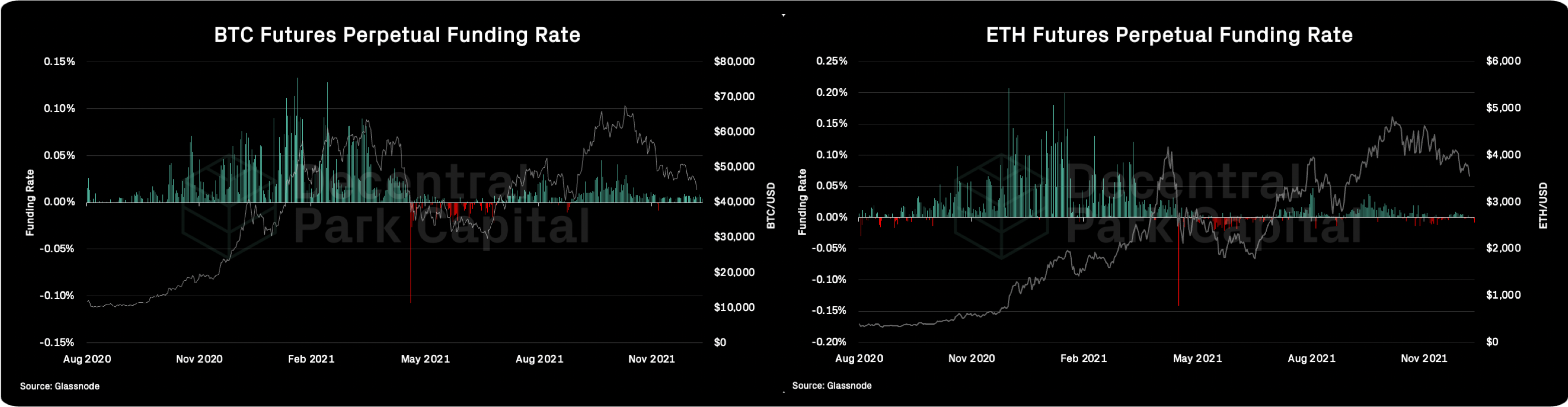

Trader positioning; Funding rates remain moderately positive for BTC while flipped negative for ETH. Open interest still up 24% since December despite 18% decline in BTC/USD over the same period.

Omenics Sentscore (BTC); Sentiment around BTC has fallen to all-time-lows since June 2021.

Exchange inflow/outflow (BTC, ETH); Exchanges seeing ~$400m in net exchange flows for BTC and $1.4B for ETH. Largest net inflows volumes historically and points to investor capitulation.

USD-Pegged Stablecoin Flow; Continuation of net outflows for USD-pegged stablecoins pointing to potentially limited opportunistic buying by investors at current price levels.

📚 On Market Conviction [@FloodCapital]

📚 DAOJones Options [@ZoomerOracle]

📚 Asset Management Protocols on Solana [@PsyOptions]

📚 Maelstrom [@Arthur Hayes]

📚 Game Theory Behind Curve And Convex [@TheBlock]

🎙️ Advice To Entering The Industry [FTX Podcast]

🎙️ Token Sales [The Metaverse Podcast]

🎙️ Outlook on Industry [Between2Chains]

🎙️ Tom Emmer on MMT, CBDCs and Crypto Policy For 2022 [On The Brink]

🎙️ Welcome to 2022 - The Year of Absolutely Everything [The Breakdown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.