The Weekly #179

The Weekly #179

Markets continue to show consolidation patterns overall while DeFi assets shine brightly.

A Slow Start To 2022?

A Very Happy New Year!

Crypto markets start the year in a relatively calm mood with the global market cap up 2% for the week. Bitcoin has kept range-bound since December between $52k and $45.5k.

Data points continue to highlight soft market dynamics. Global daily exchange volume has fallen 50% since the start of November despite the range-bound price action, approaching 6-month lows ($26.1B).

Declines in volume is not unique to any single asset. Exchange volumes are hitting all-time-lows since July 2021 and March 2021 for Bitcoin and Ethereum respectively.

This points to more general muted interest by investors who are returning from the holidays but equally contrasts the exuberant dynamics seen at the start of 2021 across the market.

A driving factor in crypto has oftentimes been the macro piece with crypto being traded as a risk-on market. However, we’ve seen a divergence between them in the run up to year end (crypto weakness against flat/up stocks).

The $6.1B options expiry at year end was balanced between bears and bulls bringing little change to the price structure around the event, failing to sustain the 3% rally medium-term.

Other analysts are pointing to technical bearish indicators short-term (e.g. ETH) which mirror Bitcoin’s rally to $64k and $69k tops. Namely, long consolidating price action after breaking above two highs.

Key On-Chain Indicators

On-chain indicators like STH-MVRV paint a similar picture. Bitcoin’s STH-MVRV has kept below 1 which has historically coincided with prolonged bearish periods/poor demand dynamics. The 1-line has often worked as a resistance/support line and breaking through has been a good indicator for market reversals.

For Ethereum, we have now seen ~400k ETH of net inflows to exchanges since the start of December. Bitcoin remains net negative. Increased supply to exchanges may indicate investors offloading positions and can add significant sell pressure in the immediate term.

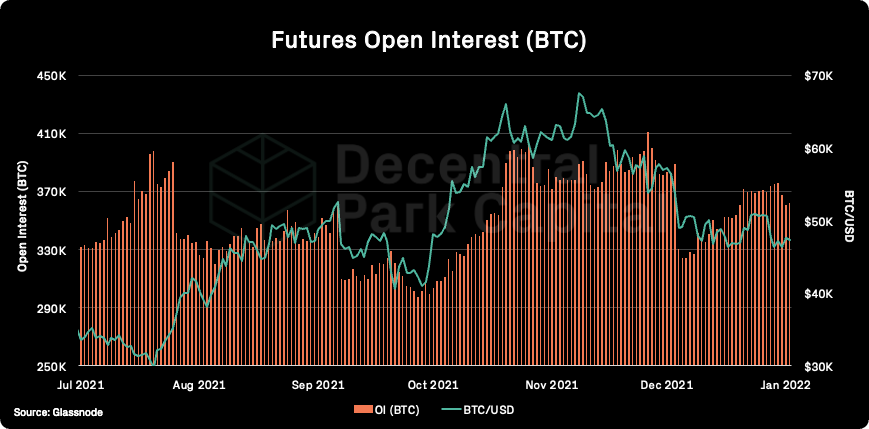

Futures

In the futures market, the risk of leverage for long and short squeezes is reduced in the immediate term. Bitcoin denominated OI has fallen 3% (362k) and is ~50k BTC off its highs. Futures volumes is also becoming thinner, falling nearly 50% since December 2021.

Very slight positive funding rates persist across the board which arguably indicates more neutral sentiment in the markets.

Reduced futures volumes against rising OI from here can favour a localized leverage squeeze so it will be important to pay attention to these metrics over the coming days/weeks.

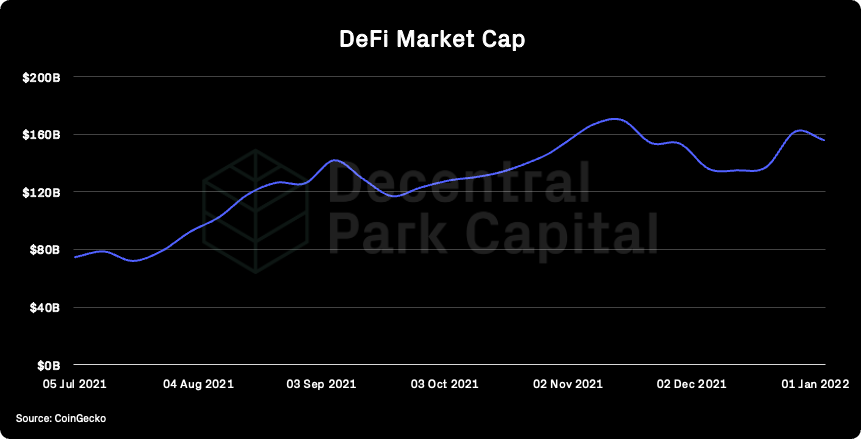

DeFi

While wider market sentiment appears more neutral, one sector that has attracted investor attention in recent weeks has been DeFi. DeFi market cap climbed to new highs since mid-November ($162B) at the end of the year.

The more significant data point, however, has been DeFi dominance climbing to new ATHs, finally breaking above 6.5%. This could signify a momentum shift to the sector.

From a pure technical perspective the writing was on the wall. FTX’s DeFi Perps on both its USD and ETH ratios were severely oversold (the latter bouncing from its ATL and lagging core ecosystem assets for most of 2021).

The sector has been buoyed by Ethereum-centric DeFi assets - both large- and mid-cap names including, yearn.finance, Frax Share, and Ribbon Finance.

In most cases, we can attribute specific catalysts for these performances. In December, Yearn Finance started to buyback YFI from the open market (0.77% of total supply). FRAX’s stablecoin monetary supply has climbed 50% while Ribbon Finance TVL surged to $300m.

Several observations can be made in the context of where DeFi has been over the past year:

DeFi is outperforming the wider market. High-cap/mid-cap names can outperform small-caps

DeFi assets have often remained oversold relative to their underlying activity or usage and this may be recognized

Fundamentals continue to remain key for analyzing sector/asset performance

We maybe starting to see the first signs of structured products like Ribbon Finance lift off

L1 Ecosystem Assets

Not all L1s have seen muted price action relative to DeFi. Fantom, Atom, and NEAR have all seen >70% returns on their ETH ratios since the holidays.

Cosmos - Now connects over $68B in digital asset value across 28 IBC-enabled chains. Sentiment around Terra has likely carried over to Cosmos.

NEAR - Aurora’s EVM layer for NEAR took off in November 2021 with its TVL quickly climbing to >$600m. DeFi applications like Synapse are bridging over to Aurora.

Fantom - Ecosystem TVL climbed to ATH $6.6B with over 1.4m unique addresses and 93k smart contracts.

Core ecosystem assets have been, and will likely continue to be, good proxy plays for overall utility growth in the market. Multi-billion ecosystem funds will clearly play a key role in fuelling this growth in 2022.

Top performing assets have centred around Ethereum DeFi with performance often being tied to headlines/event-driven catalysts. Note - DeFi top performers have been the global top performers.

Global (7d%):

Ribbon Finance (+76%)

Alchemix (+74%)

Frax Share (+62%)

Dopex (+61%)

DeFi Kingdoms (+38%)

DeFi (7d%):

Ribbon Finance (+76%)

Alchemix (+74%)

Frax Share (+62%)

Dopex (+61%)

DeFi Kingdoms (+38%)

Lido DAO

Lido’s TVL (staked valued via its DAO) has climbed to new ATHs - $13.3B. Lido has benefited from market appreciation in the underlying assets. For example, over 66.5m LUNA is staked via Lido today - an asset up 20% over 2 weeks.

LDO remains >70% undervalued according to its APT ratio.

Convex Finance

Convex Finance is the largest protocol ‘holder’ of veCRV and is on track to overtake all other protocols combined. Convex made $64m in the month of December - a 15% MoM decline but is still impressive.

Tokemak

The decentralized market making protocol has reached >$1B in TVL, aided by the launch of different reactors including UST. Total TOKE addresses has also seen good growth, surpassing the 3k mark.

TOKE holders direct the TVL of the protocol where its economics can evolve into reward distribution model where holders get a share of accrued protocol controlled assets (PCA).

Tokemak launched UST reactor. APY now stands at 9% for UST depositors and 47% for TOKE stakers.

Convex concluded rewards for Sushiswap CVX/ETH pool. LPs are expected to migrate to Curve CVX/ETH pool to continue receiving CVX incentives. APY is 19.5 - 39.7% with LP tokens staked in Curve gauge (CRV rewards) and 43.3% (CVX rewards) with LP tokens staked in Convex.

Badger used BADGER tokens from treasury to restore governance tokens to those affected by the frontend exploit happened in early December 2021.

Convex soft launched FXS product. During Phase 1 LPs can convert FXS into cvxFXS (works like cvxCRV), cvxFXS staking is not available yet, but cvxFXS holders will be eligible for Frax Finance’s upcoming FPI airdrop at the maximum possible multiplier. Learn more here.

US SEC Head Hires Crypto Advisor Amid Continued Regulatory Uncertainty. Corey Frayer is hired to advise on “SEC policymaking and interagency work relating to the oversight of crypto assets,” according to a new press release from the regulator.

Legal experts in India state cryptocurrency can no longer be banned as the Reserve Bank of India called for an outright ban on crypto.

Binance gains regulatory approvals to provide crypto services in Canada and Bahrain. Binance have restricted Ontario users from trading on its platform or open new accounts after a meeting with the Ontario Securities Commission.

Global market cap: $2.4T; Global market cap has fallen 5% over the past week.

DeFi: $156B; DeFi market cap has fallen by 4% - slightly less than the wider market.

Market shares; Bitcoin dominance continues to fall closer to 2021 lows (43.8%) as high and mid-cap name performance put pressure on its market share.

BTC/USD and ETH/USD (D)

ETH/BTC (D)

Price action; Overall soft markets. BTC finding good support at $45.5k and ETH $3.6k. BTC showing early signs of bullish RSI divergence on the daily. RSI values across the board are oversold/neutral (40-50). Relatively low volumes.

Volatility (BTC & ETH); BTC and ETH 30D vol rose in the run up to the new year but has since fallen. 3-month implied volatility for ETH has fallen to yearly low.

Combined order books; Order books look heavier on the bid side. Heavier resistance up to $48.8k (Source: Bitcoinity).

Crypto vs. SPX; Crypto correlation to equities weakened over December but early signs this is reversing. Concerns around Omicron may be alleviated for investors with U.S. stock futures gaining near their record highs.

GBTC premium; GBTC discount kept low at 20%. 30D volumes also flat (5.4m) indicating overall limited demand on secondary market for GBTC. Grayscale’s GBTC AUM has dropped 30% since early November.

ETHE premium; ETHE discount at 13%, slightly above ATL levels. Higher discount since November indicates demand for ETHE shares has continued to get weaker. ETHE volumes have kept flat over the same period.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has picked up over the last week indicating a relatively higher network congestion.

On-chain real (BTC) & off-chain volume; BTC on-chain volume increased ~3% over the past week. BTC and ETH spot volumes (7d MA) have decreased 3% and 6% respectively for the same period.

Hashrate & Difficulty; Bitcoin hashrate has climbed to new all-time-highs making the network more secure from a 51% attack perspective. Bitcoin has fully recovered from its 50%+ drop in hashing power driven by the Chinese mining ban.

Active addresses (BTC); Active addresses (30d MA) has fallen 1% over the past week.

Trader positioning; Futures OI fallen for both BTC and ETH since late December along with declining USD-denominated futures volume. ETH seeing lower put/call ratio while BTC seeing a higher ratio (divergence).

Omenics Sentscore (BTC); Sentiment around BTC picked up towards year end but has fallen since the asset fell further below $50k.

Exchange inflow/outflow (BTC, ETH); Very high net inflows for ETH to exchanges while BTC sees continued moderate net outflows.

USD-Pegged Stablecoin Flow; Continuation of net outflows for USD-pegged stablecoins pointing to potentially limited opportunistic buying by investors at current price levels.

📚 2021: 21 Graphs That Defined The Year For Crypto [Decentral Park Capital]

📚 Tokemak Oil: Greed-onomics, Efficiency, and Ease of Use [@Ghost_08]

📚 December Summary [@lars0x]

📚 The Rise of LUNA [@JayJaboneta]

📚 Samsung NFT Support [The Verge]

🎙️ Closing Out Another Year [Between2Chains]

🎙️ Big-Picture Power Shifts To Watch in 2022 [The Breakdown]

🎙️ The Biggest Winners, Losers, and Memes [Unchained]

🎙️ The Biggest Stories In Crypto and Macro in 2021 [The Breakdown]

🎙️ Endgame [Bankless]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.