The Weekly #175

Bitcoin tops $58k as uncertainty around the Omicron COVID varian resets traders' risk-on appetite. Gaming-related assets lead the pack for weekly performance while Ethereum L2 TVL climbs to $6.7B.

Macro Factors Weigh in On Crypto

Another week in crypto and its hard not to see some bearish sentiment trickling in. Bitcoin is trading at the same levels than 7 days ago but failed to break above the $60k mark. The asset moved closer to this key psychological level in the run up to the $3B options expiry with max pain being $58k.

The cost of puts relative to calls has increased which indicates increases levels of fear in the market. As highlighted last week, concerns about the the Fed’s accelerated plan to increase rates and a higher dollar has put pressure on cryptoassets.

This still seems to be the case with the dollar index surging to 97 - increasing 3% since the U.S. inflation data on November 10th and an ATH since mid-July 2020.

However, the new concern in the markets for investors is the Omicron Covid variant. Much about this new ‘highly transmissible’ variant is unknown and it is likely that this uncertainty will weigh heavily on risk appetite over the coming weeks.

The S&P 500 is down 3.15% from its November highs while 10-yields fall below 1.5%.

There are reasons to be optimistic too. We are seeing continued net outflows for large cap names like BTC and ETH. This indicates healthy, sustained levels of BTC and ETH accumulation.

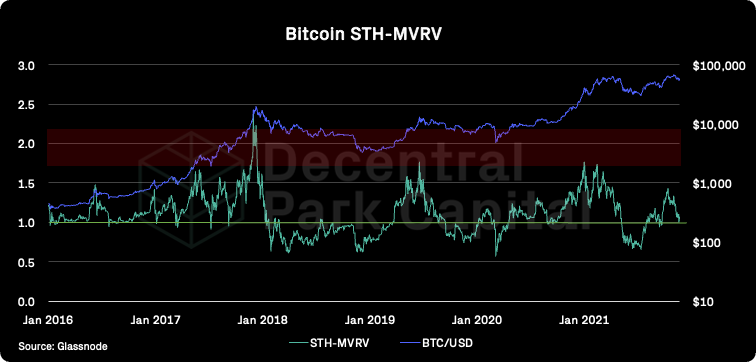

Shorter-term valuation metrics that analyze the behaviour of short-term investors is also positive. The short-term MVRV has bounced above 1 which can often (but not always) act as a support in bull trends.

If broken below 1, Bitcoin more often enters a bearish period where the 1 line is used as a resistance line. This will be one key metric to pay attention over the coming days/weeks.

Ethereum Scaling to Record Highs

Total-value locked across Ethereum L2s continues to surge to new ATHs - currently standing at $6.7B. This growth is outpacing TVL on Ethereum L1 with L2 TVL on track to represent 5%+ that of Ethereum L1 TVL by year end.

ZKRollup-based solutions now account for nearly 1/3 of all L2 TVL but optimistic still leads with 67% dominance. The imminent launch of the ZKSync token and Starknet will likely drive ZKRollup dominance much higher.

ZKSync is also already 85% cheaper to transfer ETH and tokens that both Optimism and Arbitrum. Despite this, we are seeing significant growth of alternative L1s like Avalanche.

Transaction count on the L1 has surged to new ATH (700k) - 40% that of Ethereum’s. The Avalanche-Ethereum bridge also has the second highest TVL, increasing 172% over the past 2 months tp $6.8B.

Increased usage has meant swap fees climbed to $8.40. At the same time, ZigZag swap fees have stayed $0.94 (88% lower than those on Avalanche). Despite a relative more expensive environment for users, Avalanche’s Blizzard and Rush funds continue to help attract users to this chain.

Building On The DeFi 2.0 Narrative

Finally, emergent USD-pegged stablecoins like FRAX continue to show promising growth. Aided in part by Olympus DAO, the DeFi 2.0 narrative will with the launch of the Frax Price Index and further innovation around their AMO controllers.

In short, we will see further innovation for how DAOs can form mutualistic relationships for aligned initiatives with algorithmic stablecoins playing an increasingly important role within those initiatives.

Top performing assets over the past week have been concentrated around gaming/play-to-earn assets:

Global:

Bitkub Coin (+555%)

Gala (+83%)

The Sandbox (+80%)

Ethereum Name Service (74%)

Basic Attention Token (+46%)

DeFi:

Seedify.fund (+67%)

cBAT (+46%)

DerivaDAO (+43%)

Anyswap (+36%)

Ampleforth (+35%)

LRC

LRC has 4x over the past month and been an outperformer. Key drivers include GameStop-related rumors around an NFT exchange using Loopring’s technology. Trading volumes have increased since the news with 95% of activity being AMM-related.

However, LRC trades at a very high premium to its overall volume (150 P/S) although this has halved in November.

OHM

The total market value of treasury assets backing Olympus is climbing back to ATH levels ($850m) and over $500k in partner’s tokens.

Adding UST bonds (next stable reserve) proposal has been submitted which will diversify the treasury further and allow Olympus to go cross-chain to the Terra ecosystem where it can earn additional yield.

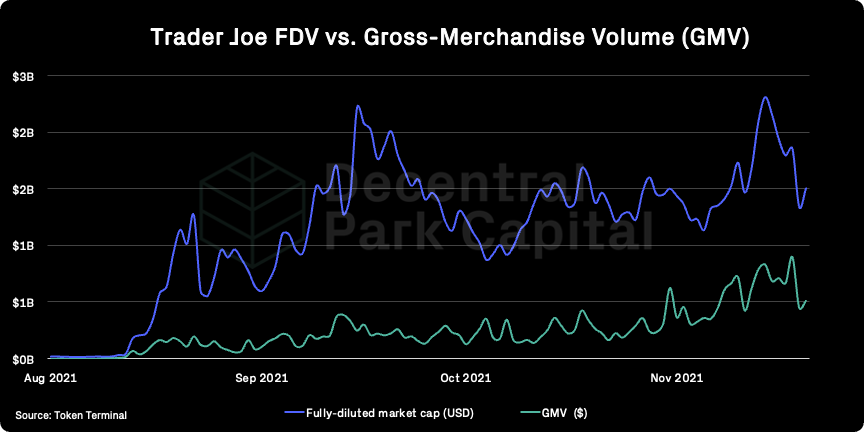

JOE

Trader Joe printed a new ATH for daily volume ($900B). TJ’s ecosystem competitor, Pangolin, prints 8% of the daily volume today. TJ’s to gun for the more widely adopted tokens in the Avalanche ecosystem compared to the higher risk, lower volume tokens on Pangolin.

This may have kickstarted a positive feedback loop where higher liquidity results in lower slippage, higher trading fees etc.

Curve launched CRV / ETH pool, incentives TBA this week.

Pika, perpetual swap protocol on Optimism, is live on mainnet, LPs can deposit USDC, but the vault is currently at max capacity.

Curvance was announced, launch date TBA. Protocol will allow users to borrow against Curve and Convex LP tokens.

Platypus, stable swap protocol with one-sided liquidity, launched on Avalanche, LPs can provide USDT, USDC, DAI and MIM, with $2.5M liquidity cap per pool (currently reached). APY is close to 100% for each asset.

Tokemak launched first wave of reactors. LPs can stake FXS, ALCX, SUSHI, TCB and OHM for almost 50% APY in TOKE rewards.

Coinbase, Binance.US, Tether probed over consumer risks by key senator (Bloomberg). In response to regulators issuing a report on stablecoins, Senate Banking Committee chairman Sherrod Brown sent letters to executives at major US crypto players to learn more.

Crypto oversight road map is set by U.S. banking regulators (Bloomberg). The Fed and other banking agencies released an agenda for 2022 outlining areas of focus to include how to weigh custody, crypto-backed loans, and capital standards. Separately, the OCC indicated banks must get sign-off before engaging with digital assets. Read more here and here.

Bank of America sees stablecoin regulation as catalyst to mass adoption (CoinDesk). Research note class US Treasury’s “Report on Stablecoin” an “indication of urgency” for regulation given their potential as a viable global payment method.

Global market cap: $2.71T; Global market cap has been flat over the past week.

DeFi: $152B; DeFi market cap has also been flat for the past week. DeFi dominance has fallen a further 3%.

Market shares; Bitcoin dominance has kept flat over the past week and now standing at 47.8%.

BTC/USD

ETH/USD

ETH/BTC

Price action; BTC weakness printing a descending channel, finding initial support at $53.3k. ETH/USD more stable and finding support at $4k. ETH/BTC up 4% for the week with RSI approaching overbought levels.

Volatility (BTC & ETH); BTC 30D vol has kept relatively flat while ETH has risen over the past week. 3-month implied volatility for ETH and BTC have fallen slightly.

Combined order books; Order books look slightly heavier on the ask side. Heavier resistance all the way up to $59k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC trading more like a risk-on asset of late with the asset showing weakness along with equities driven by concerns around the Omicron Covid variant. European markets are recovering from Friday’s sell-off with U.S. stock futures showing similar patterns.

Uncertainty around the new variant likely to weigh on risk appetite but eyes will also be on key economic data in equal measure (e.g. November Job reports).

GBTC premium; GBTC discount floor now ~11.7%. Morgan Stanley increased its GBTC by more than 63% from Q2 to Q3.

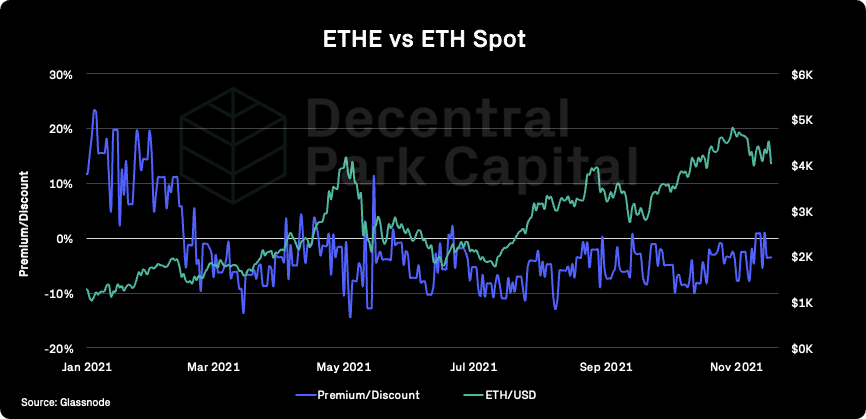

ETHE premium; ETHE printed 1% premium last week but failed to keep in positive territory, falling back to a 3.4% discount. 30D average ETHE volumes remain flat since mid-October indicating relatively low demand.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains relatively low indicating low network utilization.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

On-chain real (BTC) & off-chain volume; BTC on-chain volume increased ~21% over the past week. BTC and ETH spot volumes have stayed flat over the same period.

Hashrate & Difficulty; 7D hashrate has fallen 3% over the week. Bitcoin had its first difficulty drop since mid-July following weaker BTC price.

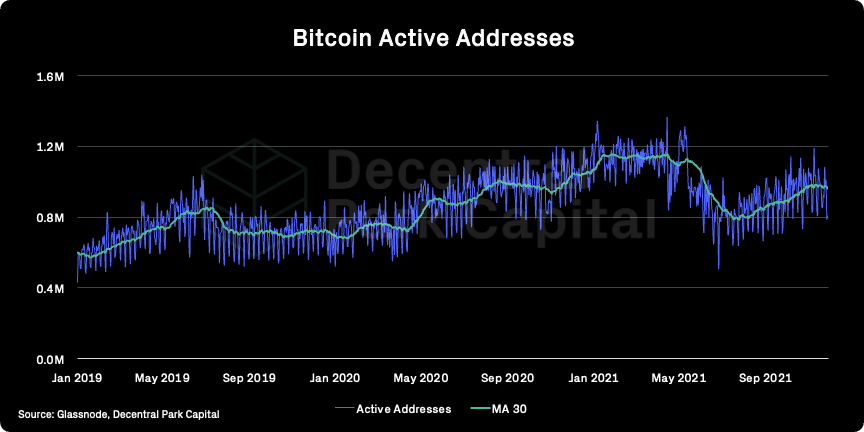

Active addresses (BTC); Active addresses (30d MA) has fallen 1% over the past week along with weaker spot action.

Trader positioning; Perpetual funding rates remain slightly positive for BTC and more neutral for ETH. Open interest remains high for both BTC and ETH and are 16% and 18% from their ATH peaks in line with spot action. Perhaps limited deleveraging and rather lack demand for leverage-long positions to levels seen in late October.

Omenics Sentscore (BTC); Sentiment score around BTC continues to fall over the past week showing a similar sentiment pattern to mid-September when Bitcoin fell from $52k to $40k.

Exchange inflow/outflow (BTC, ETH); Strong net outflows for BTC on the 7d MA. ETH printing moderate net inflows (USD) over the past week but ETH balance on exchanges has begun to fall once again.

USD(b) supply; Total stablecoin supply has increased by 1B over the past week and now stands at over 138B.

📚 A Theory Of DeFi [algo_class]

📚 DAOs And Labor Movements [Li Jin]

📚 DAO Treasury Diversification [Accel_Capital]

📚 Hop Protocol Update [HopProtocol]

📚 Painting The Bear Market [Jason Choi]

🎙️ PleasrDAO [Delphi]

🎙️ Weekly Roundup #263 [On The Brink]

🎙️ Polygon: The Swiss Army of Knife of Scaling [Bankless]

🎙️ Pierce Crosby on Market Mania [The Scoop]

🎙️ What Jerome Powell’s Second Term Means For Bitcoin [The Breakdown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.