The Weekly #174

Crypto markets show good recovery from last week's retrace. On- and off-chain analysis point to promising levels of demand with the macro environment still conducive for risk-on assets overall.

The global crypto market cap continues to pull back from ATH levels ($3.04T), falling a further 7% over the past 7 days.

Last week, weaker spot markets, leveraged long traders and headline-driven catalysts were all potential drivers for the more volatile price action. However, simple RSI analysis had signalled an incoming correction with the indicator continuing to be a very useful momentum indicator.

BTC eventually found support at $55.7k with the asset now heading back closer to that level.

From a macro perspective, investors are clearly pricing in rate hike increases in 2022 with the US dollar index up 4 weeks in a row reaching ATH since July 2020. With consumer inflation printing its biggest annual increase in 31 years and forcing the Fed’s hands for higher rates will attract yield-seeking capital.

Crypto assets like BTC are also likely viewed as risk-on meaning during periods of stress, investors may look to take profit from highly profitable positions. Last week was likely that time.

Looking forward, there macro bullish signals can still be found. These include strong earnings and the continued fiscal stimulus from the recent $2T Social Spending and Climate Bill.

However, the reality is rate hikes still loom over the market and arguably pose the single biggest risk to markets overall. Fund managers perceive this risk higher in November than last month.

In the futures markets, BTC funding rates have fallen 67% from early-November highs with leveraged long traders being flushed out. While traders are taking a predominantly bullish stance, continued slowed momentum can exacerbate price action near-term.

Conversely, ETH is more neutral with long liquidation risk being lower. BTC call options for year end also dominate around $100k.

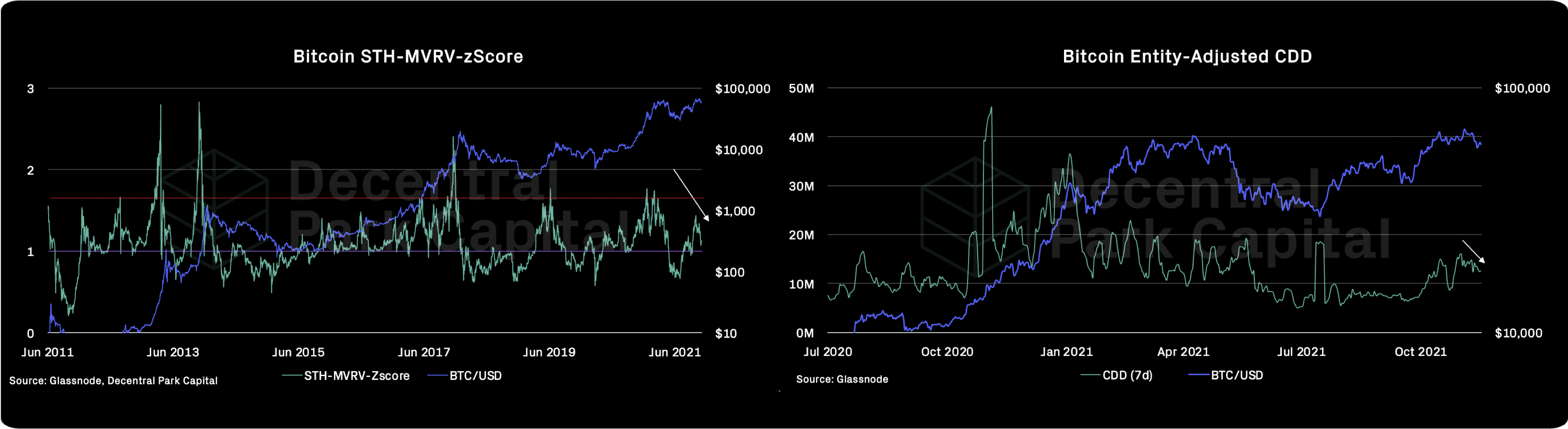

Looking on-chain, short-term holders are selling less after modest spending. The STH-MVRV indicator is reset closer to 1 which has historically coincided with good periods to be long.

Long-term holders are likely taking less profits now as indicated by the Coin Days Destroyed (CDD) metric.

DeFi

DeFi was not immune to last week’s pullback but has since recovered well from Friday’s lows (+$10B market cap). Best performing assets were Avalanche-centric including JOE (74%), BENQI (70%), and Pangolin (18%).

AVAX continues to print new ATHs ($136) after announcing a partnership with Deloitte to build disaster relief platforms. However, we can still see Ethereum-centric growth on L2s.

Boba Network prints the largest TVL change over the past week seeing $800m in contribution. Fast withdrawal times to Ethereum is salient for users and we may see continued interest here relative to other optimistic solutions.

Looking forward the next ecosystem arguably primed for significant relative growth is NEAR. NEAR announced a $800m ecosystem fund for DeFi, NFTs, and gaming. With only ~$100M in ecosystem TVL, NEAR has the largest fund size to TVL ratio in the market.

With its smart contracts being built in rust, projects and talent on Solana may be looking to ‘parallel develop’ on NEAR. Simply put, what is good for Solana, may also be good for NEAR.

Top performing assets have been native ecosystem assets and Avalanche-related DeFi dApps.

Global:

Gala (+297%)

Crypto.com Coin (+51%)

Elrond (+47%)

Avalanche (42%)

LINK (+40%)

DeFi:

JOE (+73%)

BENQI (+63%)

Pangolin (+19%)

GMX (+19%)

STP Network (+14%)

wNXM (Discount 40%)

Discount has narrowed from 70% (ATH) to 40% since late October. With the capital looking to buy wNXM off the secondary market, free market dynamics appear to be front running this activity (self-fulfilling prophecy).

Nexus P2B ratio at 0.9 with the asset still oversold relative to its book value. New covers for November forecast to be on par with October total ($180m) at current rate.

LDO (-50% FDV/TVL)

Lido continues to trade below total value committed to Lido validators. LDO reacted strongly at 70% FDV/TVL with that level fast approaching once again (i.e. strong ETH price action with weaker LDO/DeFi price action)

BENQI (-7% FDV/TVL)

The Avalanche-based lending protocol has seen $400m higher TVL in its markets while seeing its borrow volume increase 61% over November. BENQI’s borrow volume is now 20% that of Aave’s and 25% that of Compound’s.

BENQI is priced at a higher premium to borrow volume than Aave and Compound (BV/FDV ratio of 1.5 vs 2.5 and 2 respectively) but this gas is closing since inception.

GMX

GMX has been a top performer over the past week as the Arbitrum-based hybrid DEX top $110m in TVL. Volumes average ~$50m daily with over 90% being attributable to perps.

With no strict incentives at play, this growth in volume looks to be natural demand from users. More importantly, these volumes are on par with Perpetual Protocol’s volume where its V2 will also be launching on Arbitrum in Q4.

Abracadabra increased SPELL emissions to Avalanche with 5.8% of tokens rewarded to Curve MIM/USDC/USDT pools. MIM can be borrowed against AVAX, AVAX/USDC JLP, wMEMO and xJOE, but reserves are almost depleted.

Tokemak concluded C.o.R.E.2. reactor voting, winners are FOX, VISR, SNX, ILW and APW. Holders will be available to stake these tokens in Tokemak new reactors.

Tokemak launched bribing service similar to Curve, TOKE holders now can earn bribes for voting in C.o.R.E. During C.o.R.E.2. voting, $834K of FOX and $600 of VISR were paid as bribes.

Popsicle Finance made first buyback of it's ICE token and revenue distribution (20%) to nICE holders after relaunch two weeks ago.

Teher commences active testing of Shyft solution to FATF ‘Travel Rule’ (Cryptopolitan). The largest stablecoin by market cap announced it is integrating with Shyft Network to test a “decentralized compliance framework and smart contract solution” to FATF requirements.

Ripple Labs wants to limit SEC sway over crypto as legal fight rages (Bloomberg). The company is promoting a larger role for the CFTC amid calls for industry collaboration and reigning in the SEC’s legislation by enforcement. Ripple introduced a Real Approach to Cryptocurrency Regulation in support.

US Congressmen introduce bill to modify crypto tax provision in infrastructure law (CoinDesk). Bipartisan group introduced a bill to narrow the broker definition and tax compliance requirements. This is a strong signal that legislators continue to expand their understanding of digital assets.

BlockFi faces SEC scrutiny over high-yield crypto accounts (Bloomberg). After several state sanctions, the SEC confirmed that it is “scrutinizing” whether the flagship yield product is a security.

Global market cap: $2.69T; Global market cap has decreased 10% over the past week.

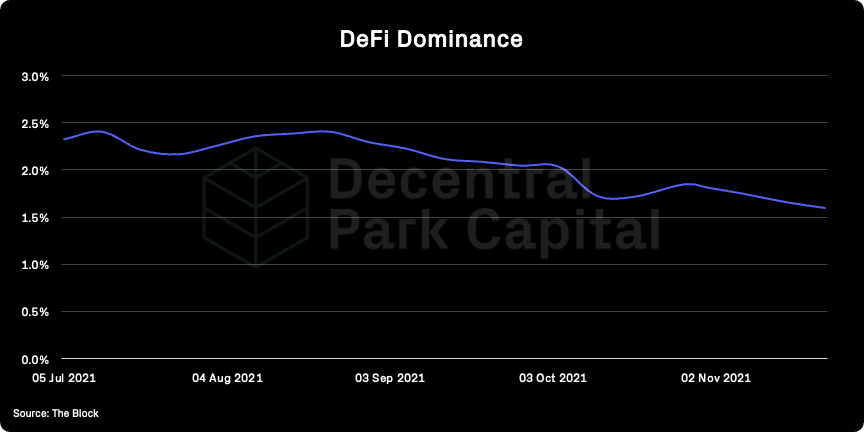

DeFi: $152B; DeFi market cap decreased 9% over the past week but strong recovery since Friday (+7%). DeFi dominance continues to fall since August, decreasing a further 4% over the last week.

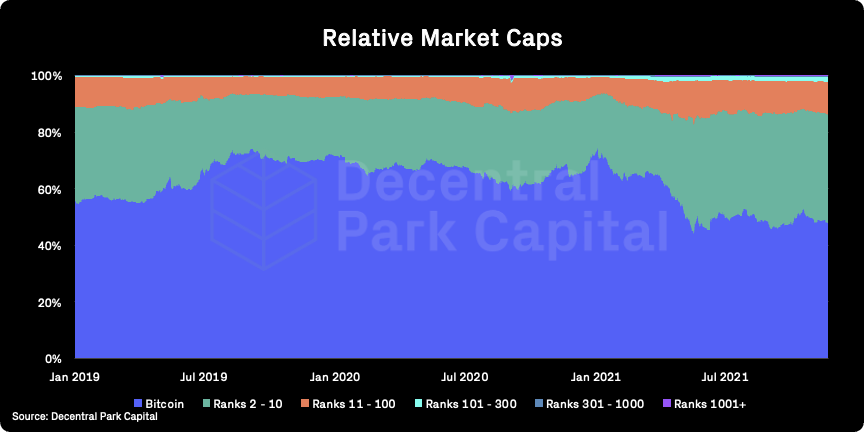

Market shares; Bitcoin dominance has fallen 1% over the past week (48%) as high cap names continue to claw back market share.

BTC/USD

ETH/USD

ETH/BTC

Price action; Relative soft markets with BTC/USD support formed at $56k-$56.5k. Stronger recovery in ETH vs. BTC since last week’s low. Daily RSIs all in more neutral territory.

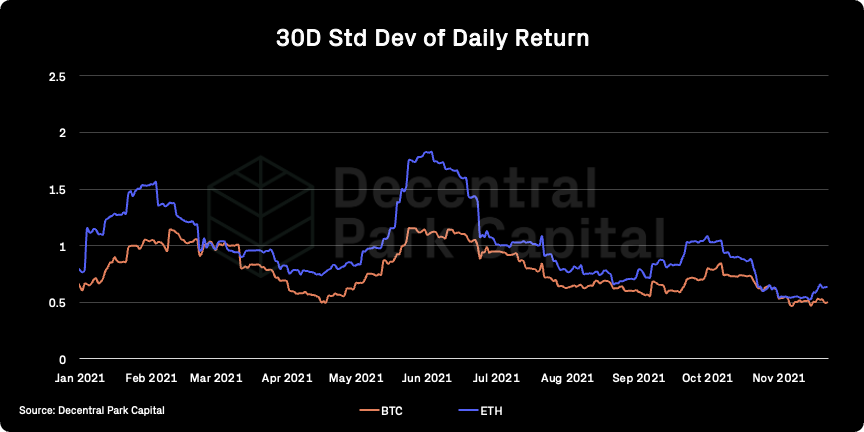

Volatility (BTC & ETH); BTC 30D vol has kept relatively flat while ETH has risen over the past week. 3-month implied volatility for ETH has increased while BTC has kept flat.

Combined order books; Order books look slightly heavier on the bid side. Heavier resistance all the way up to $58.5k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC mostly trading like a risk-on asset. Equities remain strong overall helped by upbeat retail and technology earnings. BTC becoming less correlated to equities in November but may be a temporary relationship as has been the case numerous time throughout 2021. Overall macro environment is net conducive for crypto over the short-term.

GBTC premium; GBTC outperforming vs. spot over the past few days with the GBTC discount at an ATL since September. Indication of strong demand with weaker price action.

Grayscale remains committed to transforming the trust into an ETF with the operation completed as early as July 2022.

ETHE premium; ETHE printing slight premium (0.8%) for first time since mid-September. Indicates strong demand at lower price levels (similar to GBTC) but possible we see discount returning as has been the case throughout 2021.

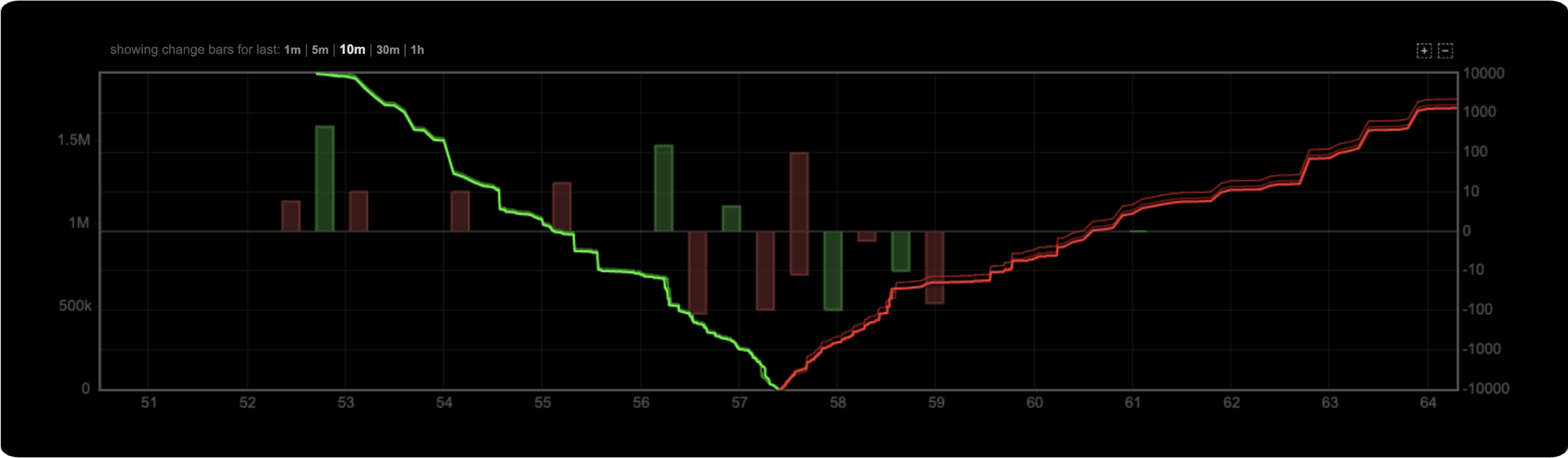

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains relatively low indicating low network utilization.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

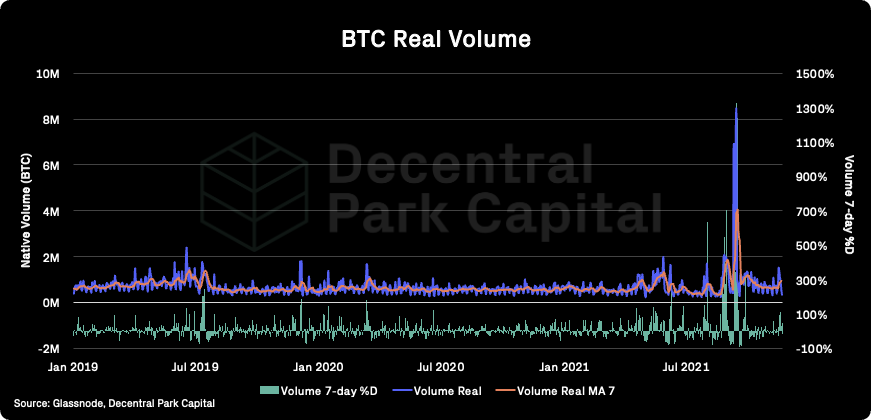

On-chain real (BTC) & off-chain volume; BTC on-chain volume increased ~27% over the past week. BTC spot volumes have increased 10% while ETH spot volumes have kept relatively flat 7% over the same period (divergence).

Hashrate & Difficulty; 7D Hashrate has kept flat over the past week. El-Salvador announced its plan to build a Bitcoin city at the base of its Conchagua volcano as the mining market booms outside of China. At the same time, Norway and Sweden highlight concerns to the EU about the industry.

Active addresses (BTC); Active addresses (30d MA) has fallen 1% over the past week along with weaker spot action.

Trader positioning; Perpetual funding rates slightly positive for BTC and neutral for ETH. OI for BTC and ETH has fallen 7% and 18% from their ATHs respectively.

Omenics Sentscore (BTC); Sentiment score around BTC has fallen over the past week showing a similar sentiment pattern to mid-September. This preceded BTC’s moved from $43k to $53k.

Exchange inflow/outflow (BTC, ETH); Very strong net outflows for ETH (USD). Moderate net outflows for BTC. Both assets have seen a ~2% reduction in supply on exchanges over November.

USD(b) supply; Total stablecoin supply has increased by 1B over the past week and now stands at over 138B.

📚 Treasury Backed Instruments [lazyvillager]

📚 Nym Thesis [Eden Block]

📚 Astroport Lockdrop [Astroport]

📚 ETHLisbon Hackathon Projects [0xminion]

📚 L2 misconceptions [Polynya]

🎙️ Paradigm [UpOnly]

🎙️ Starbuck and Miami Are Launching Tokens [Between2Chains]

🎙️ State of The Charts [Bankless]

🎙️ Taproot Facelift & The Economy [Real Vision]

🎙️ Are Stablecoins The Path To Continued Dollar Dominance [The Breakdown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.