In The Weeds #6

Diving into the latest innovation around liquid staking derivatives, decentralized custody, and multi-collateral stablecoin designs

Welcome to Decentral Park’s new research sub-newsletter: In The Weeds.

This weekly instalment will focus solely on key technical developments and themes within Web3, keeping you ahead of the game on upcoming trends.

Let’s get stuck into this week’s key highlights.

1: Lido V2

What is it? Our old friend Lido Finance, the leading Liquid Staking Derivative (LSD) provider by TVL got followers of the LSD narrative riled up last Tuesday when they released their largest upgrade to date, Lido V2. This comes at a time that’s being dubbed ‘LSD Spring’, with LSDs performing particularly well heading into the Ethereum Shanghai upgrade, and various LSD providers releasing new integrations and product upgrades.

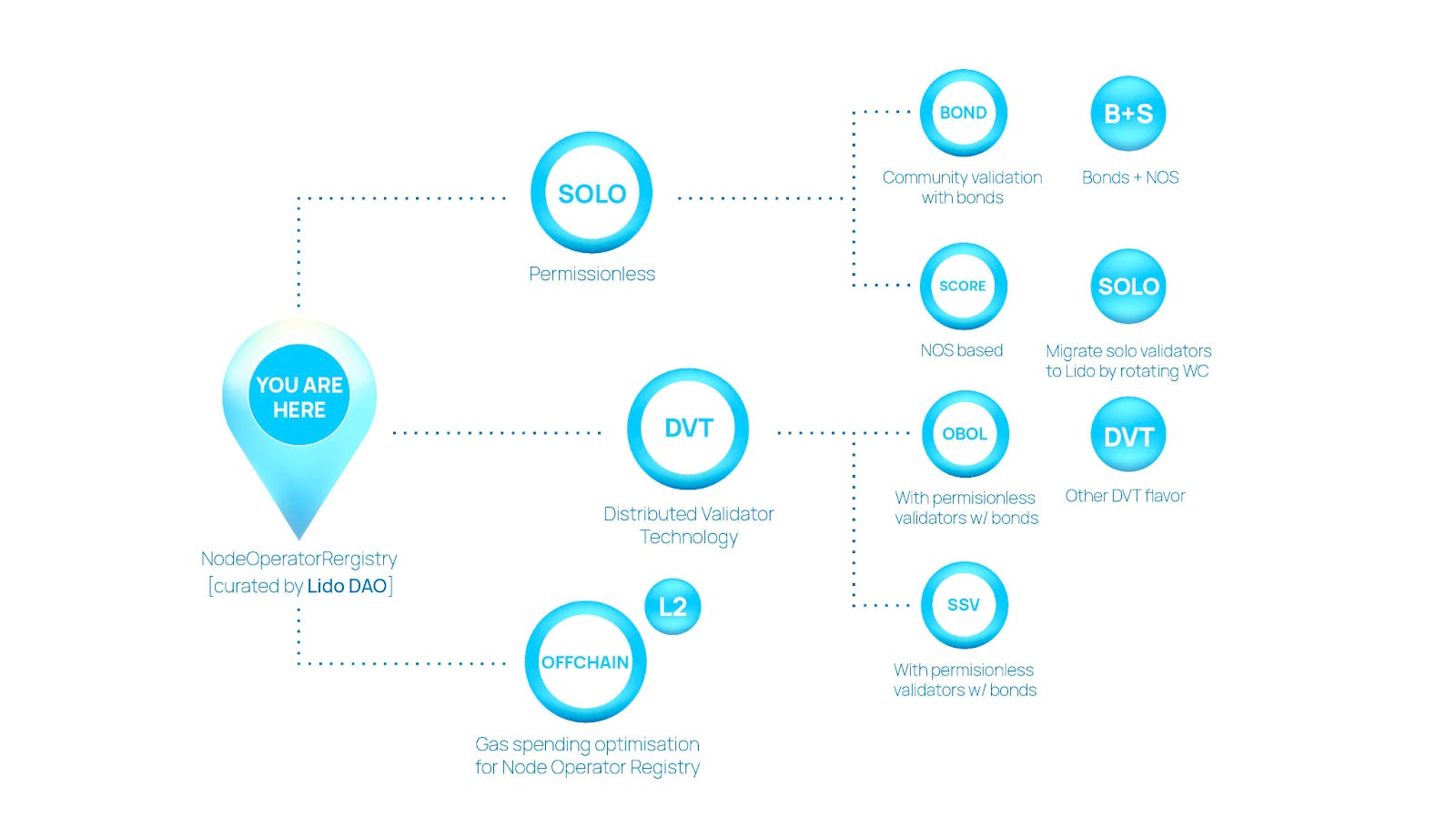

So, what’s changed from Lido we’ve grown to know and love? The V2 upgrade is centred around two major focal points, the Staking Router and Withdrawals.

Let’s start with the Staking Router, which has an overarching goal of increasing diversity within the validator ecosystem. The upgrade essentially moves the operator registry to a modular and more composable architecture, from a previously DAO-controlled registry of node operators.

What’s meant by this is that the Staking Router will act as an aggregator, allowing stakers, developers and node operators to seamlessly connect. It’s worth noting here that node operator refers to any type, ranging from solo stakers to DVT clusters.

In actual terms the Staking Router is a controller contract that will allow Lido to evolve into an extensible protocol via a modular infrastructure that node operators, stakers and developers can plug into.

The router will be made up of various modules that will be treated as sets of validator pools that can act as potential supply for the protocol, either on the staking or node operator side. Each module is independent, and will therefore be responsible for managing an internal operator registry, storing validator keys, and allocating stake and rewards between the operators that participate in the module. It’s worth noting here that modules can be made up of a single node operator type (DVT cluster, DAOs, solo stakers) or a blend.

The Withdrawals section of the Lido V2 upgrade is rather self-explanatory, it’s Lido preparing for a post-Shanghai upgrade world. At a very basic level, the upgrade will enable stETH stakers to withdraw their ETH from the Beacon Chain Deposit contract on a 1:1 basis post-Shanghai.

Lido’s V2 announcement lays out two withdrawal modes, Turbo and Bunker. Turbo will be the default mode, in which withdrawal requests are fulfilled quickly, using all available ETH from user deposits and rewards. While withdrawal times are uncertain and will depend on various factors, it is expected that they’ll range between one and a few hours.

Bunker mode is merely an ‘in case of emergency’ mode, which prevents sophisticated actors gaining an unfair advantage in the event of a mass withdrawal crisis. This can be thought of as a transaction order randomiser, mitigating the extent to which these sophisticated actors can manipulate preferential treatment.

Why is it important? Shifting from a DAO-controlled registry of node operators to what will become a permissionless integration of a variety of node operator types creates an obvious benefit of mitigation of network downtime risk.

Using a variety of node operator types here aids to the resiliency of the Ethereum network, which is ultimately the name of the game when it comes to staking.

The UX improvement from a node operator onboarding perspective should drastically enhance the diversity of Lido node operators, given the added incentive, and broader scope of node operator types. This is crucial to achieving the above major benefit.

A nice touch of the Staking Router is that it can also allow the storing of keys on L2 or off-chain, which dramatically lowers protocol costs and increases the potential number of node operators.

Another added benefit is the flexibility that the Staking Router introduction allows when it comes to node operator modules. Each individual module, and the corresponding subsets of their respective validators, will be able to customise parameters under which they operate. This ranges from fees applied, or collateral requirements.

The importance of the upgrade with regards to withdrawals is self-explanatory. It turns Lido into a complete LSD provider on the Ethereum network, allowing stakers to unstake at any time. Lido simply has to upgrade their protocol to keep up with the evolving Ethereum ecosystem.

Though one element of this that is perhaps less obvious is that it actually diminishes the need for Lido as a DAO to incentivise peg-stability. Previously, Lido had been forced to heavily incentivise liquidity on exchanges such as Curve, where users would typically be rewarded high APY in LDO tokens in exchange for providing sufficient liquidity to run an efficient buy-sell market that would maintain stETH/ETH peg.

With withdrawals enabled however, this peg-stability mechanism is replaced by a simple arbitrage opportunity, whereby speculators are able to redeem stETH for an ETH profit when below parity, and vice versa. This should in theory reduce the extent to which LDO emissions create sell-pressure on the token, given the reduced need to incentivise liquidity. Now, that’s not to say Lido will stop incentivising liquidity altogether, in fact liquidity is crucial for LSDs, though the rate at which emissions occur is expected to diminish.

Where does it go from here? Though roadmap timelines in crypto are rarely reliable, the Lido V2 timeline can be simplified into three main sections: (1) February - security audits, and the official vote, (3) April - deploy V2 to the Ethereum Goerli testnet, (3) March - Mainnet contracts to be deployed, which aligns with the expected date for the Shanghai upgrade.

One piece that is particularly interesting about the Lido V2 upgrade is their focus on DVT clustering. For those of you unfamiliar with the term, we took a dive into the technology in our first ever ‘In the Weeds’.

Not only has Lido included DVTs as seemingly a core focus, but they have recently undergone a second round of DVT testing with Obol Network and SSV Network, attempting to encourage solo stakers to partake in a DVT cluster. Our prediction within the first ‘In the Weeds’ that LSD providers would adopt DVT is beginning to play out sooner than expected, and is only expected to continue.

We’re also seeing the integration of third-party rating solutions in order to maintain a trustworthy set of node operators, even within a permissionless regime. Solutions such as Rated, which have been increasingly participating in the Lido ecosystem, are a leading example of such a solution. We at DPC expect to see a rise in the importance of such third-party, independent node operator measurements and ratings.

From a withdrawal perspective, we’re expecting one thing and one thing only… increased staking participation rates throughout not only Lido, but the whole Ethereum staking ecosystem.

Today, there is an enormous sense of uncertainty attached to staking ETH, with an unknown unlock deadline. Post-Shanghai however, assuming it is a success, that uncertainty will be entirely removed, allowing stakers to trust their value within the Beacon Chain contract.

For context, the Ethereum staking participation rate currently sits at ~13.8%, while withdrawals-enabled chains such as Solana and Cosmos sit at ~70.4% and ~63.1% respectively. We anticipate the result being a material staking participation rate, from which Lido, and other LSD providers, will benefit.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

2: MPC and Decentralised Custody

What is it? Since the dawn of crypto-time one phrase has been prominent, “not your keys, not your crypto”. While the UX within the crypto space continues to be sub-optimal at best, it is actually rather straightforward to hold crypto in a self-custodied wallet. This includes the process of bridging digital assets from centralised exchanges, which are currently home to the majority of liquidity, to self-custodied wallets.

For institution-grade investors however, it’s not so simple. This is because they’re required by law to hold customer assets above a certain amount with ‘qualified custodians’. The SEC for example requires that customers assets above $150,000 are held in such a manner. This means that above certain monetary thresholds, which generally are relatively low for such investors, investors are unable to simply spin-up a wallet and self-custody their crypto assets.

Given regulatory pressures and the collapse of large industry players, institutional-grade investors are becoming increasingly deterred from custodying digital assets with centralised exchanges. The phrase “not your keys, not your crypto” never really went away.

It’s therefore necessary for these institutional investors to look to qualified custodians that can offer them the best of both worlds.

Enter Multi-Party Computation (MPC) and decentralised custody…

MPC is a method employed by qualified custodian providers such as Fireblocks and Copper to allow digital assets to be stored within a fully on-chain wallet, accredited to an institutional-investor, without the need for these investors to risk exposure of their private keys.

This is achieved leveraging zero-knowledge proofs, meaning private keys are no longer required to be stored in one single location on the qualified custodian side. Instead, the single point of compromise is removed by breaking the private key up into shares, encrypting these shares, and dividing them amongst multiple ‘parties’, or machines. These parties are completely blind to each other's underlying valuable data (i.e. private key share) at all times.

As such, MPC enables fully decentralised custody, employing blockchain technology to immutably store each asset’s ownership data. The result is that transactions can be processed by these qualified custodians, without the need for private keys to be held as a single point of compromise attack vector.

There are many types of MPC algorithms leveraged within the qualified digital asset custodian space, such as Gennaro and Goldfeder, the Lindell et al. and the Doerner et al. For an in-depth dive into the nuances of each algorithm, I’d recommend exploring this resource produced by Fireblocks.

Why is it important? MPC and decentralised custody enables institutional-grade investors to invest in the crypto ecosystem while staying true to its underlying core values. This is crucial for institutional investors, because it enables them to maintain ownership of their assets, and removes the fear associated with FTX-esque incidents in which they could potentially lose value entrusted to them.

Moreover, it’s actually a safer form of custodying assets than merely leaving them on a centralised exchange. The process of decentralising private key data makes the compromise of a private key within MPC-enabled custody solution highly unlikely.

Now, these are clearly reasons why MPC and decentralised custody is important to institutional investors, but the big question that remains is why should investors who aren’t institutional investors care about MPC and decentralised custody? The answer is simple: the ecosystems that qualified custodians leveraging MPC solutions cover, to some degree, dictate where institutional investors can put their cash.

As it currently stands, the coverage universe is fairly limited, often only to ERC-20 tokens although occasionally reaching out to BEP-20 tokens and SPL tokens. What this represents is a significant kink in the armour of the app-chain thesis, with ecosystems such as Cosmos and Polkadot often overlooked, as well as smaller ecosystems.

The bottom line is that until qualified custodians expand their coverage universe, assets such as OSMO will lack the catalyst that comes with a wall of institutional capital. This is something that all investors should be paying attention to, and builders should be actively seeking solutions for.

Where does it go from here? The obvious answer to where this all goes from here is that the coverage universe needs to expand sufficiently to enable institutional investment into all major ecosystems.

This is something that represents a large opportunity for builders in the space, or specific qualified custodians looking to be on the cutting edge of institutional custody solutions. This is also potentially one of the biggest areas of focus from a value-add perspective for business development representatives of app-chains and lesser covered ecosystems.

Beyond this there is, and will continue to be, innovation at the MPC algorithm level with the goal of optimising for transaction speeds within the MPC model. For example, Fireblocks released MPC-CMP, an innovative algorithm type that at the time of release offered the fastest transaction signing speeds of any MPC algorithm by 800%, while Multichain has also entered the game with fastMPC.

3: Aave GHO

What is it? Since the long awaited deployment of Aave’s GHO stablecoin to Ethereum Goerli testnet occurred this week, and the recent BUSD drama, it only seemed appropriate to dive into GHO itself.

GHO is an overcollateralized, decentralised, dollar-pegged stablecoin minted that is backed by assets supplied to the Aave protocol. This means that collateral backing the GHO stablecoin is limited to the assets available to supply on the Aave protocol.

The mechanism is simple, to mint GHO, you must supply assets to Aave with the relevant corresponding collateral ratio, and to retrieve your collateral you return the GHO borrowed which is then burnt by the protocol. Interest payments accrued to Aave by minters of GHO, i.e. the associated borrow costs, are directed in their entirety to the Aave DAO treasury.

What’s novel and interesting about the GHO stablecoin, as opposed to decentralised alternatives such as DAI and Frax, is that GHO facilitates multi-asset collateral. This essentially means that users are able to mint GHO utilising a culmination of their entire Aave supply portfolio, be that ETH, LINK, wBTC etc.

The result being that rather than a user having to enter multiple loan positions across each individual asset, they’re able to enter into one borrow in a multi-asset manner, defending liquidation with any supplyable asset to the Aave protocol.

What’s also particularly interesting about GHO is that the collateral acts in exactly the same way a traditional supplied asset would do in the Aave protocol, generating yield. This can act to mitigate and potentially even in some cases completely offset the associated GHO borrow costs.

Why is it important? GHO represents the largest lending protocol in the ecosystem, with a total TVL of $4.63B entering the decentralised stablecoin competition. Aave is arguably perfectly positioned to dominate this sub-sector, and capture a significant portion of DAI and Frax’s combined $6.11B market capitalisation.

This is especially true when considering that stablecoin total reserve size on Aave comes to $46M, and it is expected that Aave will funnel users, either through economic incentives or simple asset or design choices, towards GHO borrowing.

While not yet material, it’s also worth emphasising the fact that Aave has specifically outlined L2s as a large opportunity space for GHO. Should we see Aave deployed to zkEVMs alongside existing L2 solutions such as Optimism and Arbitrum, as is expected, Aave will have a direct route to onboarding users to the GHO stablecoin in the L2 ecosystem from launch.

Where does it go from here? While GHO has not yet been deployed to mainnet, Goerli testnet appears to be going smoothly. This could indicate that release is somewhat imminent, with expectations being that GHO will be released in Q1 23’.

One of the features that we at Decentral Park are most excited about is facilitators. In short, facilitators are parties that are authorised to mint GHO in a trustless manner up to a certain threshold.

As it currently stands, only the Aave protocol and FlashMinter (minting equivalent of FlashLoans) will be facilitators should the proposal be approved by governance. However, the future of facilitators is what excites us.

Aave has outlined a future in which facilitators could range across various strategies, such as real-world asset facilitators and DAO-treasury-backed facilitators.

This opens up a whole host of possibilities that range outside of simply supplying Aave V3-approved supply assets, and into the realm of real world use cases, such as borrowing GHO against hard assets like property. The potential that GHO facilitates for Aave goes far beyond how we think about DeFi lending protocols today, and into a real-world integrated lending platform, simply run on crypto infrastructure.

That said, the regulatory pressure is tightening and the broad application of securities law within the Web3 ecosystem may be upon us in 2023. One particular sub-sector? Stablecoins. And GHO has those yield components at the heart of the product for the regs to double click on. Time to buckle up.

Key Decentral Park Links:

> Decentral Park Research Hub

> Decentral Park Market Pulse

> Decentral Park Website

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.