The Market

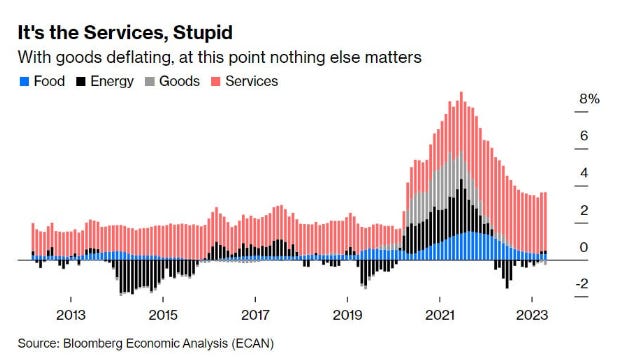

The crypto market is embracing a breath of life this week as the lower than expected May CPI number brings hope for a rate cut before September. Although the deceleration of inflation is good news, we are far from being out of the woods yet, given that the decline is mostly driven by food and energy costs. The cost of services, including housing, is more stubborn and more sensitive to wage growth and rate actions. If the Fed starts to cut rates too soon, service inflation could ramp up again. As we mentioned before, the Fed will need to see more data showing inflation catching up with slower economic growth to ensure they can safely cut rates.

The broader risk market is celebrating the inflation slow down, with BTC crossing the $67K level and QQQ up more than 2% this week. It’s noticeable that both the Global Net Liquidity indicator and the M2 supply have started an uptrend since the beginning of May. We expect liquidity conditions to continue improving heading into the summer as the slow down of Fed’s Quantitative easing brings $40B into the treasury market monthly. Additionally, there is a potential likelihood of rate cut before September, which is now priced with close to 50% probability.

The spot ETF has also averted the outflow trends last week. Even GBTC has seen days of inflows in the past two weeks. The deadline for the SEC’s decision on the ETH spot ETF is coming up next week. ETHE is currently trading a discount of 20%, indicating a low probability of approval. What will be interesting to watch is the SEC's reason for rejection. If it’s still related to potential market manipulation issues, similar to the argument they made when rejecting BTC spot ETFs before, this can be addressed as the CME ETH futures trading volume grows (currently about 1/6 of the BTC futures volume). If it’s related to ETH being considered a security, at least the SEC will have made it on record, and it will be up to the court to make the determination. Given the multiple ongoing lawsuits with the SEC around the essential issue of whether digital assets are considered as a security or not, any clarity on the SEC’s stance on ETH will speed up the progress.

TradFi Update

Speaking of progress, CME is planning to launch BTC spot trading in addition to BTC futures. We consider it as important a milestone as the spot ETF launch because this opens the door for spot BTC to be traded on a regulated TradFi exchange. The significance comes in many folds:

Regulatory Clarity: It is unlikely for CME to announce the plan without CFTC’s blessing. If approved, spot BTC will officially enter a regulated TradFi exchange and be treated like other commodities.

Institutional adoption: fund managers can now purchase BTC on a regulated exchange. With the availability of both spot and futures instruments, they can conduct basis trades more efficiently. This could bring healthy two way flows from smart money institutional capital.

Infrastructure Development: crypto trading requires different wirings than commodities. The fact that CME can offer this speaks to their infrastructure readiness to handle this new asset class. What’s more important to watch is how CME handles the custody issue. If Biden vetoes congress’s repeal of SAB 121, then it is hard to get TradFi banks or broker-dealers to custody crypto given the expensive capital requirements. Whatever CME chooses as custody will help push for a regulated custody solution for crypto.

Despite heavy push backs from the current administration and certain big banks on crypto, we have other TradFi institutions pushing for mainstream adoption of Bitcoin, such as CME, Blackrock, Fidelity and Franklin Templeton. We believe crypto is here to stay despite the uphill battle the industry is fighting.

DeFi Update

With Ethereum’s modular infrastructure being tested, there are a few smart contract platforms that have demonstrated potential to rival Ethereum in this cycle. Solana’s economic activity, considering both transaction fees and the MEV to validators, shows a real potential to flip ETH. TON, with access to Telegram’s 900M users, has become the new favorite for crypto investors.

We see a similar phenomenon in the last cycle, where quite a few smart contract platforms emerged as Ethereum killers and achieved great price performance during the bull market. The highest market cap ratio an Ethereum killer has ever achieved is around 37%, by the BNB chain, in the middle of the 2020-2021 bull cycle. Solana is currently at 21% of ETH’s market cap, with a potential for a 5X increase to flip ETH. TON is currently at 6% of ETH’s market cap and 30% of SOL’s.

Source: TradingView

From a valuation perspective, both SOL and TON are still looking cheap compared to ETH. For early ecosystems such as TON, we believe DAU is a better metric to watch than TVL or fees, as gathering users is a higher priority than making money. According to Metcalfe’s law, TON’s market cap over user metric is only 1/10 of Ethereum’s, especially given that the current DAU is still only a negligible portion of Telegram’s 900 million user base.

For a more mature ecosystem like Solana, its P/E ratio, calculated as marketcap over fees, also looks cheaper than Ethereum. We expect heighted economic activity to continue on Solana given its better blockchain performance and a thriving DeFi ecosystem. There is a real chance for Solana to flip ETH and for TON to close the gap in market cap with Solana in this cycle.

Source: Artemis, Decentral Park Capital

Top 100 MCAP Winners

Fantom (+22.76%)

Chainlink (+21.22%)

Arweave (+19.22%)

CORE (+18.19%)

Solana (+17.79%)

Top 100 MCAP Losers

Dogwifhat (-15.58%)

Worldcoin (-13.54%)

Ethena (-10.55%)

Render (-8.57%)

Starknet (-7.26%)

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.

About the Author

Kelly is Portfolio Manager and Head of Research at Decentral Park Capital. Investing across sectors with a thesis driven, deep research approach.

Prior to this, Kelly has led research and product efforts at CoinDesk Indices and Fidelity Digital Asset Management. Kelly has been a TradFi investor for 15 years before joining the crypto space.

You can follow Kelly on Twitter and LinkedIn for more frequent analysis and updates.