The Weekly #239

The Weekly #239

A key week on all fronts. Crypto slides from regulatory headlines despite the broader risk-on environment. BTC dominance has been the play for investors and is likely to remain resilient for now.

Join the 1000’s founders, investors, crypto funds, brokerage firms, and developers in getting free cutting-edge crypto research by subscribing below:

The US Warpath on Crypto

It was a pivotal week in crypto with the U.S. regulators charging Coinbase and Binance with unregistered securities exchange allegations. While there are lots of nuances, legal terms, and lack of clarity on a number of fronts, the summary is that:

Coinbase - SEC alleges the company has operated as an unregistered broker, exchange, and clearing agency arguing the company acted as an intermediary, handling orders, and facilitating bids all at the same time.

Binance - The SEC alleges the above but adds on the comingling of customer funds and that CZ was “secretly” controlling Binance.US plus CZ owning and operating an entity that was inflating Binance.US’ trading volume.

When it came to price action, markets saw a 6.5% decline following the SEC charging Binance headline-only then to a recovery of 5.7% as Coinbase was then charged - a recovery that didn’t reverse the prior losses.

On Saturday, a broad-based market sell-off continued with a further 5.7%. So far, we’ve only seen a 1.16% gain from the local bottom.

It is also unclear why a more significant retrace lagged so much after the headlines but there is evidence that sharp withdrawals of liquidity prior to the weekend crash were a key factor.

Zooming out, we can see global MCAP measures have stabilised at the ~$1T mark, although broken out of the ascending channel and $1.04T support. Chopping around such a key psychological level, for now, seems reasonable as investors continue to digest the headlines.

BTC and ETH remained relatively stable over the past week, declining 3.2% and 6.7% respectively. BTC found support at $25.4k - previous resistance in August 2022 and February 2023.

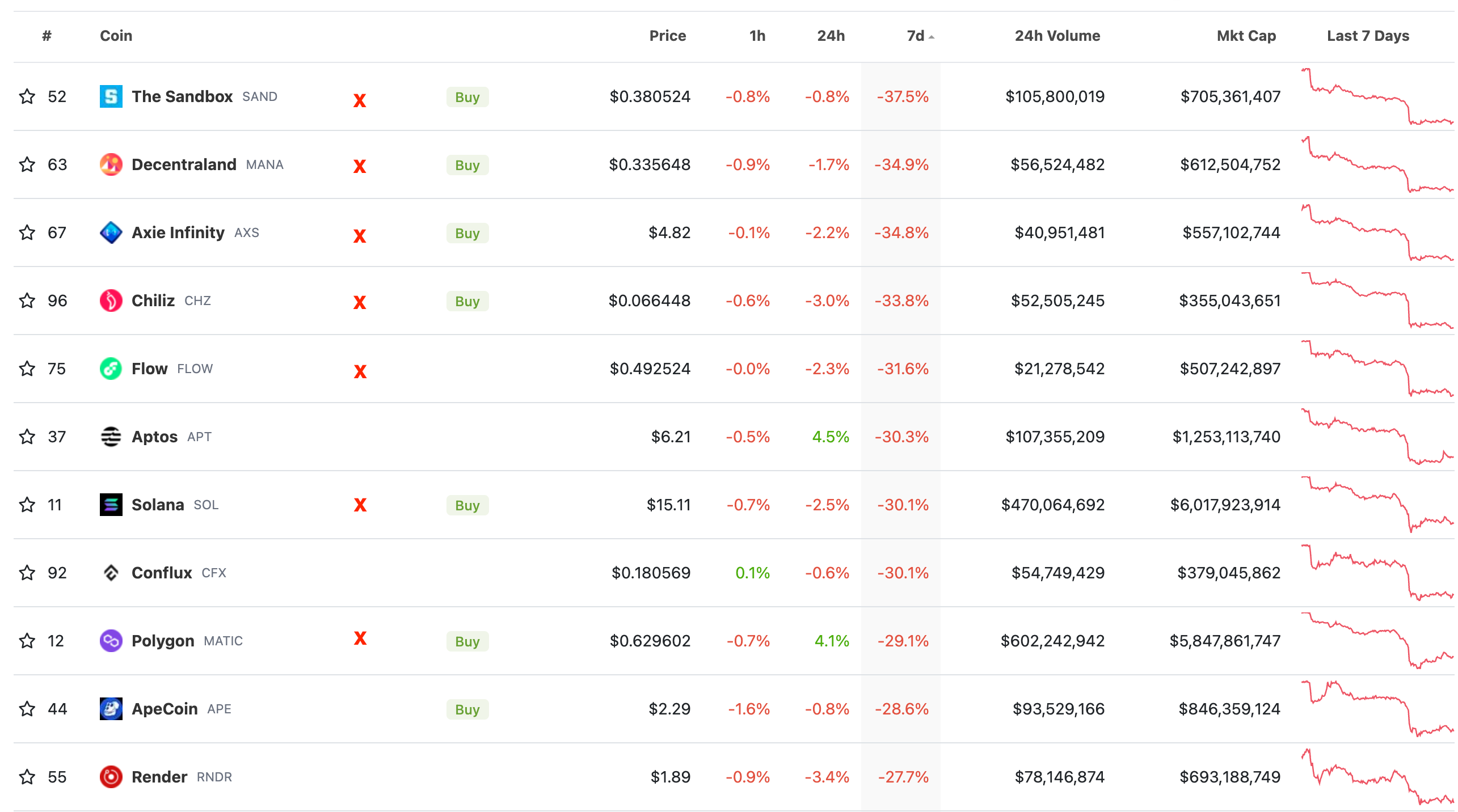

Alt coins were hit hardest with the worst-performing assets over the past week drawing down 30%+. We can see that most of the worst-performing assets were also labelled a security by the SEC in last week’s filings against Binance and Coinbase.

This suggests that de-risking by investors has been more concentrated around assets with perceived higher regulatory risk. Other assets like RNDR are retracing from their impressive run-up prior to the headlines.

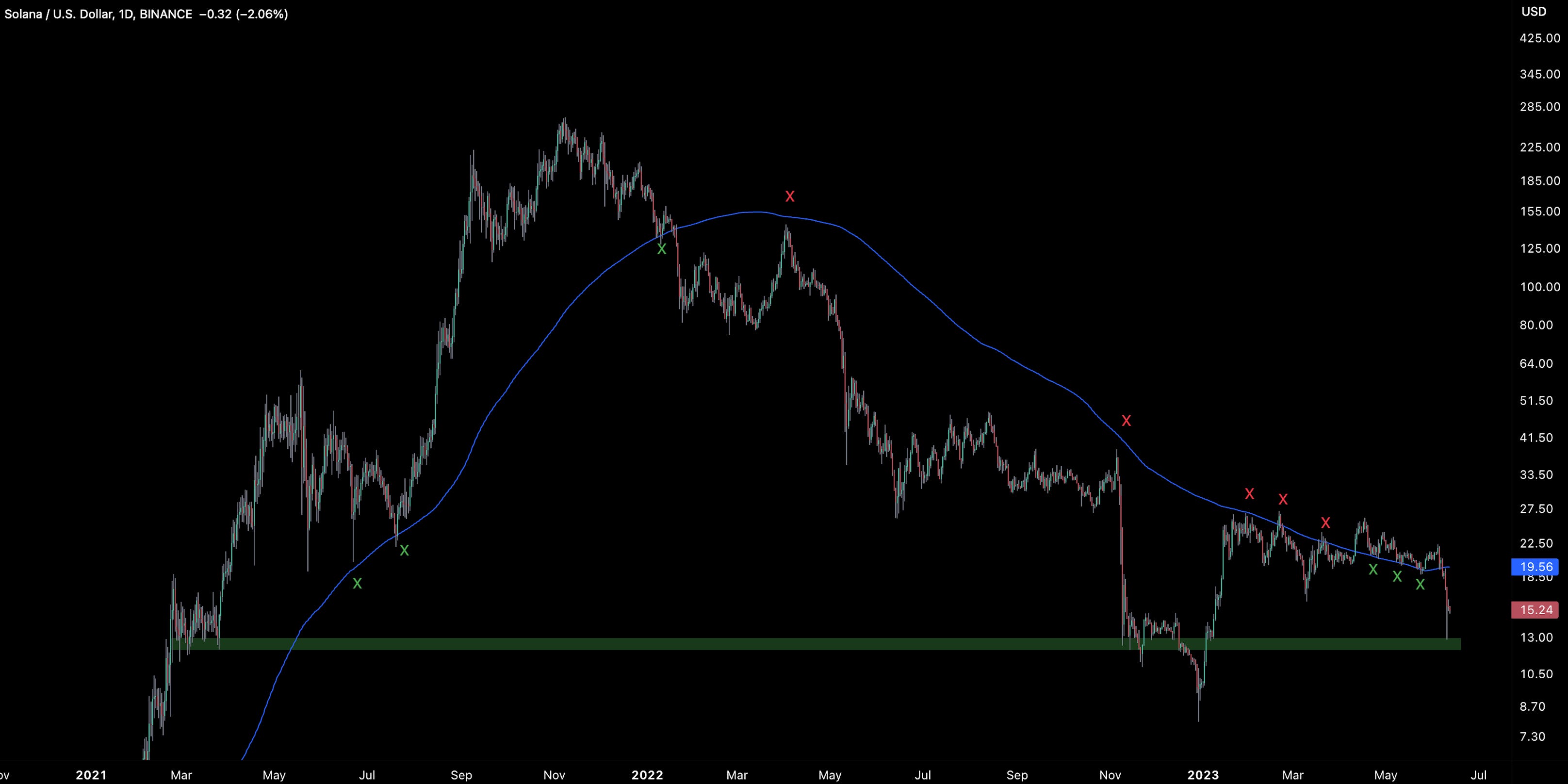

Majors like SOL, ADA, and MATIC have reversed some losses after printing new lows since early January 2023.

We see a number of examples of assets retracing briefly back down to peak fear periods in 2022.

SOL found support at $12.8 - the level found during the collapse of FTX in November 2022.

The Altcoin market (excl. BTC and ETH) declined 17% from its 200D MA to $292B - again the support found in November and December 2023.

It makes sense to think the prices collapse back to those levels but not lower (at least for now) as what was being priced during that period by investors was the collapse of the largest crypto exchange due to fraud.

While this may seem constructive, there are a number of factors that may or may not be priced in given the uncertainty.

One of them is the criminal indictment potentially coming for Binance from the US DOJ.

A second-related issue is the collapse of liquidity and/or accessibility of assets for at-risk exchanges like Coinbase and Binance due to regulatory pressures.

In numbers, Binance has an estimated ~19% of global cryptoasset market volume. The combined volume of Coinbase and Binance increases this to 21%. The exchange with the more incriminating evidence alleged against it by the SEC is the largest player by volume within the market. This comes at a time when liquidity is already extremely thin.

There is also a risk of incoming exchange de-listings making the exchanges themselves become forced sellers if their respective users don’t either sell or move assets off their platform.

One example is Robinhood (choosing to de-list SOL, MATIC, and ADA) which had ~$1.3B of assets on their platform as of March 31st 2023.

Next week specifically is also significant for a number of reasons:

The Hinmen documents in the Ripple vs. SEC battle are to be released on June 13th - these are based on a speech explaining why Bitcoin shouldn’t be considered a security. This will likely only fuel the relative strength of the orange coin further.

SEC’s rulemaking response - the regulatory body has been requested to explain why the SEC may decline a petition by Coinbase that seeks formal rulemaking in the digital asset sector.

House Financial Services Committee forming a full committee hearing titled “The Future of Digital Assets: Providing Clarity for the Digital Asset Ecosystem”. Comes after a new stablecoin bill was drafted.

While the focus on the US is for good reason, we often forget divergent jurisdictions that are becoming more welcoming to the crypto industry including regulatory frameworks. We also tend to forget about the potential for real utility within the space during these times too.

Relative Performance

Bitcoin dominance clearly shows the extent to which BTC has remained resilient since the 2022 market bottom in November. Throughout this year, we have stated that a break above the 49%-50% zone would mark a new market regime for the orange coin - of prolonged outperformance, breaking away from the cyclical trend seen since May 2021.

Meanwhile, ETH dominance falls as BTC strengths while stablecoin dominance ticks higher in a signature risk-off move.

The DeFi sector broke below its support relative to ETH following the regulatory headlines with an unclear target.

Macro

There are a number of key macro events to watch this week too including the US CPI Tuesday, the FOMC rate decision on Wednesday, ECB rate decision Thursday, and Eurozone CPI Friday.

US CPI expectations are pricing in a 4.1% YoY change in headline (from 4.9% prior) while core inflation remains sticky at 0.4% MoM. The consensus is for the Fed to pause this week.

This comes as the S&P rises >20% off its October lows - a common marker for a bull market. Goldman has even raised its SPX target to 4500 by YE with rallies extending outside of tech.

The bearish divergence of crypto to equities illustrates how sentiment is being negatively affected by the regulatory overhang during what appears to be a risk-on environment.

Dollar also ticks lower after printing a lower peak in May. Dollar weakness would normally be beneficial to BTC as the value of the denominator is falling.

Therefore, another way to chart crypto’s own rally is through Bitcoin's dominance itself. Growing risk appetite more broadly translates to growing BTC attractiveness relative to the broader market. BTC has offered the best risk-adjusted returns alongside the highest absolute returns.

The liquidity picture remains the same too. Global and US domestic liquidity measures are positively trending, not negative. And this runs counter to the consensus narrative that the TGA rebuild will quickly suck liquidity from the system once again.

While overall market liquidity could conceivably go lower, we maintain that the degree to which it could fall is relatively limited given the margin for error until financial instability is created within the system.

This would also come with the backdrop of contracting economic data, falling prices, and rising unemployment. For BTC (beta), market liquidity is the broader, slower driver for its price performance.

So to come full circle, both BTC and ETH are in unique positions where:

They appear more resilient in the wake of the recent regulatory headlines (non-securities).

Have the currency debasement narrative tailwind as dollar weakness kicks in and the RoC of liquidity increases.

The financial system instability narrative tailwinds as regional bank pressure increases from the commercial real estate sector.

Likely remain listed on venues due to point 1 (accessibility resilience).

For these reasons BTC (and possibly ETH) are more likely to maintain their dominance than to lose it - both in upside and downside market swings.

Decentral Park Market Pulse

Want real-time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

ICYMI: On Bitcoin’s Valuation

Global Market Cap

$1.026T; Crossed below the $1.04T support level and finding support at $1T MCAP.

DeFi

$35.9B; Declined 16.2% over the past week and is now 17.8% below its 200d MA.

DeFi/ETH has fallen to 17%, breaking support since May 2021. The sector remains unattractive to investors relative to majors.

Trader Positioning

BTC OI weighted funding rates remain positive (0.00363) from $26.4k to $25.6k indicating traders continue to take a predominantly bullish stance.

Positive impulse for ETH funding rates to 0.01 on Monday morning.

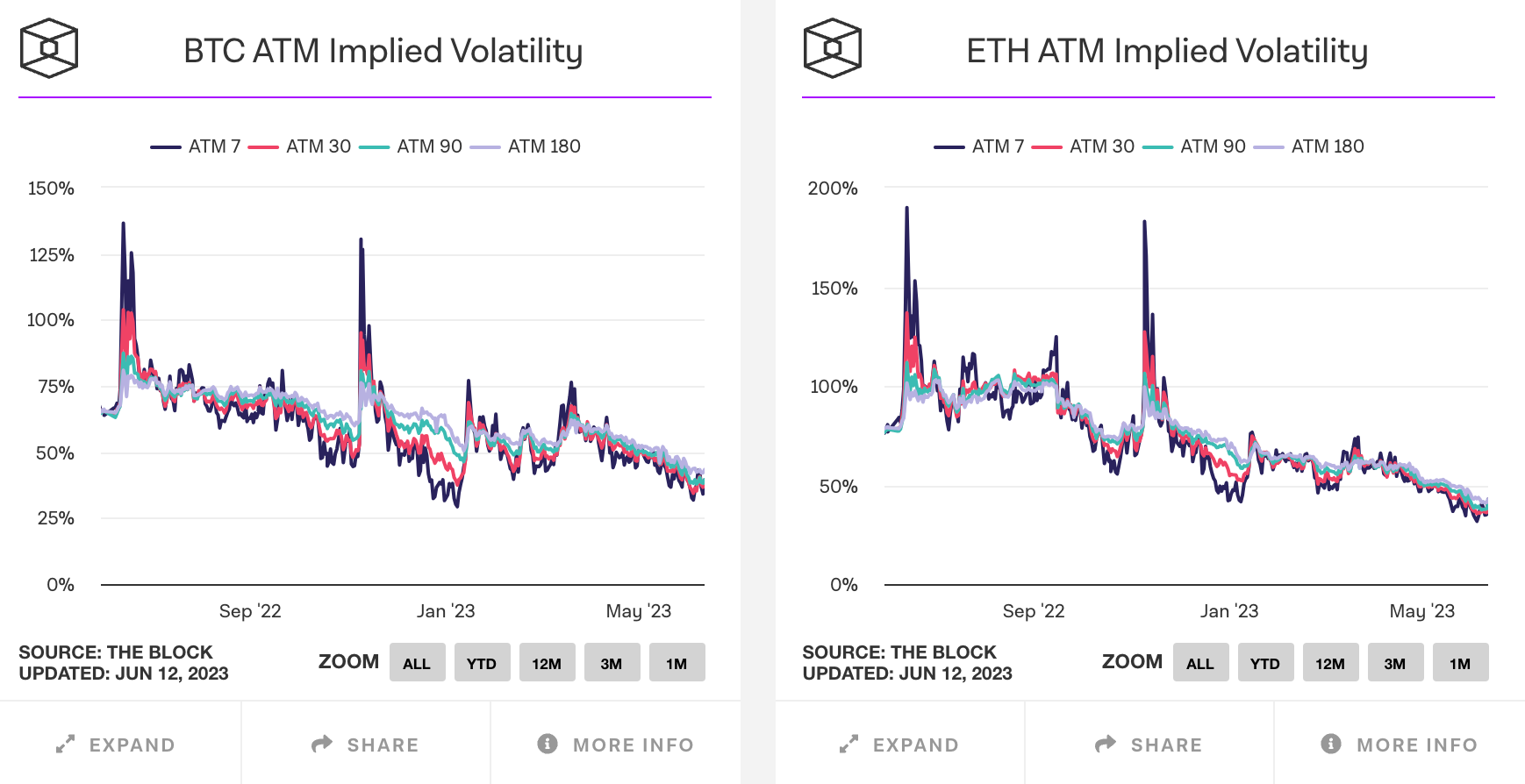

BTC and ETH implied vols continuing their grind lower and point to no signs of panic selling after the SEC filed lawsuits against the two largest cryptoasset exchanges.

Grayscale Trusts

No material change in GBTC premium as it trades ~42.3% but overall trend is a premium widening.

ETHE discount to NAV is still much wider than GBTC’s at ~54.6%. The overall trend here is also widening with little investor interest despite the relative resilience of ETH within the market.

Cryptoasset investment products saw $39m net outflows representing the 6th consecutive week of outflows totalling $272m.

BTC/USD Aggregate Order Books

Order books look slightly heavier on the bid side. Heavier resistance all the way up to $27k.

Miners

Bitcoin hash continues to climb higher with 30d MA climbing 50.2% YTD (374m TH/s).

Hashprice ticks higher as hash rate outpaces BTC spot. Overall pressure on miners starting to mount and we pay close attention to a hashprice reaching levels seen at BTC’s market bottom in 2022.

Revenue from BRC-20-related activity for miners remains low at ~2 BTC/day. Interest in ordinals has dissipated with those inscriptions providing no real utility today. This may change in the future.

We can identify potential drivers for best and worst-performing assets over the past week:

Top 100 (7d %):

GT (-2.1%)

XRP (+-2.1%)

LEO Token (-2.4%)

BTC (-2.9%)

Monero (-4.8%)

Bottom Top 100 MCAPs (7d %):

The Sandbox (-35.6%)

Decentraland (-32.9%)

Chiliz (-32.4%)

Axie Infinity (-32.0%)

Flow (-30.1%)

> UK Crypto Policy [The Block]

> 100M$ Fight for Crypto in D.C. with Ryan Selkis [Bankless]

> How the SEC Has Lost Credibility [Unchained]

> CAT Labs on Combating and Preventing Crypto Crime [On The Brink]

> Mike Novogratz on Crypto’s Outlook, Trading, & Storytelling [1000x]

> Coinbase invited to set up shop in Hong Kong after SEC lawsuit [Blockworks]

> Investing in Gensyn [A16z]

> Existential Doubt [Chris Burniske]

> Destruction of money and inflation [AndreasSteno]

> ETH on exchanges, ETH staked [ASvanevik]

Key Decentral Park Links:

> Decentral Park Research Hub

> Decentral Park Market Pulse

> Decentral Park Website

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.