Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below:

Stuck in the mud

Since June 2022, BTC has been chopping around within ‘macro channels’ with ‘micro ranges’. June-November was the $18k-$25k (green) macro battle ground. This macro channel was subdivided into two halves - defined as below or above $20k.

Fast forward to today and BTC is exhibiting the same pattern only this time the halve is $17k (a $3k drop) with a macro channel top of $18k.

It seems traders have spotted this pattern and started applying the Constanza rule. The outlook remains bleak for the near-term with it looking increasingly harder for BTC to break above the $18k level and then the previous $25k high.

Gauging risk-off behaviour

The ETH/BTC ratio has also been informative for risk behaviour by the market. The ratio has struggled to to gain ground since November with 0.076 being used as strong resistance and often been pulled back to its 200d MA - a sign that the market remains cautious and has low directional conviction.

BTC’s higher dominance over the past month is also indicative of the risk-off environment that seems persistent heading into the new year.

BTC.D has edged higher from 40% to 42% since the collapse of FTX while BTC has remained largely range-bound between $16-$18k. This signals that BTC continues to be used as a more (liquid) defensive asset vs. names further down the risk curve.

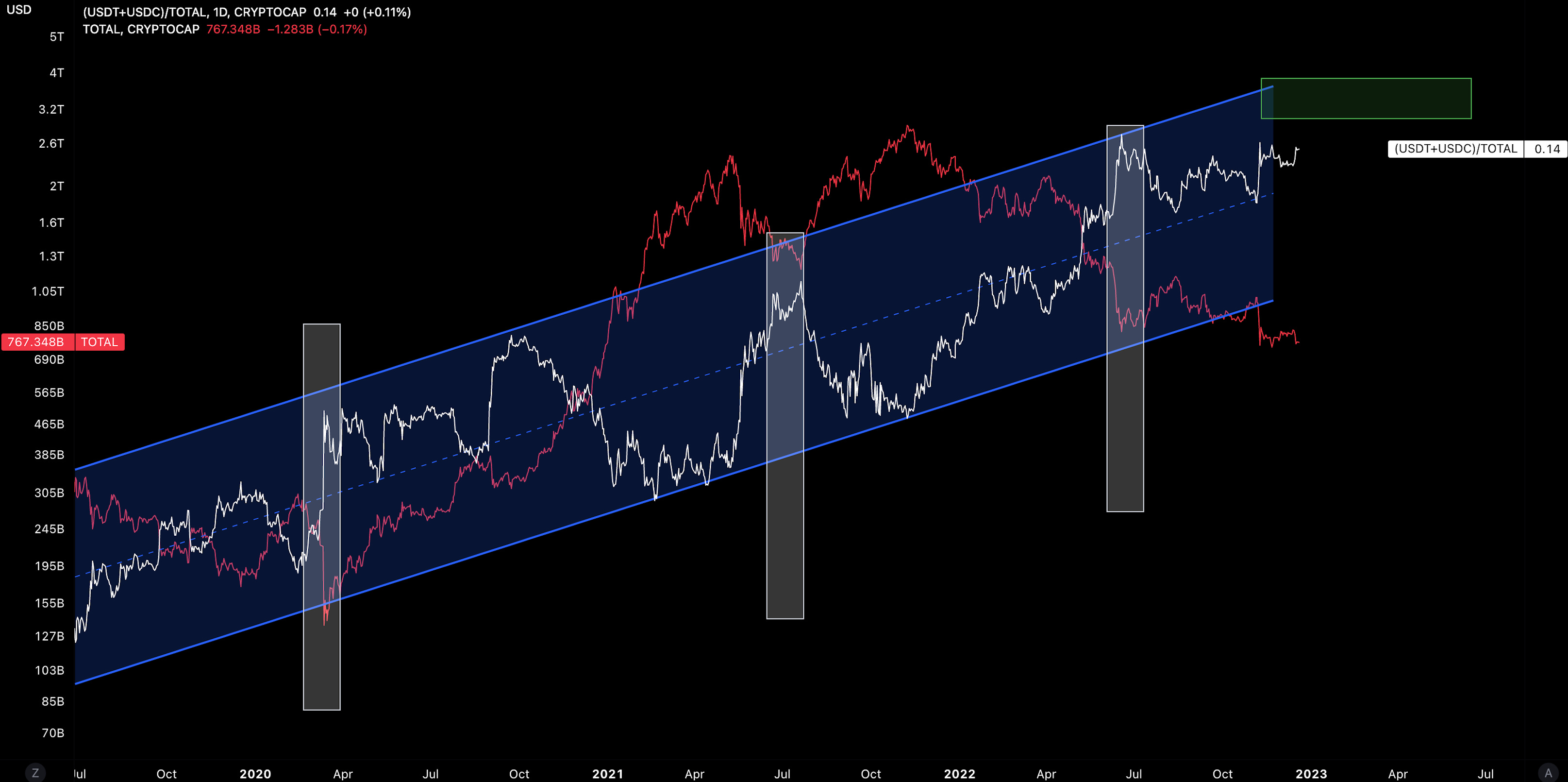

We can also look to the trend in stablecoin dominance in the market which has remained elevated for most of 2022 (14%+). Extreme moves in this metric can be useful to determine periods of market distress that provide opportunities for long traders.

Every spike often coincides with local market bottoms. Crypto may be in deep value territory now but more extreme prints to the upside for stablecoin dominance provides a higher conviction signal for allocators to start deploying.

Analysis on specific sectors also show the extent of risk-off appetite.

For DeFi, the sector is in a vulnerable position as can be seen by the DeFi/ETH ratio which is breaking down below multi-year support (22%).

Technicals like D RSI indicate a short road to oversold levels but these signals have been poor leading indicators for broader market trajectories. What has been more impactful has been the persistent regulatory risk overhang and lack of retail interest even at relatively cheaper levels.

A weak DeFi/ETH chart coupled with ETH being a more defensible asset vs. regulatory considerations (securities) means the higher cap name has become a relatively more attractive play for many.

At the same time, it’s also providing an opportunity for other opportunistic investors to allocate to decentralize networks over corporate networks at more attractive levels.

Risks in the market

One of the growing concerns in the market today has been centred around centralized exchanges, including Binance which, after a series of interviews, has raised more questions than provided answers.

Sharp withdrawal increases by the market from the centralised exchange has ensued with ~90k BTC leaving so far in December (net outflows). Binance’s BTC balance is now 15k below levels seen during the FTX collapse.

Total assets held in Binance wallets was $69.5B 1 month ago but has since declined by 21% to $55B.

The specific concern is not necessarily related to customer deposits (although the chances of clear audits in the future are looking unlikely) but the potential $2.1B clawback from FTX. If Binance is unable to handle such a clawback, then it would likely either imply the exchange is illiquid and/or they had a set of losses to offset their FTX investment gains.

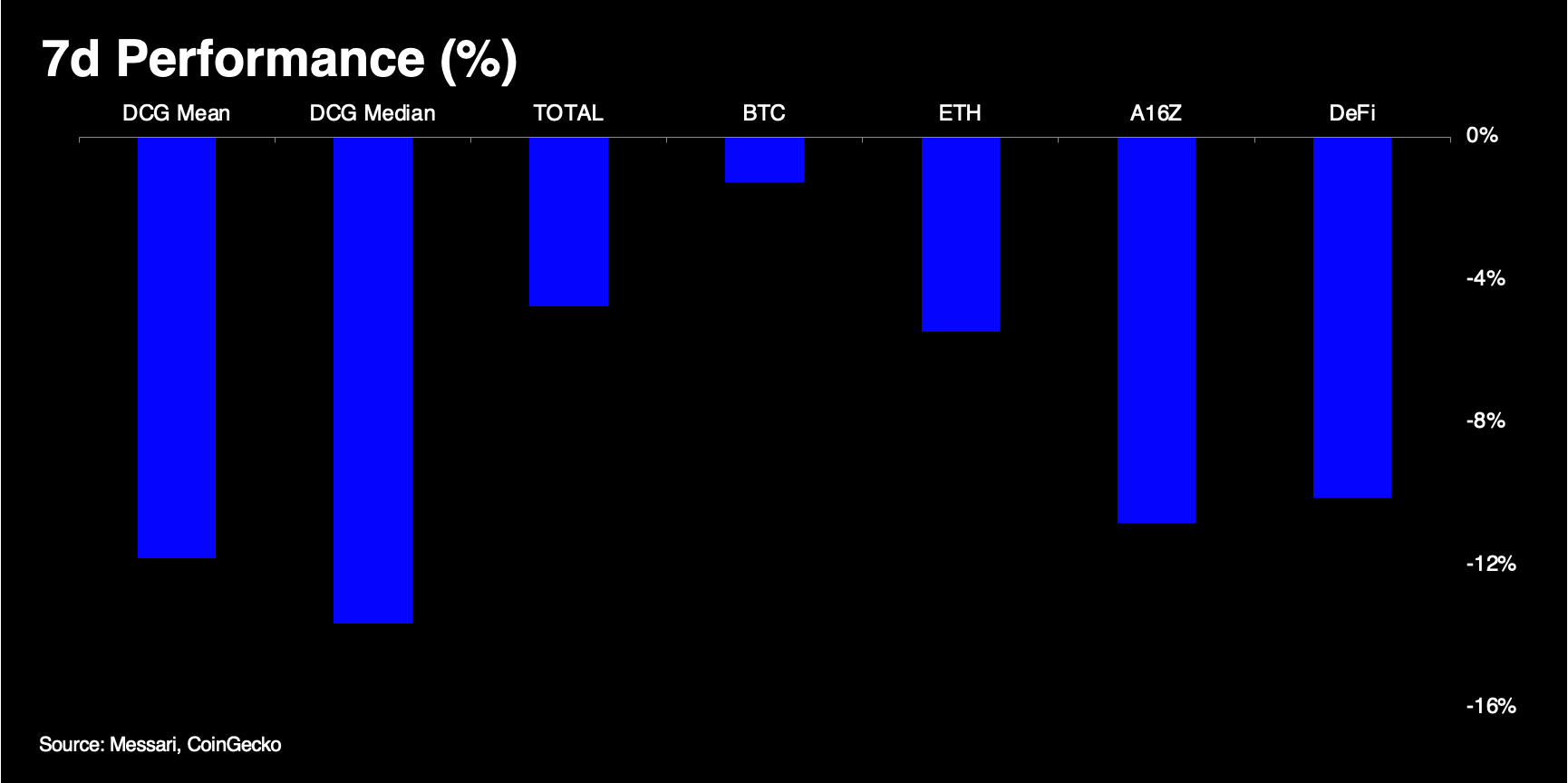

The other concern relates to DCG who owns key operators such as Grayscale and Genesis. Just last month, Barry Silbert revealed a $2B debt in a shareholder letter, driven by the continued fallout throughout 2022.

There is now evidence that DCG has started to liquidate their liquid portfolio in order to recapitalise. Over the past week, DCG liquid portfolio has, on average, performed worse (-12%) than market beta, sectors like DeFi, as well as other fund portfolio like A16z (-10%).

Key names like Filecoin and Flow were hit hardest, declining 26% and 17% over 24 hrs on the 17th of December.

Asset drawdowns are likely a result of forced selling and/or the market frontrunning the forced selling by DCG. It is less likely due to low utility or changes in the respective network’s fundamentals as some have reported.

The problem here is that falling asset prices means DCG’s valuation also declines (net equity) while the liabilities stay the same. In other words, lower valuations coupled with more time creates more risk for a creditor workout. It maybe no surprise that a dark market for claims is allegedly forming.

DCG’s selling may also colour NEAR’s persistent underperformance vs. the broader market over the last 6 months. NEAR is now down 93% from its ATH is January 2022 ($20.8). NEAR’s sell off is so prominent that it has been selling off harder than SOL over the past week relative to the broader market.

In April 2022, Barry Silbert revealed that NEAR was the 3rd largest holding in the DCG liquid portfolio.

NEAR’s performance relative to the market also looks eerily similar to GBTC’s premium to NAV which now stands at -48.6% (ATL). Recall that DCG has levered exposure to GBTC. A higher discount to NAV in a sideways/down market is the opposite of what DCG needs or wants.

A driver in new interest may stem from Grayscale looking to return up to 20% of its Grayscale Bitcoin Trust’s capital to shareholders if a spot ETF conversion fails. However, a timeline has yet to be defined. It is also not clear how this would affect other dominant products like ETHE.

Macro

Markets seem to be coming to terms with the ‘higher rates for longer’ narrative and its implications. Higher chance of recession, lower corporate earnings, higher unemployment, lower commodity prices, and lower equity valuations.

Last week’s 2% decline in $SPX marked a 2nd consecutive week of weakness, falling further below the technical area of interest - the 200d MA. The expiration of $4T of options had likely added turbulence to the highly volatile week.

There are concerns that quants will now be needing to offload up to $30B of stock futures due to the higher downside volatility of equity benchmarks, causing price to tumble even further.

Morgan Stanley became more bearish in their 2023 forecast, pointing to a sharper decline in earnings ($180/share) against an equity premium that is currently lower than in August 2008 (despite valuations being higher).

Their forecast equates to a 3,000 point $SPX which marks a 22% decline from last Friday’s close.

The other north star for equities is Fed Net Liquidity which remains highly correlated with equity performance.

With the Fed sticking to its $95B QT unwind, there is likely further downside risk for equities heading into the new year. This would be net negative for crypto even without considering its own intra-market risks.

Meanwhile, DXY (dollar gauge) is approaching key support of 103 and we could see a corrective move higher. The conviction on this would increase the more technicals like W RSI fall closer to oversold levels (30). This corrective move higher would tie in with further weakness in risk assets like equities and crypto.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Global Market Cap

$767B; Global market fell +4% over the past week. Finding initial support at the bottom end of the channel range ($760B). Limited technical support until $680B (-11%). No RSI divergences on the daily or weekly.

DeFi MCAP

$32B; DeFi MCAP declined 11.5% last week (-$4B) largely due to negative sentiment around centralized exchanges (i.e. Binance) coupled with forced selling/frontrunning of forced selling by DCG.

Bitcoin Dominance

42%; Bitcoin dominance sticking higher as the asset becomes more defensible in a increasingly skittish and concerned market. Every bounce from support (39%) over the past 2 years has resulted in Bitcoin dominance surging to 48%+ before its larger correction downwards (next cycle). Implies further relative strength for the orange coin.

Trader Positioning

Aggregate funding rates for BTC slightly positive (0.0001%) while ETH is slightly negative (-0.0001%) signalling a divergent view on both assets.

No material change in BTC and ETH futures OI ($5.3b vs. $4.8b respectively).

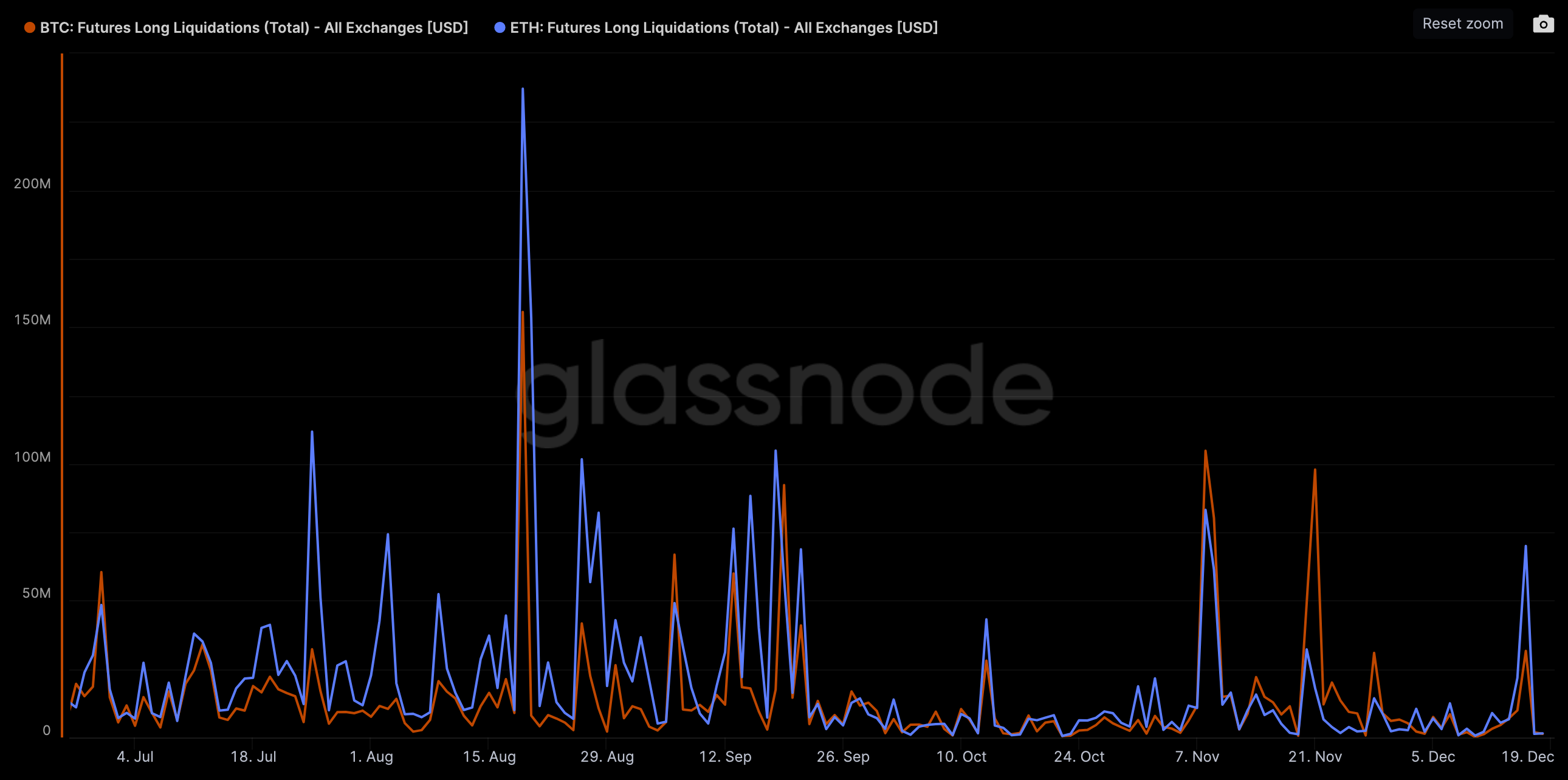

We saw a spike in long liquidations for both ETH and BTC on Friday (16th December) with a more pronounced spike for ETH ($70B vs. $31B). No doubt helped drive underperformance of ETH vs. BTC over the period.

Grayscale GBTC

GBTC discount to NAV printing a new ATH (48.89%) before narrowing slightly to 48.57% to finish the week. 30D average volumes climbing to new highs since July 2022 (7m) indicating larger players selling shares over the past month against little buy interest.

ETH discount to NAV printing new ATH last week too (-53.56%). 30D volumes at highs since August 2022 (4.4m).

Volumes

Daily exchange volumes bouncing off annual lows ($11.74B) right on cue. Repeat pattern of lower highs and lower lows over the year.

Aggregate Order Books

Order books look heavier on the bid side. Heavier resistance up to $17k.

Miners

Bitcoin has rate has fallen 9% from its peak on December 13th, 2022. Next difficulty estimate is +3.64% meaning miners will find it relatively harder to find the right hash for each block.

No clear theme across top performing names. Toncoin is now ranked above Avalanche and Chainlink by market capitalization.

Top 100 (7d %):

Toncoin (+30.8%)

XDC Network (+12%)

OKC (+10.7%)

OKB (+3%)

Bitcoin SV (+1.3%)

DeFi Top 100 MCAPs (7d %):

bZx Protocol (+140%)

Tellor (+6.2%)

Olympus (+4%)

Dopex (+2.3%)

Dopex Rebate (+0.6%)

🎙️ The Three Risks Left For Crypto [On The Margin]

🎙️ Smart Money Finds Opportunity [Empire]

🎙️ Where Things Stand Now With Inflation and the Fed [Odd Lots]

🎙️ Modular Execution Blockchains [Epicenter]

🎙️ Weekly Roundup [On The Brink]

📚 Crypto Options Market Has Become More 'Interdealer' Since FTX's Blowup: Paradigm [Coindesk]

📚 Warren’s Reactionary Crypto Policy vs. Dorsey’s Decentralized Social Media Gambit [Coindesk]

📚 On MEV [Dan Robinson]

📚 The Next-Generation Uniswap For Real-World Commerce? Pointswap Brings Popular Beauty and Fashion Brands To Web3 [The Block]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.