Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below:

Halloween Rally

Crypto has had a positive week, gaining 8.25% and topping out at the $1T mark.

Contentious periods for the market can often be identified by its ‘battle’ against the 200W MA where the markets are now back above the key line.

Global MCAP has now broken the wedge formation to the upside and signals a period of bullish price action.

Last week’s move was met with a rally in aggregate daily exchange volume, topping out at $23.5B. Nothing too surprising here. We can see YTD that these peaks are not unusual signifying periods of renewed interest.

What may be more useful is if we see a return back to the overall YTD trend of new lows and more muted peaks or if October marked the lows for volume.

BTC/USD hit $21k resistance finally breaking above the $20.5k level we had been so used to since September.

For the bulls, the orange coin broke out of its wedge pattern to the upside and potentially marking a period of bullish action.

ETH stole the show for the first time since the merge, printing a 16% gain for the week. ETH/USD kept long-term support and all eyes will be the ratio being able to break convincingly above its 200d MA for the first time since July 2021.

ETH’s relative strength drove the ETH/BTC ratio to new highs since the merge in September (0.077572).

Bulls are quick to point out the key levels breaking on the longer-term charts (monthly).

BTC’s dominance has fallen back below 41% as ETH’s dominance climbs closer to 21%. Key support for ETH’s dominance was held since September while BTC struggled to break past 42% which had been relatively easy for every bounce off of the lows.

Perhaps the signals for a change in the guard were there.

Realized vol has also plunged to new lows despite the recent action. Bitmex’s 7D vol has now collapsed to 13.24 and higher vol move is still very much on the cards. Has anything actually changed yet?

However, this rally didn’t feel like previous bull market rallied. ETH’s strength was also seen against alternative smart contract blockchains. ETH managed to outperform every high cap name in this bucket apart from ATOM (which outperformed ETH by ~2%).

Those positioning for capital to simply flow down the risk curve are likely to have been surprised.

One reason could be the continued influence of derivatives on price action. For example, ETH short liquidations totalled $272m on 29th October while other $3.4m was printed for SOL on the same day.

That said, the dominance of cash margined futures OI over crypto margined has been climbing which reduce the probability of amplified liquidation cascade.

Looking ahead for the next few weeks, we may now see a re-rate in alternative L1s where traders perceive of price dislocation between these assets vs. ETH.

DeFi’s dominance vs. ETH was also questioned over the past week. Again, this is unlike previous rallies where DeFi has historically performed well on an absolute and relative basis during broader risk-on periods.

These data points signal that these are bounces from lows but the classic hallmarks of ‘altszn’ are nowhere to be seen yet.

Halloween Pump - A Time To Reflect On The Terrifying Reality

Crypto have largely been mirroring the gain seen in equities for the past weeks. SPX has now bounced >11% since the new 2022 lows and it seemed that risk-on sentiment around the mid-term elections is picking back up.

Then, over the weekend, GS raised the Fed’s interest rates to 5% (75 BPS this week, 50 BPS next week, and 25 BPS in February).

Citing the need to tackle ‘uncomfortably high’ inflation, the narrative may now shift once again from recession risk to price risk.

The picture is murky for risk assets like equities. The current rally indicates a recognition that the markets think current levels are becoming more constructive. After all, we’ve now seen the ‘big hit’ on growth tech from the Fed’s restrictive policy.

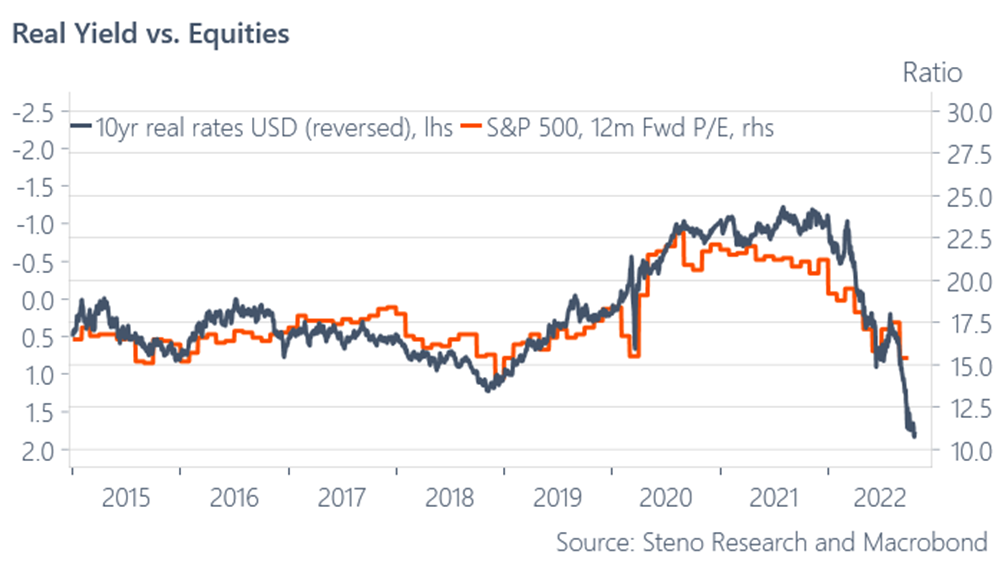

At the same time, real yields continue to rise that may suggest any rally we see is ultimately doomed. Real yields currently put S&P 500 12m Fwd P/R at ~11.

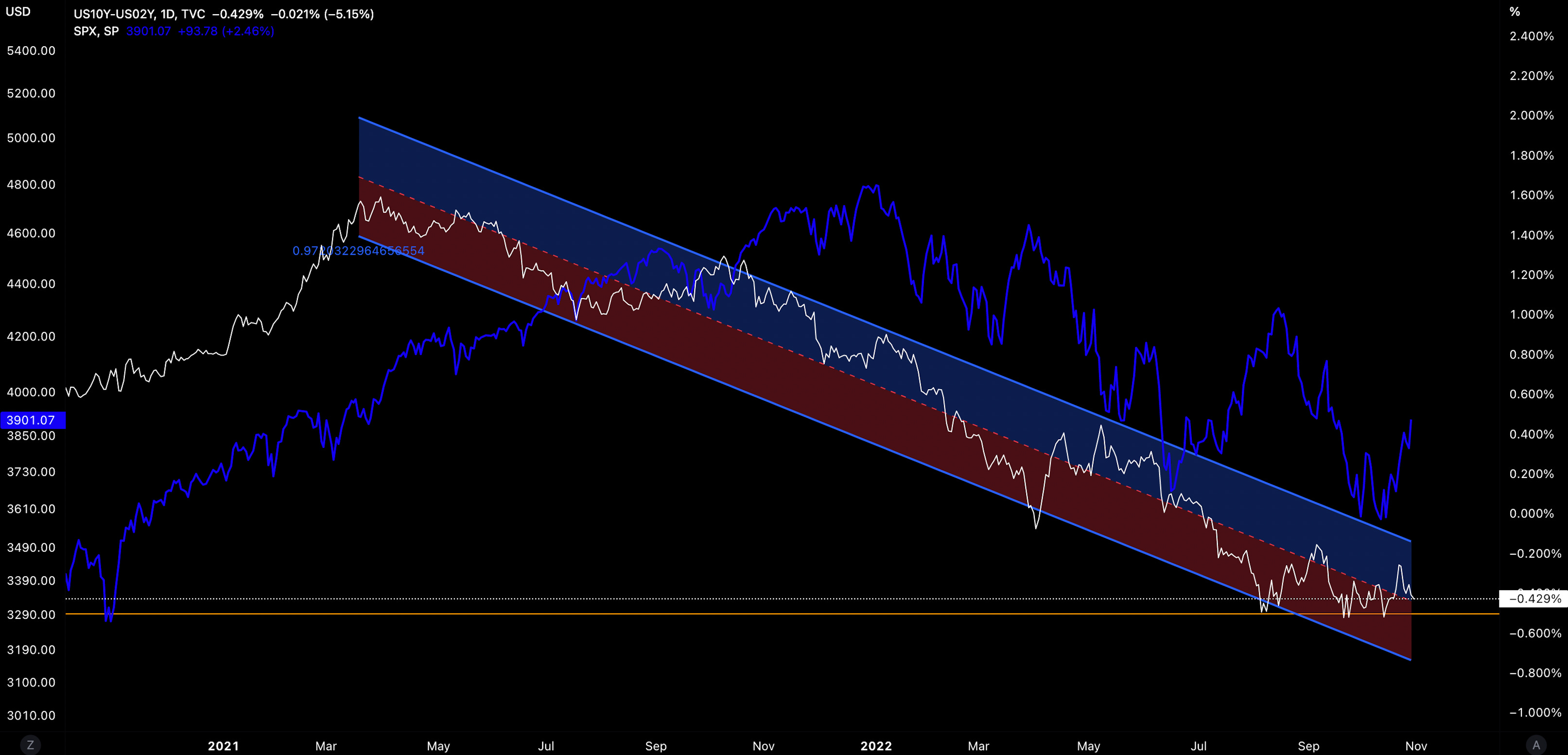

We can also see the US10-2 yield curve becoming more inverted at a time when equities are seeing green. Confirmation of a recession ahead is providing cold comfort for investors who now see reasons for the Fed to take their foot off the brake.

Net liquidity measures is the only scare you need this Halloween. Net liquidity currently prices SPX at 3750 (a 4% decline from current levels).

That said, several rallies this year have printed higher deviations from liquidity (~350pts) implying that this rally could top out closer to 4100 (+5% from current levels).

The problem for the Fed is that the hit on the real economy has not been too significant.

U.S. economics growth has stayed resilient while the labor market remains robust. Large savings in the US has buffered individuals where consumer spending actually increased 0.6% in September. And yet markets are now tagging onto the idea that the Fed will need to slow down the pace of its rate hikes. There is no doubt, the Fed will have to do more.

Labor market weakness is what will matter for the Fed. That is unless ‘something breaks’ requiring central banks to take decisive but opposite action to what they have been doing YTD. The alternative scenario is when disinflation trends get clearer and clearer (and face increasing pressure from the political camps).

It is only when unemployment rises substantially will we see prices fall substantially. Higher unemployment > recession > lower prices.

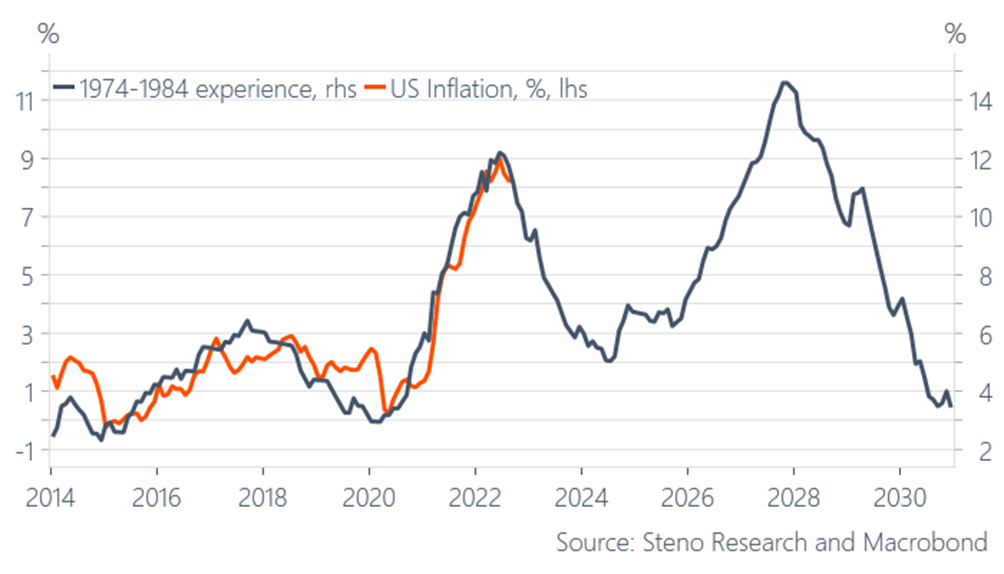

As Andreas Larsen highlights:

“We have never had inflation running at current levels without experiencing a so-called double top inflation regime. That was the case in 1974-1980 and in 1946-1951…Markets will consequently likely try and chase the zero time value of money narrative once more over the next few years, before the next inflation wave kicks in. The smart investor ignores it and ensures that the portfolio is sufficiently inflation protected for the decade ahead.”

So while markets are preempting what the Fed may do, it is also creating a more accommodative environment overall. This only gives the Fed more reasons to not take its foot off the brake sooner.

So where do we stand? It is reasonable to expect the Fed to indicate the slow down of rate hike pace into December. The risk here is to not conflate this pace slowdown with not needing higher rates overall. An extended period of elevated rates will still be very challenging for risk assets.

When it comes to crypto, we are at or approaching several key levels. If we beak above or below these key levels, both outcomes all will be telling.

For now, it looks like risk is back on the menu for many who have missed out on performance for several months at this point. How long until this rally fades is another question altogether and may become the market’s ultimate trick or treat.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Global Market Cap

$983B; Global market cap gained 8.25% last week and has opened the week positive too (+1.16%) adding to conviction we could be entering a bullish period after breaking the wedge pattern to the upside. Eyes on climbing above the 200d MA.

DeFi MCAP

$46B; DeFi market cap has increased 9% over the past week and looks to reclaim the 200d MA too.

Bitcoin Dominance

40.4%; BTC dominance collapsing back to 40% as strength in alternative assets (i.e. ETH take charge). RSI now oversold and next signal will be bullish divergence on the daily or weekly.

Trader Positioning

BTC-denominated and USD-denominated futures OI starting to decline. BTC-denominated OI fallen by 100k since October 25th. Shorts that blew up over the past week with limited new OI being added since.

Aggregate perp funding rates remain moderately positive indicating overall bullish trader positioning.

Term structure in state of contango heading into FOMC meeting (futures price higher than spot price).

Decline in BTC options OI put/call skew.

ETH also seeing growing funding rates indicating stronger conviction by traders of bullish price action ahead.

Grayscale GBTC

GBTC’s discount to NAV has widened from 34% to 36% over the past 5 days and is still kept within the descending channel.

Grayscale ETHE

ETHE’s discount to NAV has kept flat over the past 5 days at 31.9%. 30D volumes have also kept flat over the past week.

Volumes

Daily exchange volumes have spike to $25B but unclear if YTD trend will continue. BTC-denominated transfer volume is low but bouncing off its lows since July 2021.

Aggregate Order Books

Order books look fairly even on both sides. Heavier resistance up to $21.2k.

Miners

Bitcoin hash rate (3d MA) has spiked to new ATHs. 272 TH/s while difficulty has increased to new ATHs. This comes at a time when miners face higher energy costs and more muted price action for BTC/USD.

BTC/USD trading below its production cost for sustained period of time has driven a 2nd capitulation event for miners who face being cash flow negative alongside limited financing availability.

Top performers seen largely in mid-cap names but liquidity remains very thin with some names below printing no more than $3m/daily volume (Covalent).

Top 100 (7d %):

Dogecoin (+103%)

Tokenize Xchange (+54.1%)

Klaytn (+49.3%)

Osmosis (+32.1%)

Mina Protocol (+29.0%)

DeFi Top 100 MCAPs (7d %):

Dopex (+35.9%)

Osmosis (+32.0%)

Dopex Rebate (+28.2%)

Covalent (+26.9%)

xSushi (+24.1%)

Gearbox LM program is launched for DAI, USDC, WETH, WBTC and stETH. LPs can earn up to 12% on stables and 14% on ETH,

Synthetix treasury is co-incentivizing the SNX pool on Hop with OP tokens. Total APR is 36% in OP and HOP.

Harbor, a stablecoin protocol on Cosmos, announced HARBOR airdrop to Stride's stATOM / ATOM pool LPS.

Oasis launched AAVE StETH/ETH earn strategy with 3.5x max leverage, annualized APY for the last week is 13.60%.

📚 AAVE on zkSync [Blockworks]

📚 UK Winter Is More Likely to Be Colder as Energy Fears Grow [Bloomberg]

📚 ETH validators post merge [pintail]

📚 DeFi Lender Arco Protocol, Launched on Aptos Blockchain, Goes Dark After Botched Fundraise [Coindesk]

📚 Huobi Stablecoin Plunges 70% as Justin Sun Readies Tron Replacement [Blockworks]

🎙️ Big tech Wreck As Earnings Disappoint [On The Margin]

🎙️ Weekly Roundup [On The Brink]

🎙️ Backing stablecoins with mortgages [The Scoop]

🎙️ On Sei Network [The Block]

🎙️ Mango Markets Hack and The Ethics of the Event [Unchained]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.