Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below:

A New Market Structure

Crypto markets have come under some more pressure over the past week with global MCAP down 1% or 24% below its August 2022 peak. Before we dive into the state of affairs there, let’s recap on the key developments over in macro.

Central banks around the world have continued to push the ‘fight inflation’ narrative through their blunt instruments. The Fed and ECB raised rates by 75 BPS at the September FOMC meeting while some have done this in parallel with quantitative tightening (reducing central bank balance sheets).

We are now seeing the dramatic impact these operations are having on the market. This includes the bond market (e.g. US) where market volatility is now higher than volatility over in the equity market - a dynamic far from ‘normal’.

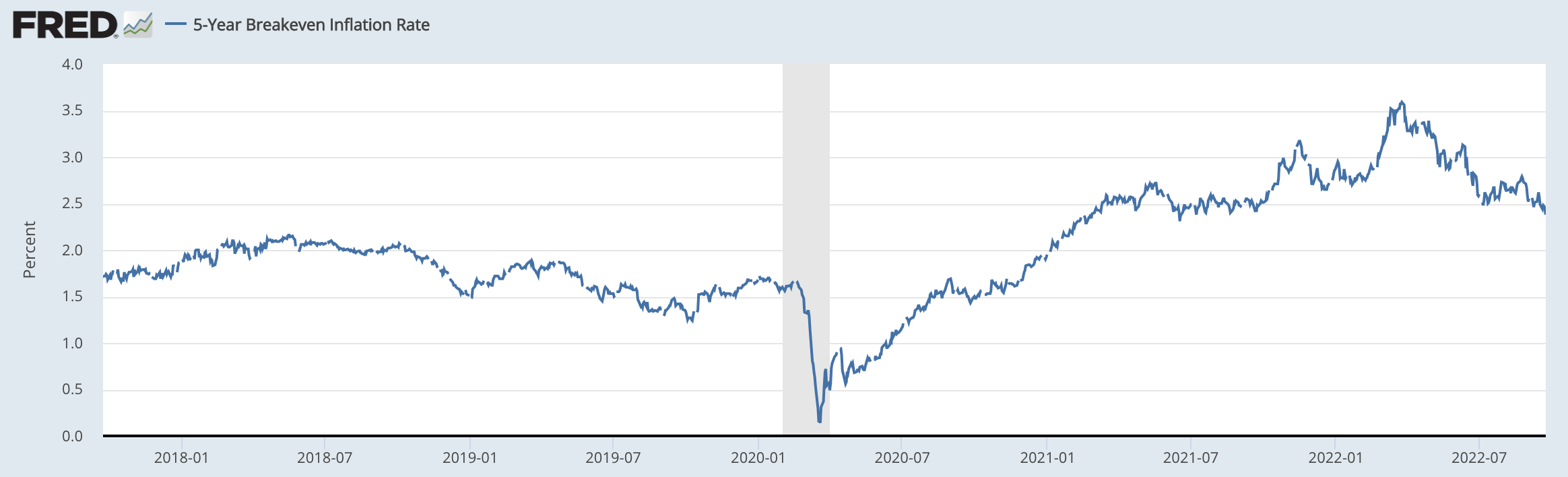

Forward looking expectations of inflation (e.g. 5-year breakeven inflation rate) appear to be broadly in line with the Fed’s attack on higher prices.

Bond yields continue to edge higher while those inflation expectations continue to go down. In other words, there are simply no buyers in the bond market.

US real rates measures have soared at their fastest past on record. Why is this important? Three main takeaways:

The raise of real rates on people and companies when debt loads are already significantly high. Note - loans can adjust with broader market akin to variable rates for mortgages.

Stocks looks less attractive for investors as real rates continue to surge.

Technology companies that were often discounting cash flows using negative rate models now have to adjust to positive rates. Higher valuations in the high growth sector now looks much less attractive.

To sum the problem: central banks is now needing to cap prices by keeping interest rates elevated at a time when liquidity is becoming tighter and debt is becoming higher.

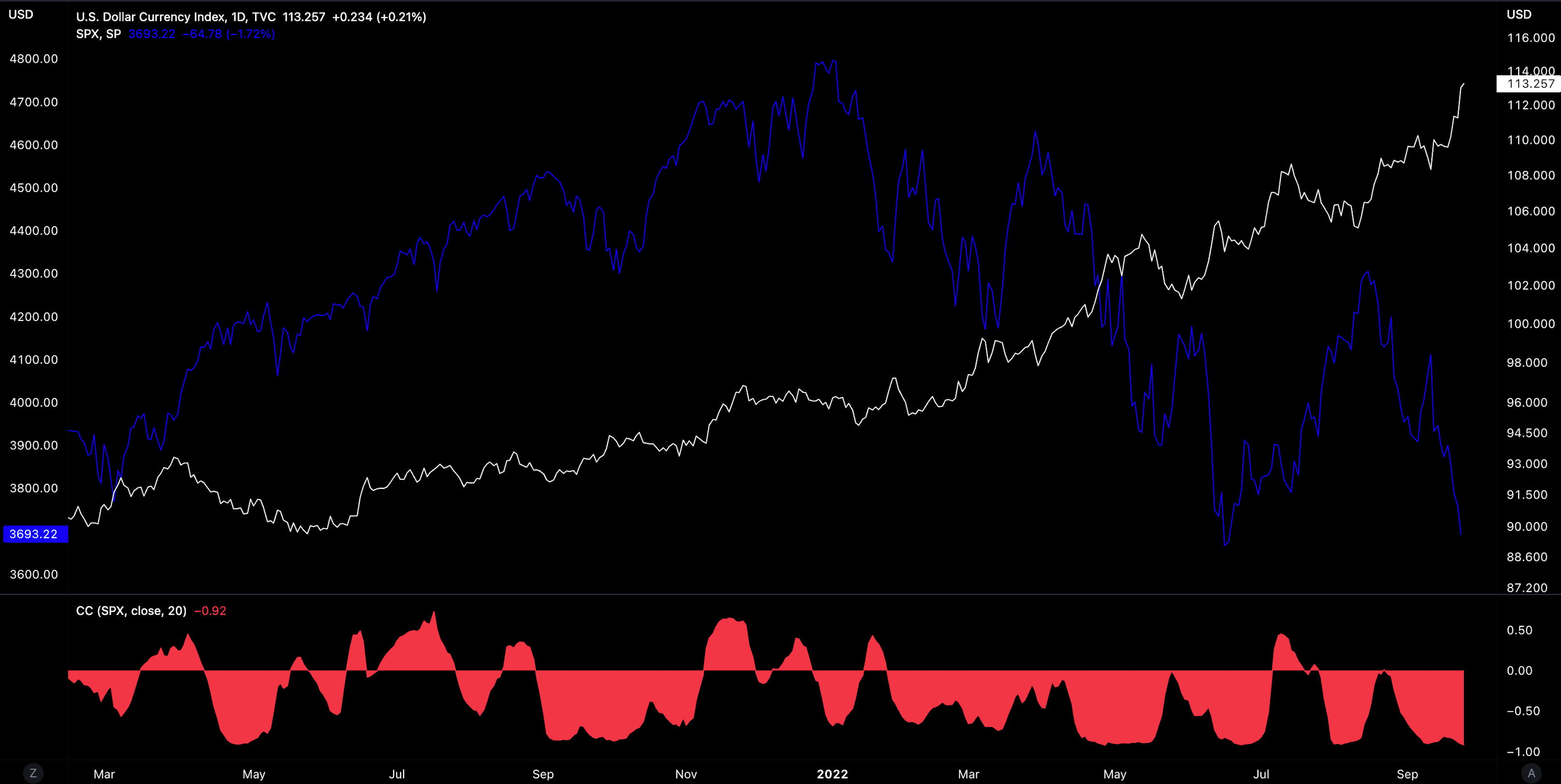

Add dollar strength into the mix and we have a the perfect cocktail for a market disaster. Dollar gauges continue to surge to new highs since June 2022 and the impact on stocks is clear - an overall negative correlation.

Why? Dollar strength coincides with negative effects on assets prices. These include: tighter monetary policy (higher cost of capital), tighter liquidity (access to capital), and impact of higher inflation (PV discount rate).

Without clear market intervention by the Fed, this relationship is likely to continue. As I have written extensively so far this year, stocks will come under much more pressure with corporate earnings adjustments being the umbrella driver.

Keep Calm And Carry On

UK fiscal policy has done little to build confidence for both domestic and foreign investors. The new government have prioritised the side of growth (vs. price) by introducing large tax cuts and energy bill subsidies at a time when prices have risen to 14-year highs. The fear by investors is higher government borrowing and higher disposable income.

The response has been nothing short of bleak with the pound now falling to its ATL with the dollar.

The impact? The market expectation is the BoE to be very aggressive in raising rates by 150-200 BPS by November. Accelerated monetary policies will make conditions worse, faster.

But this is a crypto newsletter. Why is all of this important? Zoom out.

There is now an incentive for central banks to increase rate at equivalent or a more accelerated rates compared to others.

The problem in the UK highlights the difficulties when the treasury and central banks are not aligned. Pound’s weakness is really just dollar strength. Currency devaluation is only going to add pressure to prices for countries outside of the U.S.

However, currency strength also has its own issues. On the U.S. side, there is alignment between the treasury and central banks but its’s accelerating market dislocations as mentioned above (albeit for different reasons).

The Fed’s QT has meant is no longer buying bonds that has historically propped up the market and enabled its large spending spree.

Put simply, the dollar milkshake continues to be drunk and dollar strength is headwind pressure for cryptoassets.

So it seems you either have currency weakness which fuels higher prices and interest rates for that respective region or you have dollar strength which, in today’s market structure, signifies risk-off mentality.

There are only two ways for the cryptoasset market to reverse from this market mess:

Central banks pivot. Note - this can mean a spectrum of outcomes but includes no more rate hikes. Perhaps politically-led with mortgage rates and unemployment on the rise.

The cryptoasset market decouples from broader risk market altogether

For the former, it is possible central banks like the Fed will overextend on their mission to tackle price with the risk being impractical debt payments and unnecessarily high discount rates for growth equities for years.

Of course, the flip side here is risking inflation no longer being capped at the desired level of 2-3%.

For the latter there is little evidence of this happening. That said, crypto MCAP denominated in NDX has been largely flat over the 3 months and particularly in the last week. Crypto is moving approximately in line with NDX but not worse (high beta).

The skeptic will rightfully point out this can just be noise with the majority of data points suggesting a positive relationship between Crypto MCAP/NDX and NDX itself. Time will tell if we are entering a new regime but for now the signals are interesting but not yet telling.

So where do we go from here?

The bond market may still be the best north star for investors but significantly lower liquidity means at best signals may be harder to obtain and at worst misleading.

Using deviation from trend analysis for key metrics such as for the US02Y-US10Y spread may be useful.

Others may look at how far equities may need to mean revert as a function of the fed balance sheet.

For now, it appears that risk assets continue to face material macro headwinds over the coming months. How crypto responds to this dynamic is TBD.

However, the current pace of the global bond market ‘unravelling’ is significant.

Raised rates while national debt grows is an unsustainable path longer-term. Something will have to give.

So how far can the market push things over the edge before central banks step in?

That is the big question.

Cryptoassets

BTC has managed to keep above $19k despite being a red week for the assets. Technicals point to a possible inflection point in 1-3 months.

Meanwhile, ETH has clawed back above $1.3k after the asset were sold off hard post-merge.

The key trend to watch is BTC dominance. As we highlighted in early September, technicals and the macro meant playing to Bitcoin’s relative strength became attractive.

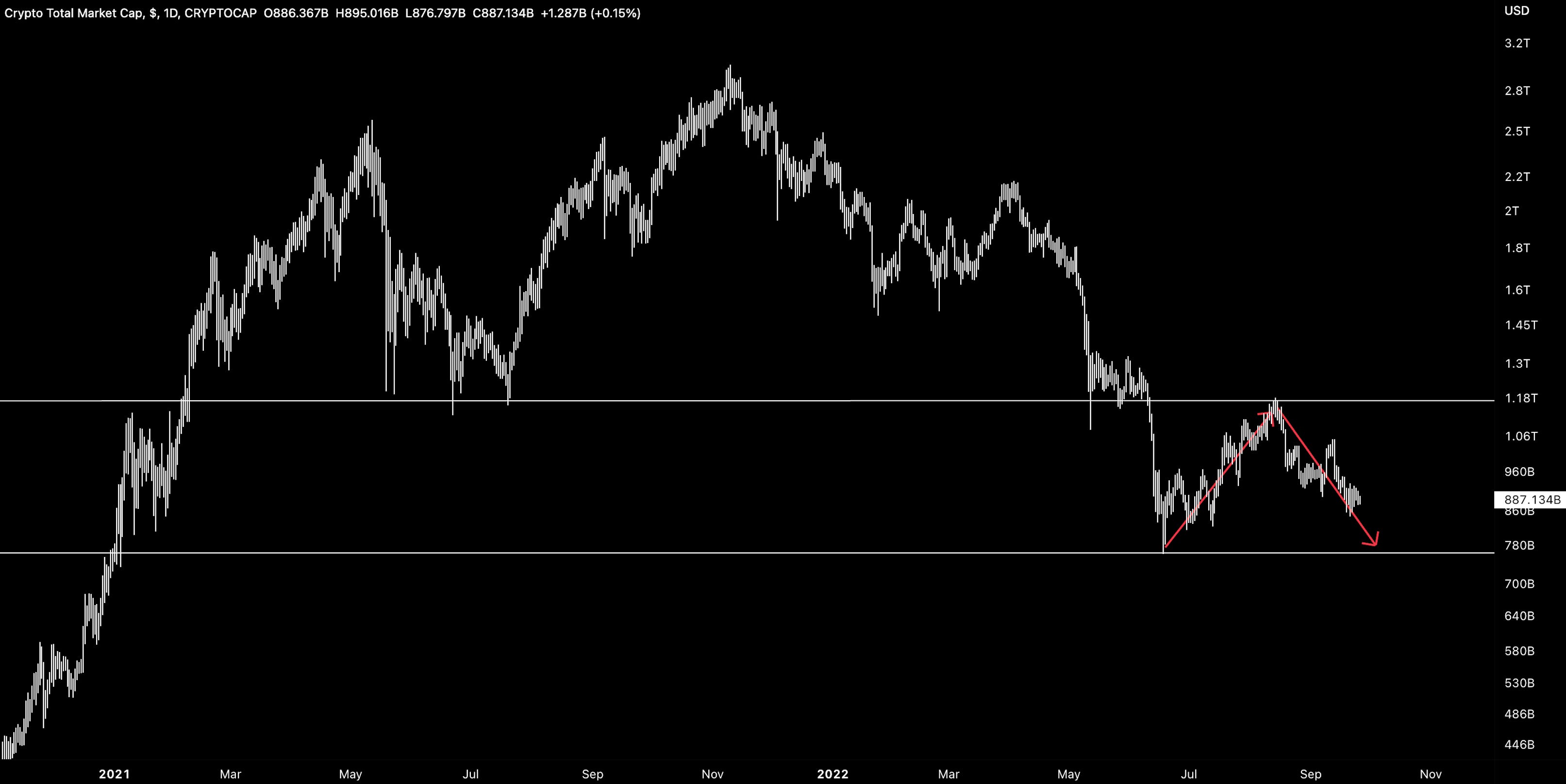

Bitcoin’s dominance appears to still be bouncing off its 39% 2-year floor with every bounce seeing dominance climb to 48% before cooling off. A break above this channel should it occur would also likely signify a more prolonged period of Bitcoin relative strength.

The Growing Impact of Derivatives

Global spot volume appears to have found a new $18B floor for now but it is unclear if this can be sustained in a deteriorating macro environment.

What is arguably more clear is the role of derivatives in leading price action. Futures volume for BTC and ETH remain elevated ($36 and $30B respectively) with futures open interest outpacing market cap growth.

Higher speculation in these markets have driven larger liquidation volumes which more recently has been skewed on the long side.

On-chain Models

On-chain models (e.g. Metcalfe’s) for majors continue to paint a bearish outlook. Networks users for both Bitcoin and Ethereum are mean reverting back to declining trend as expected. Note, the (growing) impact of the derivative market may skew this relationship.

Bitcoin also faces more idiosyncratic pressures on the mining side. Hashrate continues to outpacing price, putting stress on the smaller and less profitable mining companies.

Unsparingly, analysis shows that when this metric surges (mining companies face higher cost pressures in relation to competition) this coincides with equity value depreciation. It seems likely that mining companies are entering another phase of capitulation.

Not all cryptoassets have performed equally over the past week. Weekly outperformers such as COMP (+29.4%) and XRP (+33.3%) highlight certain pockets of high speculative interest by traders seeking returns.

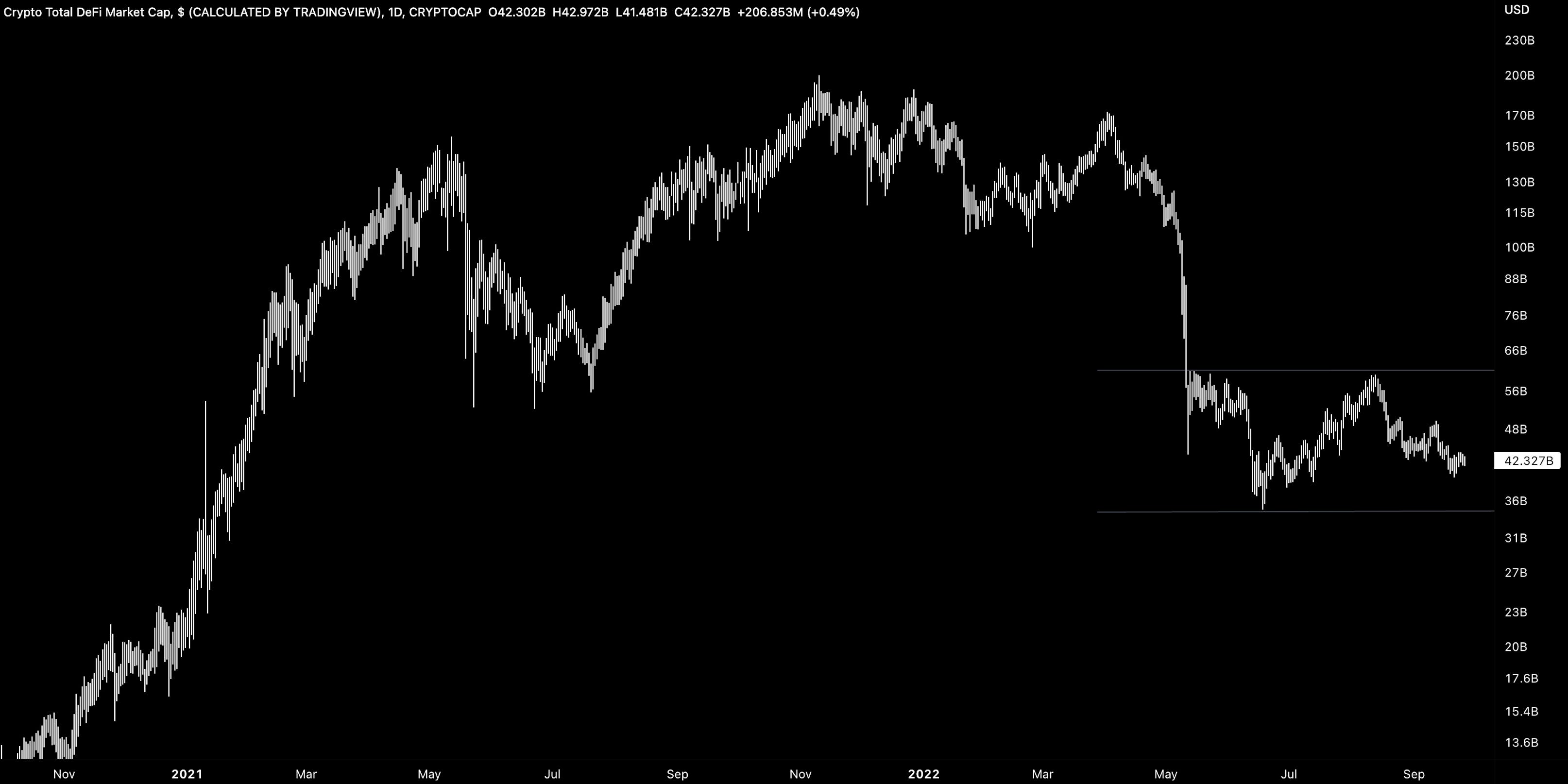

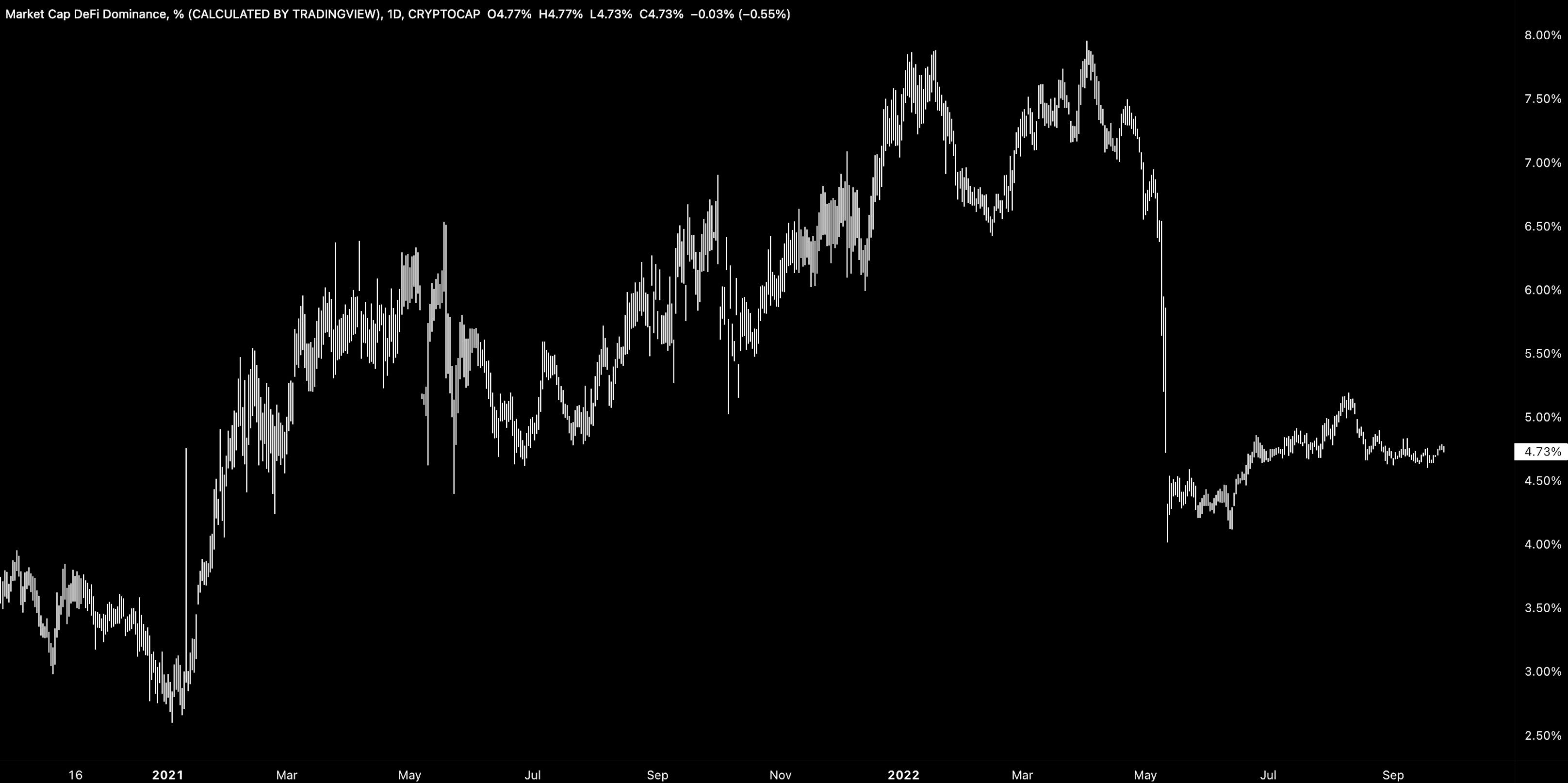

It is these pockets that have been driving DeFi dominance stability over the past week. Our DeFi/Total index shows the sector continuing to deviate materially away from trend post etheruem merge.

Given the broader outlook, the risk for investors is to the downside and there is a good probability we see this sector lose out on relative value and mean revert once again.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Top performers over the past week are largely speculative/headline driven:

Top 100 (7d %):

XRP (+31.4%) - speculation around SEC <> Ripple lawsuit resolve

Compound (+29.7%) - Compound III release

Tokenize Xchange (+27.1%) - new release

Algorand (+25.9%) - release of ‘State Proofs’ for decentralization push

IOTA (+19.3%) - partnership with Germany infrastructure project

DeFi Top 100 MCAPs (7d %):

Reserve Rights (+50.3%)

TracerDAO (+49.7%)

Compound (+29.7%)

Ampleforth (+23.3%)

Injective (+21.8%)

WKAVA rewards are live on Kava Curve DAI / USDT / USDC pool with 13.5% current APR.

Aura is adding 5 new pools this week, including LDO / wstETH and rETH/RPL pools.

Silo increased incentives to AURA holders, SILO / ETH pool now earns 300 - 700% (max boost) APR.

Stride launched stSTARS / STARS liquid staking pool with STRD rewards and 81% total APR.

Global Market Cap

$894B; Global market cap increased by 1.06% last week. Cryptoassets are opening the week to stead start (+1%). Overall consolidation pattern emerging (lower highs, higher lows).

DeFi MCAP

$42.3B; DeFi market cap increased slightly by 1.2%. Still kept range bound between $43B and $60B.

4.73%; No notable moves in DeFi dominance over the past week which indicates the sector is moving in line with the broader market for now.

Bitcoin Dominance

40.8%. Bitcoin dominance bouncing higher from its 2021-2022 lows. Next key level to break will be ~42%. Every time BTC.D bounces from 39%, it has rallied towards 48% as the asset claws back relative value after being negated.

Trader Positioning

The BTC implied vol term structure seeing short-dated (1W) being back in line with longer-dated tenors which stand ~68-69.

Highest BTC OI by strike (30SEP) for puts is $18k (6,652) and $25k for calls (2,119).

Highest ETH OI by strike (30SEP) for puts is $1k (43,950) and $5k for calls (90,150)

Aggregate BTC funding rates moderately positive but appears traders are lacking clear direction over the past few weeks. ETH funding rates neutral.

Grayscale GBTC

GBTC discount to NAV widening to new ATH as supply outstrips demand.

Grayscale ETHE

ETHE discount to NAV also widening as ETH spot also comes under pressure. 30D volumes on track to reach new lows since 2020 (3M).

Volumes

Daily spot volumes have increased 26% over the past month. Not clear if new floor of $18B/daily will be sustained. BTC-denominated volume flat at ~3.4m.

Aggregate Order Books

Order books looks heavier on the bid side further away from bid-ask price. Good support at $18k and below.

Bitcoin Hashrate

Bitcoin hash rate has declined 3% over the past week after difficulty adjustment increased 3.45% on September 13th.

Bitcoin hash rate/price ratio is surging to new annual highs as miners faced increased resource competition in the face of higher energy costs, higher cost of credit, and lower market prices.

📚 Global Crypto Adoption [Chainalysis]

📚 A Primer in Zero Knowledge Proofs [Varun Shenoy]

📚 Crypto Loan Activity [Caue Oliverira]

📚 Hacker steals $950,000 from crypto vanity address as exploits continue [The Block]

📚 How BlockFi Went From Tech Unicorn to Crypto Burnout [Blockworks]

🎙️ Will the Debt Crush Powell’s Volker Dreams? [The Breakdown]

🎙️ The Sovereign Debt Crisis Is Coming | Brent Johnson [Blockworks]

🎙️ The Chopping Block: Why ETH Dumped So Hard After the Merge [Unchained]

🎙️ On When Token Models Make Sense [The Scoop]

🎙️ FX In Decentralized Finance [The Curious Learners]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.