Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below:

No Rudder In A Fast Current

Happy Labor Day!

The global cryptoasset market has chopped around the $950B MCAP level for the past week as summer draws to a close.

Momentum like the RSI (W) indicates near oversold levels today but the trend has been very much to the downside. The initial downside risk to cryptoassets appears -20% from current levels at ~$760B - the 2018 peak and 2022 low.

Overall, the market appears directionless with declining volume and no clear momentum being snowballed up or down. The way risk assets more generally have reacted to recent macro headlines has perfectly illustrated this.

Last week, trades braced for a slurry of economic data including for U.S. manufacturing. The August S&P Global US Manufacturing PMI came in at 52.8 vs. 52 expected with the index price figure being its lowest since July 2020.

The cryptoasset market retreated back in the hours after the ‘higher-than-expected’ PMI print with BTC/USD falling back to the $19.5k level.

However, it was the labor market print on Friday which acted as the only blocker for traders deploying risk back into the market before the big US CPI print later in September.

The labor market stayed solid in August with employers adding 315k jobs last month, representing a strong pace of growth.

Risk assets reacted positively initially as the up-is-down world we find ourselves in means any pullback in job growth is good for the Fed who believe the job market is overheated.

US equities dropped by more than a percentage point, falling for three consecutive weeks. Despite recent drops, P/E ratios remain far above the 5 and 10 year averages (22.9 and 20.3 respectively) and point to a necessary re-rate in equity valuations to finish a complete ‘reset’.

BTC/USD spiked 2.25% off the back of the labor market news but was stopped in its tracks at the $20,400 level. The pair then retreated back to the $19,500 level once again painting a clear $20k consolidation channel since the end of August.

I Need A Dollar, Dollar Is What I Need

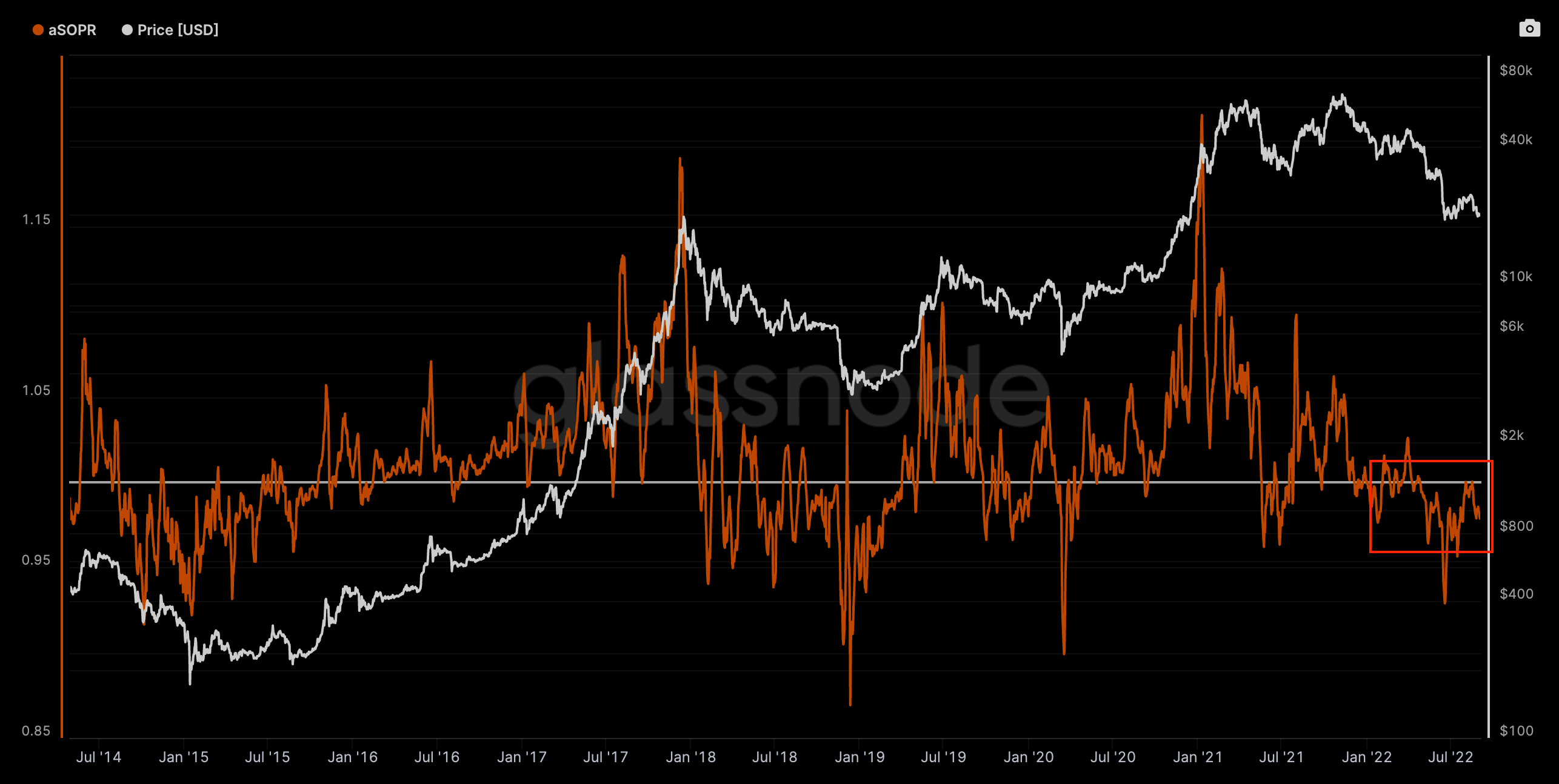

A conclusion here is that BTC holders appear to be taking profit on any BTC rally that occurs.

This supports conclusions from a number of on-chain indicators including aSOPR which measures the average profit or loss multiple on spent coins. During bearish trends, an aSOPR of 1.0 can act as resistance where investors sell their BTC during rallies and offload their positions near their cost basis.

The LTH-SOPR, which only focuses on long-term BTC holders shows that cohort is also feeling the pain. With the LTH-SOPR at <0.6, buyers who bought during the last bull cycle are realizing losses >40%.

LTH-SOPR can act as a higher conviction signal for when prices may be more supported for a long-term recovery (>1 on the ratio) but as we see historically, this can often take some time to develop.

The number of BTC last moves 7+ years ago has also spiked in recent days. Every time these very dormant BTC were moved, price subsequently dropped 20-80% in the months following the on-chain signal.

The Decentralized Finance (DeFi) has equally found it hard to find a direction. For now the total DeFi MCAP index (Cryptocap) has stayed above $43B. Its ability to stay above or move below this levels may indicate the medium-term direction of the sector.

A more bearish interpretation can be seen by extrapolating previous trends in the DeFi/Total MCAP ratio.

The ratio has formed a clear descending channel since the crypto bear market began with the sector losing relative value vs. the broader market.

The extent of the ratio drawdown has been largely the same each time - one can draw and use the exact same line to forecast when the local bottom has formed before the before a leg up to the next peak begins.

Using the same line again, this implies the next local bottom in the ratio on the 14th October.

We can also see that the peak-to-peak timeline has 2x every time with the last cycle forming over a 134 day period.

If we see the pattern continue, the next time we see a peak in the ratio would be in ~230 days with a rally. Equally a break out of this channel is possible and would be informative for showing how the market may be structurally changing.

The crypto markets is also heading into a macro heavy few weeks which will likely weigh on price action.

The US August CPI will be released in or around the same day as Ethereum’s merge with the Fed’s next FOMC meeting on the 20th-21st of September.

ETH/USD has also chopped around the $1.5k level for several weeks now but the driver in price has been exogenous to Ethereum. The higher rates for longer, strong dollar scenario has meant Ethereum has been climbing a steep hill.

However, if we look at the ETH/BTC we see a different story where that ratio has rallied 62% since its 2022 low. Therefore, traders playing the merge that have adjusted for the macro risk have been rewarded well.

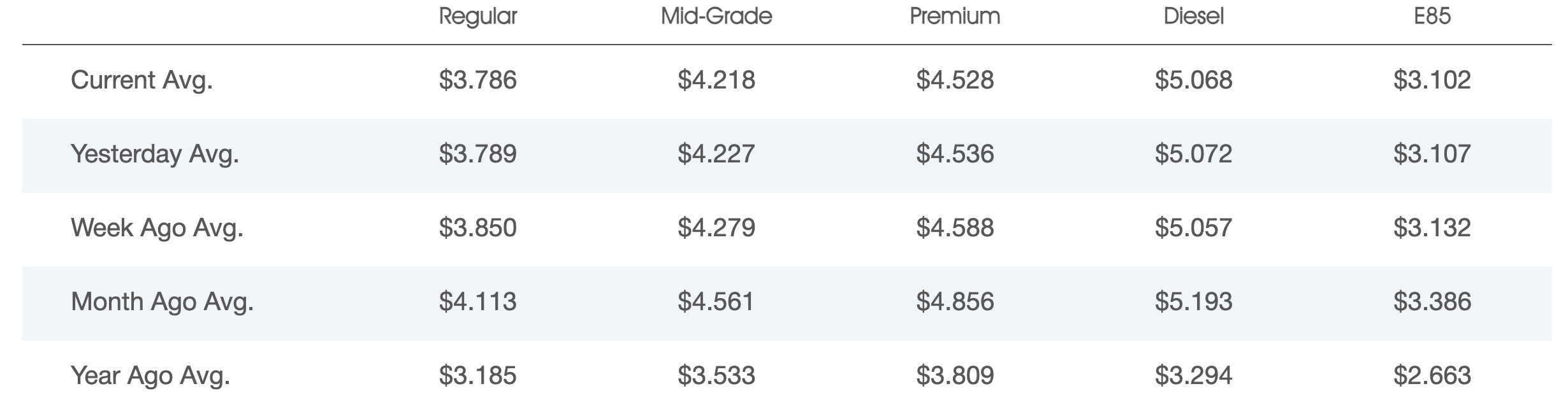

Looking ahead, the key question on everyone’s mind is around the CPI print. Will backwards looking, US gas prices (a key driver in the previous month’s decline) have kept relatively low ($3.786) compared to just 1 month ago. Note, gas prices remain well above the year-ago price of $3.18.

This bodes well for a decline in CPI for but other factors including rent costs may also offset this dynamic.

Equally, supply concerns for oil remain with West Texas Intermediate crude advancing towards $89/barrel. This comes after demand concerns last week drove prices down, easing concerns for many.

Fast forward 1 week later and Russia’s key natural gas pipeline to Europe has been shut down indefinitely due to a ‘leak’, driving up benchmark gas futures by 35%.

The Euro falls under $0.99 for the first time in 20 years.

The concerns now don’t just revolve around the rising price of natural gas. They also revolve around the increased demand in crude-based fuel.

Meanwhile the dollar keeps on getting stronger from a ‘cocktail’ of tighter monetary policies from the Fed vs. a worsening energy crisis in Europe.

On Monday, the U.S. Dollar currency index (DXY) reached a new annual high of 110.27 and can put further pressure on risk assets like crypto if the dollar rally extends even further.

Unchartered Territory

These directionless and hollow markets may see higher volatility near-term but the skew remains to the downside. Looking forward, the next guiding light for many risk investors will be the US CPI print next week.

The important point here is that it’s not necessarily the rolling over of CPI that’s important for central banks but rather the elevation of inflation above their respective targets.

Above all else, we simply find ourselves in unchartered territory.

And just like any unchartered journey, the journey reveals its story one moment at a time.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Ethereum-based DeFi assets are often outperformers in the market (vs. alternative L1 DeFi assets). High beta ETH merge plays continuing to outperform.

Top 100 (7d %):

DeFiChain (+37.8%)

GMX (+37%)

Celsius Network (+24.8%)

Lido DAO (+20.9%)

Comos Hub (+19.4%)

DeFi Top 100 MCAPs (7d %):

GMX (+37%)

ROOK (+34%)

Dopex (+28.4%)

Balancer (+26.1%)

Lido DAO (+20.9%)

Pika, perpetual swap exchange on Optimism, announced OP incentives for liquidity providers, 480,000 OP will be distributed to vault depositors over the next 6 months.

Convex added new FRAX / OHM (68% APR) and FRAX / ZZ pools (50%).

Gearbox integrated Yearn vaults for leveraged staking, stETH / ETH pool has the highest APY of 30% with 7x leverage.

Global Market Cap

$951T; Global market cap increased by 4.3% last week. MCAP is falling (1%) off growing macro fears.

DeFi MCAP

$44B; DeFi market cap increased 5.5% but weakening on Monday morning (-1.2%). The sector continues to be reflexive to the broader market.

DeFi Dominance

4.7%; DeFi dominance still ~42% from its ATHs in March 2022. Expectation is an increase in dominance if risk assets respond well to the incoming US CPI print and/or merge momentum snowballing once again.

Bitcoin Dominance

40%; Bitcoin dominance is at its 2021 floor of 40% as the orange coin has come under pressure from relative strength in ETH and growing flight to stables (risk-off environment).

Volatility

The BTC implied vok term structure steepening over the past few days with short-dated (<1w) vols dropping as the longer-dated tenors remaining firm at ~70-72 levels.

Positioning

No notable change in Bitcoin futures open interest ($11.5B) while aggregate funding rates have flipped moderately positive indicating a predominantly bullish positioning by traders. Funding rate remains negative for ETH and likely driven by ETHPOW trades. ETH perpetual OI retreating from ATH (66%) and may indicate that traders have set up most of their merge trades leading into the event (TBD).

Grayscale GBTC

No material change in the GBTC discount which now stands at 32.3%. Investors interest remains low.

Grayscale ETHE

ETHE discount widening once again and so far adds support to descending channel formed since January 2021. Forecasting this dynamic forward would imply ETHE underperforming vs. ETH over the coming weeks (high beta).

Volumes

Global daily exchange volume forming lower peak ($20.2B) with the market appearing to continue its 2022 trend of lower peaks. This signals investor apathy and muted interest by market participants. Bitcoin currently has 2x that of Ethereum for exchange volume ($9B vs. $4.5B).

Aggregate Order Books

Order books look heavier on the bid side. Stronger resistance up to $20k. Source: Bitcoinity.

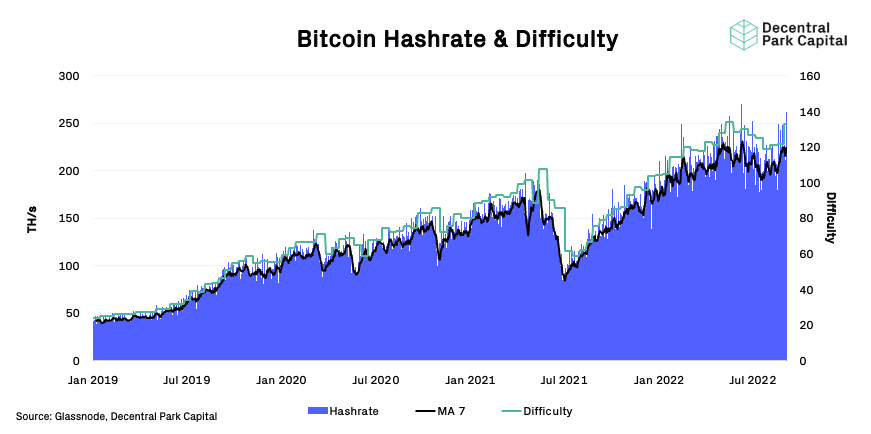

Bitcoin Hashrate

Bitcoin hash rate has jumped 1% over the past week with mining difficulty increasing 9.2% - the largest percentage jump in difficulty since January 2022. Hash rate has recovered despite dropping mining profitability (15% since August 18th).

Pooling, one of the world’s largest Bitcoin mining pools is facing liquidity problems.

📚 U R A QT [Grit]

📚 Arbitrum Ecosystem Overview [Corleone]

📚 Dune Digest #45 [Dune Analytics]

📚 Aave ETHPOW Fork Risk Mitigation [Gauntlet]

📚 Backtesting Ethereum’s EIP-1559 [Dunleavy]

🎙️ Balaji Srinvasan’s Network State [Real Vision]

🎙️ Dive Back into MEV with Alex Stokes and Chris Hager [Zero Knowledge]

🎙️ Second-Party Custody with Fedimint [On The Brink]

🎙️ Navigating a World Trapped between Scarcity & Abundance [Hidden Forces]

🎙️ Just How Bad Is The Economy Getting in China? [Odd Lots]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.