Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below:

Hollow Markets

For some time now, my market analysis has led me to be cautiously bearish until I see clearer signs of looming accommodative monetary policies and looser liquidity conditions. Watching the market psychology of hope, disbelief, and adaptation has been nothing short of fascinating.

But don’t be fooled.

These markets remain hollow.

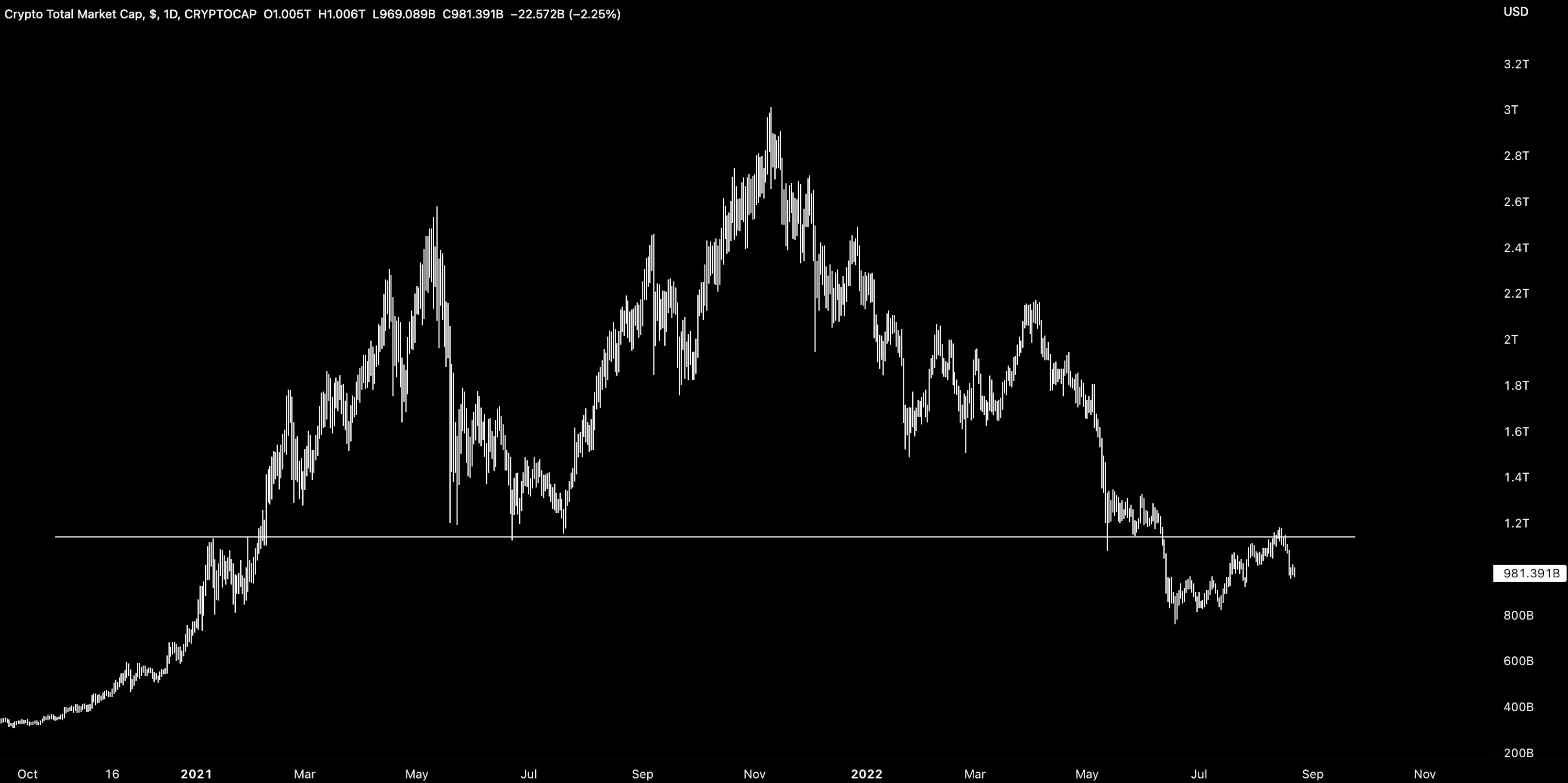

Cryptoassets have had their more significant re-traces since the June 2022 low. Global MCAP has fallen ~17% from its August peak with very few names spared in the recent drawdown.

Global MCAP is now back below its critical level of $1.14T and has now broken its upwards channel.

ETH/USD, the consensus bet given the looming merge, has re-rated 24% since its August highs and is back below key support of $17k. Note, these levels were support throughout 2021 and 2022.

Liquidation analysis indicates that futures had a part to play. Over $168m longs were liquidated last Friday driving a sharp 12.9% drawdown in price.

As usual, assets down the risk curve (e.g. in DeFi) were hit harder. High beta plays like LDO have taken top spots for underperforming vs. the broader market (-27.5%).

In a bearish scenario, DeFi/TotalMCAP (proxy for DeFi dominance) could re-trace a further 40% to hit the bottom of its descending channel. The index has oscillated between both lines since last September. The broader pattern remains bearish unless seen otherwise.

Morgan Stanley stated last Friday that:

“It will be difficult for this crypto cycle to bottom without “fiat leverage growing or crypto leverage growing.”

The only thing becoming tighter than market liquidity is the regulation and those headlines are now coming in thick - from OPAC and FDIS.

Regulatory overhang will do little to comfort those waiting on the sidelines especially when unclear events like Ethereum’s merge will likely demand further questions in this domain.

Core proxy of market interest are still muted. Daily exchange volume continues to wane. With the recent price rallies not being accompanied by rising volume. The dominance of futures volume vs. spot highlights the growing role of derivatives here.

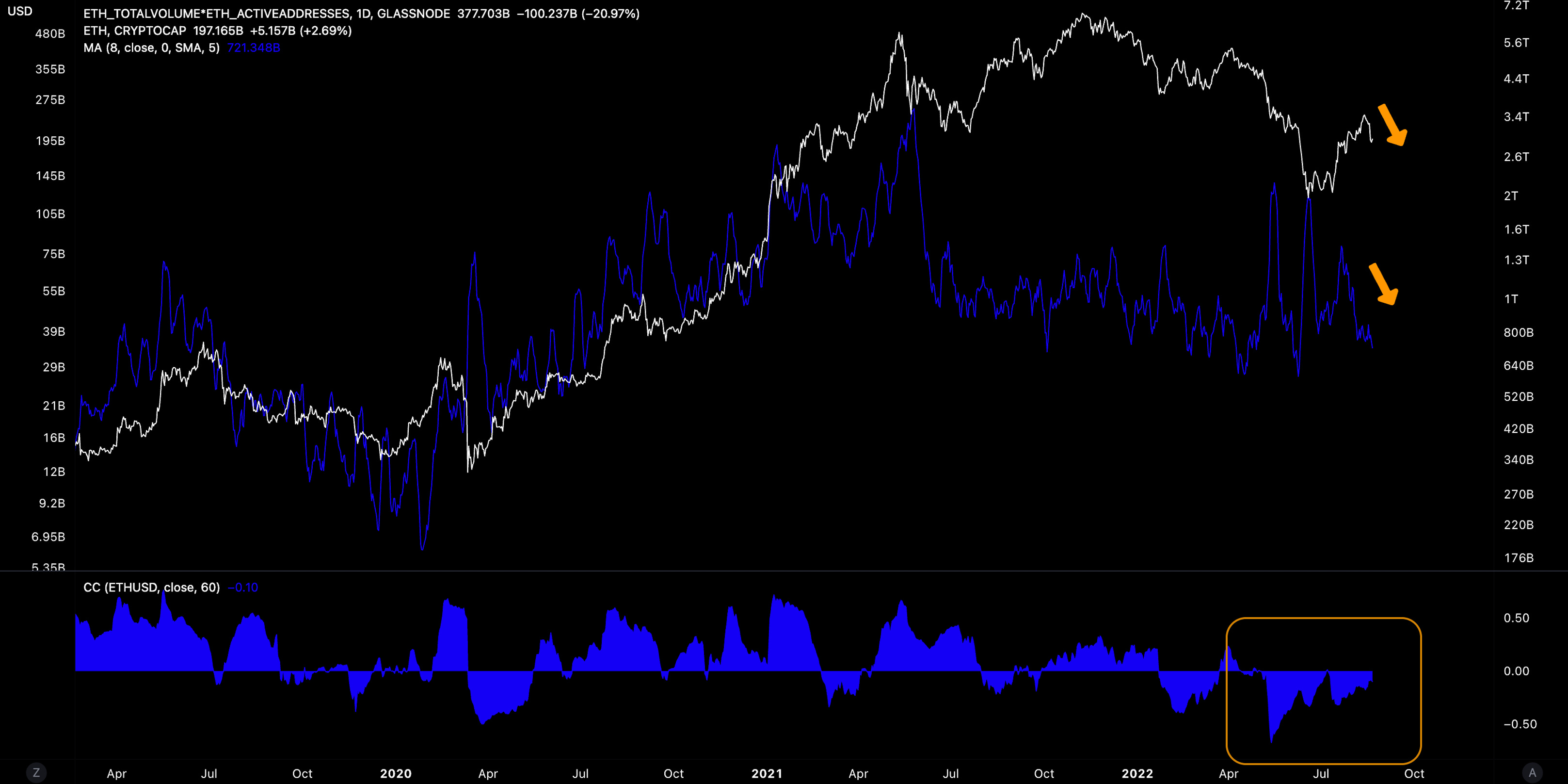

Since June, on-chain valuation models were broadly now supporting the price rally. On-chain activity indices for Ethereum were negatively correlated for a period of time which is now falling which was expected.

We are seeing on-chain activity and price move in synchronicity once again.

Other on-chain signals point to optimism such as the Bitcoin hash ribbons which has printed its ‘buy’ signal. This signals the completion of miner capitulation (71 days in total) - the 3rd longest in history.

This is a compelling signal but questions remain over its viability in the current macro set up which is material different to the one in motion since Bitcoin’s inception. Time will tell.

So a flurry of overextended longs have presented volatility but price action wasn’t futures liquidations per se.

The Wake-Up Call?

The driver of the driver was the buckling of risk appetite given the macro developments.

Markets are seeing broad declines in European and US equities. Futures on the tech-heavy NASDAQ fell 1.8% on Friday and a further 1.59% this morning. This was carried over to the cryptoasset market.

Investors appear to start waking up the looming recession, hikes going higher, balance sheet reductions, and elevated inflation.

It is reasonable to suggest that the H1 2022 re-rate in equities was driven by an adjustment to (accelerated) tighter monetary policies. It is reasonable to also suggest that a potential second re-rate in equities is driven by contraction in economic growth and therefore corporate earnings.

We may be seeing an opposite dynamic between price and earnings to the one seen in Q1/2 this year - market price fall while earnings meet or beat expectations. Profits remain healthy as consumer spending and the labor market remained strong.

After all, it takes a while for tighter monetary policy to take effect on the broader economy.

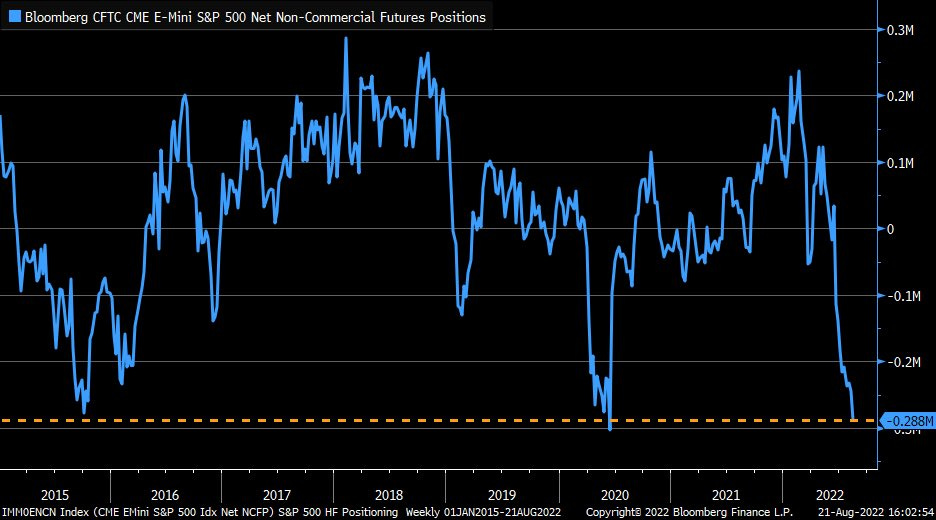

This gave fuel for equity valuations to rally higher - the most hated rally in recent memory. Hedge funds are now becoming even more net short ($125B) on the S&P 500 futures. Of course, the unwinding of their positions (as was the case in June) perhaps through opaque Fed comments could exacerbates the situation even more.

The problem now being that corporate earnings, particularly those with low pricing power, are vulnerable while prices have rallied 24% since the yearly lows.

Take Apple which makes up 14% of the NASDAQ 100 beat expectations taking in profits of $83B. This has taken APPL to clear overbought levels where its recent selling has driven the broader NASDAQ decline - and therefore crypto.

Note the signs of slowdown is already in sight. Apple’s YoY EPS fell 7% falling due to ‘rising operating expenses’ and the ‘strong dollar’.

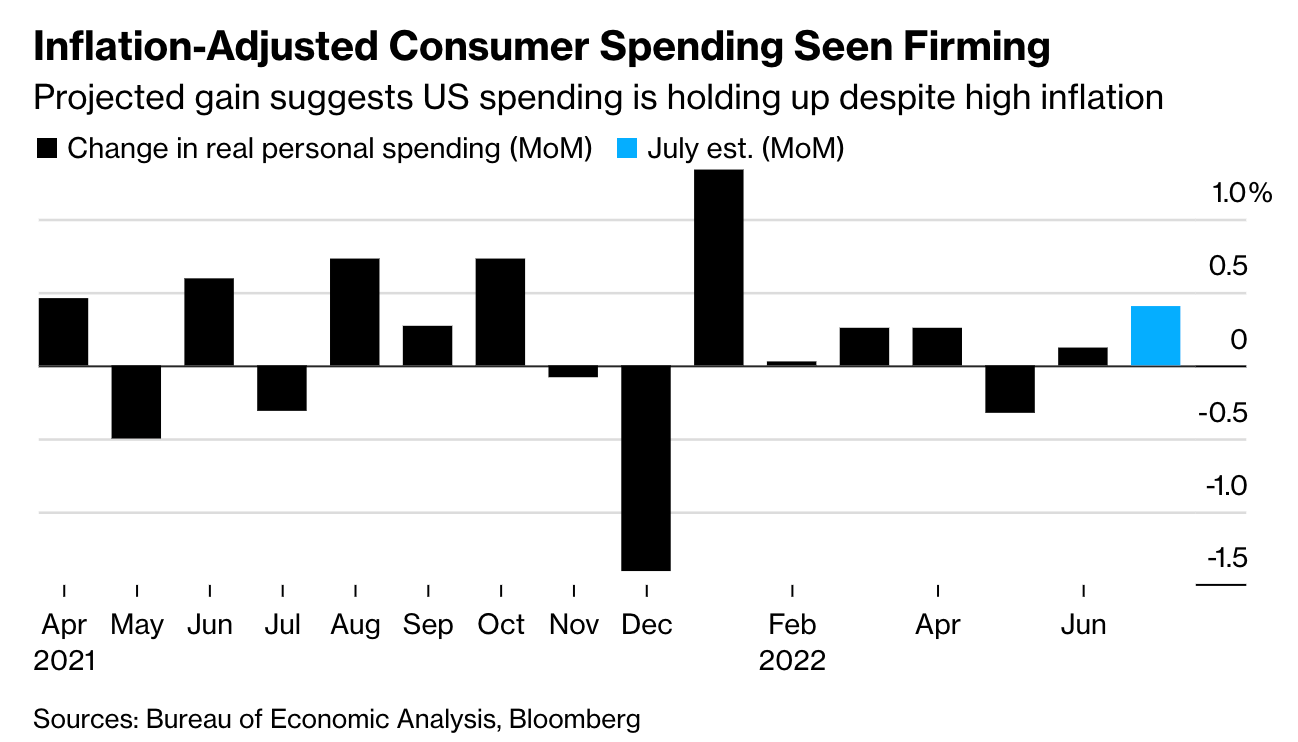

Taking the first, there is reasons for optimism. US spending (inflation-adjusted) is holding up despite elevated prices. However, this adds fuel for the Fed to do more to tighten financial conditions in order to bring prices back to acceptable levels.

After all, the Fed has failed to keep its QT targets with conditions being more accommodative than restrictive. As warned many times before, crypto, driven by liquidity and monetary supply, is at risk if an accelerated QT track is resumed which appears to be the case.

Taking the second, stronger dollar, we are seeing dollar gauges like DXY eye new ATHs and offering little respite for US corporations with reliance on exports.

The dollar milkshake theory is in full swing.

Global recession and emerging market debt crises continue to act as material tailwinds for the global reserve currency. In other words fundamental headwinds for risk assets like crypto where the value of the denominator is increasing.

Meanwhile, the European energy crisis pushes on with benchmark futures rising 16% as Nord Stream pipeline will stop for 3 days due to ‘maintenance’.

This comes as Citi forecasts UK inflation to hit 18% due to rising natural gas costs demanding rates to climb to 7% by the BoE. In the US, changes in the housing market driving changes in CPI measures lag boding poorly for bringing CPI back down.

For now, it appears the brief exuberance in risk markets maybe taking a pause as investors consider a reality check. All eyes will be on the Fed’s symposium at Jackson Hole this week, paying close attention to Powell’s potential ‘resetting of expectations’.

Failing to reset those expectations on central banks' current paths may pave the way for a world of hurt.

What will matter in the these hollow markets, as has always been the case, will be the data itself.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Top performing assets include high beta plays in ETH (WNXM) and protocols that are unwinding where those assets are re-rated according to their balance sheet (TRIBE).

Top 100 (7d %):

EOS (+16%)

Chiliz (+6.7%)

Chain (+2.2%)

Frax Share (+2.2%)

Evmos (+0.8%)

DeFi Top 100 MCAPs (7d %):

Stargate Finance (+94%)

bZx (+44.5%)

Tribe (+30.4%)

Wrapped NXM (+29.3%)

KNC (+10.5%)

Convex added new Frax pools including FRAX / IQ, pitchFXS / FRAX, FRAX / SYN with ~100% current APR.

Aura is currently offering 3x higher yields (13% APR) on stETH / ETH than non-boosted depositors on Balancer.

Gearbox unpaused the protocol after pathing the bug reported last week. No funds have been lost and no bad debt has accumulated.

The supply cap on Aave for sUSD on Optimism has been increased to $20M, supply APR is 4%.

Global Market Cap

$1.05T; Global market cap has fallen 18% over the past week.

DeFi MCAP

$46.5B; DeFi market cap has fallen by 14% over the past week as investors down the risk curve take chips of the table.

DeFi Dominance

$4.7%; DeFi dominance weekly change was -2.57% with next support line 4.2%. A break below may confirm bearish trend more broadly for the sector. D RSIs indicate potential breathing room to the upside prior to this outcome.

Bitcoin Dominance

41.3%; Bitcoin dominance has kept relatively steady over the past week as the asset hold relative value against its peers.

Volatility

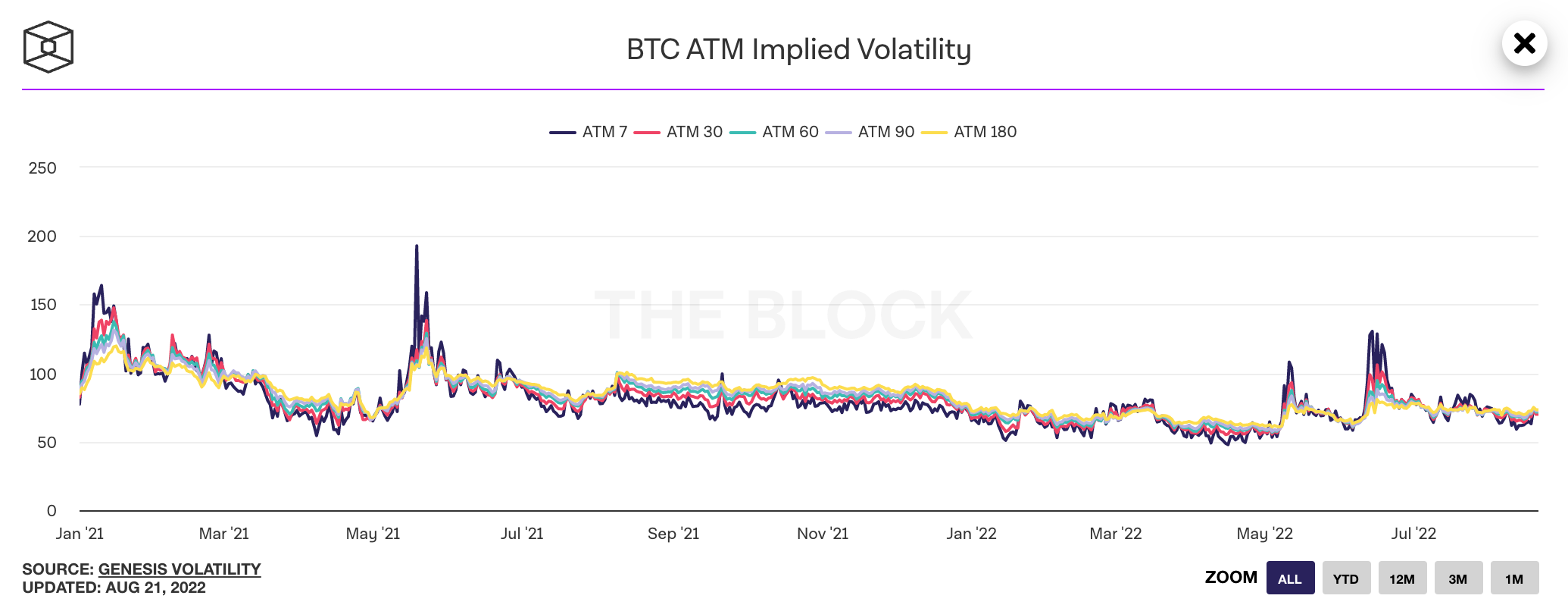

BTC; Long dated vols have increased after the recent buying pressure.

Trader Positioning

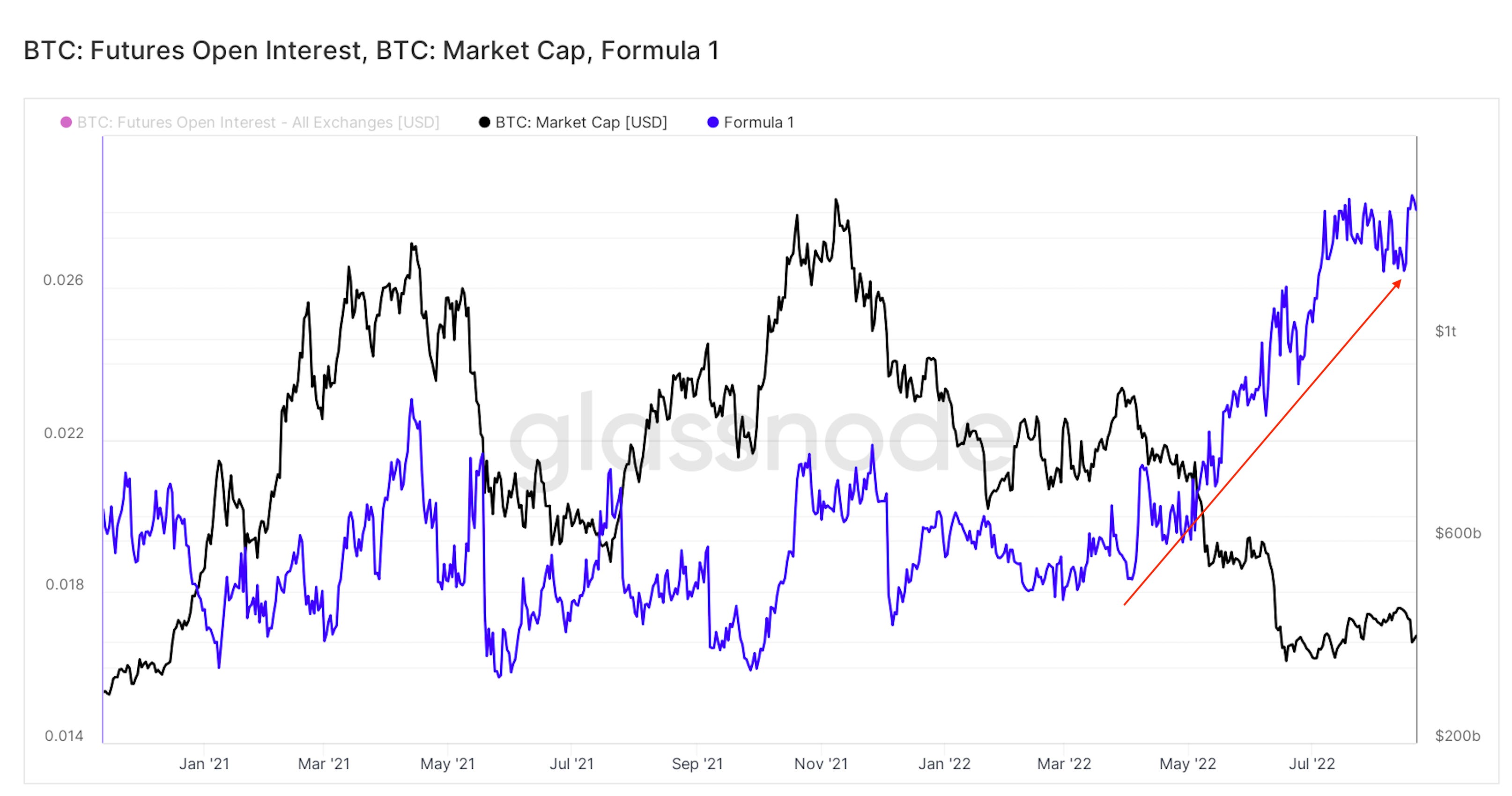

BTC and ETH open interest (OI) $11.5B and $7B respectively. Large liquidations have reduced ETH OI by 22% ($168m on 19th August 2022). Aggregate funding rates are now negative for BTC and ETH (moderate) indicating overall bearish trader positioning in futures markets. OI/MCAP ratios for BTC and ETH are near ATH posing volatility risk despite recent liquidations/price action. Uptick in put/call ratio for ETH.

Grayscale GBTC

GBTC discount hovers near ATH at -32.57%. Weak spot action likely to widen discount to new ATHs.

Grayscale ETHE

ETHE discount narrowed early last week as demand grew relative to share supply. Discount cooled off since as prices re-rate.

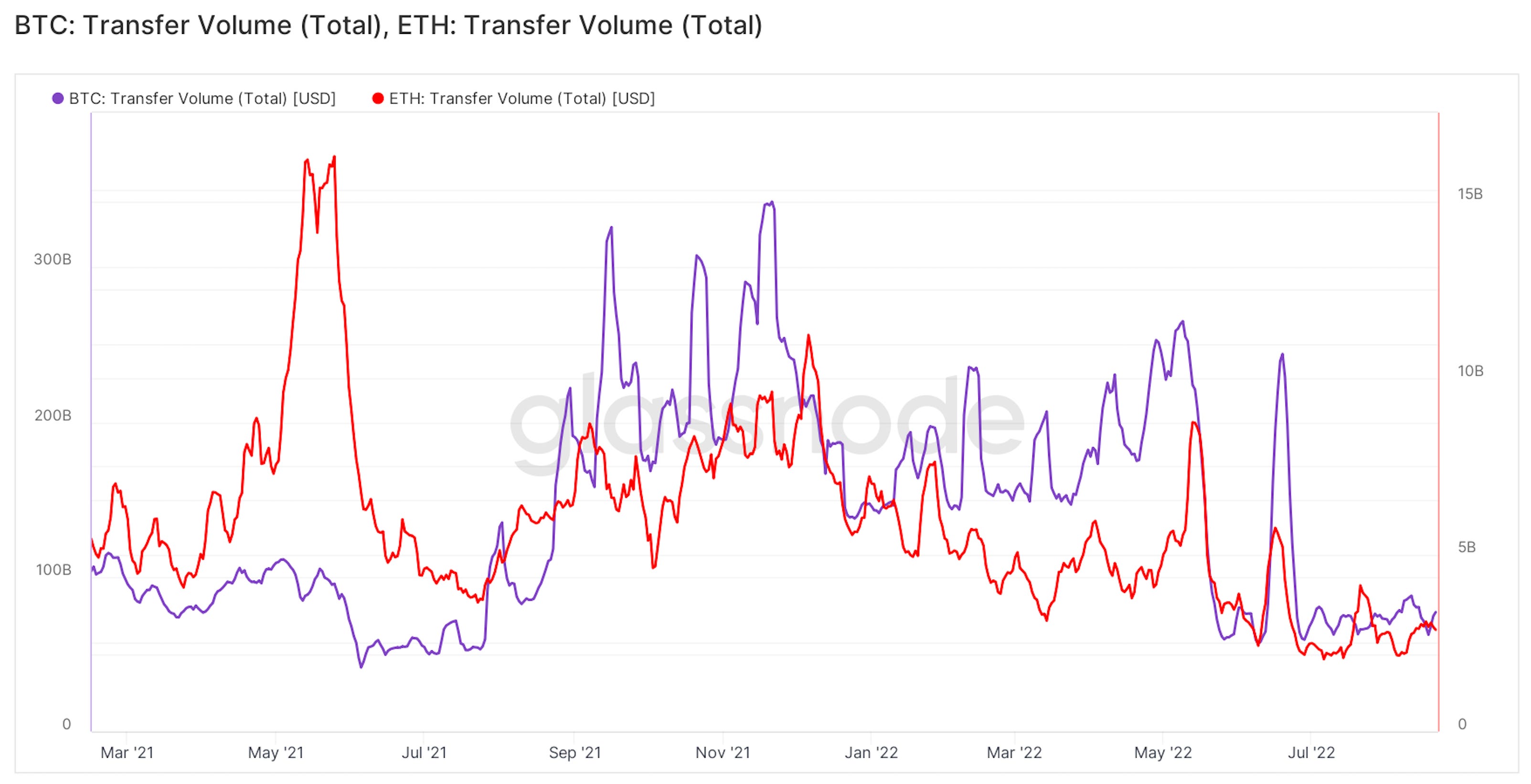

Volumes

Exchange volumes for BTC and ETH has been flat MTD. On-chain volume has also been flat MTD but ~40-50% below levels seen in Q1 2022 indicating relatively lowwe levels of on-chain activity.

Combined Order Books

BTC aggregate order books appear stronger on the bid side. Heavier resistance up to $21.5k.

Bitcoin Hashrate

Bitcoin hash rate has increased 4% over the past week (7D MA). This comes as the Bitcoin hash ribbons indicator prints a ‘buy’ signal indicating the end of miner capitulation.

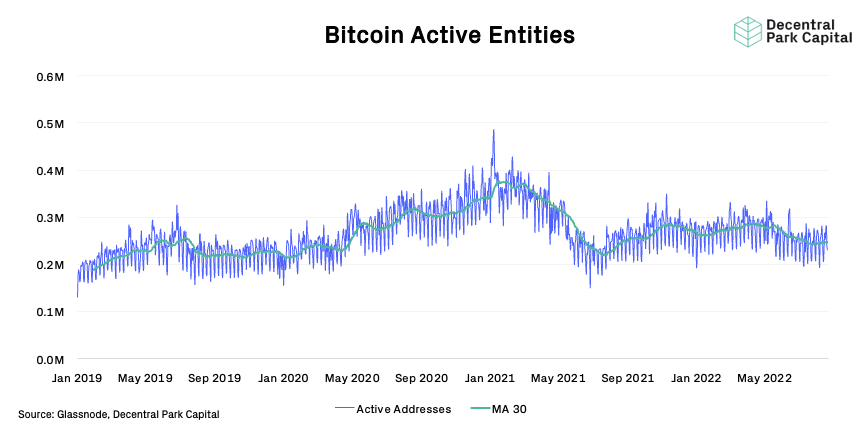

Active User Base

BTC; The Bitcoin network is still seeing a less active user based. Active entities has is up ~1% over the past week.

📚 GMX vs. Curve On Volume [button_fml]

📚 ETHMexico Finalists [ETHGlobal]

📚 State of DeFi Lending [SoDL]

📚 Parsec Weekly [Parsec]

📚 Wall Street Bears Take Revenge After a $7 Trillion Rally [Bloomberg]

🎙️ How Stablecoins Became A Powerful Force In Crypto [Odd Lots]

🎙️ MakerDAO’s Growth Strategy [Empire]

🎙️ On The Blockchain Funds of Funds Landscape [On The Brink]

🎙️ Welcome To The ‘We Just Don’t Know’ Economy [The Breakdown]

🎙️The Disinflationary Trend Is Over [Blockworks Macro]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.