Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below.

A Sunny Spell In A Stormy Macro Season

Crypto markets jump higher after a largely uneventful weekend. Majors like BTC and ETH are up 4.6% and 4.4% respectively.

Cryptoassets continue to be lifted in line with the broader equity markets with NDX closing its 3rd positive week in a row - up 20.56% from June lows. The correlation between equity indices like NDX and the crypto markets remains strongly positive and will likely remain the case for the foreseeable future.

The boost in equities have come from several factors including:

Better-than-expected earnings including Starbucks where little evidence yet of lowered consumer demand

Surprise re-bound in July services PMI shook off worries that the U.S. had already fallen into a recession (even though that may be the case now or in the future)

James Bullard (St. Louis Reserve President) stated he doesn’t think the U.S. is in a recession and that rate hikes can continue.

Yet, at the same time the growth outlook remains dire potentially putting a limit on equities in the medium-term.

In fact, the equity market resilience has been so strong that investors have largely shrugged off any geopolitical tensions (Pelosi’s trip to Taiwan) and surprise payroll increases.

For the S&P 500, its 4W performance is approaching 2 SDs.

Of course, the latter putting a higher likelihood of a 0.75 BPS rate hike for the next Fed meeting in September. All eyes will be on new data coming in, including the US CPI release later this week.

CPI July MoM estimations are ~0.1-0.2% aided by lower fuel prices during the month - much closer to the levels the Fed are looking for. However, core CPI may be ~0.5%. For now, the Fed’s bias is towards large interest-rate hikes.

The Inflection Points

The upcoming events in the macro calendar comes at an interesting time for the cryptoasset market.

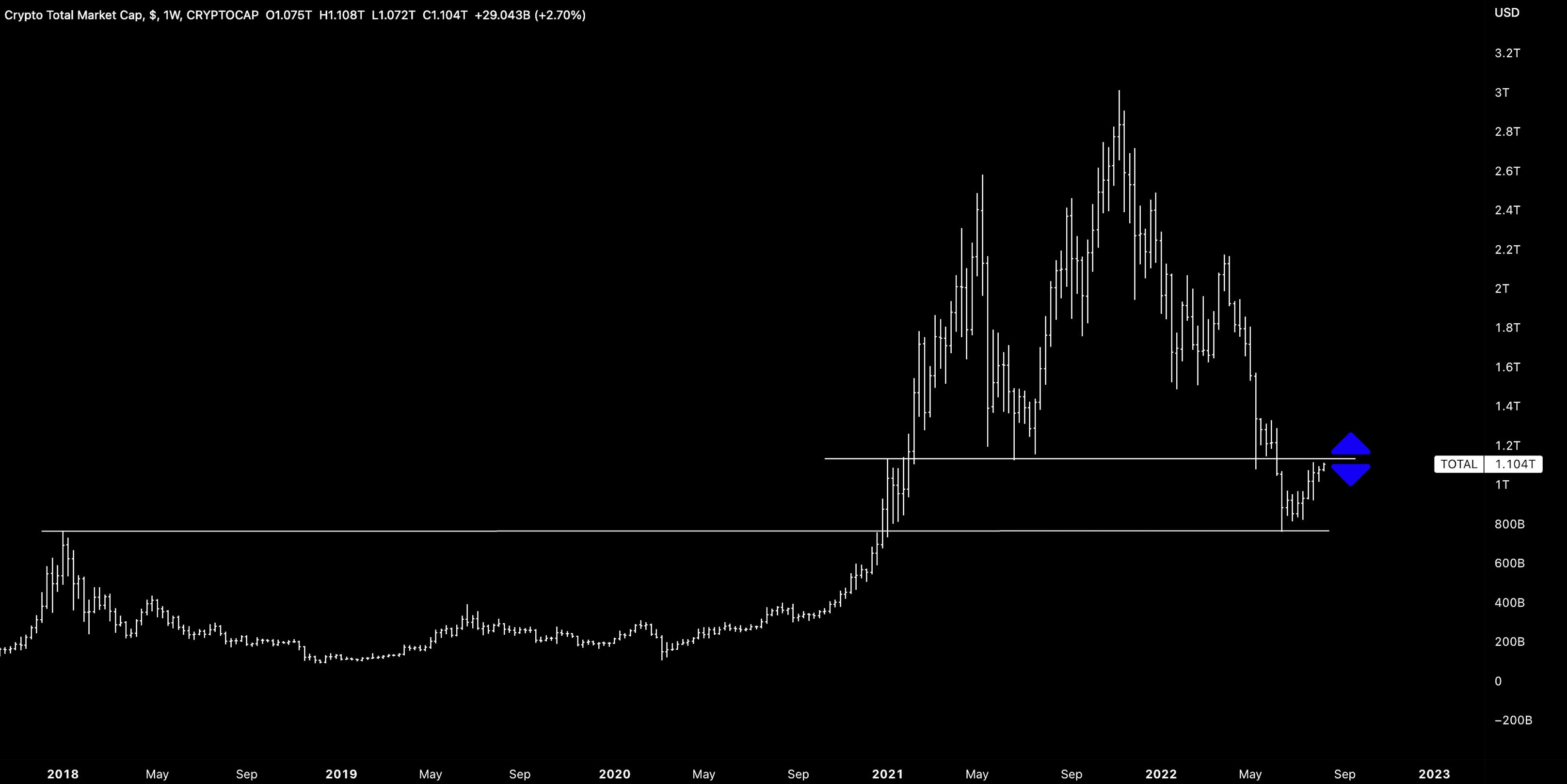

Global MCAP has yet to break above its peak in Jan 2021 where it has been hitting a ceiling of $1.14T for the past month. A convincing break above here would be telling of medium-term trajectory. Even more interesting if the incoming macro headlines are not conducive for risk assets in general.

The merge has also boosted ETH in its own way with the ETH/BTC being lifted 50% since the June 2022 lows.

ETH/USD also seems to also be at an inflection point ($1745) - a frequent bottom throughout 2021. An increasing number of traders buying spot to short futures to potential arb forks during the merge could keep ETH on its same path.

The trade has become so crowded that Sep and Dec ETH futures are now in backwardation.

The ETHE discount to NAV is also diverging away from GBTC indicating a growing demand for ETH via the equity market. After all, ETHE provides a potential high beta play on ETH leading up the merge if a narrowing of the discount if projected by the investor.

Note, ETHE volumes have been falling significantly while the discount narrows potentially indicating a low conviction rally for the trust.

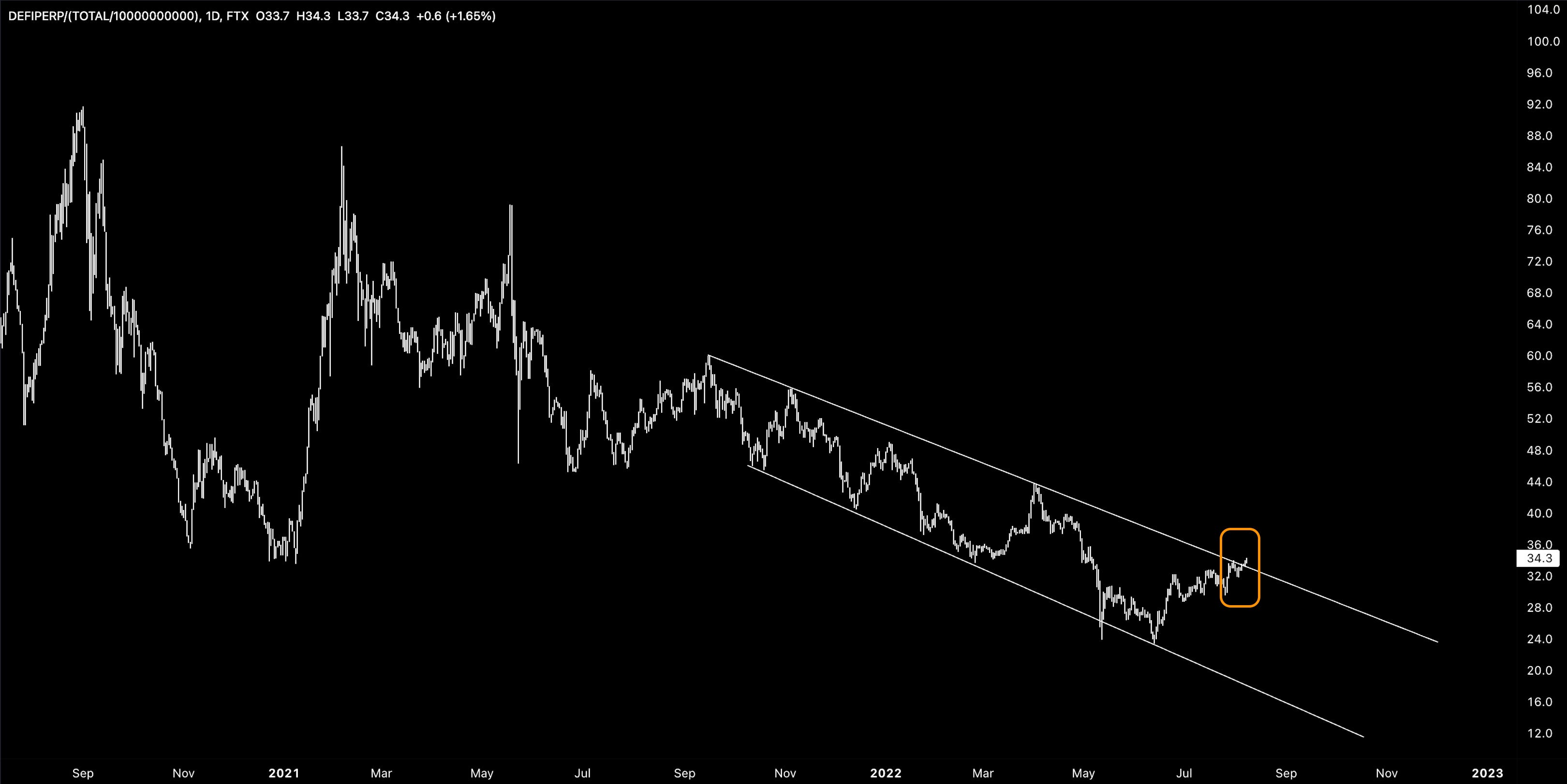

There is also evidence of increased capital deployment down the risk curve with DeFi/GlobalMCAP index starting to break out of its descending channel. Note, temporary breaks can occur such as the 12th May so the time spent outside of the channel is equally important.

We can also see that the stablecoin MCAP dominance continues to fall from its earlier peak. Declines in this index often coincides with price rallies as investors rotate out of stablecoins to deploy risk.

While this is bullish, it’s unclear whether we rebound off the trend line or fall all the way towards to the lower channel line.

I Say “Recession”, You Say “S’all Good!”

Yet, there are still warning signs of more potential downside ahead. The 2/10Yr treasury spread remains negative for 23 trading dates in a row - often viewed by the markets as a sign of imminent recession.

Severe 2/10Yr treasury spreads often often preceded sharp declines in equities where earnings and growth outlook and re-evaluated recession dynamics really start to kick in.

Dollar strength remains, building on the outperformance at the end of last week after the release of strong U.S. jobs data.

The expectation of higher rate hikes and tightening liquidity (QT) is constructive for the dollar for the medium-term and may continue to act as a headwind for cryptoassets should this play out.

On-chain valuation models also show why there should be caution. Economic activity on Ethereum has been falling over a lower number of addresses (Metcalfe’s) while price has diverged upwards (negative correlation).

These models imply that sustained price rallies should be accompanied with higher economic activity (as has often been the case historically).

Put differently, the recent ETH outperformance appears to be driven by merge speculation vs. on-chain economic growth.

More broadly, daily exchange volume has fully rounded off following the wider trend YTD. This indicates short-term peaks of speculative activity but lower overall interest in an increasingly illiquid market.

It seems all rosy for the time being with momentum continuing to swing with the direction of the current narratives.

However, continued tightening to suppress inflation, expected contraction in corporate profit margins, and accelerated unwinds of central bank balance sheets all paint a bleak outlook that is at odds with the mood in risk markets today.

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Top performing assets over the past week have often either been headline-driven (e.g. Flow) or futures-driven (e.g. Celsius).

Top 100 (7d %):

Flow (+59.2%)

Celsius Network (+42.5%)

Decred (+40.4%)

Quant (+28.2%)

Chilliz (+26.2%)

DeFi Top 100 MCAPs (7d %):

Dopex (+73.9%)

Rocket Pool (+37%)

Bounce (+29.6%)

Seedify.fund (+28.8%)

Ribbon Finance (+27.0%)

Curve launched TUSD / FRAX stable pool, current gauge APR is 6-15%, Convex offers 11%.

Velodrome announced that it will distribute 75,000 OP to veVELO holders, users have to have at least 10K veVELO by August, 10 to be eligible.

Stake DAO reported 7% and 11% APY performance of ETH CC and BTC CC v2 option strategies.

Solarbeam, Moonriver & Moonbeam AMM, updated xcKSM / stKSM farming pool, users can receive SOLAR, MOVR and LDO rewards for 50% total APR.

Global Market Cap

$1.18T (CoinGecko); Global market cap has grown 4% over the past week.

$52B; DeFi market cap has increased by 6% over the past week while DeFi dominance has been flat for the same period.

Bitcoin Dominance

Bitcoin dominance oscillating around 41% YTD with weekly RSI firmly in neutral territory. If we see continued strength in ETH/BTC in short-term, dominance will likely fall.

BTC/USD and ETH/USD

BTC/USD still below 50d MA but keeping above its 200d MA while W RSI recovering from being oversold (38).

ETH/USD fighting key levels with near-term direction likely driven by a convincing break above or below ($1.76k). W RSI also recovering from being oversold.

Volatility

Realized volatility for both ETH and BTC has been largely flat over the past week as market chop around within tight bands.

Trader Positioning

ETH printing lower put/call ratio as traders take a predominantly bullish stance. Bitcoin OI on CME remains flat in August while volume appears more muted. Bitcoin CME futures volume is forecast to reach $27B in August at current rate. This would be 28% lower July’s $38B print. ETH perp futures volume has picked up in recent week as traders likely look to hedge their ETH spot exposure.

Combined Order Books

Aggregate order books look fairly even for now. Source: Bitcoinity

Macro Correlations

Crypto vs. Equities vs. Gold vs DXY; Cryptoasset correlations with broader risk markets remain high (strong positive correlation; 0.89+) Any volatility in SPX and NDX over coming weeks is likely to trickle over into the cryptoasset market.

Trusts

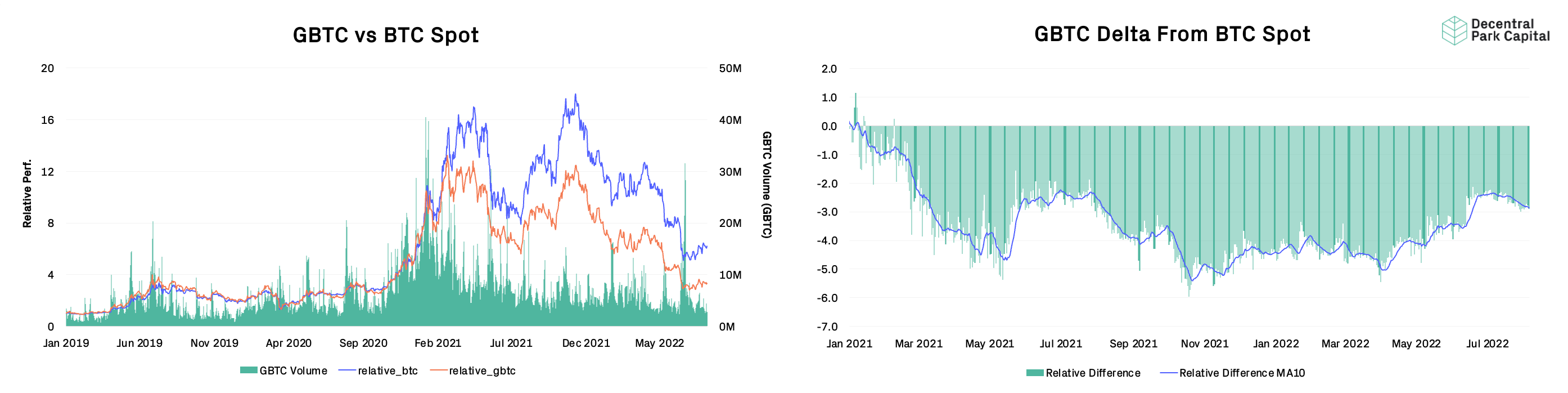

GBTC; GBTC discount hovering near all-time-highs as demand for GBTC shares on the secondary market remain low. GBTC 30D volumes continue to plummet (4.37M).

ETHE; ETHE discount narrowing likely from the growing merge narrative. However, this ETHE rally has been met with falling volumes from July highs (3.9M) so may not be a high conviction trading that is narrowing the discount.

Mempool Size

No notable increase in mempool size meaning demand for block space is relatively low.

Mining

Bitcoin hash rate appears to remain in a broader downtrend implying miner capitulation is maybe incomplete. Bitcoin hash ribbons reflects this dynamic too with no clear ‘buy signal’ yet printed for the metric.

Volumes

On-chain real (BTC) & off-chain volume; On-chain volume has been largely flat since early July while prices have increased (divergence).

Exchange Flows

Net exchange flows for BTC has yet to flip positive with more BTC being withdrawn than deposited.

📚 A16z Weekly [A16z]

📚 On Pivots [MacroAlf]

📚 Paradigm LP Letter Excert [Matt Huang]

📚 The Future of MEV [0xfbifemboy]

📚 Dimension of Web2 vs. Web3 [Antoniogm]

🎙️ Jan Hatzius On The Narrow Path To Avoid A Hard Landing [Odd Lots]

🎙️ Weekly Roundup Ep 338 [On The Brink]

🎙️ Complexity Theatre [The Breakdown]

🎙️ Crypto’s Liquidity Engine, OTC Desks, and CEXs [Empire]

🎙️ Why Global Liquidity Matters Now More Than Ever [Hidden Forces]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.