No Country For Old Frameworks

Gas Station Proprietor : Call it?

Anton Chigurh : Yes.

Gas Station Proprietor : For what?

Anton Chigurh : Just call it.

Gas Station Proprietor : Well, we need to know what we're calling it for here.

Anton Chigurh : You need to call it. I can't call it for you. It wouldn't be fair.

Gas Station Proprietor : I didn't put nothin' up.

Anton Chigurh : Yes, you did. You've been putting it up your whole life, you just didn't know it. It's been traveling twenty-two years to get here. And now it's here. And it's either heads or tails. And you have to say. Call it.

Gas Station Proprietor : Look, I need to know what I stand to win.

Anton Chigurh : Everything.No Country For Old Men (2007)

It’s been an eventful week.

While it would be impossible to cover all the happenings for the past 7 days in this newsletter, we will cover some of the key market signals Decentral Park continues to monitor.

What should be clear at this point is that the cryptoasset market is facing mounting pressures endogenously and exogenously.

Recent endogenous factors include 1) distressed lending companies such as Celsius working DeFi positions in an attempt to stabilize liquidity, 2) Three Arrows Capital unwinding its liquid book, and 3) Ethereum’s difficulty bomb. This of course comes at a time when the increasingly illiquid cryptoasset market was feeling the pressure from tighter monetary policies particularly in the US.

This brings us to the exogenous factors where the path to a global recession seems more likely than earlier in 2022. After the Fed raised rates by 75BPS, the terminal rate by the market has increased to 4%.

Crypto’s global market capitalization has fallen back below the $2T mark ($933B) as liquidations and deteriorating market sentiment became the key forcing functions last week.

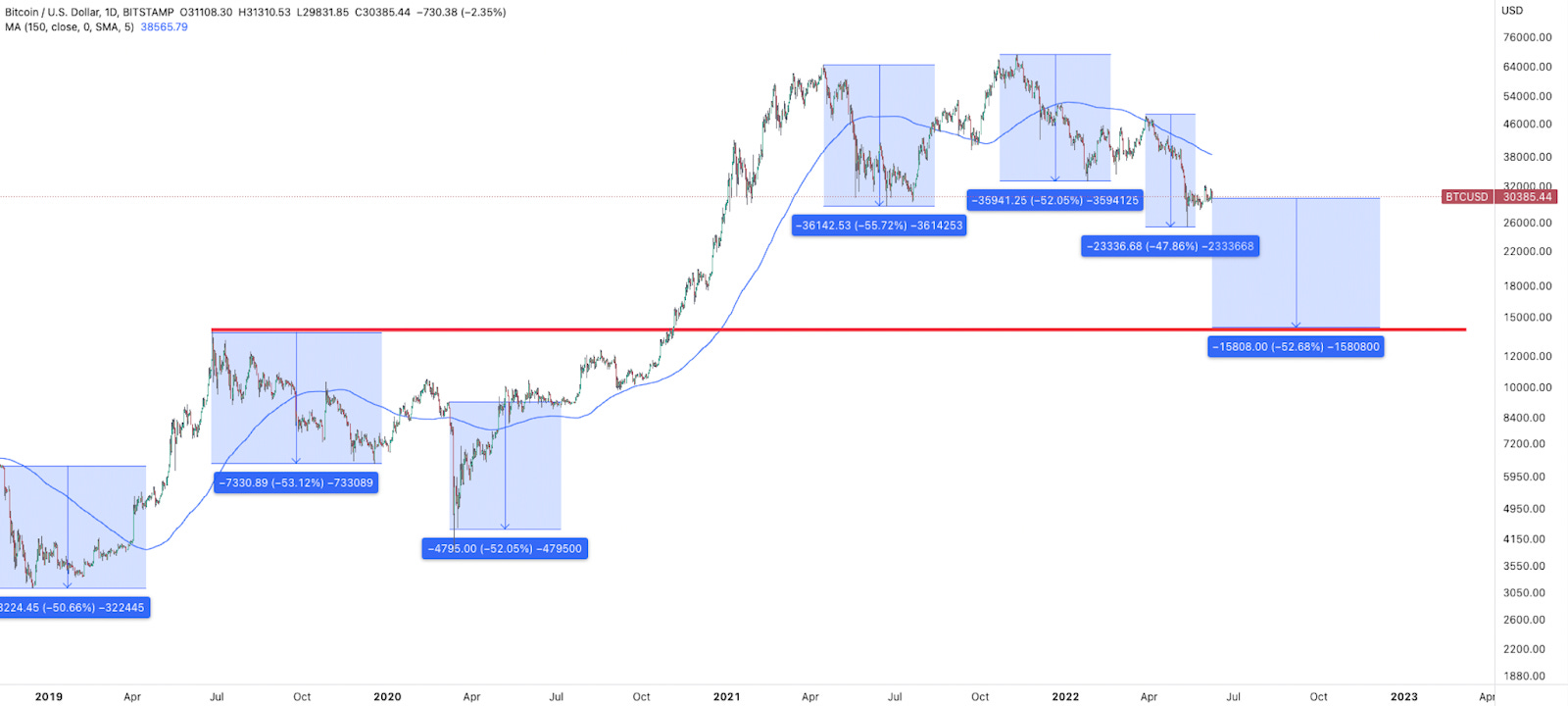

In early June, there were certain capitulation price forecasts for BTC that suggested a $20-$22.5k target. These included the 60M MA ($22.5k), Bitcoin Electricity Cost model ($20.2k), and 2018 re-trace move (-70% to $20.5k).

After the mid-June drawdown, Bitcoin oscillated around the $21k mark. Incorporating miners into the equation, hash ribbons model suggests a miner capitulation is well underway with no evidence yet of a price recovery.

The issue with extrapolating previous cycles to today is that the market structure we find today (and potential endogenous and exogenous price catalysts) are simply novel. Put simply:

What has worked in the past may not work in today’s market environment.

We have no historical data for how crypto may trade without quantitative easing - a policy rolled out in response to the 2008 financial crisis. That 14-year experiment has now ended and we’re now bracing for impact.

Over the weekend, BTC finally broke the $20k mark finding support at ~$17.6k. Bitcoin has often retraced 50%+ and so the 41% drawdown last week could be taken as a positive.

All eyes will now be on BTC/USD using $20k (2017-2018 cycle high) as new support or new resistance. Both exogenous and endogenous factors may act as forcing functions for outcomes the market may not be necessarily pricing in.

The macro outlook will continue to be a guiding light for most traders as Bitcoin remains strongly positively correlated to NDX throughout the previous week.

As global liquidity tightens and disposable income drops to new lows since 2008, it begs the question of who will be the new net buyers over the coming months?

As the market has drawdown, beta assets have underperformed DeFi indices (DEFIPERP) by 10%+.

With borrow/leverage positions often using BTC or ETH as collateral (incl. within DeFi), it may be that liquidation or forced selling by distressed companies are impacting beta more negatively than assets further down the risk curve.

That said, DeFi protocols that have been at risk of company unwinds (e.g. Celsius) have been underperforming both DeFi indices and beta.

For example, Aave has been used as the primary lending protocol for stETH leverage trades. With stETH/ETH ratio falling within Curve, borrow positions have been at high risk of liquidations with the net outcome being a mass exodus of capital (TVL).

For CVX, the stETH/ETH ratio falling would lead stETH-ETH LP tokens to be removed from Convex in size with stETH-ETH LP tokens making up ~12.5% of Convex TVL.

stETH/ETH has found stability at 0.93 after companies with sizeable stETH holdings have been swapping out for ETH or USDT (despite slippage).

The number of ETH in the stETH/ETH Curve pool now stands at 117k (source: LidoAnalytic) Curve’s pool tail risks mean ETH’s balance falling to <100k will make it much harder to re-balance the pool to maintain equilibrium. Aave has $1.36B of stETH supplied to its lending market.

As for Aave liquidations, we note a $147m collateralized debt position at risk of liquidation at $894 ETHUSD (-18% from current prices). For MakerDAO, $350m+ collateral at risk of liquidation at $630-$660 ETHUSD price and $350m at $13.5k WBTC/USD.

Note, these levels can change frequently with users/entities adding collateral or repaying debt.

A risk covered in previous editions of The Weekly centred around Ethereum’s difficulty bomb during times of potential capitulation.

The reality is that Ethereum’s declining network utilization and strong CEX dominance has meant that, while median block intervals have increased leading up to its difficulty bomb, median gas prices have fallen to annual lows.

It therefore remains unclear the extent in which network congestion plays a factor over the coming months from a sentiment perspective.

Call It

Today, we see cryptoasset prices trading around their previous cycle highs yet fundamental headwinds clearly remain.

An ‘exponential age’, long-term investment framework for cryptoassets may ease concerns around possible medium-term volatility. Yet, the potential for cryptoassets to extend their drawdowns from unwinds and tighter monetary policies (incl. their second order effects) still remain a real possibility.

Central banks may be waiting for things to break but the market is already showing signs of breaking. Mortgage backed securities receiving ‘no bid’ earlier in June is just one clear example.

It’s not an easy set up. Significant breaks below current key levels likely may in-turn lead to forced selling including from miners illustrating the risk of market reflexivity to the downside. This is despite cryptoassets already being at depressed prices.

So it appears we are at somewhat of an inflection point in the market.

So in spirit of Anton Chigurh:

We’ve been traveling since 2008 to get here. And now it's here.

Call it.

DeFi Factors

Solana

A whale’s $170m collateralized debt position on Solana’s lending protocol, Solend, is at risk of liquidation at a $22.3 SOL/USD.

20% of the position would be liquidated against an increasing illiquid market, increasing network congestion from liquidation activity - something that has previously led Solana’s blockchain to halt.

It is unclear whether Solend’s governance will pass an emergency takeover of the whale’s account.

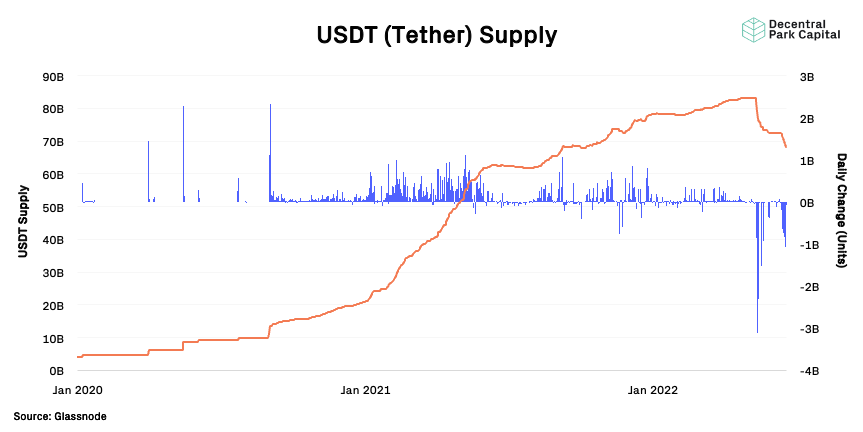

Tether

Tether is seeing its supply contract at an accelerated rate once again. $20B USDT was redeemed last month and at current average pace, supply will reach 50B in 1M and 40B in 2M.

Large traders may actually be incentivized to unwind Tether given its opaque, non-audited reserve backing (buy discounted USDT below peg or at peg, redeem, and repeat - all while they are net short on USDT/USD where profit is higher than at-risk redemption capital). The strategy for these traders being that eventually USDT is unable to be redeemed 1:1 for USD due to illiquidity.

It may also be that reduced USDT supply implies accelerated redemptions which may be from institutions looking to de-risk their cash positions.

A systematic unwind of Tether could potentially bring potentially unprecedented risk to the cryptoasset ecosystem where where the probability, while low, maybe higher than the market currently appreciates due to perceived incentivised for opportunistic traders.

Short squeezes have led to certain DeFi names to outperformance such as SNX with the possibility of other assets following suit as shorts get ahead of themselves.

Top 100 (7d %):

Helium (+30.4%)

Bitcoin SV (+30.2%)

Synthetic Network (+26.2%)

Elron (+22.2%)

Basic Attention (+18.9%)

DeFi Top 100 MCAPs (7d %):

Synthetic Network (+26.2%)

Ribbon Finance (+16.5%)

API (+15.8%)

GMX (+14.8%)

JOE (+10.4%)

Silo, a lending protocol to borrow any crypto asset with another, plans to launch mainnet beta in the end of June, more details coming.

Synthetix launched atomic swaps that allow low-slippage ETH <> USD <> BTC swaps through Curve pools, increased volume ($100M+ daily) resulted in 30% APR in sUSD and 27% APR in sETH pools. More details on atomic swaps here.

ZigZag, an orderbook DEX on zkSync, is rumored to launch a token (ZZ?) on the 24th of June.

Lido's stSOL now can be used as collateral in Solend and other lending protocols on Solana. LTV is set to 75% with 4% supply APR in LDO and SLND rewards.

Global Market Cap

$934B; Global market cap has fallen 15% over the past week although the wider trend remains down.

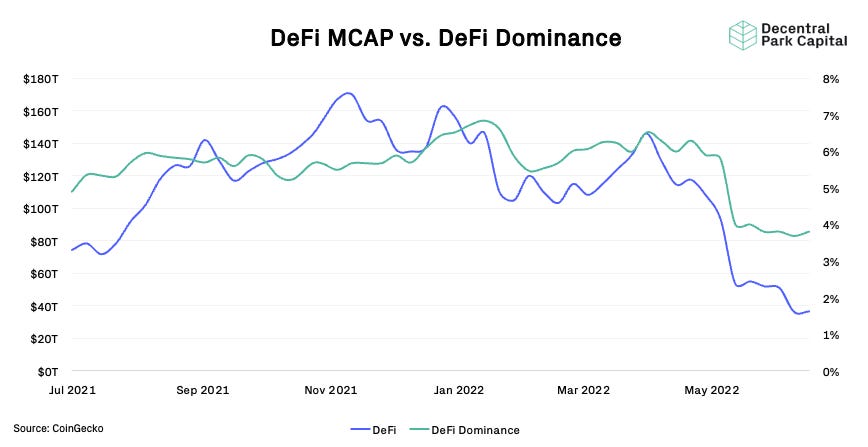

DeFi MCAP And Dominance

$36.6B; DeFi market cap has increased by 1% over the past week. DeFi dominance has increased by 3% as beta assets are hit by liquidation events.

Bitcoin Dominance

Bitcoin dominance has fallen to 44.3% as the orange coin loses relative market share against other high cap names.

BTC/USD and ETH/USD

BTC/USD and ETHUSD back above key lines - $20k and $1k respectively. Unclear whether to be used as new support or flipped to resistance. Daily RSIs recovering but remain very low indicating assets are still oversold. ETH/BTC hovering at June 2021 support (0.055) after forming bear flag pattern.

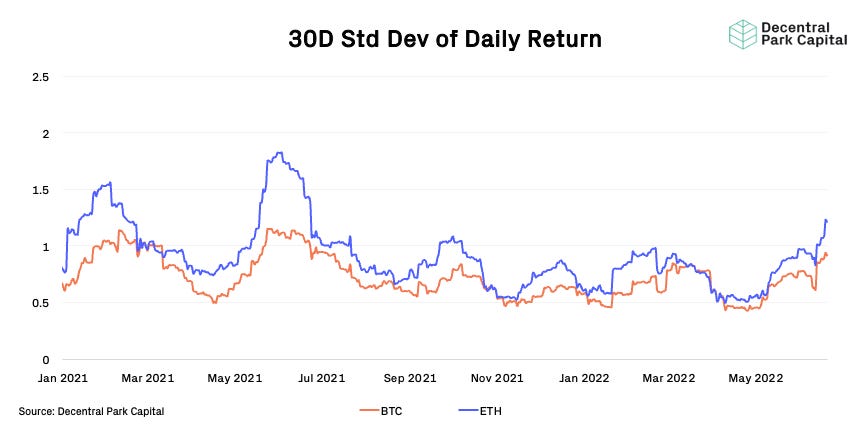

Realized Volatility

BTC & ETH; Sharp increases in realized vol for ETH unsurprisingly. 30D Implied vol for BTC and ETH remain elevated vs. earlier in the month (100 and 122 respectively)

Trader Positioning

Put/call ratio for ETH continues to fall while (0.32) while BTC remains elevated (0.68) implying a more bearish skew in positioning for the latter. Funding rate for ETH turned moderately positive as traders take a predominantly bullish stance in the futures market.

Combined Order Books

Order books look fairly even. Slightly heavier resistance up to $21.1k. (Source: Bitcoinity).

Crypto vs. Equities vs. Gold vs DXY; Cryptoassets remaining positively correlated to equity indices like SPX and NDX.

Grayscale Trusts

GBTC; GBTC discount widening to new ATHs (34%). Three Arrows Capital were one of the largest GBTC holders (38.8m shares) but appears they have offloaded potentially via OTC. Discount has been widening at a faster rate than ETHE.

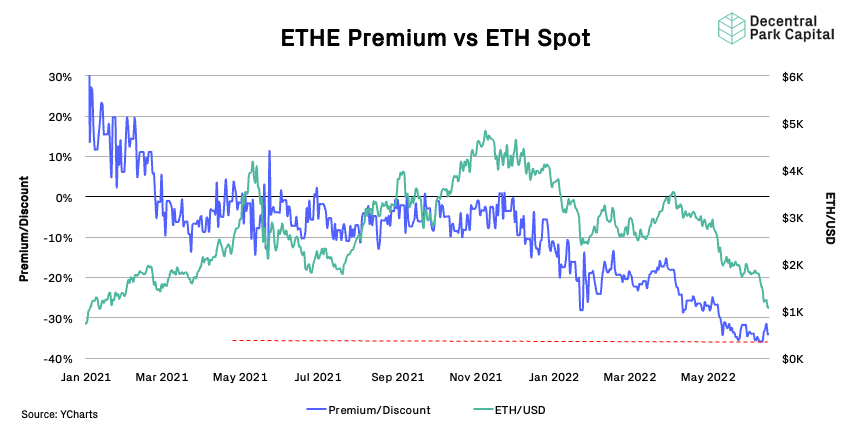

ETHE; GBTC discount still hovering near all-time highs (-34%) and driven by wider spot action. ETHE secondary market volumes have hit 5m for the first time since March 2022.

Mempool Size

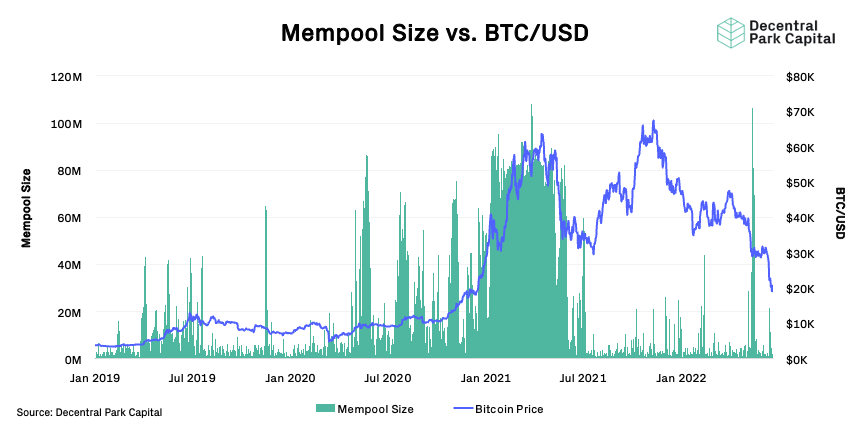

Size in MB; The mempool size for the Bitcoin network spiked but remains relatively low with few high value transactions competing with low value ones.

Bitcoin Hashrate

Bitcoin hashrate (7D) has fallen 10% as miner revenue falls 50% since April 2022. Bitcoin miners can remain profitable if BTC/USD keeps above its electricity cost ($20.2k).

Volumes

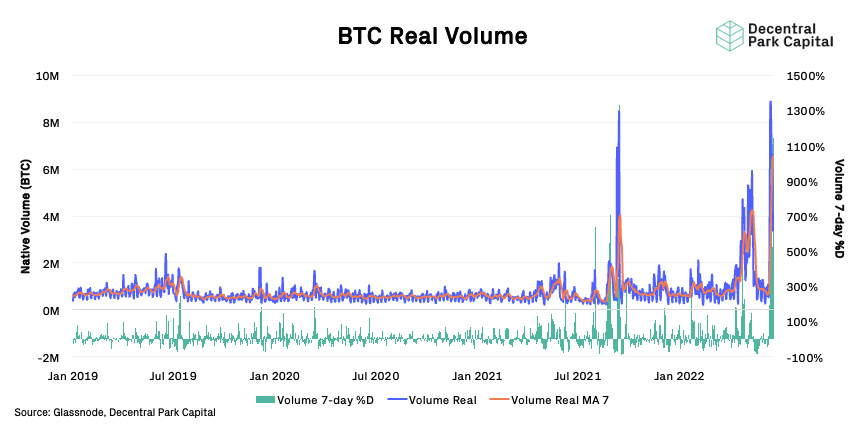

On-chain real (BTC) & off-chain volume; On-chain volume has spiked over 700% while spot volumes have increase 100% (7D MA).

Active User Base

BTC; The Bitcoin network is seeing a less active user based. Active entities has fallen 1% over the past week.

Exchange Flows

BTC, ETH; Exchanges are seeing net inflows of $780m of ETH but net outflows of $1B for BTC. Miners have also been sending ~100-150 BTC to exchanges from their wallets which, according to Glassnode, is 2-3x volumes seen in April 2022.

📚 Cryptoverse Download #1: The Convexity of Bitcoin mining at 20k BTC [Cryptoverse Download]

📚 On Babel Finance [Blockanalia]

📚 Solend Saga [0xrooter]

📚 Housing Market On The Edge [Bloomberg]

📚 A16z Report Takeaways [cryptoPothu]

🎙️ On Scalability With STARKs [On The Brink]

🎙️ Why It’s So Hard To Get The Oil Taps On [Odd Lots]

🎙️ The Importance Of Risk Management [The Scoop]

🎙️ US Recession odds Surge Over 70% [The Breakdown]

🎙️ Can Crypto Find A New Narrative? [Empire]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.