The Weekly #200

A relief bounce during a not so relieving situation

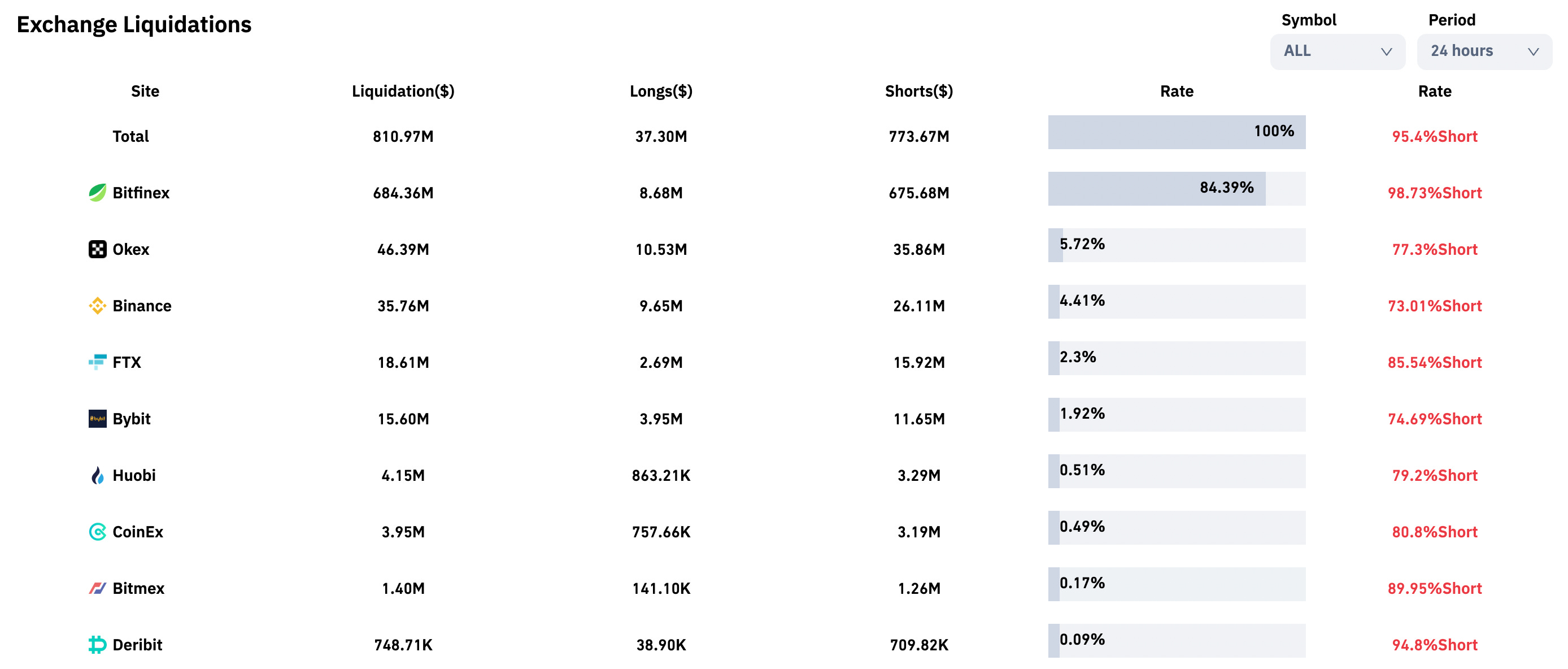

After a relatively quiet weekend, cryptoassets have been bid up with the help of a number of short liquidations in the past 24 hours.

A total of 51,500 traders have been liquidated to the sum of $811m. The large majority of these traders caught out shorts. Futures funding rates remain moderately positive with traders taking a predominantly bullish stance.

It’s clear that illiquid markets have help accentuate moves both the downside and upside.

For beta assets like BTC, key levels ($30k) have been breached but has faced initial resistance at $31.4k in morning hours. While we are seeing buying power below $30k we are equally seeing selling power at these levels.

Bitcoin (along with other, highly correlated cryptoassets) remain weak until $33k level and beyond are broken convincingly.

The Cha Cha Slide

We can point to key macro events this week that may act as a guide post for price action near-term.

Both the US and ECB are set to release CPI numbers. For the US, inflation data will be released on June 10th with forecasts showing an annual increase of 8.3% - in line with April’s print. The 10Yr breakeven inflation rate is also at a 1M high.

No ‘significant’ decline in inflation means the Fed’s 50 BPS hikes in upcoming FOMC meetings seem more likely than ever to materialize. Unemployment claims also fell although payroll growth itself slowed down in May.

However, arguably the most interesting markets are US bonds with the 10Yr eyeing up the 3% yield once again.

Yields in current market cycles have never breached their previous cycle highs and a sustained breach of 3% will likely mean the market is now structurally very different.

A potential re-test of those levels within this market cycle is already significant. So much so that hedge funds became net sellers at the end of May. Taken together, sustained inflation expectations as told by the bond market would mean yields are more likely to remain elevated than significantly retreat by Q3.

It’s unclear whether high inflation prints will collapse cryptoasset prices from here. What’s more clear is the risk assets are looking for a direction and that material moves to the downside in equities will be the ultimate driving factor.

And the picture remains bleak. Credit impulse and forward P/E ratios all indicate potential future declines until a Fed put.

Market Structure

The cryptoasset market is likely not yet structurally at ‘peak capitulation’. For BTC, several indicators point to a potential $20k-$22k support zone.

These include technical indicators like 60 month exponential MA as well as on-chain indicators such as BTC’s production cost and STH-LTH realized price ratios.

For alternative L1s, market cycle history could be key with ‘poster child’ names mirroring the longer standing names during previous cycles.

An example here could be SOL which may end up mirroring ETH’s first cycle drawdown of ~94%. Through this framework, a $12 SOL is no longer inconceivable but, as highlighted above, a more painful macro development is what would ultimately drive us to that point.

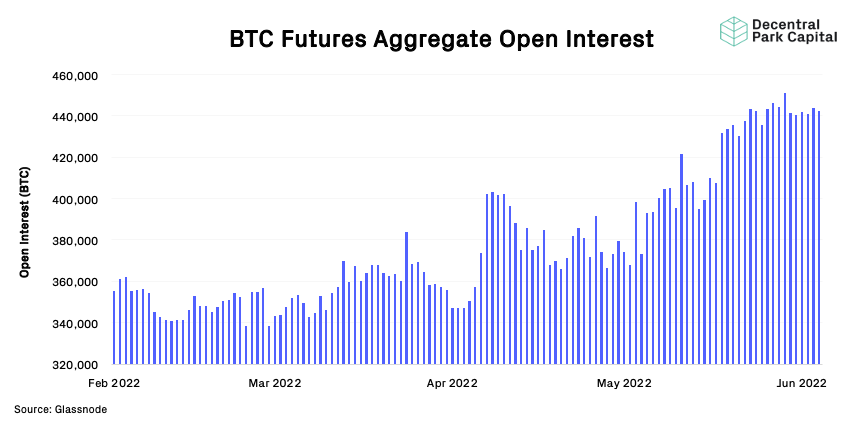

High interest in the futures market may also accelerate price movements too with aggregate open interest for Bitcoin futures remaining flat but elevated at 444k BTC. This is despite recent liquidations we’ve seen.

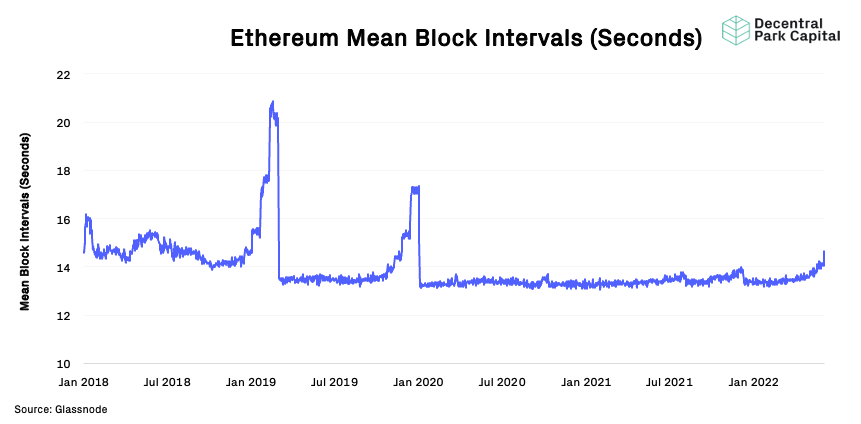

At the same time, idiosyncratic risks for Ethereum could revolve around its difficulty bomb.

The net result is a harder mining environment that extends out average block times and higher gas fees as network participants compete for block space.

Despite scheduled for sometime in June, we are already seeing the early signs of potential difficulties to come. Mean block intervals are already ticking up to 14.6 seconds - up from 13.5 seconds in early May. Ethereum core developers are in agreement that the difficulty bomb should be delayed by 2-4 months.

Just as investors may look to make on-chain trades, higher demand for block space during high network congestion will do little to buoy sentiment. That said a ‘bomb flush-out’ and successful merge may equally come after a further ‘price flush-out’ driven by macro.

For now, expectation of directional action in the market seems skewed to the downside than to the upside.

So in the words of Mr C: “How low can you go?”.

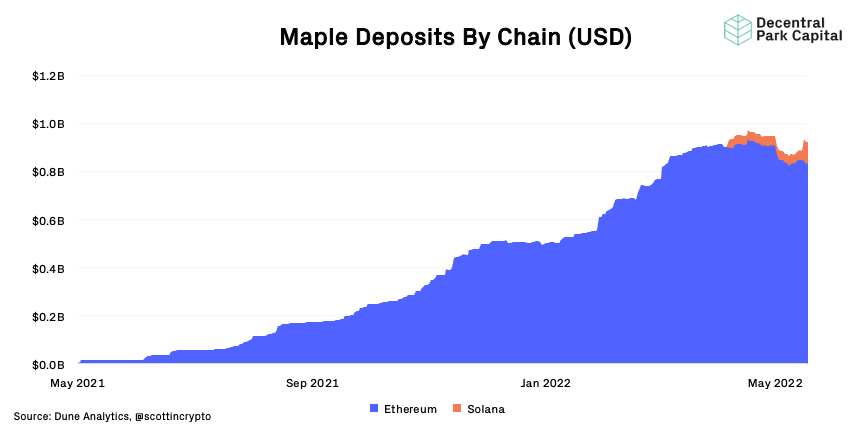

Maple Finance

Maple Finance has seen a healthy uptick in total deposits on its Solana platform which now stands at $90m (2x 7D).

Using an undercollateralized loan model for longer duration means Maple’s TVL can be more sticky and using USDC as a core loan asset means it can be relatively stable too. This comes as Genesis becomes the first CeFi to join Maple Solana as a pool delegate.

Since Maple released xMPL staking, over 27% of the circulating supply is now staked to earn MPL rewards. Note, staking does not lead to token price appreciation a priori.

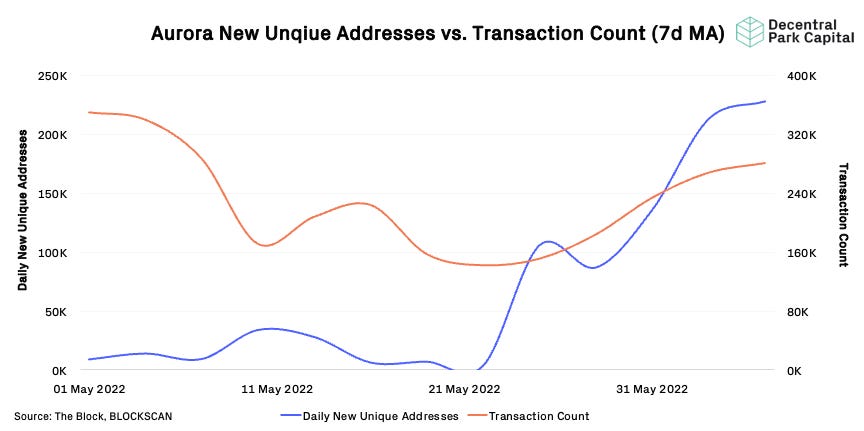

Aurora

Near’s EVM layer, Aurora, has seen significant uptick in daily new unique address since mid-May (10x). Simple transaction count has kept largely flat over the same period.

Potential catalysts for uptick in active user based include Trisolaris revamping its token economics and theses written around Aurora NFTs.

No clear theme across top performers for the week. We are seeing relief rally in assets that were sold off the most including Anchor and Fantom over the past month but base case is these rallies are temporary.

Top 100 (7d %):

eCash (+19%)

Theta Network (+16.2%)

Helium (+16%)

Cardano (+13.9%)

Loopring (+14%)

DeFi (7d %):

Bella Protocol (+31.4%)

Balancer (+17.4%)

Loopring (+14%)

Dopex (+12.5%)

Curve DAO (+12.2%)

Curve’s 3pool stabilized after parameter change with USDT share dropping from 75% to healthier 60%.

Balancer is launching on Optimism L2, OP liquidity mining rewards are expected, details TBA.

Hop Bridge is going to use 1m OP tokens to cover up to 80% of gas costs for users bridging to Optimism network. Proposal is expected to go live when Hop DAO is launched.

Stake DAO was whitelisted to lock BAL tokens, allowing it to implement sdBAL liquid lockers similar to sdCRV model. Users will be able to enjoy veBAL rewards while staying liquid.

Theme 1: Policy, Regulation, & Markets

We are anticipating a draft proposal next week for broad-based US legislation from Senators Lummis (R-WY) and Gillibrand (D-NY):

Crypto Implosion Juices Senate Odd Couple’s Push to Clamp Down (Bloomberg)

Lawmakers introduce bill to include crypto in Congressional disclosures (The Block)

Crypto firm Ripple will explore IPO after SEC lawsuit ends, CEO says (CNBC)

Theme 2: Bitcoin

The New York legislature approved a bill last week to limit crypto mining in the great state and it is now with the governor to sign into law.

New York Legislature Approves Bill to Limit Cryptocurrency Mining (WSJ)

New York Attorney General Warns of Risks in Crypto Investment (WSJ)

Environmentalists Target Greenidge as They Turn Up Pressure on NY Governor to Sign Mining Moratorium Bill (CoinDesk)

Theme 3: Stablecoins

Global stablecoin regulation took a big step forward last week as Japan passed targeted regulation and the Bank of England/HM Treasury issued a report indicating there could be a rescue in the event of mass retail contagion.

Why Regulators Are Worried About Stablecoins (WSJ)

Japan Passes Stablecoin Bill Aimed at Protecting Crypto Investors (Decrypt)

Bank of England to Rescue Collapsing Stablecoin Issuers—If They’re Big Enough (Decrypt)

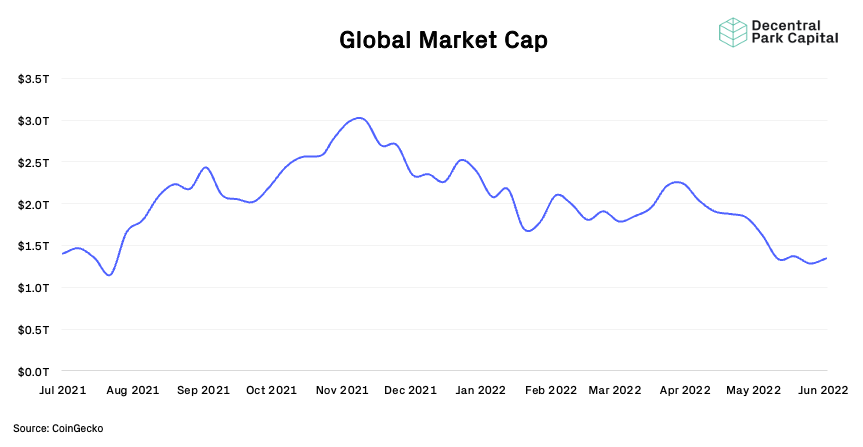

Global Market Cap

$1.34T; Global market cap has increased 5% over the past week although the wider trend remains down.

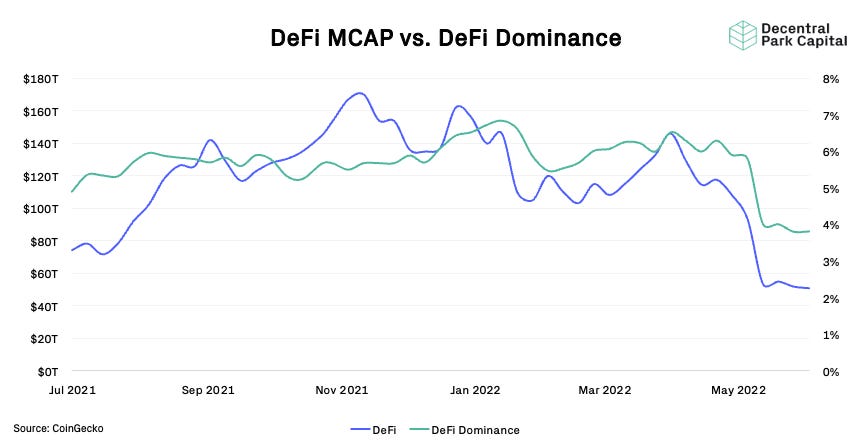

DeFi MCAP And Dominance

$54B; DeFi market cap has fallen by 2% over the past week. DeFi dominance has increased by 1%.

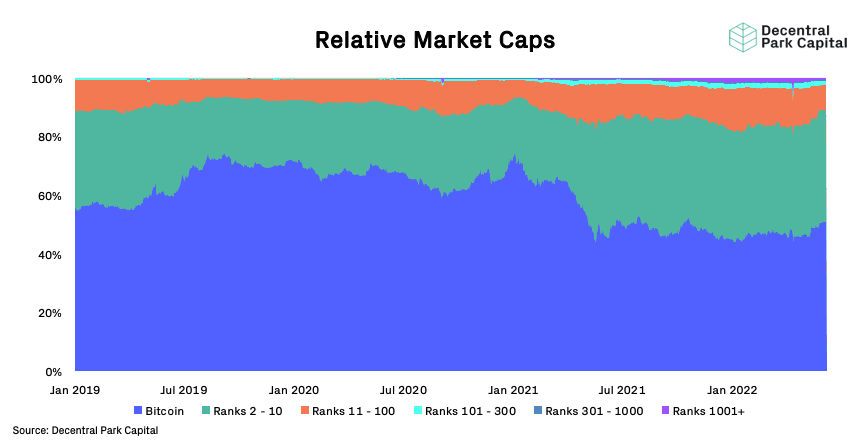

Relative Market Caps

Bitcoin dominance has climbed to 51% - a new high since mid-October 2021. The orange coin has been holding relative value against most other cryptoassets over the past month.

BTC/USD and ETH/USD

ETH/BTC

Relief bounce in assets over last 24Hrs with relatively low spot volume. BTC and ETH key resistance at $32k and $2k respectively. Daily RSIs largely in neutral territory with bullish divergence formed over May for BTC/USD. ETH/BTC potential RSI divergence forming on the daily. ETH/USD printing lower highs and flat bottoms.

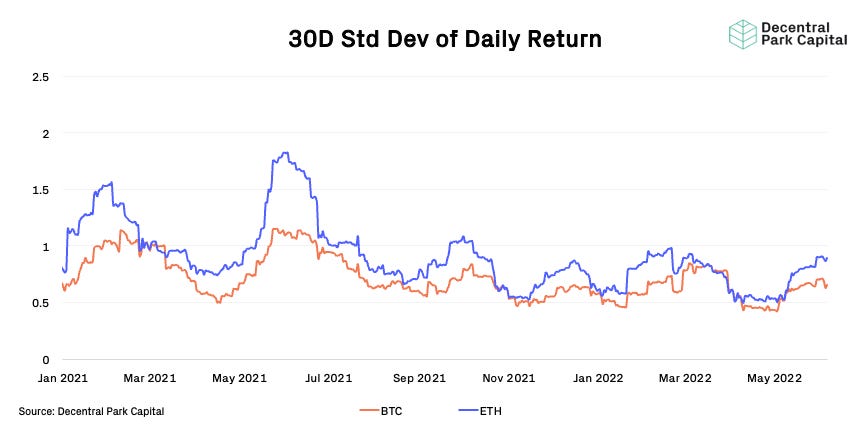

Realized Volatility

BTC & ETH; Slight increase in realized vol for ETH. 30D Implied vol for BTC and ETH fallen over the past week to 63 and 77 respectively.

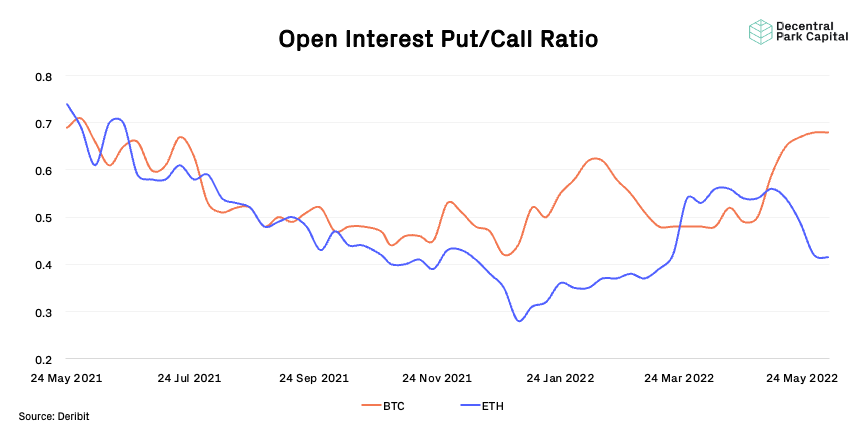

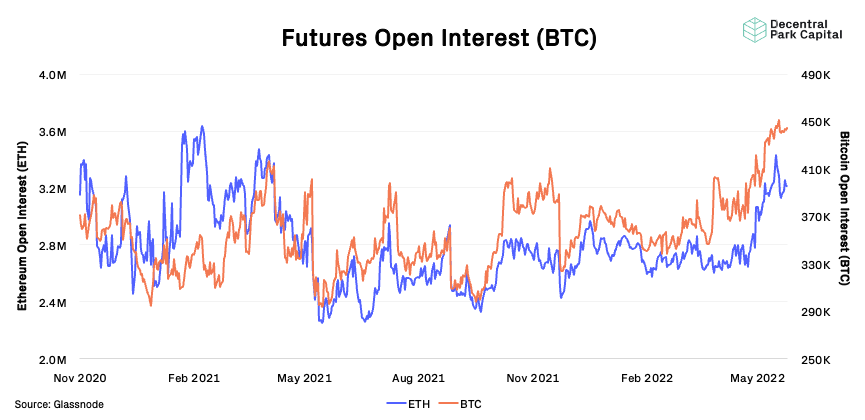

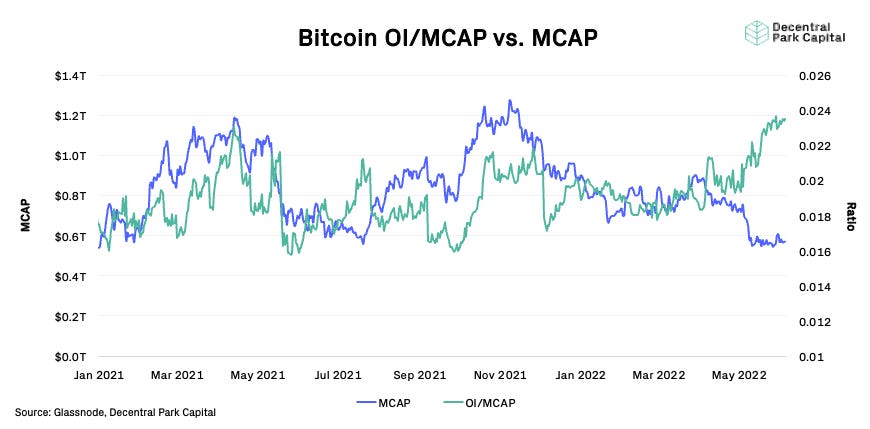

Trader Positioning

BTC out/call ratio remains elevated but flat while ETH has diverged away (declined) since mid-May 2022. Open interest for BTC and ETH remain elevated despite recent liquidations and price action. Positive funding rates across the board indicating bullish dominance by traders. Flat market capitalization with elevated open interest has kept OI/MCAP ratio at annual highs.

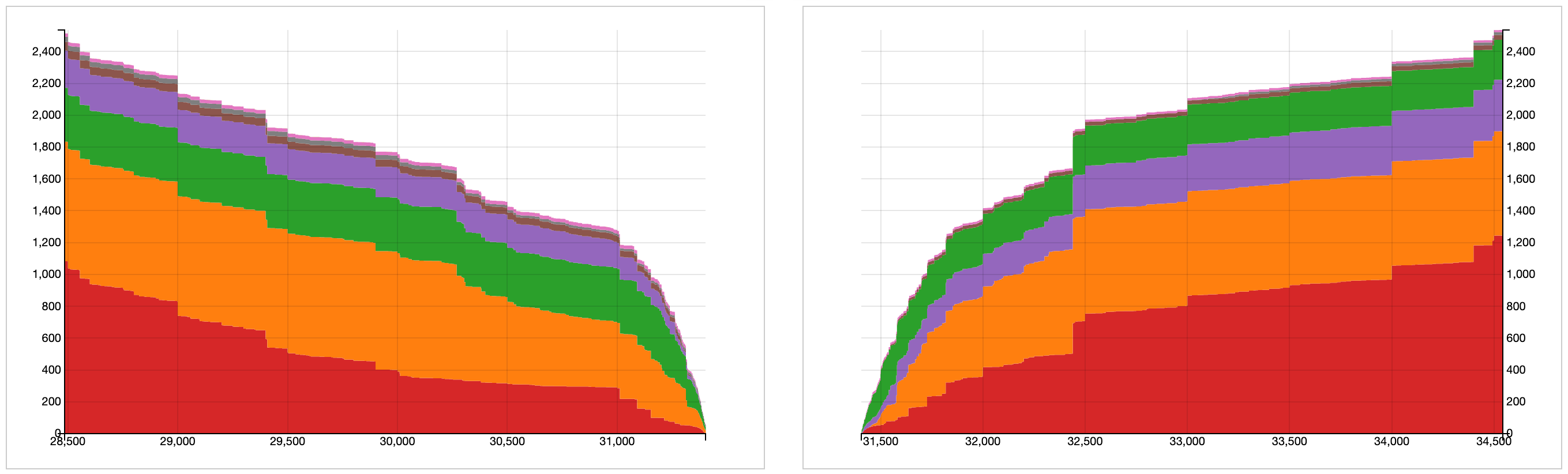

Combined Order Books

Order books look fairly even. Slightly heavier resistance up to $32.5k. (Source: Bitcoinity).

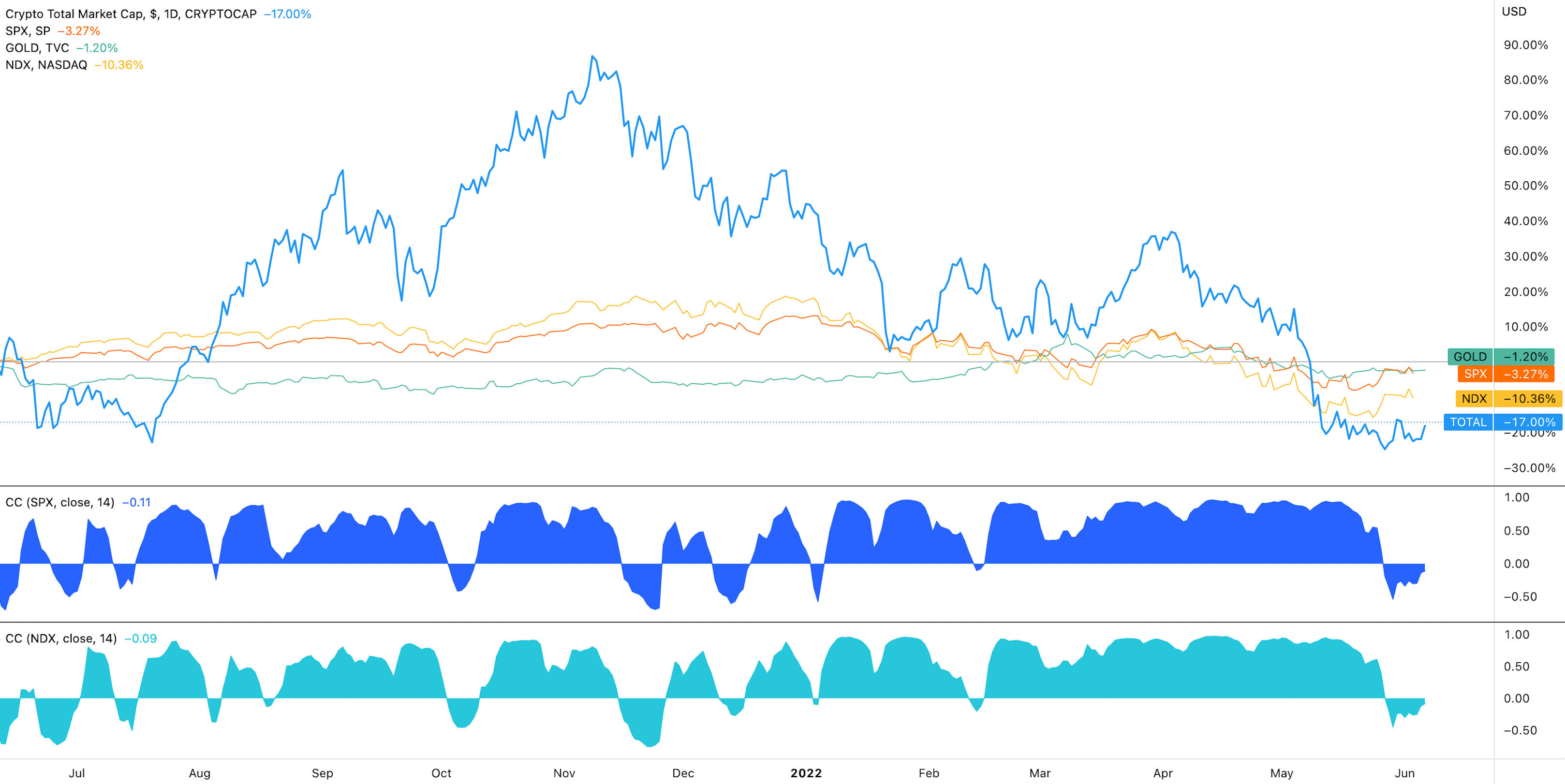

Crypto Correlations

Crypto vs. Equities vs. Gold vs DXY; Cryptoassets having a negative correlation to equity indices as crypto traded lower against a recovering stock market. Negative correlation appears to be weakening over the past week as both start moving in lock step once again.

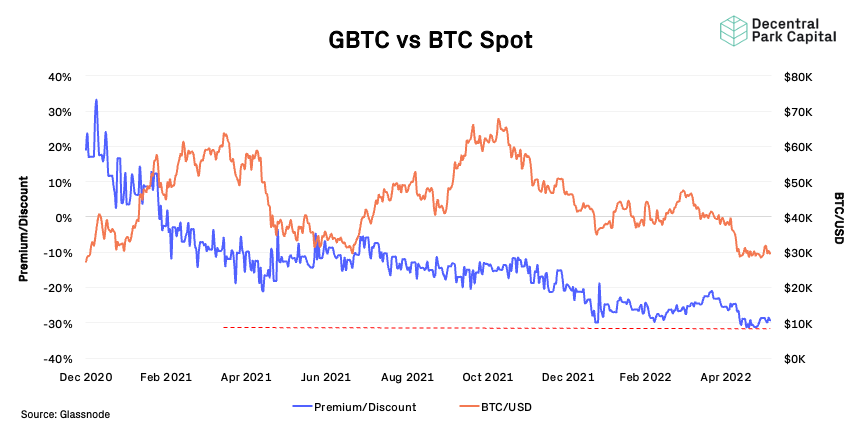

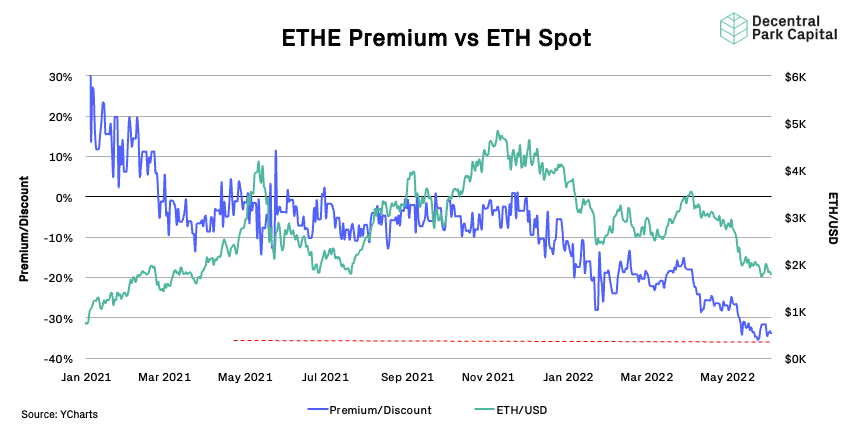

Grayscale Trusts

GBTC; GBTC discount still hovering near all-time highs (-29.43%) and driven by wider spot action. GBTC secondary market volumes have stayed flat over the past week as investors take a sit and wait approach.

ETHE; Discount remains near ATH (35%) and also driven by wider spot action. ETHE secondary market volumes also kept flat over the past week meaning there is very little dynamically between ETHE and GBTC at present.

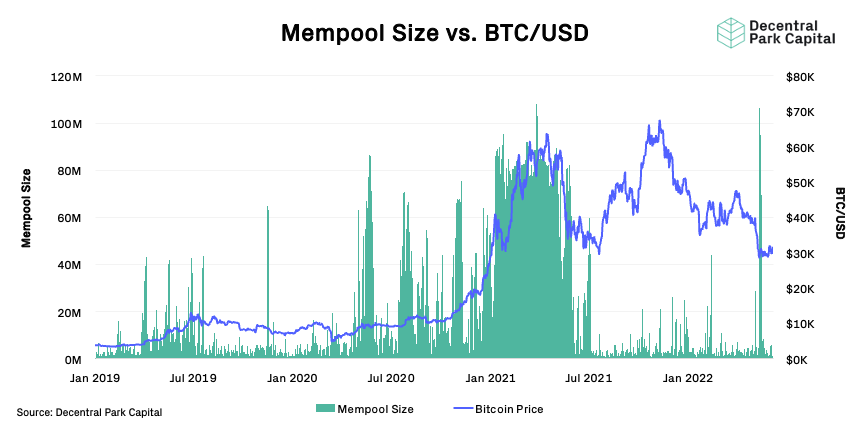

Size in MB; The mempool size for the Bitcoin network remains low will few high value transactions competing with low value ones.

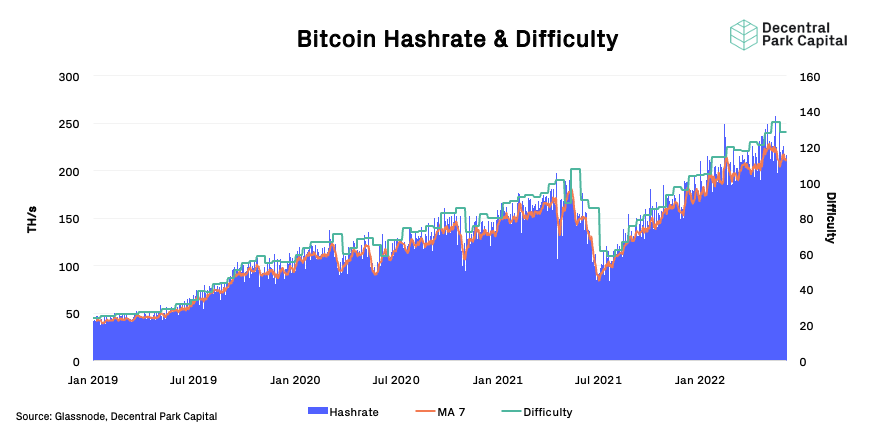

Bitcoin Hashrate

Bitcoin hashrate (7D) has fallen slightly over the past week (-3%) as miner revenue fell 21.6% to $900m in May.

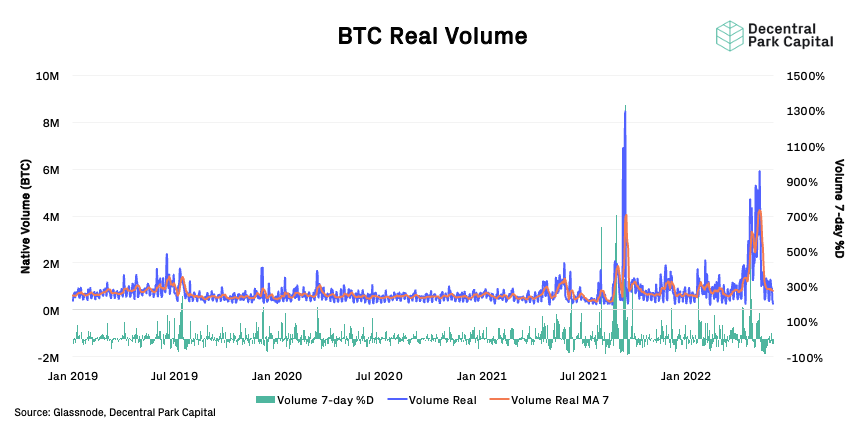

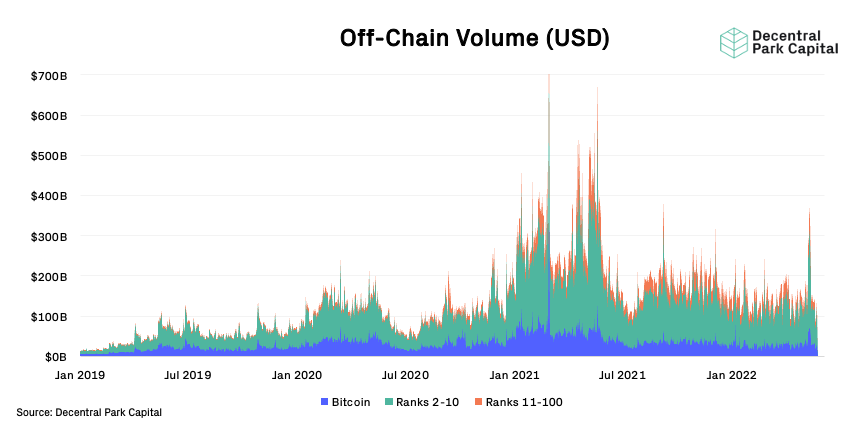

Volumes

On-chain real (BTC) & off-chain volume; On-chain volume has fallen 9% over the past week while global off-chain volume (exchange) has fallen 5%.

Active User Base

BTC; The Bitcoin network is seeing a less active user based. Active entities has fallen 2% over the past week.

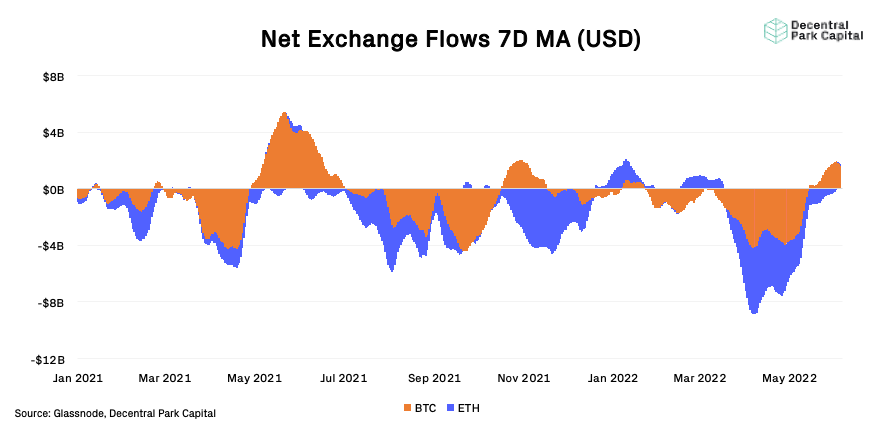

BTC, ETH; Exchanges are seeing net inflows $1.5B/day for BTC while ETH is seeing $175m/day. The divergence here may be due to Bitcoin miners selling inventory due to depressed prices.

📚 Porter Finance Launch [Porter Finance]

📚 Token Vesting [Blockanalia]

📚 Solana Mainnet Outage Report [Solana Status]

📚 On Protocol Controlled Value [SalomonCrypto]

📚 Evolution Of Token Distribution Models [CoinList]

🎙️ Silvergate CEO Alan Lane On The Business of Stablecoin [Odd Lots]

🎙️ The Everything Bubble [Empire]

🎙️ Weekly Roundup [On The Brink]

🎙️ It’s OpenSeason For Regulatory Enforcement [The Breakdown]

🎙️ DyDx On DeFi’s New Users [The Scoop]

Decentral Park is hiring! Please reach out to hr@decentralpark.io with your CV if you wish to apply for the following positions:

Decentral Park is an equal opportunity employer.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.