Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below.

The crypto markets saw some recovery over the past few days with total market capitalization reaching climbing 5%.

Beta assets like BTC climbed back above key resistance of $30k with low spot volume. It appears the bull/bear wars continue to battle out around these zones.

Despite best efforts by bulls, $31k-$32k remains a tough resistance zone and a convincing breakout above here would be needed for support of a large reversal pattern. ETH/USD faces similar challenges around the $2k mark with ETH/BTC facing key resistance at 0.069.

Capital has flowed down the risk curve this week with slight outperformance with alternative Layer 1 assets like AVAX (+4.4%) and SOL (4.5%).

Crypto’s relief rally can be partly attributed to a weaker dollar (DXY). Investors have been exiting the greenback on hopes that loosening lockdowns in China could finally help global growth with supply chains still be negatively affected. DXY has been on a correction course since its bearish RSI divergence.

This appears to be a temporary correction with the fundamental story for dollar strength not likely to have changed. In other words, the dollar Milkshake is being drunk before the Fed unwinds its balance sheet in June.

It can also be attributed to the broader equity markets too. Equity futures are starting the week in green territory (SPX +1.01%) and appear to be recovering from their yearly lows for now.

But we may not be out of the woods. The S&P fell 21% from its ATH but for the past 12 recessions since WWII, the median S&P correction has been 24% with an average of 30%. For broader bear markets, the average decline has been 37.3%.

Greg Jensen (Bridgewater) echoes wider concerns stated that inflation and slowing economy is a ‘toxic mix’ for markets over the coming months.

There are endogenous risks within crypto that also point to further drawdown volatility too. We are also seeing net exchange inflows for beta assets like BTC (~$560m) as the asset consolidates around $30k. In other words, more BTC being deposited to exchanges than are being withdrawn which can be seen before and during declines in price.

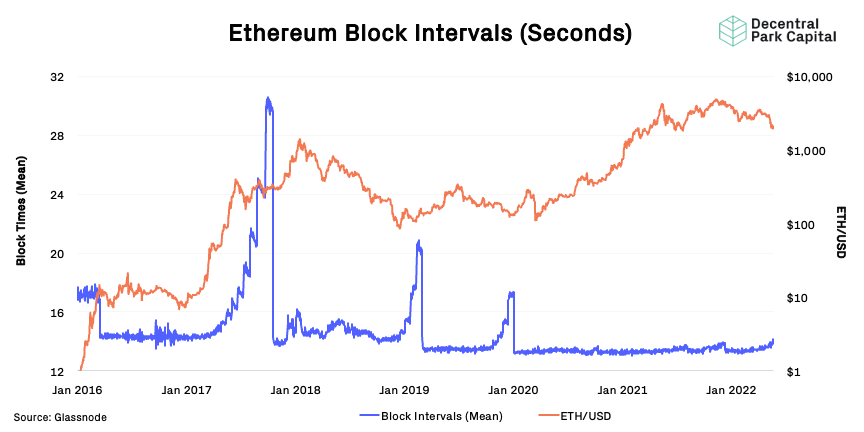

Ethereum’s Difficulty Bomb Is Ticking

Ethereum’s difficulty bomb was set up to accelerate the transition to a proof-of-work network. The ‘bomb’ exponentially increases the difficulty levels of the puzzles required for proof of work mining.

The net result is a harder mining environment that extends out average block times and higher gas fees as network participants compete for block space.

The Arrow Glacier fork pushed the difficulty bomb activation to June but we can see early stages of the activation today.

Ethereum block times have increased to highs since the last activation December 2019. Note that the bomb activation periods often coincide with local market bottoms but not necessarily cycle bottoms.

This makes intuitive sense purely from a sentiment perspective. Times of high network congestion are often associated with negative sentiment as low-value transactors are unable to participate on the network.

Miners leaving the network may also accentuate the problem as making a profit becomes equally hard. This would result in a lower hashrate for the network which we are starting to see come down from ATHs levels already.

It remains unclear whether Ethereum’s difficulty bomb will lead users to alternative ecosystem. Even more unclear whether this leads to outperformance of their respective cryptoassets too.

On May 27th, Ethereum core developers will be discussing whether to delay the difficulty bomb or not with the decision directly informing the timing for the merge mainnet activation.

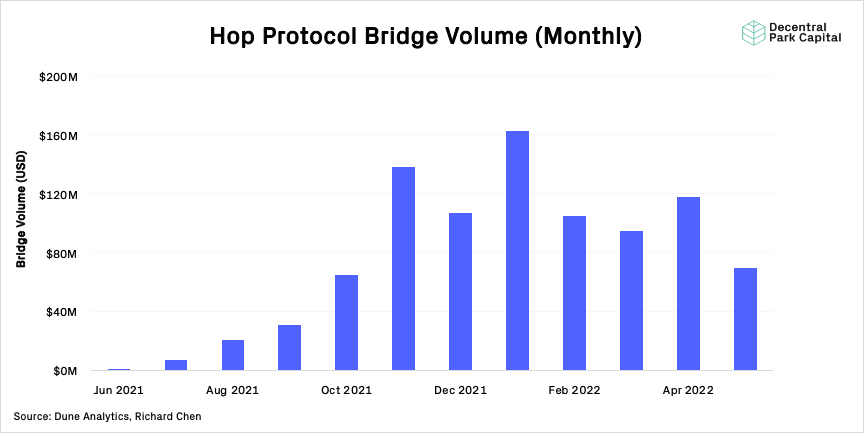

Hop Protocol

Volumes across DEXs within DeFi are on track to fall ~40% in May at current pace from April. We can see bridge volumes are also following the same pattern too. Hop Protocol has facilitated $70m so far in may - far below its $120m print in April.

Overall usage in DeFi remains muted as investors. This is also impacting the total liquidity deposited to protocols including bridges like Hop which has fallen 25% since its March peak ($100m).

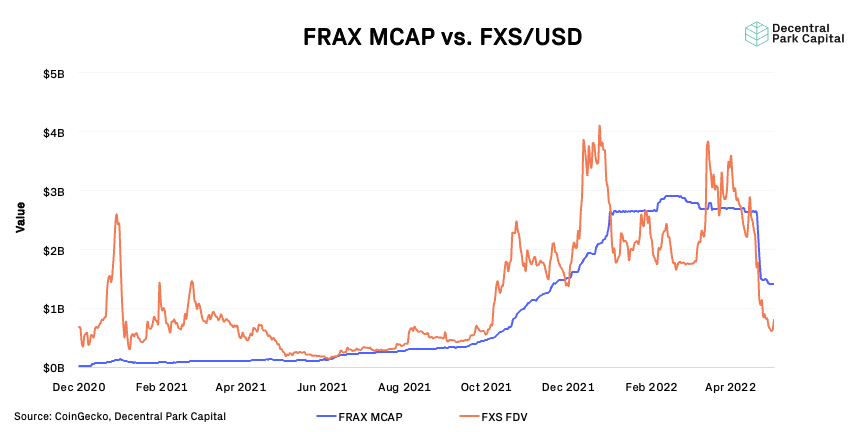

Frax Finance

FRAX’s stablecoin supply has fallen from 2.9B in March 2022 to 1.4B today - marking a 51% decline. A major catalyst has been the changing sentiment around stablecoins since the fall of LUNA/UST.

Decentral Park’s governance-as-capital valuation methodology for Frax Share posits that both FRAX and FXS are cointegrated. Since FRAX decline in popularity, FXS has underperformed the wider market by 58% MTD.

This is despite FRAX being able to maintain its peg for the past 2 weeks sufficiently well. Mechanistically FRAX is performing as designed but its risk against broader market sentiment remains.

No clear theme across top performers for the week. We are seeing relief rally in assets that were sold off the most including Anchor and Fantom over the past month but base case is these rallies are temporary.

Top 100 (7d %):

Fantom (+16%)

Kalytn (+21.6%)

KuCoin Token (+16.9%)

Aave (+13.4%)

Monero (13.2%)

DeFi (7d %):

IDEX (+67%)

Anchor Protocol (+66%)

Augur (+62.1%)

Kyber Network Crystal (+44%)

Nest Protocol (38.5%)

Voting for Silo's first lending markets has ended, the protocol will launch in beta with 10 markets including CVX, APE, FXS, stETH.

New incentivised stSOL - USDH pool is live on Raydium, LPs will receive LDO and HBB rewards, current APR is 70%.

Lido and Maker launched new WSTETH-B vault. Users now can borrow DAI against stETH with lower stability fee (0.75%) and higher liquidation ratio (185%).

Stake DAI launched new passive semi-stable agEUR - FEI LP strategy with 4.44% APR.

Theme 1 - Global Leaders Chime In

Key heads weigh in on crypto risks while acknowledging its power within the global markets.

Crypto assets are ‘worth nothing,’ says ECB’s Christine Lagarde (Politico)

Billionaire Bill Ackman Calls Terra a ‘Crypto Version of a Pyramid Scheme’ (Decrypt)

Bitcoin's Underlying Value 'Is to Do Ransomware': Former Fed Chair Bernanke (Decrypt)

Theme 2 - Key Hires

Big week for Web3 hiring.

Binance US hires former DOJ official as head of legal (The Block)

Polymarket appoints former CFTC chief Giancarlo as chair of advisory board (The Block)

Crypto Analytics Firm TRM Hires Ex-DOJ Cyber-Digital Task Force Chair (WSJ)

Theme 3 - Emerging Markets

EMs are calling for a sharper security regulations.

Panama's president not ready to endorse crypto regulation bill (The Block)

Nigeria’s SEC Affirms All Digital Assets Are Securities in New Rulebook (CoinDesk)

Portugal Makes U-Turn on Cryptocurrency Tax (CoinDesk)

Global Market Cap

$1.36T; Global market cap has increased 3% over the past week as traders de-risk from positions further.

DeFi MCAP And Dominance

$55B; DeFi market cap has also increased 3% over the past week. DeFi dominance has stayed at 4%.

Bitcoin dominance has stayed relatively flat over the past week (~49%). Bitcoin keeping relative value against alternative cryptoassets.

BTC/USD and ETH/USD

Some recovery in BTC/USD but yet to breakout above $31k-$32k resistance zone. Largely kept range-bound with low spot volume. ETH/USD facing resistance at $2.1k. Daily RSI oversold but heading closer to neutral territory.

ETH/BTC

ETH/BTC also keep range-bound so far with dynamics appearing similar to BTC/USD and ETH/USD. Resistance at 0.069.

Realized Volatility

BTC & ETH; Slight increase in realized vol for BTC and ETH. 30D Implied vol for BTC and ETH fallen to mid-March levels and suggests price action may be less choppy over coming weeks.

Trader Positioning

Moderately positive funding rate for BTC and ETH. Indicates traders remain predominantly bullish but low conviction either side. New ATH in BTC denominated OI (437k) which is outpacing market capitalization growth. Put/call ratio for BTC remains elevated after hitting 12-month high.

Combined Order Books

Order books look heavier on the ask side. Slightly heavier resistance up to $30.7k. (Source: Bitcoinity).

Crypto Correlations

Crypto vs. Equities vs. Gold vs DXY; Cryptoassets maintaining a moderate positive relationship to equity indices (0.42 for 14D) indicating cryptoassets are being traded as value and growth stocks. Gold recovering over the past week from a weaker dollar.

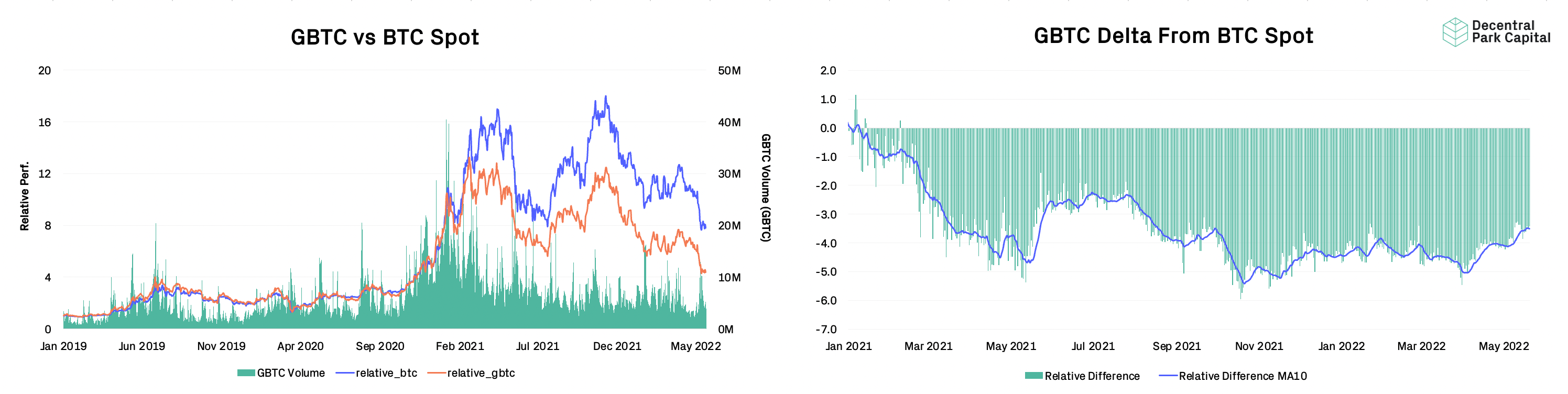

Grayscale Trusts

GBTC; GBTC discount widening to ATHs (-31%) and driven by wider spot action. GBTC secondary market volumes have stayed flat over the past week as investors take a sit and wait approach.

ETHE; Discount remains near ATH (33%) and also driven by wider spot action. ETHE secondary market volumes also kept flat over the past week.

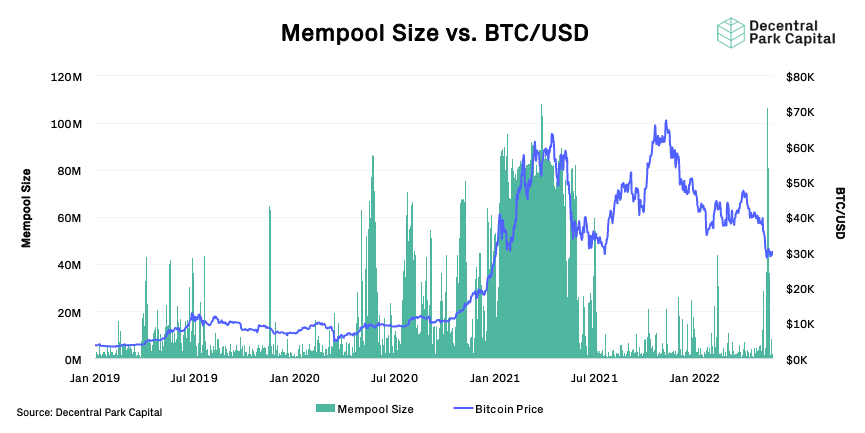

Size in MB; The mempool size for the Bitcoin network has fallen after spiking significantly as BTC holders start clogging up the network with de-risking transactions (including potentially adding to margin positions).

Bitcoin Hashrate

Bitcoin hashrate (7D) has fallen slightly over the past week (-4%) with mining keeping flat.

Volumes

On-chain real (BTC) & off-chain volume; On-chain volume has decreased 72% over the past week while off-chain volume for BTC and ETH has fallen 45% and 47% respectively.

Active User Base

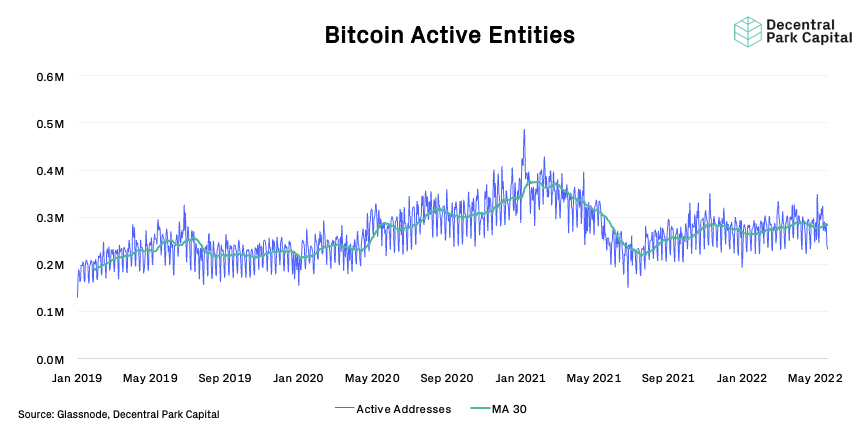

BTC; Wider market volatility has lead active entities (30d MA) has fallen 0.1% over the past week - no noticeable uptick in network usage.

BTC, ETH; Exchanges are seeing net inflows $560m for BTC while ETH is seeing $1B net outflow from exchanges on the 7D moving average (divergence). The pact of ETH’s net outflows from exchanges is also slowing down.

📚 Our Network #122 [Our Network]

📚. G2M in Web3 [Rebecca Dai]

📚 Fiscal Tightening [Joe Weisenthal]

📚 Coinbase Integrations [Jesse Pollak]

📚. The Fuel For Fast Execution [The Weekly Depths]

🎙️ Bridgewater’s Greg Jensen on Why Markets Have Further To Fall [Odd Lots]

🎙️ The FTX Podcast - Wintermute Trading [The FTX Podcast]

🎙️ Ric Edelman On The Truth About Crypto [On The Brink]

🎙️ Revenge Of The Dollar [Hidden Forces]

🎙️ Institutional Adoption Of Crypto [Real Vision Crypto]

Decentral Park is hiring! Please reach out to hr@decentralpark.io with your CV if you wish to apply for the following positions:

Decentral Park is an equal opportunity employer.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.