The Fallout

Crypto markets saw another negative week (-14.1%) as the fallout of the Terra unwind and macro environment continued to weigh on traders.

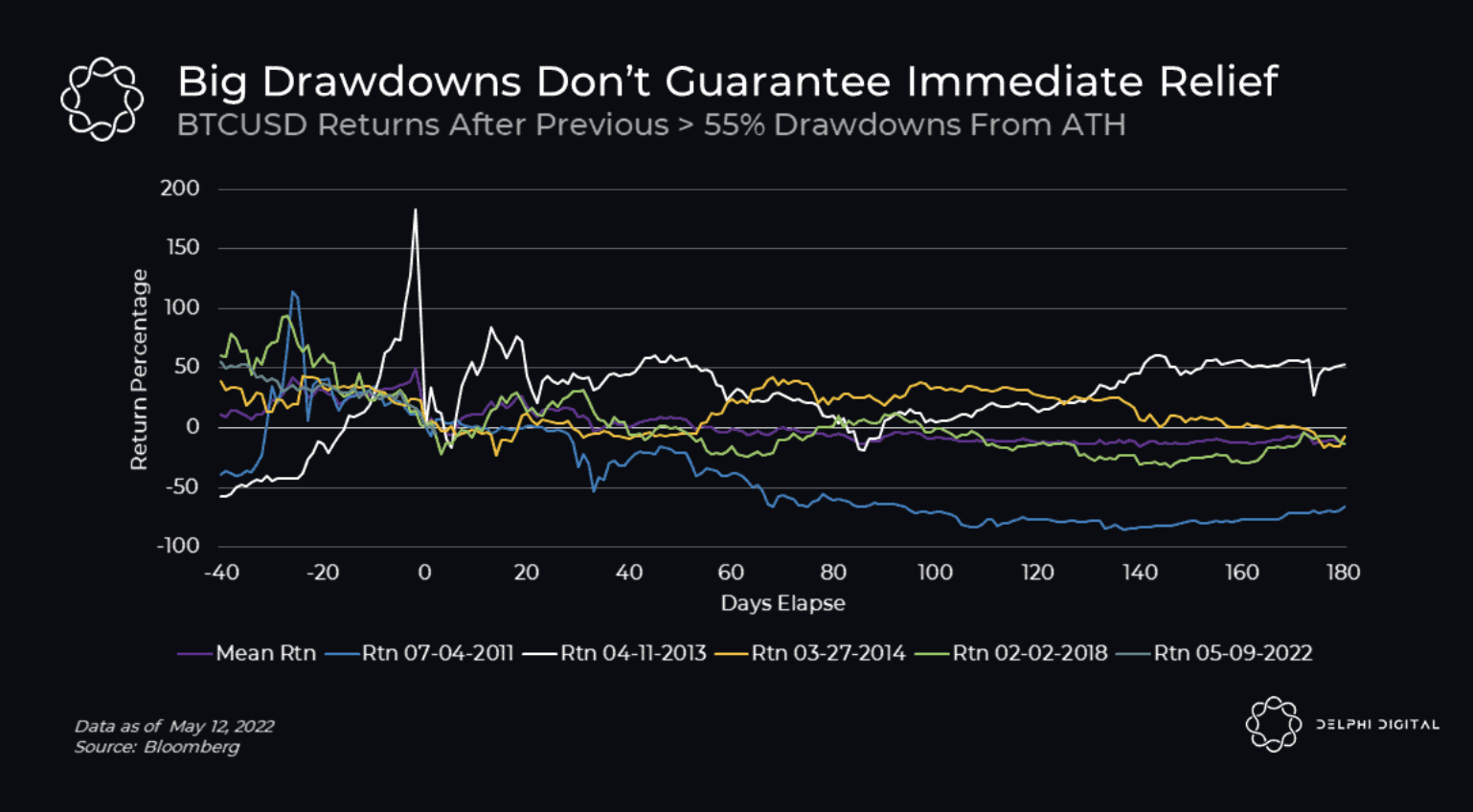

The extent of the drawdowns since April (-50%) are material but also not out of the ordinary. We saw the exact same drawdown from November’s 2021 peak to January 2022.

That said, both cases are lower than the May-June 2021 retrace (-56%) and demonstrates history can rhyme but not necessarily repeat 1-1.

BTC had its 7th negative week in a row with a ‘recovery week’ appearing to be overdue. Bitcoin’s daily RSI is low but not severely oversold, signalling this recovery week may not necessarily come just yet.

{kind=link}

Since the 12th May, long and shorts have been battling out around the $30k zone. Friday and Sunday showed hints of bull strength, taking BTC over the key psychological line. Note this strength was not enough to take the asset to the previous resistance of ~$32k on the 10th May.

The futures market shows that speculation remains elevated. BTC-denominated open interest for Bitcoin is at 410k - a little below the ATH level of 421k.

Such elevated levels often coincide with highly volatile periods start of April when BTC fell from $46k to $40k. Liquidations on both sides adding volatility remains a a real possibility. With funding rates now moderately positive, the risk is arguably skewed towards the bulls.

Looking Ahead For The Week

There is little to suggest that crypto won’t move in lockstep with equities, in particular growth stocks.

After Friday’s relief rallies over in the equity markets, NASDAQ futures are opening the week down 0.4% while SPX futures are also down 0.18%. Further tightening conditions and any equity rallies near-term are likely to weaken.

Powell indicated last week that the ability to create a ‘soft landing’ is out of the central bank’s control. Investment banks are signalling the recession outcome is likely with equities not finding their bottom just yet. BofA Global Research highlighted:

“Fear & loathing suggest stocks prone to imminent bear market rally but we do not think ultimate lows have been reached,” they wrote.

To add fuel to the fire, strong dollar is still hurting global growth by driving up borrowing costs. This is all before the Fed starts pulling liquidity in June by reducing its $8.9T balance sheet.

This week, the key factor to follow on the US side will be April US retail sales which will be released on Tuesday. Analyst expectations are a 0.7% MoM increases, higher than the prior print of 0.5%. A stronger-than-expected figure may be the positive news print traders will be looking for an otherwise bleak outlook. After all, the Fed could announce two more bumper rate hikes in the next two meetings.

We can look within crypto for catalysts too.

One of the key concerns by investors was the remaining BTC balance of the Luna Foundation Guard (LFG) putting continued price pressure on the spot market.

LFG once had 80k+ BTC reserves but, as of today, the LFG now holds just 313 BTC (~$9m). These disclosures may remove any fears by investors but the macro landscape will likely continue to be the key driver for cryptoasset prices.

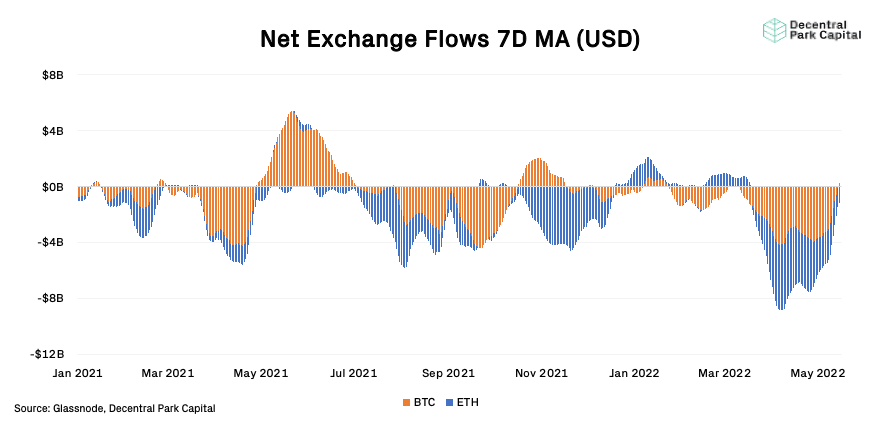

While LFG selling may not be a cause for concern, net inflows to exchanges may be. More BTC is being deposited to exchanges withdrawn in aggregate and is an infrequent but potentially important signal to consider. Sustained net inflows often coincide with market tops or prolonged periods of price action.

DeFi

In the aftermath of the great Terra unwind, several indicators point to changes in how DeFi is used:

Indicator

DeFi TVL fell 46% from early May vs. Global MCAP which only fell 26%

Why important

Indicates more capital has flowed out of DeFi since the Terra unwind as traders reset their positioning

Indicator

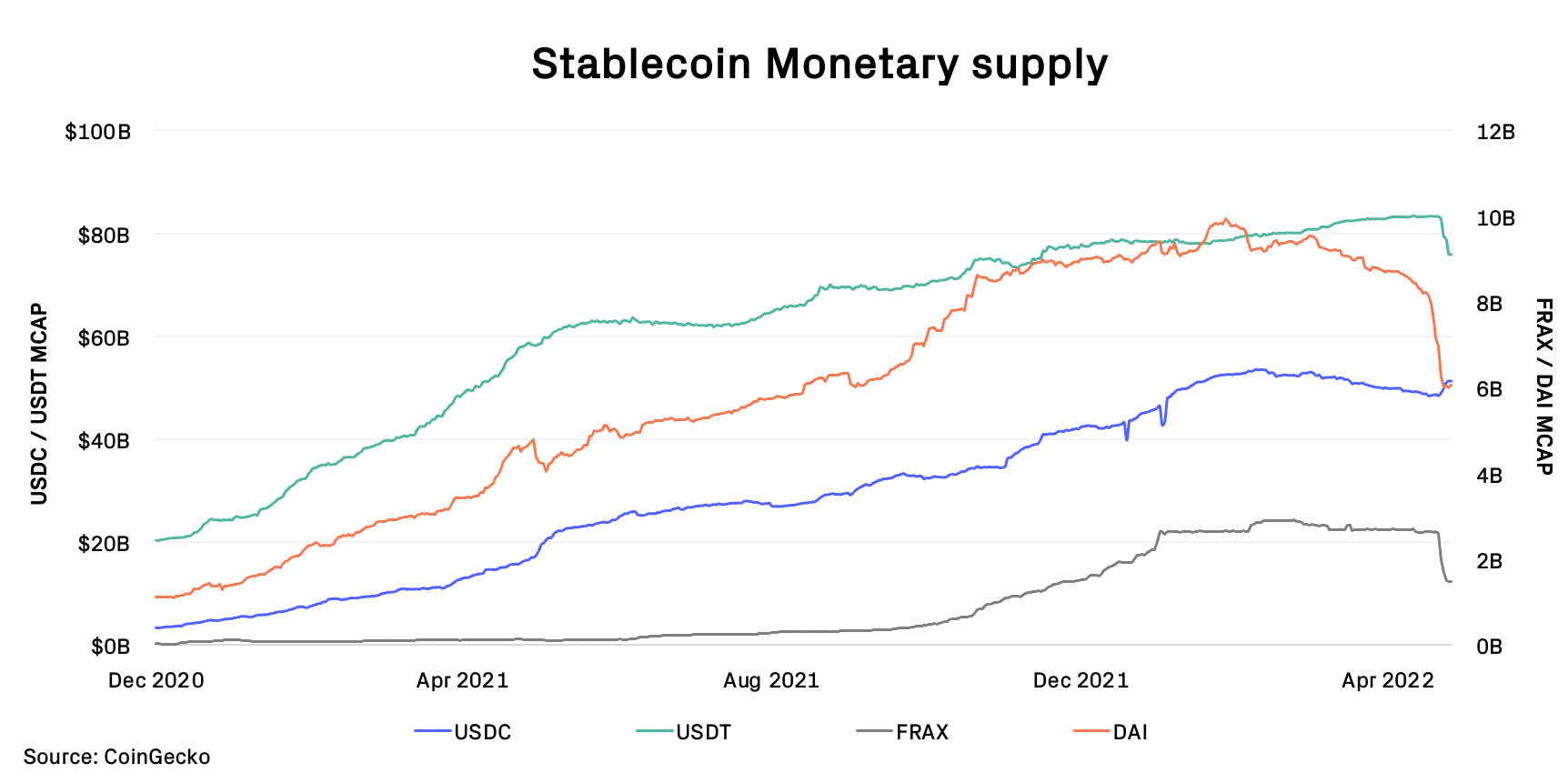

USDC monetary supply has increased by $3B (+6%) since 11th May

USDT, FRAX, DAI have seen their monetary supply fall over the same period

Why important

Algo stablecoins like FXS have underperformed the wider market by 27% on Saturday - algo stablecoin governance assets are at risk

Indicates that partially-algorithmic stablecoins like Frax are challenged by the current market’s sentiment around those algo designs. Fall in collateralized/over collateralized stablecoin supply (USDT and DAI) indicated greater deemed security in USDC than those alternative and/or users de-leveraging their vault positions.

In April, Circle received funding from BlackRock and Fidelity leading to potential capital market collaborations in the future.

So where to we stand?

An overall fickle market with long/shorts battling out around key levels to guide for near-term price action. The convincing support or loss of $30k BTC remains a good barometer for overall direction of the cryptoasset markets.

We are seeing a somewhat deflated DeFi sector in the LUNA/UST aftermath as traders look to de-risk their positions. If we are on a narrow path for avoiding a recession before the Fed starts reducing its balance sheet, it seems we are far from being out of the woods yet on a near-term basis.

Nexus Mutual

Recent volatility and growing changing sentiment around on-chain security, Nexus Mutual has seen ~40k ETH in net new active cover with total cover amount now hitting 179k ETH.

While positive for the network, Nexus’ MCR% remains below 100% meaning wNXM arbitrageurs are still unable to realize profit via the NXM bonding curve. wNXM trades at a an ATH discount of 72%.

MakerDAO

MakerDAO is entering a more challenging period. DAI supply has fallen 21% MTD (-2.4B) as user vaults are closed. Users closing their vaults has meant annualized network profit has fallen from $76m to $57m, increasing the time to fill the system surplus of 250m DAI.

The system surplus is filled by protocol earnings and MKR burning can only resume once the surplus is reached - in an estimated 778 days.

Few names printing green for the week in what is challenging market for cryptoassets. Maker being bid up as a sentiment play vs. UST but this rally was brief.

Top 100 (7d %):

Maker (+28.5%)

Chain (+5%)

Zcash (+-6.9%)

LEO Token (-7.2%)

FRX Token (-7.6%)

DeFi (7d %):

Reflexer Ungovernance Token (+52.7%)

Maker (+28.5%)

Olympus (+2.3%)

DFI.money (+1.1%)

Liquity (+1%)

Lido launched another Curve pool for stETH. New stETH / wETH pool has higher A coefficient for more concentrated liquidity and has base APR of 4% + 14.5% in LDO rewards.

Convex added support for selected Frax liquidity pools including voFRAX (10% APR), aFRAX (15%) and FPI/FRAX (13%).

Aave snapshot vote to add sUSD as collateral on Optimism passed successfully. Currently users can supply / borrow sUSD for 1.5% / 3.1% respectively.

As Gearbox is preparing to launch v2, the protocol increased credit account limit to $400,000 with 4x max leverage and introduced secret rewards for v1 users that may include early access to v2, GEAR airdrop and a spot in the pre-liquidity event.

Theme 1 - This week’s Terra/UST meltdown may just be the natural disaster event and flooring exercise needed to force regulation and open the institutional floodgate. Yes, a hybrid quasi asset backed and algorithmic stablecoin collapsed and eviscerated a large swatch of native crypto wealth concentrated during the last bull run.

The Week that Shook Crypto (FT)

Yellen: UST Collapse Could Have Been Avoided With Rules for Stablecoin Issuers (Blockworks)

Theme 2 - Crypto is officially institutional. S&P slapped a rating (any rating, who cares that its junk!) on Compound in a monumental step towards meeting institutional TradFi where it stands.

In Industry First, S&P Gives Compound Prime Junk Credit Rating (Blockworks)

D-ETF Secures $50 Million Prior to Public Sale (Blockworks)

Theme 3 - Grayscale’s GBTC is bleeding out as the discount expands, but may be the great catalyst in forcing a BTC ETF spot conversion in an effort to unlock investors after a ‘productive’ meeting with the SEC.

GBTC Discount Hits All-Time Low as SEC Mulls Bitcoin ETF (Decrypt)

Grayscale Had ‘Productive’ Meeting With SEC on Bitcoin ETF Conversion (CoinDesk)

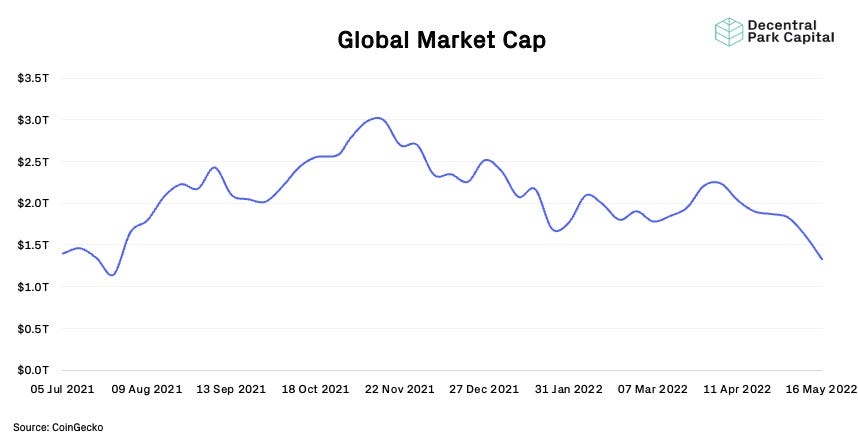

Global Market Cap

$1.34T; Global market cap has fallen by 18% as traders de-risk from positions further.

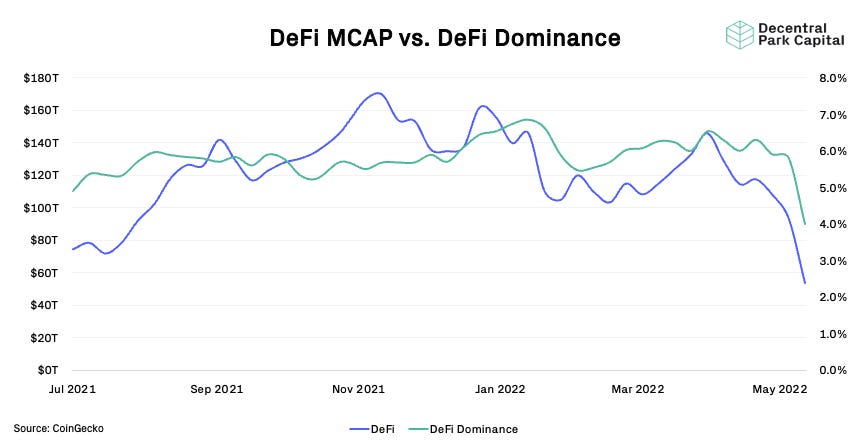

DeFi MCAP And Dominance

$53B; DeFi market cap has fallen 43% - more than global MCAP over the past week. Key driver has been the fall in LUNA market value and stablecoin supply of UST. DeFi dominance has fallen to annual lows (4%).

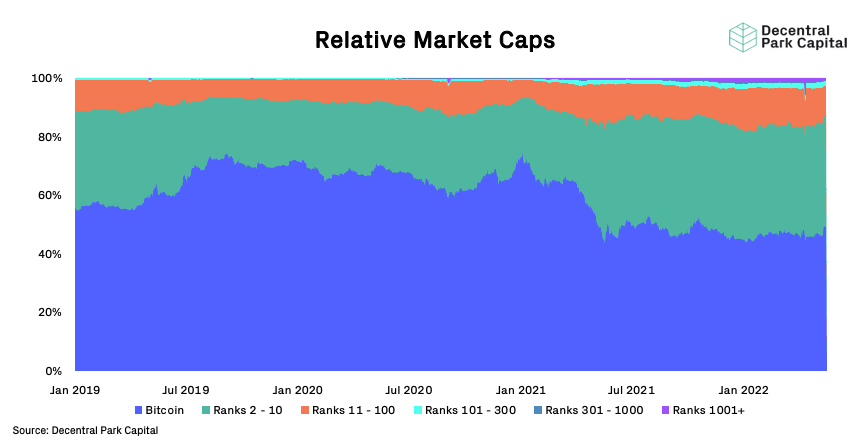

Relative Market Caps

Bitcoin dominance increasing by 200 BPS (~49%). Bitcoin increasing relative value against most cryptoassets during drawdowns (nothing too surprising here).

BTC/USD and ETH/USD

BTC/USD failing to break above $30k with limited buying if below $30k. ETH/USD facing resistance at $1.15k with $2k support looking to be tested this week. Daily RSI oversold.

ETH/BTC

ETH/BTC consolidating around 0.0681 as both assets test key levels on their USD ratios. Direction of ETH/BTC will be dependent on overall market (ETH underperformance against weakness and outperformance against strength).

Realized Volatility

BTC & ETH; BTC and ETH 30D vol has flattened over the past few days. 30D implied vol spiked on 12th May but has fallen 20%.

Trader Positioning

Moderately positive funding rate for BTC and ETH indicated traders remain predominantly bullish. Open interest for both markets remain elevated (420k BTC, 3m ETH) with risk of liquidations on both sides remaining a possibility against an increasingly soft market. Increased number of puts to calls within the BTC options market.

Combined Order Books

Order books look fairly even. Slightly heavier resistance up to $30.39k. (Source: Bitcoinity).

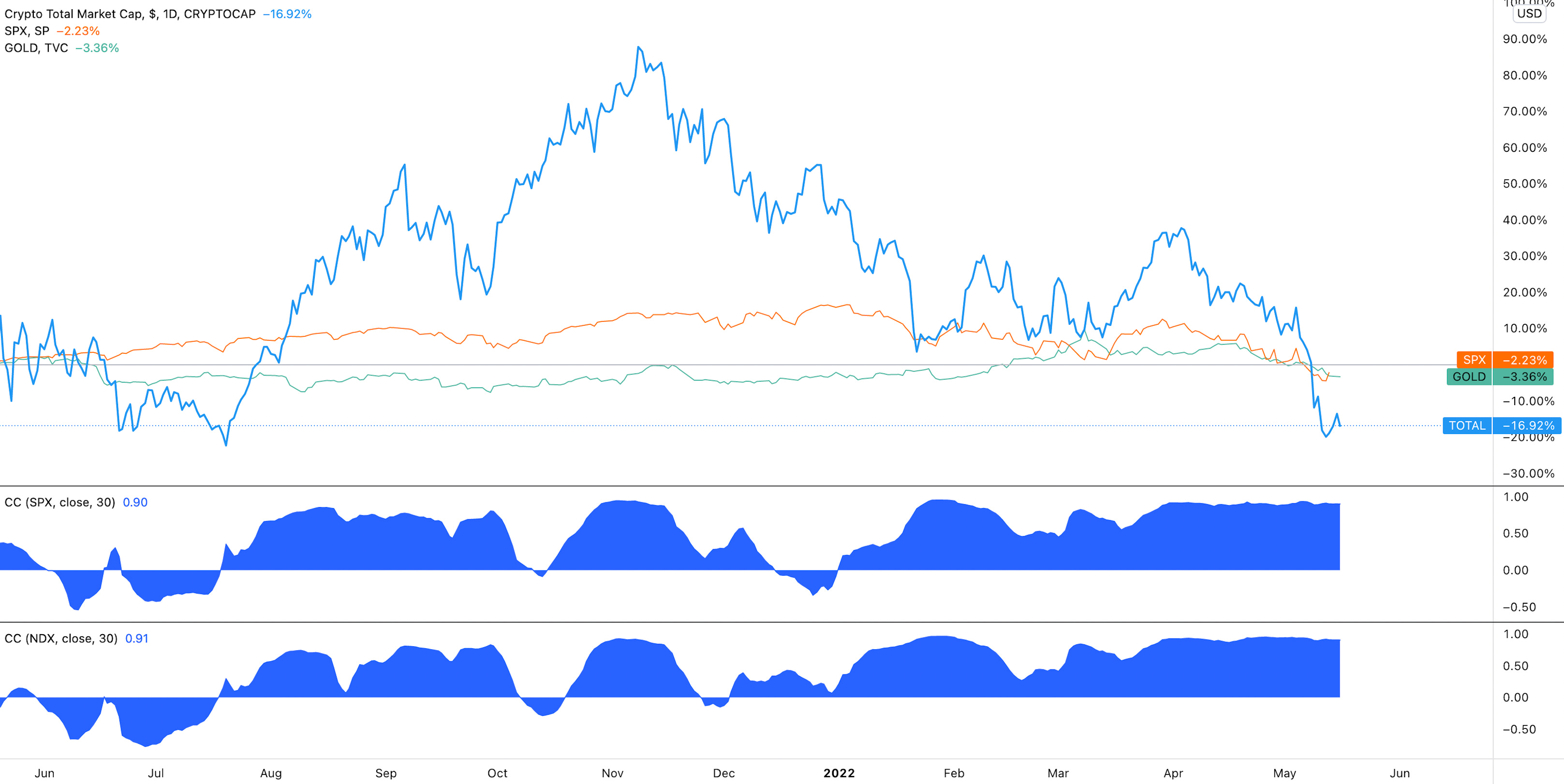

Crypto Correlations

Crypto vs. Equities vs. Gold vs DXY; Cryptoassets maintaining a very strong positive relationship to equity indices (0.91+ 30D) indicating cryptoassets are being traded as value and growth stocks. Gold continuing to come under pressure from stronger dollar.

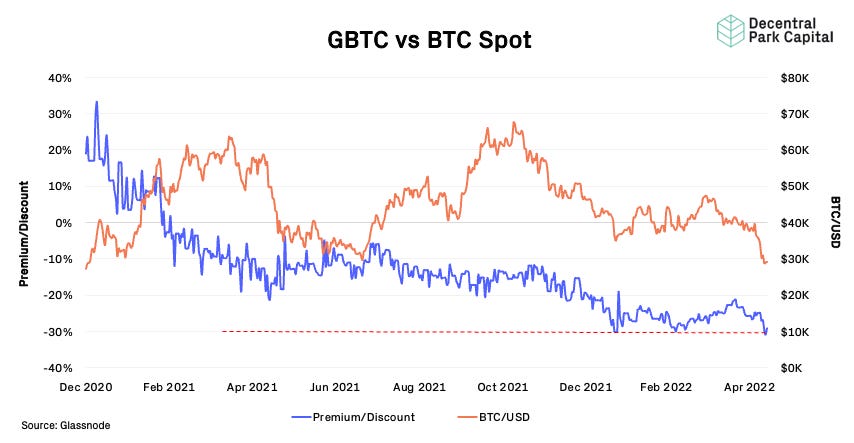

Grayscale Trusts

GBTC; GBTC discount widening to ATHs (-29%) and driven by wider spot action. GBTC secondary market volumes have increased 24% MTD.

ETHE; Discount widened to new ATH (-32.44%) and also driven by wider spot action. ETHE secondary market volumes have increased 16% MTD.

Bitcoin Mempool Activity

Size in MB; The mempool size for the Bitcoin network has spiked significantly as BTC holders start clogging up the network with de-risking transactions (including potentially adding to margin positions).

Bitcoin Hashrate

Bitcoin hashrate (7D) has kept relatively flat over the past week (-1%) with difficulty adjustment increasing 4.8% on the 11th May.

Volume

On-chain real (BTC) & off-chain volume; On-chain volume has increased 19% over the past week while off-chain volume for BTC and ETH has increased 93% and 44% respectively.

Active User Base

BTC; Wider market volatility has lead active entities (30d MA) has increased 2.5% over the past week.

Exchange Flows

BTC, ETH; Exchanges are seeing net inflows of BTC ($230m) and ETH ($10m) on the 7D moving average.

📚 This Week in Crypto - UST Depegging [Coinstack]

📚 Algo Stables In A Market Stress [Egirl Capital]

📚 Protracted Bear Markets [ianDAOs]

📚 Breaking Optimism [krzKaczor]

📚 Market Risks [Chris Burniske]

🎙️ Recession deep dive and VC psychology [All-in]

🎙️ The FTX Podcast - Jeremy Allaire (Circle) [The FTX Podcast]

🎙️ On The Third Era of Interoperability [On The Brink]

🎙️ How Should Washington Regulate Stablecoins? [The Breakdown]

🎙️ The Merge [Uncommon Core]

Decentral Park is hiring! Please reach out to hr@decentralpark.io with your CV if you wish to apply for the following positions:

Decentral Park is an equal opportunity employer.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.