The Weekly #195

The Grind Lower

Crypto faced another week of red with things looking less than rosy heading into late April.

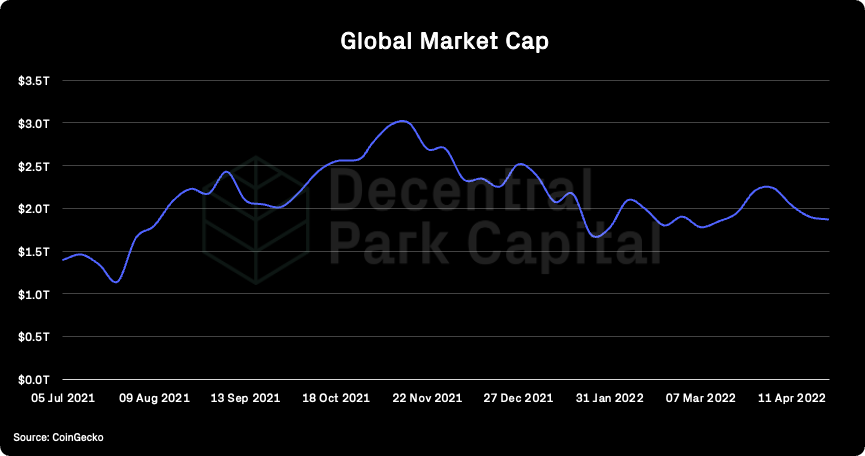

CoinGecko’s global market capitalization fell 1% over the past 7 days but with stronger weakness being seen in the last day (-4.2%).

Investors will be eyeing the $1.6T-$1.65T range seen in March for the next area of stabilisation.

Significant macro headwinds have continues to weigh in on a soft market. Spot volumes reached $16.6B last week - an ATL since December 2022 and down 30% MTD.

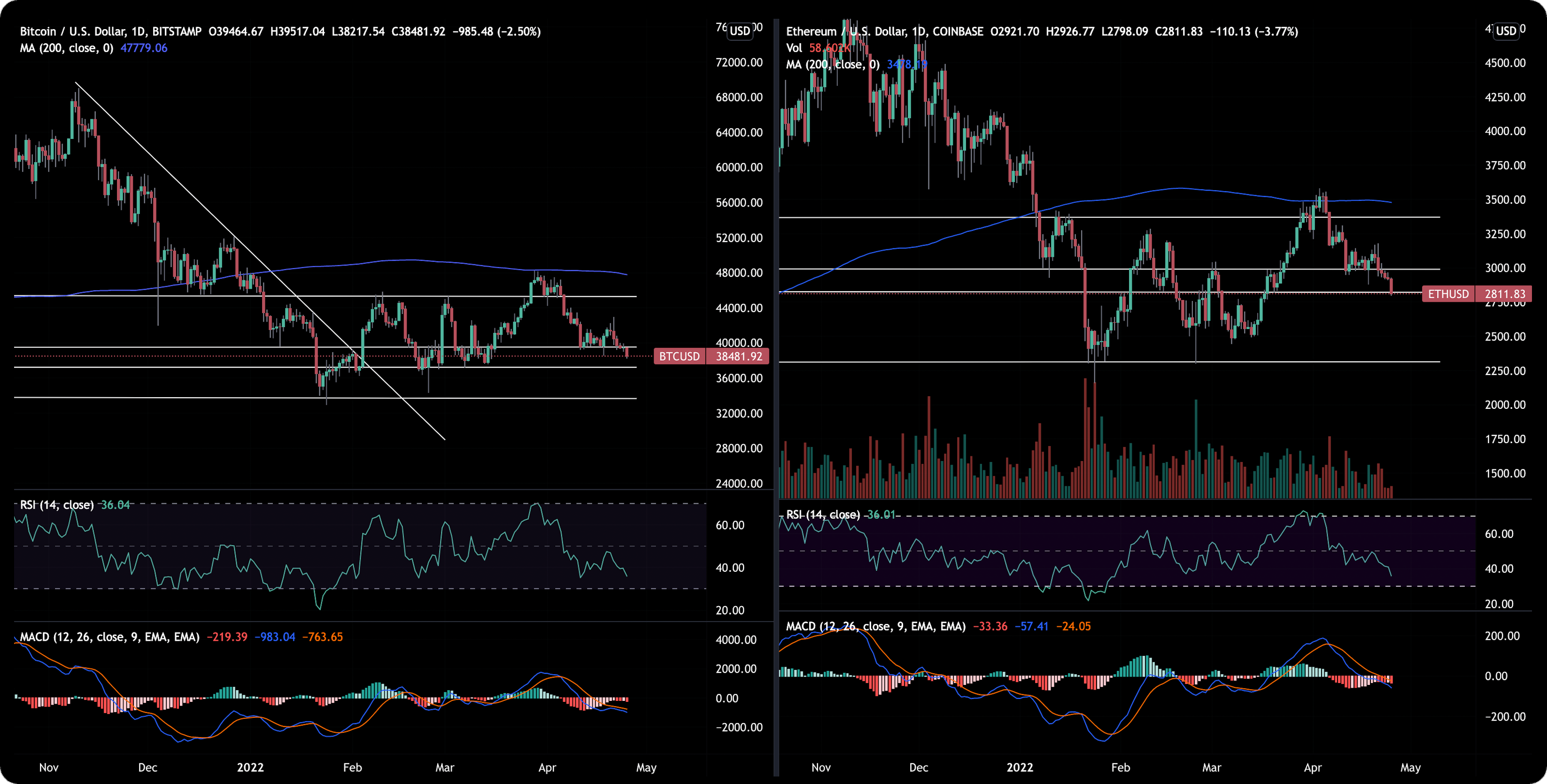

BTC/USD grinds lowers towards $37k potential support after breaking below $40k. Meanwhile ETH/USD looks set to break below $2.8k level.

We should expect markets to take a breather at some point with daily RSIs heading swiftly to oversold territory (<30).

The market is now pricing in ~270 BPS rate increases in the Fed funds futures for 2022. Deutsche Bank are expecting rates to reach 3% by March 2023.

Earnings week also provided a ‘mixed bag’ for stocks too. NFLX plunged over 35% over top line concerns while META may face similar treatment very soon.

Adding fuel to the fire, Chinese stocks, Yuan, and commodities have all plunged due to Covid cases spreading domestically in China. Concerns around economic and earnings growth outlook are clearly not just centred around the US.

Meanwhile, the US dollar has strengthened against currencies and commodities like Gold. There are now concerns of capital outflows from countries like China:

China/Japan = flat or lower treasury yields + loose monetary policy

US = higher treasury yields + tightening monetary policy

If dollar is the primary safe haven asset by investors globally, there are possible negative implications for crypto here:

DXY (dollar index) has often been negatively correlated with crypto over the last 10 years.

That said, one should always be cautious with using historical data as market structures now can be significantly different than in the past.

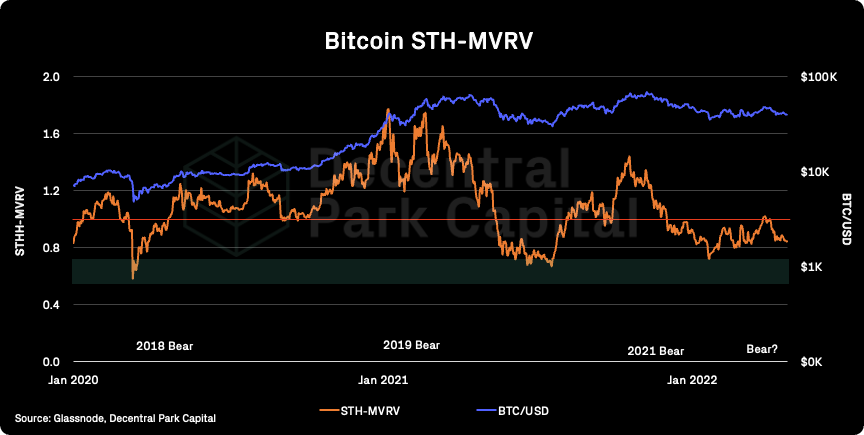

Global risk-off sentiment has already trickled into the crypto markets (Greed & Fear Index is near annual lows). One way to measure capitulation levels could be metrics such as STH-MVRV which continue to be useful to gauge short-term hold behaviour.

STH-MVRV in the 0.5-0.7 zone has been a reliable entry point signal. However, note these can be printed during prolonged bearish periods too (see 2022).

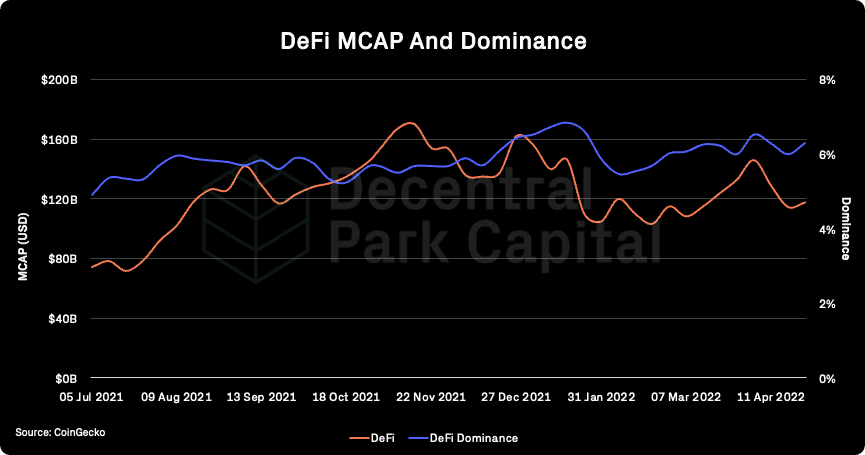

DeFi: A Tale Of Two Sides

The bear side: price

DeFi’s global market capitalization has now fallen 18% from its 2022 highs ($148B). Broad market sell offs has meant that DeFi assets (that are often further down the risk curve and more illiquid), are sold off harder than their higher cap counterparts.

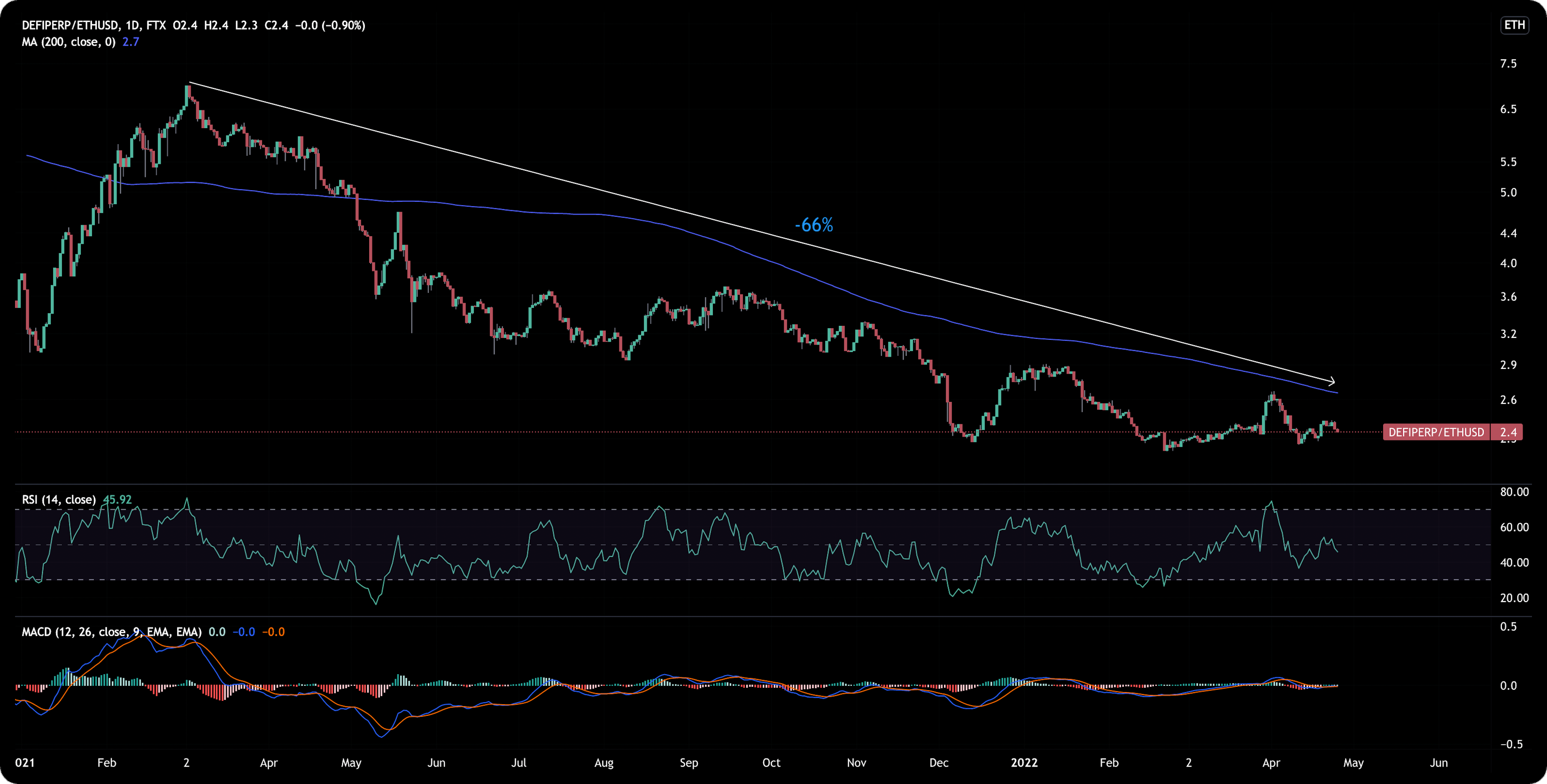

FTX’s DEFIPERP on its ETH ratio shows the extent of DeFi aggregate underperformance against beta.

DEFIPERP/ETH is hovering near ATLs, down 66% from its highs in March 2021.

Like STH-MVRV, capitulation levels (here RSIs) may inform entry levels but these can be printed during prolonged bear markets - as has been the case for DEFIPERP/ETH since March 2021.

The bull side: fundamentals

Price is useful but not the whole story. Peeling the layers of DeFi networks show continued growth across key sectors.

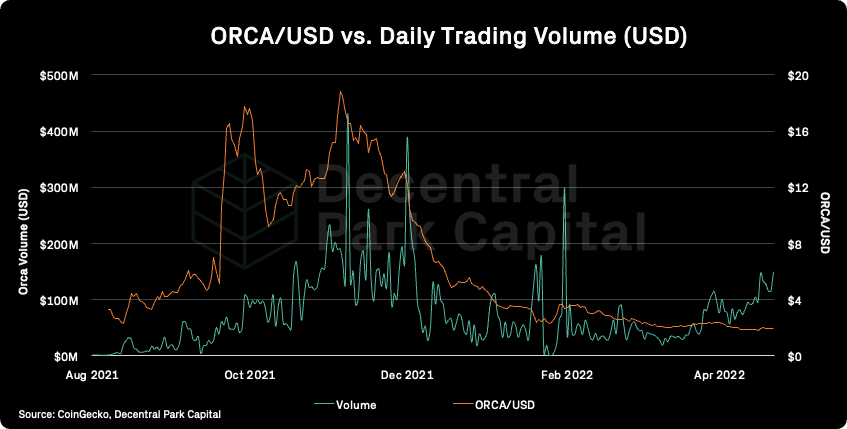

Exchanges: Orca

The Solana decentralized exchange is seeing trading volume surge to near annual highs ($200m) while its native cryptoasset moves in line with the broader market.

Liquid Staking Derivatives

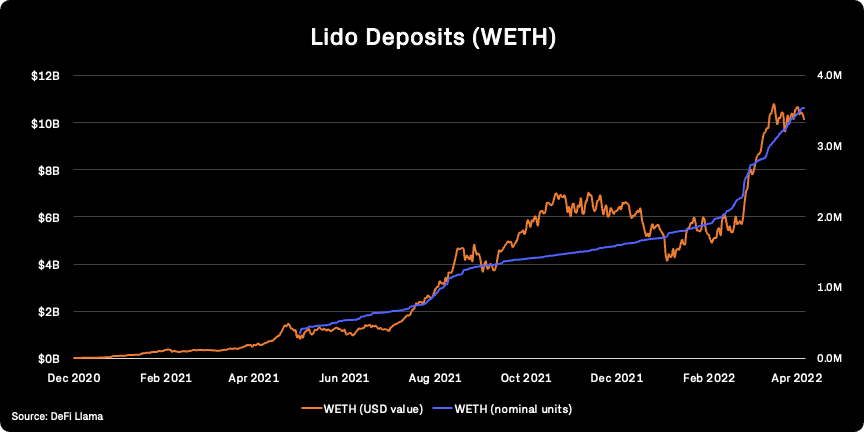

As we noted last week, Lido’s deposits in nominal units are increasing to new ATHs (3.54M WETH). Nominal units vs. TVLusd are starting to paint two different pictures.

Lido is also seeing increases for other chains like Polygon. TVL can be bolstered by a protocol’s vertical scaling strategy.

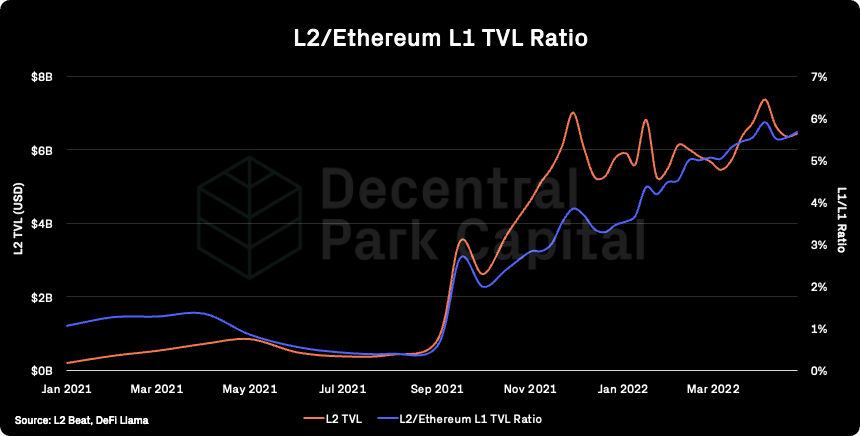

Layer 2s

TVL on L2s still stands above $6.4B today. While TVL has fallen 8% from its highs in 2022, growth in L2 ecosystems is continuing to outpace Ethereum’s L1. The L2/L1 TVL ratio is just below ATHs at 5.8%.

Growth here represents a burgeoning, scalable set of ecosystems for Ethereum users and developers which has yet to mature fully.

The price/fundamental connection

The key question for investors will how these fundamentals will be reflecting in market value. While macro headwinds fuel panic further in the market, these metrics are often lost on investors at large.

That said, they matter more on the rebound. Taking the case of Lido, growing unit count with price rallies leads to a reflexive outcome.

A rebound effect may also come at a time when institutionalization of crypto intensifies.

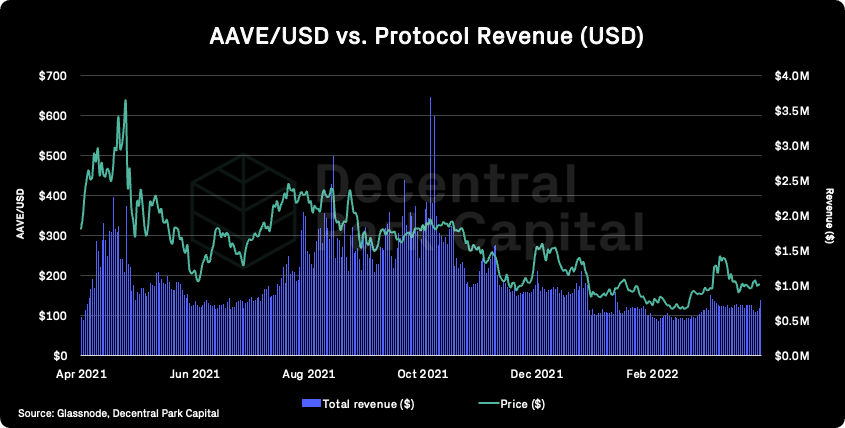

However, there is the issue of how price informs fundamentals too (not just the other way round).

So long as prices remain muted, financial-based metrics for DeFi protocols will also remain muted all else equal. You don’t have to look beyond Aave’s daily revenue vs. AAVE/USD to see this effect.

Therefore, while useful to highlight the fundamentals, for now investors may look to de-risk more broadly and it remains unclear how much emphasis will be placed on these indicators by investors as the global macro headwinds take shape.

Top performers over the past week have largely been mid-cap names including blue chip DeFi names. Few assets printing positive performance.

Top 100 (7d %):

ApeCoin (+48.2%)

STEPN (+30.6)

Terra (+14.8%)

Curve DAO Token (+14.8%)

Zcash (+7.9%)

DeFi (7d %):

Kava (+24.2%)

Kyber Network Crystal (+21.0%)

Curve DAO Token (+14.8%)

0x (+9.4%)

Ampleforth (+7.5%)

Synthetix and Lyra are now incentivizing the sUSD gauge on Curve, veCRV holders can receive 12,000 SNX and 50,000 LYRA weekly for their votes

Synapse launched a new stablecoin pool that allows users to bridge USDC into and out of Optimism, 11% APY for LPs.

Curve 4pool backed by Terra and Frax is live on Fantom network, FXS and LUNA rewards TBA.

Stake DAO launched CRV liquid locker, which allows holders to earn yield on CRV without locking it. Current APR is 12%.

Theme 1: Blue chip crypto protocols are now playing ball with federal regulators as they move quickly to comply with traditional banking regulations and fit within regulatory guardrails.

BlockFi's Flori Marquez says the company is readying the first regulated crypto yield product in the US — and shares what the $10 billion crypto finance firm learned from working with the SEC (Business Insider)

Circle Will Apply for U.S. Crypto Bank Charter in ‘Near Future’ (Bloomberg)

Theme 2: New York becoming the sandbox for state mining legislation as state legislators target mining bans motivated by environmental concerns. The same concerns driving federal legislation and enforcement in the wake of the Russia/Ukraine conflict.

New York Is Battleground for Crypto Mining Fight (WSJ)

US House Democrats Call for Scrutiny on Crypto Mining as Environmental Threat (CoinDesk)

Theme 3: Regulatory parity continues to swing from alarming to supportive, from the EU to the Pacific, with recent hacks coming out of North Korea accelerating scrutiny.

EU Crypto Firms Protest ‘Alarming’ Anti-Money Laundering Laws (CoinDesk)

Crypto Thieves Get Bolder by the Heist, Stealing Record Amounts (WSJ)

Global market cap: $1.87T; Global market cap has fallen by 2%.

DeFi: $117B; DeFi market cap has increased 3%, more than global MCAP over the past week. DeFi dominance has increased 3% over the same period. DeFi has been buoyed by key names like Luna which are counted within the DeFi bucket.

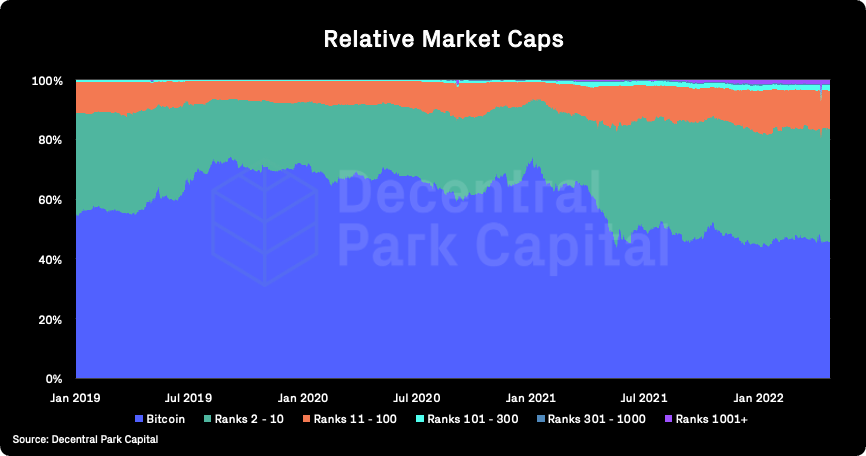

Market shares; Bitcoin dominance is holding relatively steady at ~47%. Bitcoin continues to show relatively lower downside volatility to other cryptoassets.

BTC/USD and ETH/USD

ETH/BTC

Price action; Weak price action on BTC/USD, ETH/USD, and ETH/BTC. BTC/USD finding initial support at $38.2k. BTC/USD and ETH/USD daily RSIs approaching oversold levels. ETH/BTC finding support on the 200d MA. ETH/BTC daily RSI more neutral (~50).

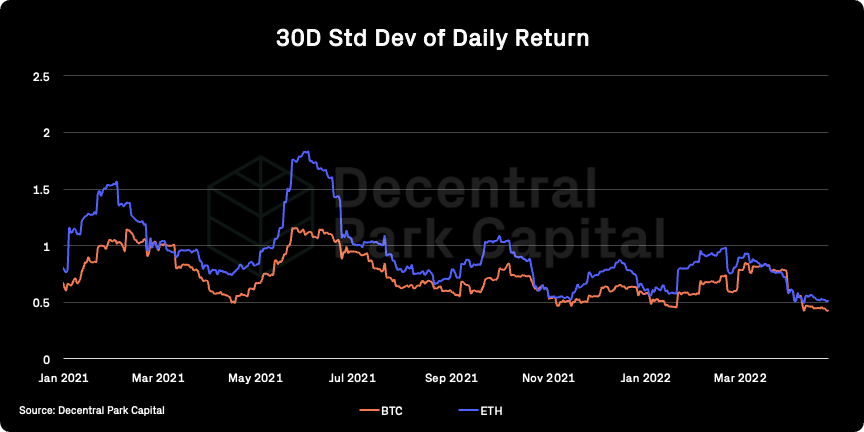

Volatility (BTC & ETH); BTC and ETH 30D vol kept flat at their annual lows. BTC and ETH ATM 1M implied vol at annual lows (59% and 62% respectively). The 3M and 6M gauges also continue to decline. Implied vol is undervalued compared to lifetime average with both calls and puts relatively cheap.

Combined order books; Order books much heavier on the bid side. Slightly heavier resistance between $39.3k (Source: Bitcoinity).

Crypto vs. SPX; Cryptoassets maintaining a strong positive relationship to equities. Correlations to NDX and SPX are keeping above 0.9. Dollar strength weighs in on Gold and currencies.

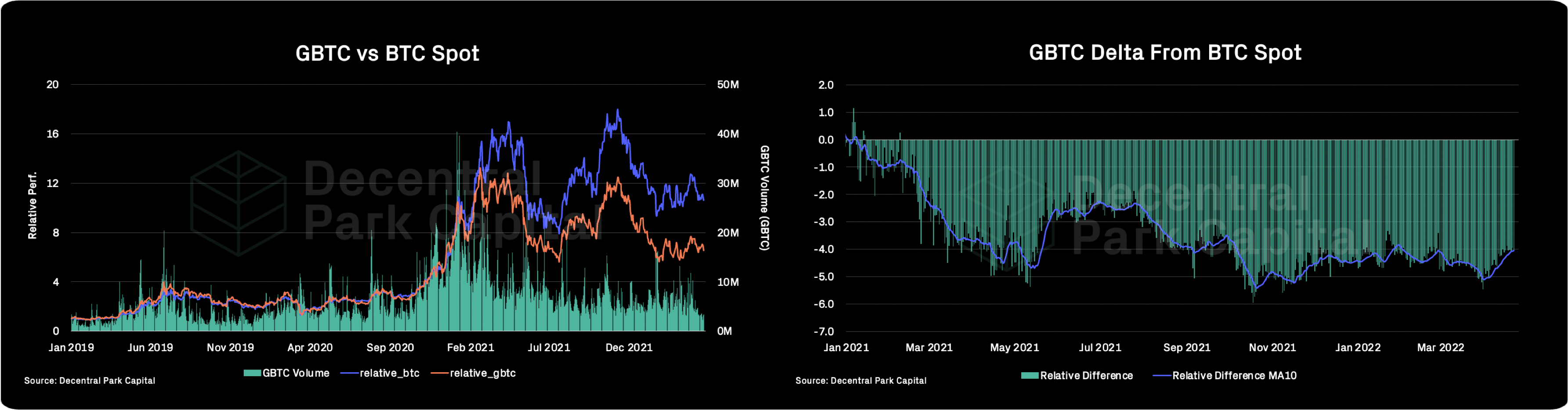

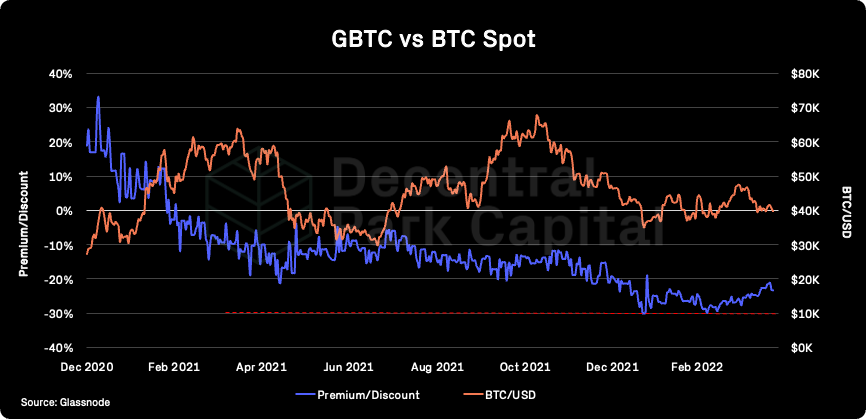

GBTC premium; GBTC discount continues to narrow over the past week over the past week (-23.29%). GBTC demand is softening however with 30D secondary market volumes falling 27% YTD.

Vanguard is to end support for GBTC and ETHE later this month. Grayscale pushes on to win over SEC support for a spot Bitcoin ETF.

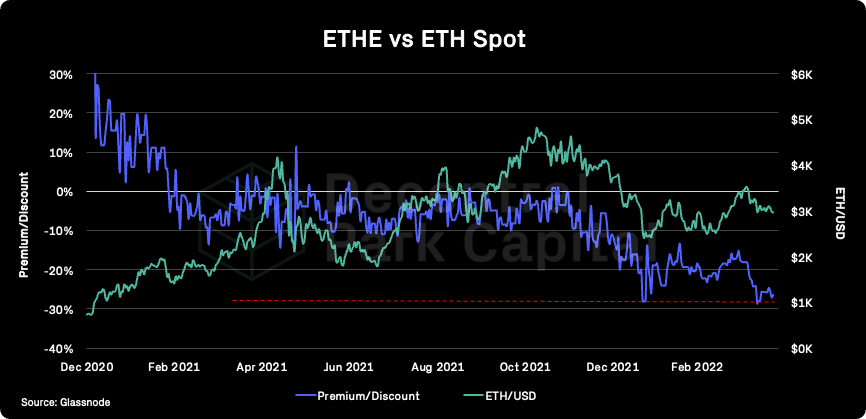

ETHE premium; ETHE discount still hovering around ATHs (26.42%). ETHE volumes (30D) are down 50% YTD indicating limited buy demand by investors including retail.

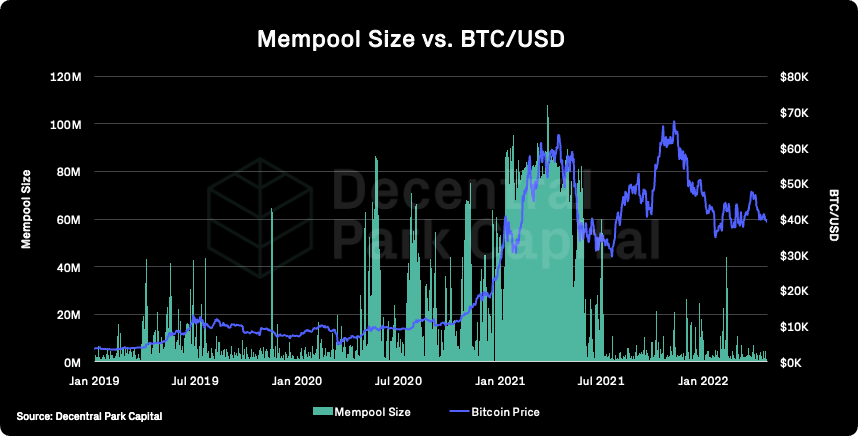

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has kept low indicating relatively low congestion on the network.

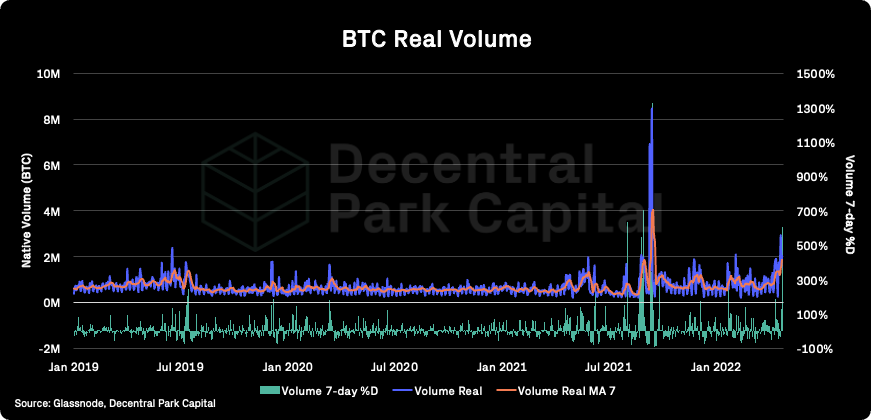

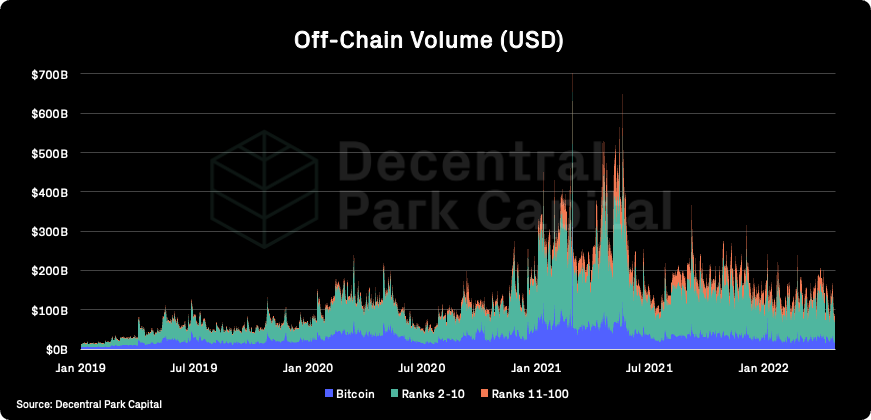

On-chain real (BTC) & off-chain volume; BTC on-chain volume has increased 40% for a second week running. Off-chain volumes increased ~10% over the past week for Bitcoin while flat for ETH.

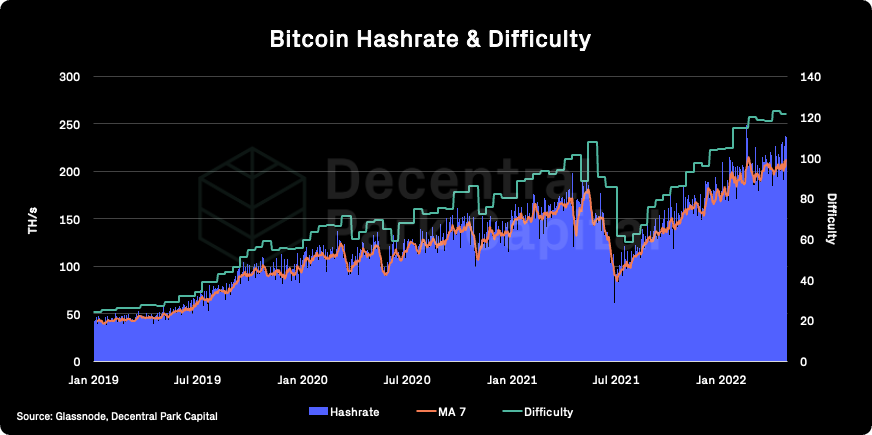

Hashrate & Difficulty; Bitcoin hashrate (7D) has increased 2% over the past week. Network difficulty expected to increase 4% in ~2 days time.

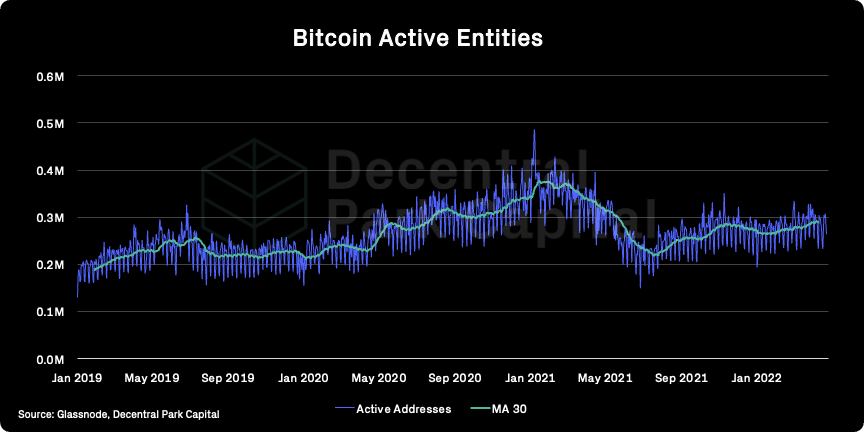

Active addresses (BTC); No significant changes in active entities over the past week (-0.57%).

Trader positioning; Good level of May and June option calls since Arthur Hayes’ blog post.

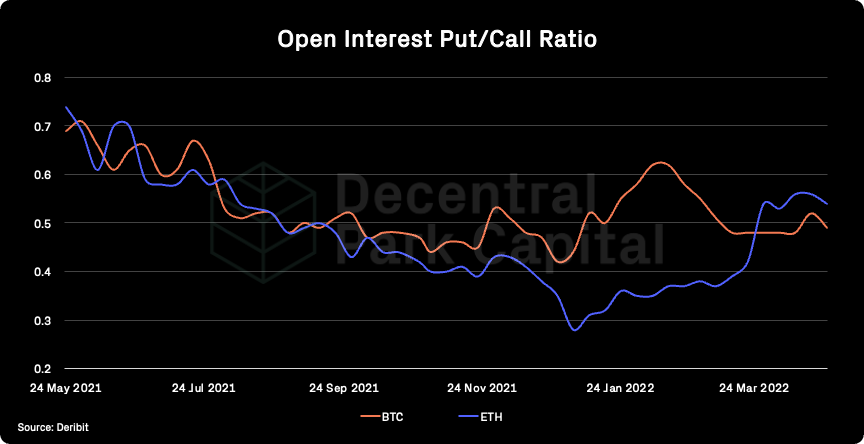

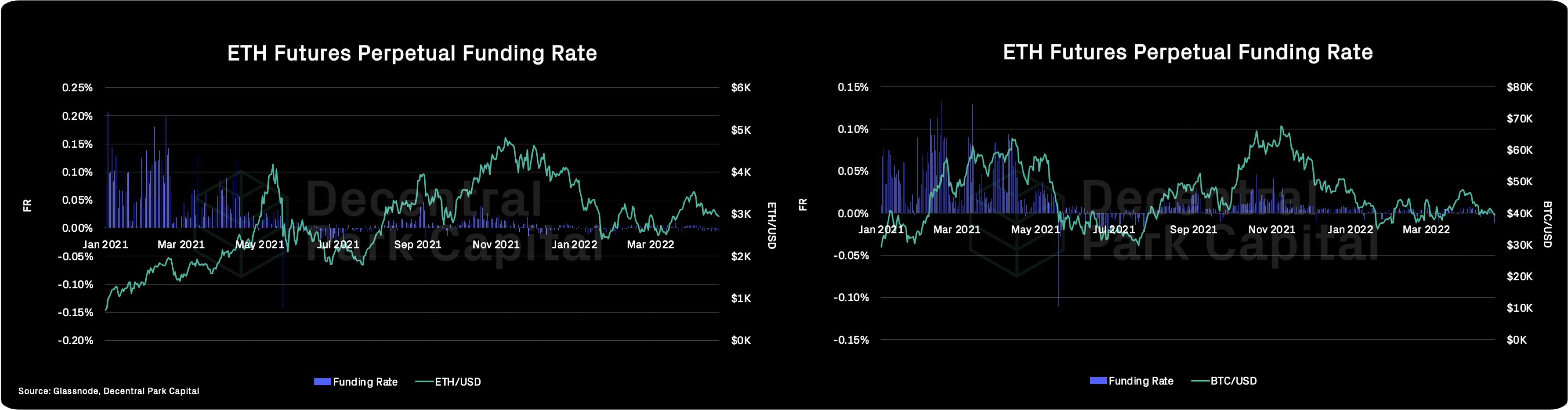

Put/call ratio stabilised after steady increase YTD for ETH. Moderate funding rates across the board indicates traders taking a predominantly bearish stance while growing OI indicates leverage is increasing.

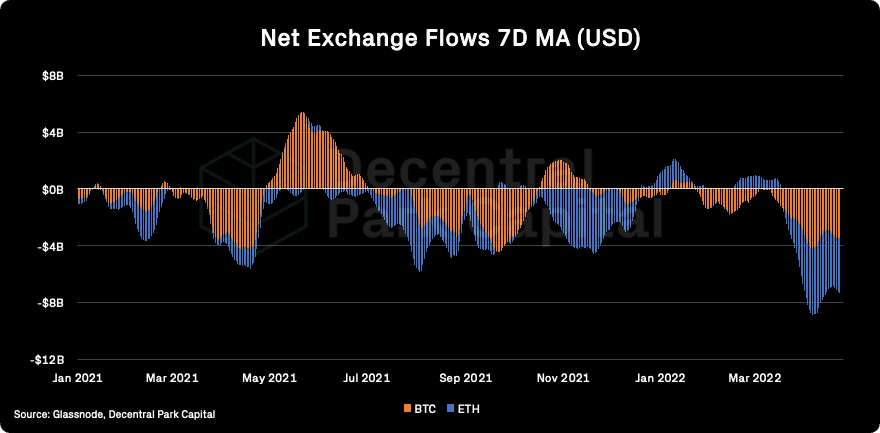

Exchange inflow/outflow (BTC, ETH); Strong net outflows for BTC and ETH from exchanges ($3.6B and $3.8B respectively). Note, net outflows from exchanges may be useful to gauge potential aggregate investor behaviour but has been a poor leading indicator for price.

📚 Solana’s congestion and its fix [@ResearchVariant]

📚 Buy and burn no more [@Volt Protocol]

📚 Q1 Avalanche Report [@Nansen]

📚 bSOL on Anchor [@LidoOnTerra]

📚 Morgan Stanley on Crypto Market Participation [@Coindesk]

🎙️ Tech work culture, crypto regulation [All-in]

🎙️ A roundup of policy discussion @ Miami Bitcoin 2022 [The Scoop]

🎙️ Bull Chase for ETH 2.0 Mege [Empire]

🎙️ Interoperability from Axelar [Zero Knowledge]

🎙️ The Stagflation Mega-Trade | Dan Morehead [Bankless]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.