The Weekly #192

Accumulation, DeFi outperformance, and evolving the Ethereum narrative in 2022.

Consolidation Post-Rally

The cryptoasset market had its best monthly performance in 2022 - printing a 25.1% gain. Markets have recovered convincingly from their early March lows 2022, now standing at a 28%+ gain from those levels today.

Momentum indicators on global MCAP suggest potential consolidation around the $2.1T mark including daily RSIs at 72.

After reaching highs of $48.2k, BTC has come off 4% and seems to have settled around the $46k mark with support found at $45.5k. Note, BTC has yet to cross back above its 200d MA which has been acting as resistance.

Cryptoasset performance has often moved in tandem with wider risk markets like equities where negative periods for SPX often coincides with negative periods for Bitcoin.

However, investors should continue to pay attention to dispersion within the cryptoasset market that may, by extension, lead to a potential divergence from broader risk-on trajectories at some point in the future.

Examples over the past week include DeFi protocols like Frax Share (+80.7%) and Lido Finance (+36%) and investors continue to be reminded how paying attention fundamentals can provide the upper hand.

Yield Inversions

However, investors should continue to pay attention to dispersion within the cryptoasset market that may, by extension, lead to a potential divergence from broader risk-on trajectories at some point in the future.

Examples over the past week include DeFi protocols like Frax Share (+80.7%) and Lido Finance (+36%) and investors continue to be reminded how paying attention fundamentals can provide the upper hand.

As Arca highlight in their recent blog post:

The easiest part of investing is finding a good idea. The hardest part of investing is finding the best pure play way to express that idea.

… In today’s market, simplistic "pure-play" thematic investing will likely help investors hone in on a specific outcome.

Yield Inversions

If equity markets do provide a ‘general pull’ for cryptoassets over the coming months, that ‘pull’ will likely be driven by investor predictions on recessions and more hawkish monetary policies by central banks.

The talk of the town has been the inversion of the yield curve - often referred to as the difference between the 10Y US treasury bill and the 2Y US treasury bill.

The inversion occurs when long-term rates drop below short-term rates because investors expect declines in short-term rates. In other words, there is growing speculation about slowing growth in the market.

The market often points to signalled accelerated rate hikes and nonfarm payroll data.

Liquidity in US Govt bonds has also dropped with the Fed ceasing the purchase of US Treasuries adding to the pressure.

But not everyone is buying the recession prediction fears. The Fed points to more reliable data like the 18M-3M spread which so far does not show any warning signs.

So where do we go from here and what does it all mean for crypto? Right now it’s far from clear.

Resilience in the equities markets against these growing macro concerns may highlight simple investor preference when faced with guaranteed negative real return on cash due to high inflation.

By extension, more speculative assets down the risk curve like cryptoassets can be buoyed by this dynamic. This is reinforced by regular, big-size fund raising within crypto (see Bain, Haun Ventures).

It’s also worth remembering, rising rates have often led to positive outcomes for risk assets.

Drawing On The Bullish Momentum

The recent rallies in both BTC and ETH appear to have been driven by spot demand with the ratio of futures/spot volumes falling since Feb highs.

More often than not, every sustained rally is led by the spot market over futures.

We can also look to on-chain indicators that signal potential market reversals. Bitcoin’s STH-MVRV (ratio of MCAP and realized cap for short-term holders) was kept below 1 throughout 2022 implying a large part of the market is nearly breaking even or dipping into losses.

STH-MVRV briefly moved back above 1 - an apparent resistance line during prolonged bear markets as investors look to pull out of the market around breakeven.

STH-MVRV using 1 as new support would add weight to a sustained bull market for the asset as has been the case historically.

Ethereum Momentum

For now though, all eyes have been on Ethereum which has outperformed BTC by 7.3% over the past week.

The move was convincing. ETH/BTC broke cleanly above its 200d MA reaching a new high since mid-January 2022 (0.0756).

Over the past week, FTX’s DEFIPERP outperformed ETH/USD by 11% while aggregate DeFi MCAP growth outpaced ETH MCAP by 5%.

What’s good for ETH is good for DeFi and the capital flow down the risk curve from beta remains a real possibility over the coming weeks and months.

The source of momentum for Ethereum (like any other cryptoasset) is never unchanging. As predicted, we are seeing the merge headlines come through in numbers but several potential momentum drivers have yet to play out.

Possible future momentum drivers:

ESG/PoS

EU’s MiCA Bill illustrated how PoW networks continue to be at risk from a regulatory perspective. Bitcoin’s large energy footprint has been a sticking point for EU regulators within the MiCA.

Ethereum avoids this altogether with the possibility of an endorsement by EU critics relative to the orange coin

L2 Services/Integrations

NFT infrastructure becoming L2 native (see Temasek Immutable raise, Gamestop NFT marketplace on Loopring).

Launch (and decentralization) of flagship zk-Rollup solutions (see Starknet, ZKSync) and L2 aggregators (see Polygon)

Release of quantum gravity bridge means new types of rollups (see Celo) could settle back to Ethereum.

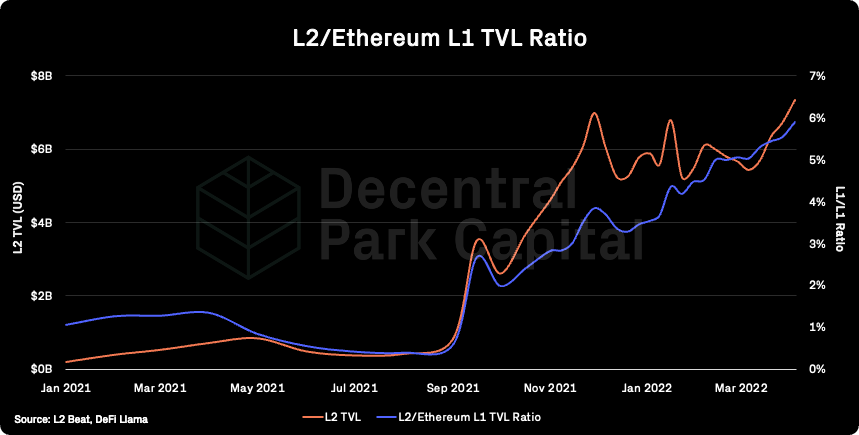

For L2s, the momentum is picking with L2/L1 TVL now reaching 6%. We are still early with L2s in aggregate contributing only 0.7%-1% of total fees for Ethereum.

Looking even further ahead, rollups will likely be labelled as a generalizable technology used by both alternative EVM and non-EVM ecosystems. For example, large validators and subnet architecture for Avalanche could be a conducive platform for rollups.

FRAX Share

FXS has been a top performer within crypto over the past week (+81.9%). A key catalyst includes Frax Finance’s collaboration with Terra for their FRAX-UST-USDC-USDT 4Pool.

FRAX will be using UST as collateral within 4Pool where UST is backed by ~$1.8B of BTC (with target of $10B). FXS FDV is back above FRAX’s monetary supply value with the two appearing to be cointegrated.

See Decentral Park’s Research Frax Finance Valuations here.

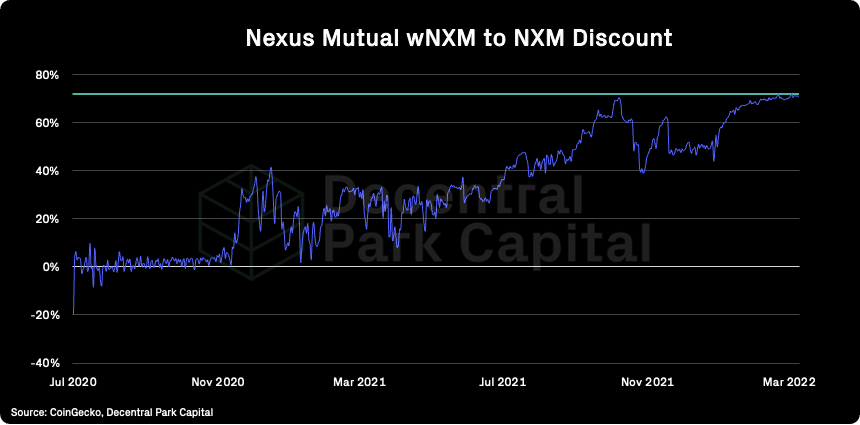

Nexus Mutual

Nexus Mutual’s active cover has fallen 33% in USD terms and 29% in ETH terms. Approximately 33% of the capital pool’s active cover will expire within the next month.

Low demand for risk cover has ensured MCR% is kept below 100% (currently 95%). Unable to realize profits from arbitraging with Nexus Mutual’s bonding curve, the wNXM/NXM discount has climbed to new ATHs (71%).

Top performing assets have been largely driven by headline catalysts (e.g. SKALE v2.0, Frax 4Pool)

Top 100 (7d %):

Moonbeam (+104.3%)

Frax Share (+81.9%)

Skale (+53.2%)

Zilliqa (+50.5%)

Aave (+40.8%)

DeFi (7d %):

Frax Share (+81.9%)

Aave (+40.8%)

JOE (+33%)

Spell Token (31.5%)

Synthetix Network Token (31.2%)

DeFi platforms have deployed to veJOE Boosted Farms. Yak will contriubte 350k JOE to be converted to $yyJOE to further boost rewards.

Anchor’s $UST rate will change from static 20% APY target to a dynamically adjusted target - rates increase by 1.5% if yield reserves increase and fall 1.5% if reserves fall by 5%. APY is forecast to be cut 1st May.

The new 4Pool will receive $3.8m CX to incentivize new liquidity where 35-70% of FXS circulating supply could be bought back via the proposed pool design.

EU lawmakers vote to extend additional AML provisions to crypto and outlaw anonymous wallet transactions, extending the Travel Rule, and effectively ending anonymity across crypto (in Europe).

EU Parliament Passes Privacy-Busting Crypto Rules Despite Industry Criticism (CoinDesk)

European Union Proposes Crackdown on Non-Custodial Crypto Wallets (Decrypt)

SEC quietly proposes a 200+ page proposal that extends the definition of regulated “dealers” to include passive market makers and liquidity providers, broadly seen as a direct attack on decentralized finance without explicitly referencing it.

How the SEC Proposal to Change One Definition Could 'Kill' DeFi(Decrypt)

Jake Chervinsky: “The SEC just proposed a rule that would expand the definition of regulated "dealers" to include people who "employ passive market making strategies" that have "the effect of providing liquidity" to others.”

Gabriel Shapiro: “it's an all-out shadow attack on decentralized finance”

Global market cap: $2.24T; Global market cap has increased by 1% as the market consolidates after breakout.

DeFi: $146B; DeFi market cap has increased 10%, more than global MCAP. DeFi dominance has increased by 9% - the largest WoW increase since July 2021.

Market shares; Bitcoin dominance has fallen to 45.58% with several large caps names outperforming the orange coin over the past week.

BTC/USD and ETH/USD

ETH/BTC

Price action; BTC/USD consolidating at support lines held during December 2021 ($45.5k-$46k) with 200d MA acting as resistance. ETH/BTC climbed above 200d MA and cooling off from 74 daily RSI. Relatively higher volume supporting price rallies.

Volatility (BTC & ETH); BTC 30D vol have both fallen over the past week. BTC ATM 1M implied vol near 3M low (56.9%) while ETHa at 3M low (64.7%).

Combined order books; Order books appear heavier on the bid side. Slightly heavier resistance between $47.5k-$48k (Source: Bitcoinity).

Crypto vs. SPX; Cryptoassets remain positively correlated to equities (0.93 30D Rolling). Equities remain a core choice for investors seeking a return against negative real rates and inflation. Equity markets buoyed in March by seeing large investors shifting ~$230B from bonds.

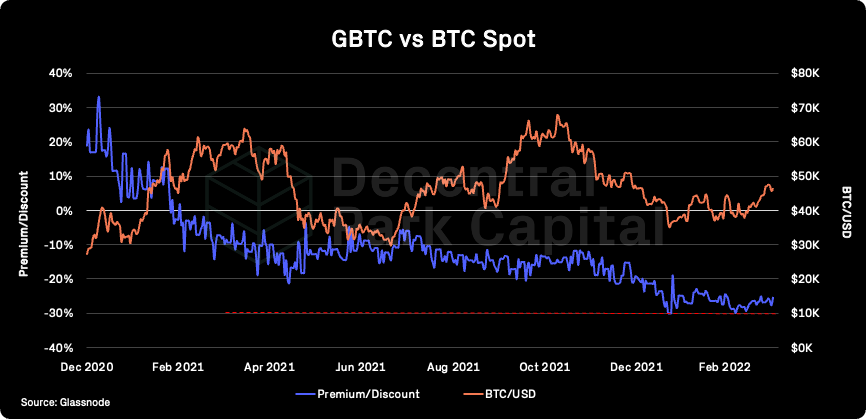

GBTC premium; GBTC discount has fallen from 26.22% to 25.45% slightly benefiting from BTC’s spot performance. Grayscale have indicated they would consider a lawsuit against the SEC if the conversion of their $30B+ GBTC trust into a spot Bitcoin ETF is rejected (Deadline is July 6th 2022).

ETHE premium; ETHE discount narrowed to 1M low (15.14%) before increasing to 18.05%. 30D volumes are still down ~43% YTD.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has kept low indicating relatively low congestion on the network.

On-chain real (BTC) & off-chain volume; BTC on-chain volume has kept flat over the past week. BTC spot volumes (7d MA) has increased 11% while ETH spot volumes has increased 13% over the past week.

Hashrate & Difficulty; Bitcoin hashrate has fallen another 2% over the past week. Bitcoin mining difficulty has increased 4.3% to a new ATH.

Active addresses (BTC); Active entities (30d MA) has increased by 4% over the past week to 287k and now ~5% YTD.

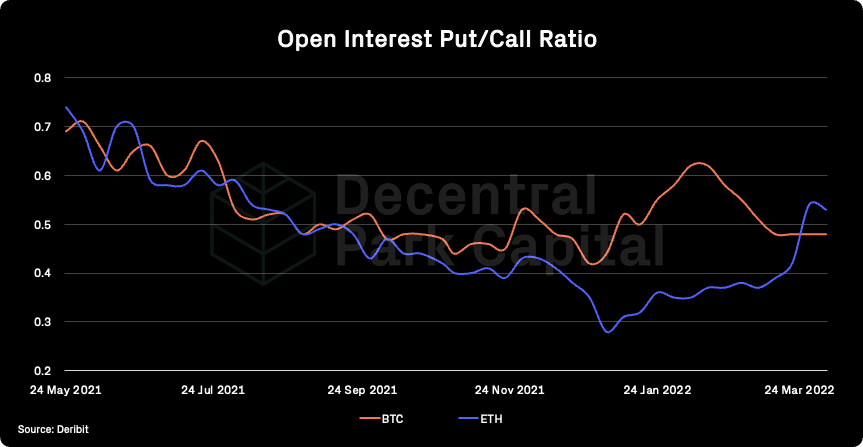

Trader positioning; No notable change in put/call ratio for BTC options. Aggregate perpetual funding rates for both BTC and ETH positive and increasing on the daily along with overall bullish sentiment.

Exchange inflow/outflow (BTC, ETH); Very strong (and growing) net outflows for BTC and ETH from exchanges ($3.7B and $4.3B respectively). A continued trend here may hint that traders are becoming less likely to sell, particularly with Ethereum.

📚 Monday DeFi Market Alpha [@dennis_qian]

📚 Challenging World-views in 2022 [@LynAldenContact]

📚 JOE Wars [@traderjoe_xyz]

📚 How PoS Could Come Sooner For Etheruem [The Defiant]

📚 Welcoming Feedback [rriccio]

🎙️ Forking The US Dollar [DeFi Mafia Podcast]

🎙️ The Ethereum Virtual Machine On Cosmos [Epicenter]

🎙️ Betting On Crypto’s Base Layer And A Multi-Chain Future [The Defiant]

🎙️ How Bitcoin Is Becoming The New Decentralized Gold Standard [The Scoop]

🎙️ The Sovereign Individual [Uncommon Core]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.