The Weekly #191

Bullish momentum carries over from stocks to crypto with decisive breakouts being seen for beta assets. Pocket Network sees ATHs for daily relays.

The Macro ‘Shrug-off’

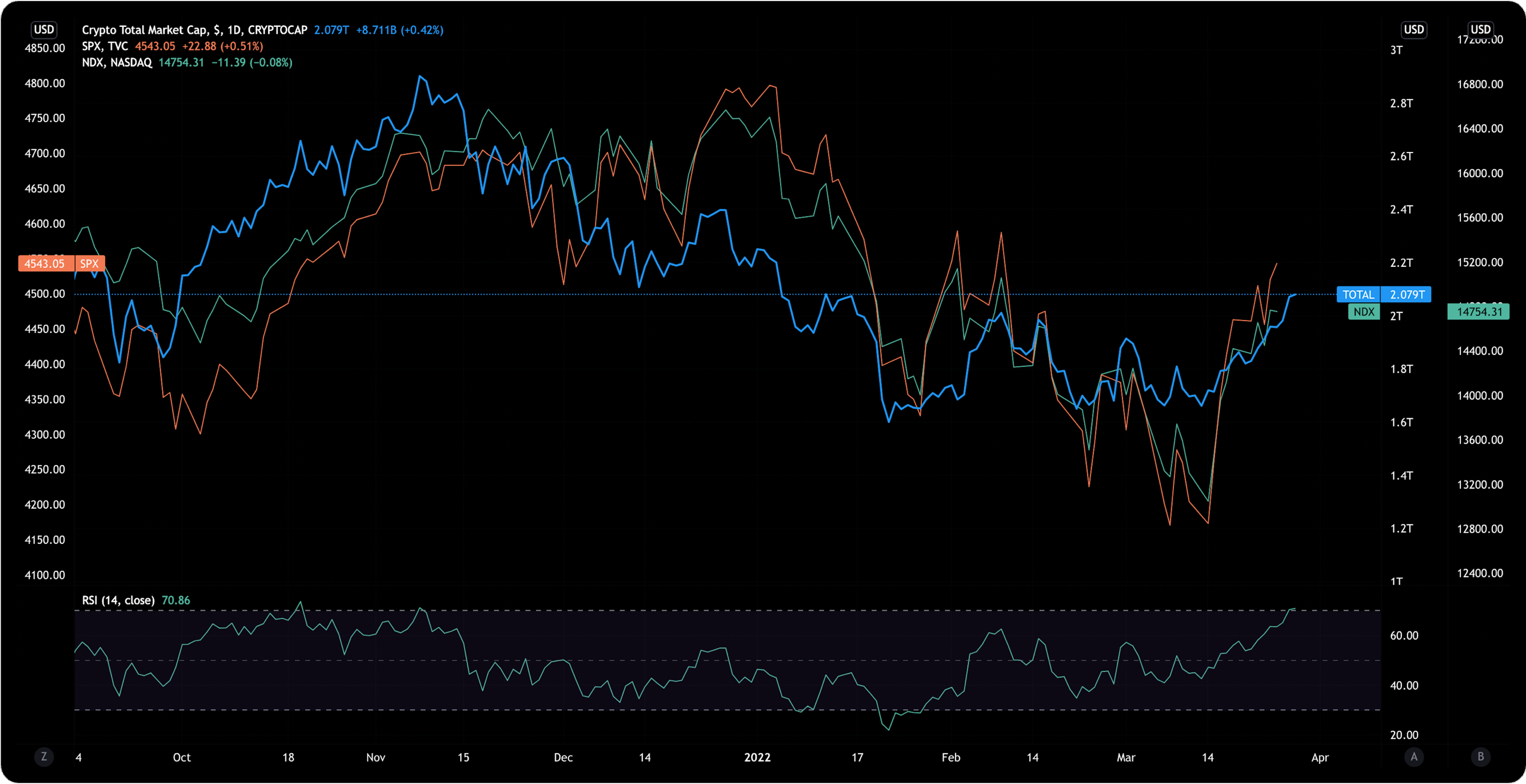

Another week, another set of green prints. Crypto market capitalization has risen 4.6% on the day, climbing further above the $2T mark - now standing at $2.3T.

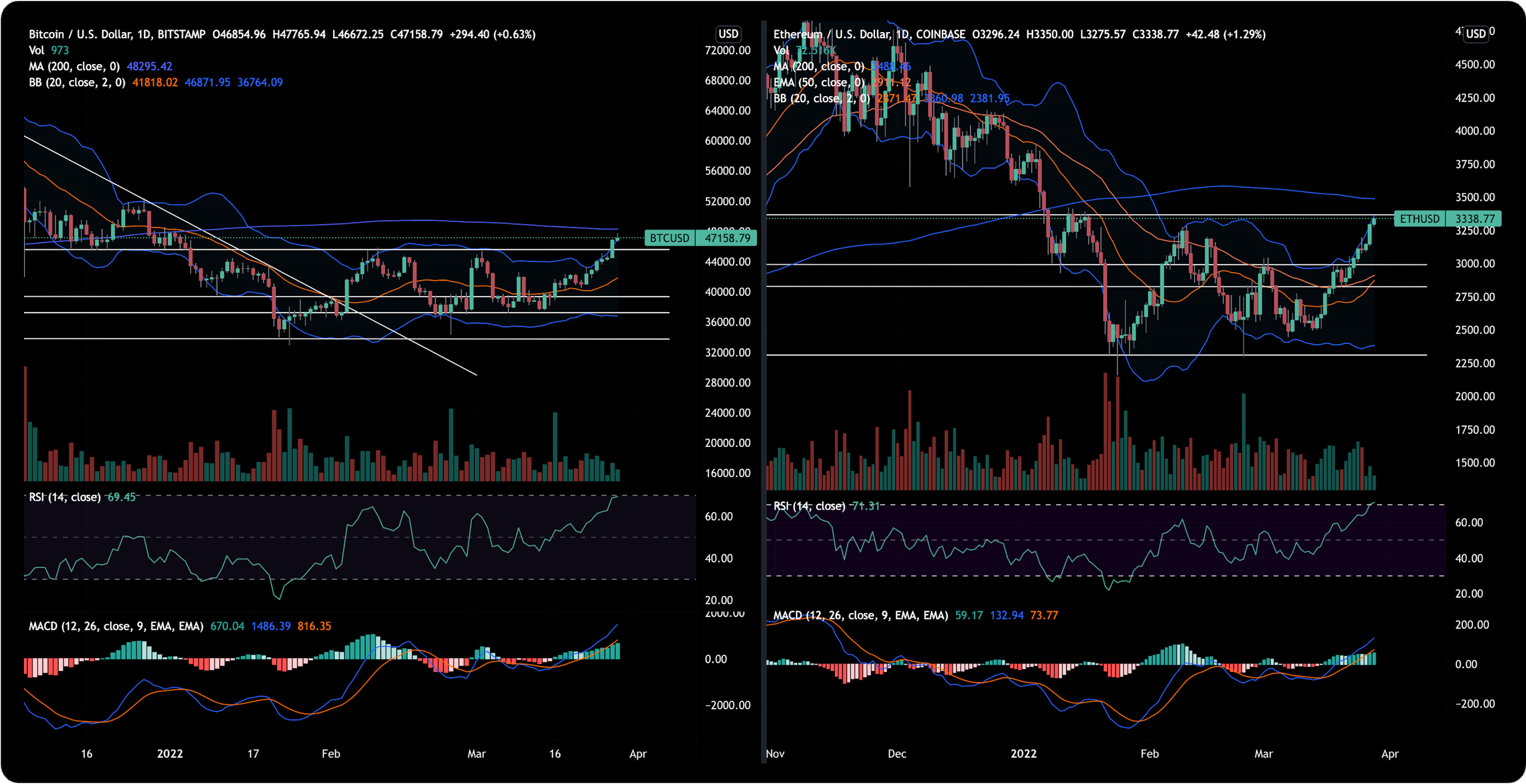

BTC has broken $45k and now trading at $47k (+6%) closer to the upper bollinger band (daily). ETH has followed suit climbing to $3.4k resistance (+6.3%). Daily RSIs are now fast approaching oversold levels (~70).

Select L1s are, in turn, outperforming higher cap names like Solana (+9.5%) and Polkadot (+10%).

As we highlighted in previous editions of The Weekly, analysis of the market structure pointed to a stronger likelihood of a volatile move in the coming weeks.

Neutral technical indicators against low volume and defiant (but growing) macro risk on appetite pointed to a more likely upwards move in cryptoasset prices and it appears this is playing out for now.

Over the past few sessions, stock investors have remained unfazed about more aggressive rate hikes, Ukrainian conflict, and spiked commodity prices.

For now, it appears recession fears are limited with stocks ‘defying the record bond selloffs. As JPM strategists note:

“Recessions only stated on average 16 months after the inversion in the spread, and never before.”

On the flipside, not everyone believes the equity risk premium should be so low and that fundamental headwinds from the Fed’s policy shift is not priced in. Just as we had dispersion in rate hike predictions, we now see growing dispersion in stock indices prediction for 2022.

Net, this has been beneficial for cryptoassets at large. 30D correlations with stock indices like SPX remain high (0.78) and it’s not clear why this relationship would necessarily breakdown near-term.

Liquidations Galore

Continues risk-on appetite has likely caught bears off in size. Firstly, Bitcoin open interest spiked to 383k BTC, a 12% increase MTD.

The OI/MCAP ratio eventually spiked above 0.02 on the 24th March - a level we note was a key area that historically precedes volatile periods from leverage flush outs.

Yesterday we saw $420m in total market liquidations of which 78.2% were short. $244m of these were BTC short liquidations.

This comes at a time when spot liquidity remains low. 7D spot volumes for Bitcoin trends at ~$6B which marks a 76% from its May 2021 highs of $26B.

Comparing BTC volume to MCAP also highlights how thinly traded cryptoassets are relative to the value of their respective network.

We also have good reason to believe there is growing demand within this relatively illiquid market. Over the past few days, the Terra Foundation has bought ~$1B of Bitcoin to back their UST stablecoin.

This liquidity dynamic is not isolated to Bitcoin. We are now seeing ATHs in net exchange outflows (~$2.3B) since November 2021.

Cryptoasset Performance

Sectors like DeFi have struggled to outperform beta over the past 2 weeks. Investors are often looking to deploy in the most liquid assets as momentum turns to the bullish, particularly where there are upcoming catalysts to point to.

Ethereum is one of those asset, outperforming its BTC counterpart by 7.7% (14D) and 2.3% (7D). See last week’s Catalysing The ETH Narrative In 2022 Edition of the Weekly.

We noted there that one of the last pieces we had yet to see take off was the off-chain coverage of the Ethereum’s merge. We believe that record on-chain adoption (e.g. Lido Finance) related to the merge will eventually lead to more widespread discussion.

There is evidence of this playing out already. As Lido nearly tops $17B in TVL, searches for ETH merge has now surged to ATHs relative to the past 12 months.

Key drivers likely include coverage from news outlets. Last week, Bloomberg analyzed the merge event within their business news vertical.

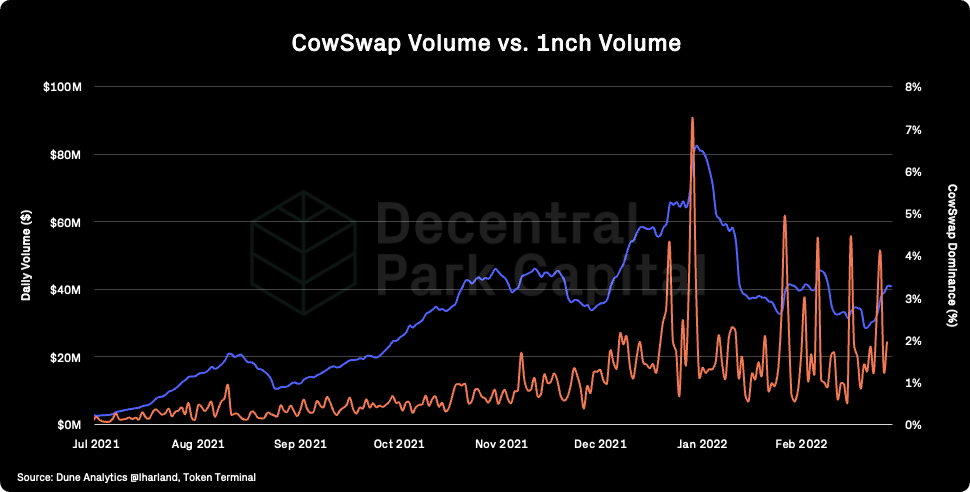

Cowswap/Gnosis

Cowswap volume has come down 50% from ATH levels seen in January 2022. Ratio of Cowswap volume to 1inch volume has kept steady at ~2% despite this fall.

GNO (Gnosis token) has been a top performing asset over the past week (+49%). Several CIPs have passed for Cowswap liquidity incentive programmes and the swapping of vCOW to COW to encourage price discovery of the COW token.

Pocket Network

Pocket Network saw new ATHs in daily relays serviced by the network - 610m. Relays were up 77.4% week-on-week. Polygon is now driving a large portion of these relays (34% 24Hr) with the network seeing relays become more distributed across a growing number of ecosystems.

The number of active staked POKT within nodes continues to increase which now stands at 600m POKT (~$600m) across 39,575 validators.

Top performing assets in the top 100 bracket include 2017-2018 coins which could reflect retail demand trickling back into the market.

Top 100 (7d %):

Zilliq (+156%)

Convex Finance (+61%)

ApeCoin (+58%)

Holo (+55%)

VeChain (+54%)

DeFi (7d %):

ICHI (+128%)

Redacted Cartel (+103%)

DeFi Kingdoms (+87%)

Dopex Rebate Token (+70%)

BadgerDAO (+64%)

Convex Finance will begin providing CVX incentives to veCRV holders beginning with 12K CVX tokens per week to the cvxCRV pool.

Yearn launched Curve Rocket Pool (rETH - wstETH) vault, currently has 7% APY.

Balancer is moving towards veBAL tokenomics, users will lock up 80/20 BAL/WETH BPT tokens instead of just BAL, the maximum locking time will be one year.

Immunefi found and reported a vulnerability in Gearbox. No funds are at risk, the protocol has been restored.

EU lawmakers step up KYC/AML requirements in an attempt to revise the current Transfer of Funds Regulation (TFR).

EU Parliament can outlaw transacting with 'unhosted' wallets, crypto advocate warns (CoinTelegraph).

EU Cracking Down on Unhosted Wallets (UTODAY)

Further work around stablecoin regulatory frameworks intensifies with key anticipated reports extending to the UK. Other countries are now looking to mirror Biden’s administration’s lead.

New UK Crypto Regulations Set to Be Announced in Coming Weeks (Beincrypto).

Bank of England Calls on Regualtors to minimize risk of cryptocurrency to financial stability (CoinTelegraph).

Financial Stability in Focus: Cryptoassets and decentralized finance (Bank of England).

Global market cap: $2.11T; Global market cap has increased by 13%, breaking above the $2T mark once again.

DeFi: $124B; DeFi market cap has increased 7%, less than global MCAP. DeFi dominance has fallen to 6% as beta assets take charge.

Market shares; Bitcoin dominance has climbed back to the 47%. Assets ranked 2-10 have seen their dominance fall slightly to 46%.

BTC/USD and ETH/USD

ETH/BTC

Price action; BTC broken past $47k today as sentiment swings to the bullish side. ETH broke past $3.4k but falling volume. Daily RSIs at oversold levels (70+). ETH/BTC RSI more neutral with and looking to break 0.0714 resistance.

Volatility (BTC & ETH); BTC 30D vol have kept flat over the past week while ETH 30D vol has fallen slightly. BTC ATM 1M implied vol near 3M low (61.24%) while ETHa at 3M low (65.59%).

Combined order books; Order books are heavier on the ask side. Heavier resistance all the way up to $49k (Source: Bitcoinity).

Crypto vs. SPX; Cryptoassets remain positively correlated to stocks with this relationship strengthening over the past week (0.84). U.S. stocks trending lower (-0.07%) in early Monday morning trading but despite continued uncertainty around the path to increased rates, recessions, and economic slowdowns driven by the Ukraine-Russia conflict, risk assets are set to be directionally positive for now overall.

Gold prices suffered a loss (-1.3%) which could reflect diminishing risk of Russia-Ukrainian escalating near-term.

GBTC premium; GBTC discount has fallen from ATHs (~30%) to 26% - a move generally in line with spot price action. Secondary market demand continues to fall with volumes falling 15% MTD (5.133M).

ETHE premium; ETHE discount narrowing closer to NAV at -17.19% also in line with spot. ETHE volumes has fallen to ATL since January 2021 (~3.4m) indicating low demand on secondary market.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has kept low indicating relatively low congestion on the network.

On-chain real (BTC) & off-chain volume; BTC on-chain volume has increased 20% over the past week. BTC spot volumes (7d MA) has increased 7% while ETH spot volumes has increased 17% over the past week.

Hashrate & Difficulty; Bitcoin hashrate has fallen 2% over the past week. Bitcoin mining difficulty has kept flat over the same period.

Active addresses (BTC); Active entities (30d MA) has increased by 3.3% over the past week to 283k.

Trader positioning; Put/call ratio for ETH has surged to 0.54 while no notable change for Bitcoin traders over the past week. CME OI has climbed to 61.3k BTC or 16.5% of total OI - up 2% since March 1st. Funding rate climbed to moderately positive for both BTC (0.006%) and ETH (0.004%).

Omenics Sentscore (BTC); Sentiment around Bitcoin remains elevated as Bitcoin surges past $47k.

Exchange inflow/outflow (BTC, ETH); Very significant net outflows for both BTC ($2.1B daily) and ETH ($2.3B daily). ATHs in net outflows for Ethereum since November 2021.

📚 Copyright Vulnerabilities in NFTs [IC3]

📚 Lending Wars on NEAR [@HiimAlen]

📚 Latest Week In Ethereum [@WeekInEthNews]

📚 Where Anchor Goes From Here [@anchor_protool]

📚 The Decomposition of Attention [knower]

🎙️ The $10B Stablecoin Bet on The Bitcoin Standard [The Pomp Podcast]

🎙️ Impact on Sanction, deglobalization, food, and shortage risks [All-In]

🎙️ Connecting Cosmos and Ethereum with Gravity Bridge [ZeroKnowledge]

🎙️ On The GBTC ETF Application [On The Brink]

🎙️ Mitigating Risk in DeFi [The Scoop]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.