The Weekly #186

Investors remain nervous with geopolitical, regulatory, and economical factors continuing to weigh in on the crypto markets.

A Nervous World, A Nervous Market

The crypto market has fallen a further 9% on the week with total market capitalization failing to climb back above the $2T mark.

Overall, it appears the crypto market is predominantly nervous - perhaps a mere extension of what we see in the equity markets more broadly today.

The cocktail of worries on the global stage (both geopolitically and economically) are still very much in play with two key ingredients to watch out for this week: The Ukraine-Russia conflict and regulation.

The Ukrainian-Russia tensions have somewhat escalated as the diplomacy avenue for both countries began to deteriorate rapidly. The impact locally to Russia has been immediate with Russian stocks falling the most since the 2008 financial crisis. The MOEX Russia Index has plunged 14%.

After breaking the $40k mark on February 4th, BTC failed to gain momentum with on/off-chain indicators last week all pointing to towards a quick softening of the market.

Through all of this uncertainty, what is becoming more clear is markets are nervous and reactionary. Headlines of a summit between the US and Russia eased concerns short-term with Biden agreeing ‘in principle’. Crypto markets recovered swiftly in the subsequent hours with BTC itself being pushed back closer to $40k (+4%).

Given markets are reactionary, headlines fueling fear can have the opposite effect. Now that it is believed Putin will recognize Eastern Ukraine separatist, widespread investor concerns are now reignited today. Cryptoasset prices came down as quickly as they came up. It wasn’t long before BTC fell back below $38k.

The contagion risk from moves seen in equities to crypto shouldn’t come as a surprise today. Rolling correlations between crypto and US equities have been keeping above 0.4 and increasing with a positive relationship likely to only grow over the coming weeks.

The second ‘cocktail ingredient’ to pay attention to this week is Biden’s executive order announcement. This order will direct a wide range of governments agencies to study cryptocurrency and CBDC as well as a framework to regulate. cryptoassets

Given the ‘nervous' market structure, this release is more likely to add volatility to markets than not. It is another question as to how much the market is already pricing in such headlines coming in.

Market’s Expectation on Fed Hikes

Last Friday, The Federal Reserve seemed to push back on what has appeared to be growing market expectations of an aggressive 50 BPS rate hike in March 2022. Tighten monetary policy too much and you stifle economic growth. But do too little and inflation continues to burn though consumer pockets.

Wall street continues to work out what the Fed will do with JPMorgan now expecting nine straight rate hikes albeit in 25BPS chunks.

The crypto market, which is down 43% from its all-time-high, could be see further pressure if the more aggressive move is made.

What’s more certain is that estimates can (and will) change quickly based on other unexpected news including Ukraine-Russian tensions.

The mix of one ingredient in the cocktail of worries can always affects another.

BTC Futures

Open interest in the futures market for both BTC and ETH have declined slightly with BTC OI down 6%. BTC-denominated OI picked up to 350k but we have yet to see a clear shift in overall declining interest in 2022.

Funding rates remain slightly positive as traders take a predominantly bullish stance. Yet, with falling funding rates and OI, bullish momentum remains faded as spot fails to break above $40k.

Falling crypto-margined futures OI (~40% vs. 70% in April 2021) has helped reduce levels of exacerbation for crypto volatility.

Short-term Holders Capitulate

On-chain like STH-MVRV also show a continuation of short-term holder capitulation as BTC heads closer to $38k. A sustained moved above 1 would indicate demand would be able to absorb any market sells (green shades).

There has been little dispersion within the crypto markets with cryptoassets tightly coupled in their trends.

ETH has managed to outperform against BTC this week (+1.5%) but still remains 22% below its early December highs.

Outperformers in the market have typically centred around data middleware protocols with API3 leading the charge (48.3%). Other oracle networks like DIA and BAND have benefitted form API3’s momentum over ETHDenver as the project attracted attention as the DeFi track sponsor.

Top performing assets are are mostly retail-centred assets indicating some pulses of interest from those market participants on select assets.

Global (7d%):

API3 (+48.3%)

DAOhaus (21.8%)

Radicle (+9.9%)

DIA (+1.7%)

Band Protocol (+1.3%)

DeFi (7d%):

API3 (+48.3%)

Anchor Protocol (+20.3%)

Radicle (+9.9%)

DIA (+1.7%)

Band Protocol (+1.3%)

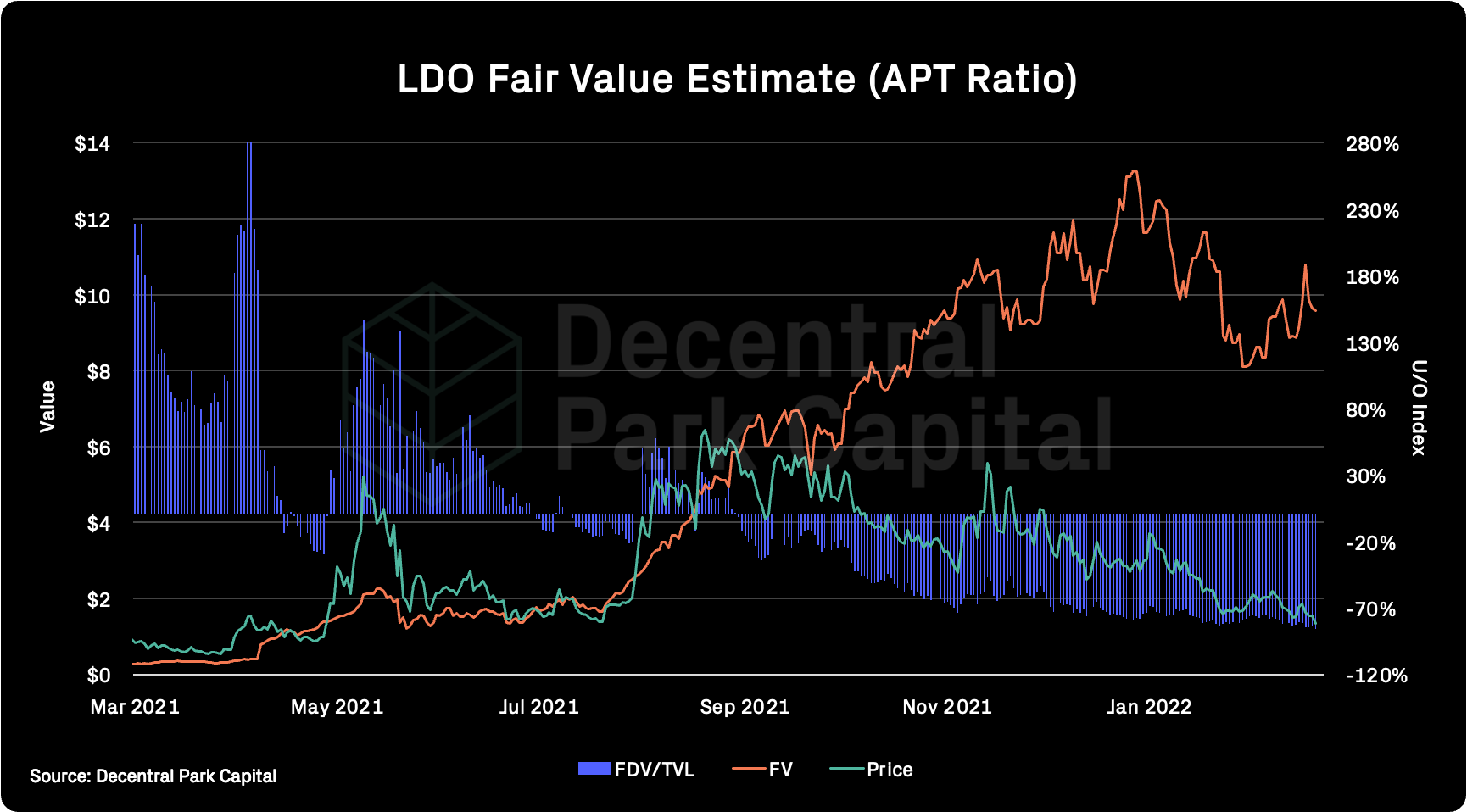

Lido Finance

Lido has seen a 17% increase in USD-denominated TVL and 20% increase in ETH denominated TVL since January 2022. LDO’s continued drawdowns against this growing TVL implies an 86% discount below its APT fair value.

After targeting the Solana and Terra ecosystem, Lido is now after Polkadot and Kusama. Users are now able to stake their KSM and unlock liquidity to be used within Kusama’s DeFi ecosystem.

Maple Finance

The institutional capital marketplace is now seeing $600m in total-value liquidity provided to Maple’s credit pools.

Last week saw over $100m in loan value provided to Alameda Research. Blue chip crypto marketplace Abra deposited $25m and existing lenders like CoinShares have provided $22m in loan value.

Lido launched liquid staking on Kusama using Moonriver. KSM can be staked for 18% APR.

Frax FPIS airdrop snapshot was taken at block height 14246086. FPIS is a seigniorage token for upcoming FXS. Aidrop details and eligible addresses can be found here.

Saber launched solUST (Soluna) / USDH (Hubble) pool. Farm is not launched yet, APY TBD.

Anchor is discussing veANC pivot. If the proposal passes, Anchor will employ Curve pioneered ve economics, LPs will be able to lock ANC to receive veANC.

Regulatory frameworks are taking shape as a global flooring exercise drives clarity for crypto assets.

UAE Readies National Crypto Licensing in Push to Embrace Fintech (Bloomberg)

Wilkins Pushes Canada for ‘Ambitious’ Cryptocurrency Framework (Bloomberg)

EU Is Open to Cryptocurrency But With Regulation, Top Official Says (Bloomberg)

Crypto bill incoming: Russia’s finance ministry kicks off public comment period (Cointelegraph)

Russian Government Introduces Crypto Bill to Parliament Over Central Bank Objections (CoinDesk)

Crypto Could Have ‘Destabilizing Effect’ on Financial Sector: FSB (Decrypt)

Global market cap: $1.8T; Global market cap has fallen by 9% over the past week.

DeFi: $110B; DeFi market cap has fallen 6%, slightly less than global MCAP. DeFi dominance has therefore picked up over the week (+3%).

Market shares; Bitcoin dominance has kept its dominance at 47%.

BTC/USD and ETH/BTC

ETH/USD

Price action; Choppy price action after CPI print. Retracements back to $38k for BTC/USD and $2.6k for ETH/USD. MACD remains heavily bearish for BTC/USD after recently crossing to the downside a few days ago.

Volatility (BTC & ETH); BTC and ETH 30D vol has fallen sharply. Implied 1M vol for BTC and ETH 59.72% and 69% respectively.

Combined order books; Order books slightly heavier on the bid side. Heavier resistance up to $38.8k (Source: Bitcoinity).

Crypto vs. SPX; Correlations between crypto and equities still remain moderately positive. Ukraine-Russian tension leads Gold to 8-month high despite interest-rate increases weighing in on the gains.

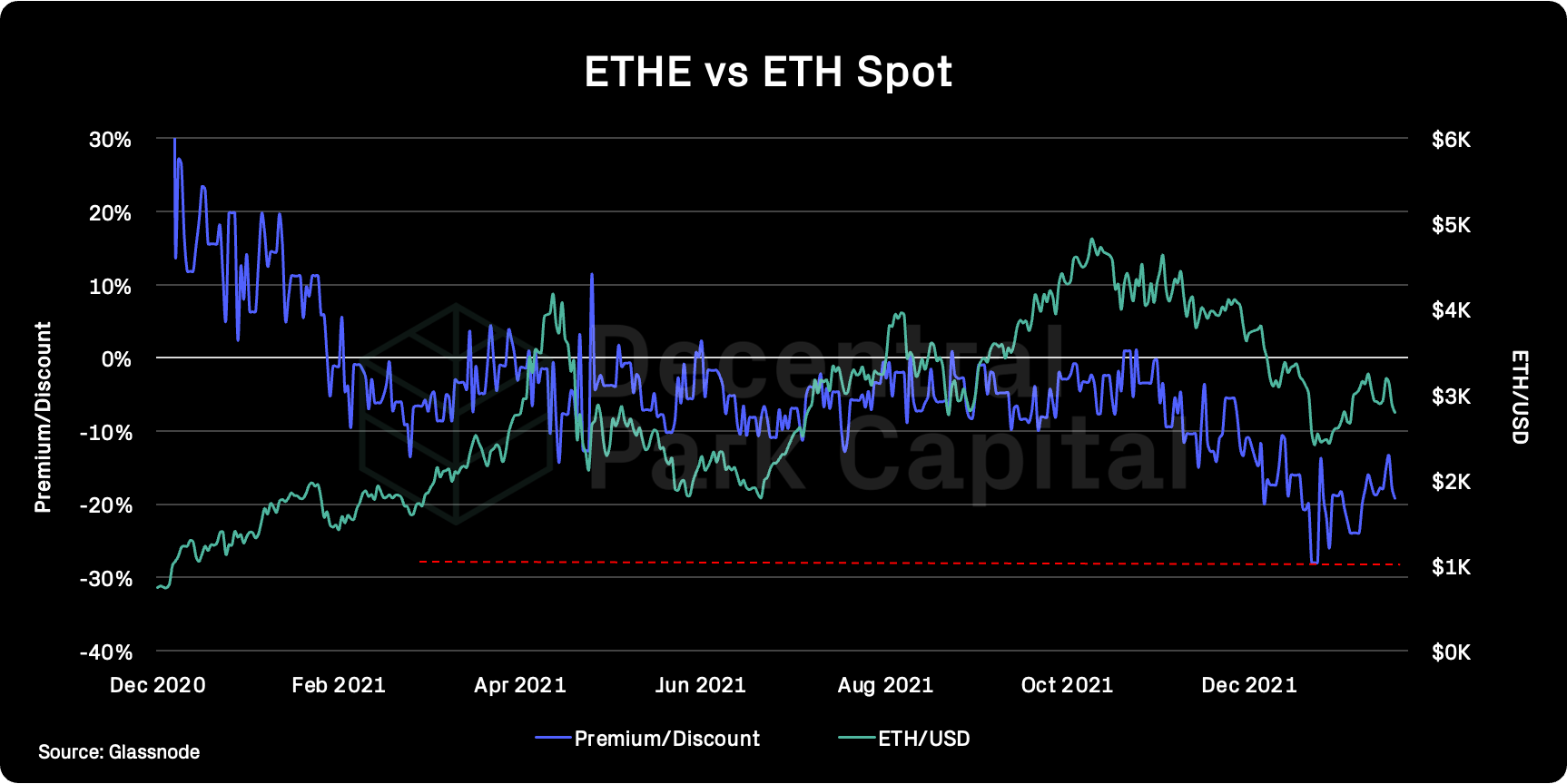

GBTC premium; GBTC discount falling to near ATHs (-26%). 30D volumes are picking up YTD (~7m).

ETHE premium; ETHE discount to NAV has fallen to 20% from 28%. Secondary market volumes for ETHE has fallen 10% YTD.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has fallen back to nominal levels in recent days as BTC rallied to $45k.

On-chain real (BTC) & off-chain volume; BTC on-chain volume has fallen 15% over the past week. BTC spot volumes has fallen 28% and 14% for ETH over the past week (7d MA).

Hashrate & Difficulty; Bitcoin hashrate has hit new all-time-highs reaching 214m (TH/s; 7d MA). Difficulty has adjusted 4.7% as a response. Bitmanu has announced 3mn bitcoin mining ASICs and represent some of the earliest 3nm mining rigs to hit the market.

Active addresses (BTC); Active addresses (30d MA) has increased 1% over the past week and continues its recovery from annual lows.

Trader positioning; Open interest denominated in the native cryptoassets (BTC,ETH) have ticked up marginally with funding rates for BTC positive albeit declining. Put/call ratio falling slightly for Bitcoin while ETH remains flat. No clear signs of bullish momentum returning today.

Omenics Sentscore (BTC); Sentiment score around BTC became moderately positive as the orange coin headed broke above the $40k key resistance. Sentiment turning negative with investors nerves commanding their positioning.

Exchange inflow/outflow (BTC, ETH); Divergence between BTC and ETH with regards to net exchange flows continues. We see ~$800m net flow out of exchanges while ETH has ~$800-$1B of net flows to exchanges.

📚 On Frax Finance [Decentral Park Capital]

📚 OpenSea Phishing Attack Breakdown [@NadavAHollander]

📚 On Series As [@csoopa]

📚 State of The Market [@Galois Capital]

📚 A Breakthrough In Token Network Design [@cdixon]

🎙️ On FAANG to Web3 [EthereumDenver]

🎙️ All-In Ep 68 [All-In]

🎙️ NFT Innovation [The Metaverse Podcast]

🎙️ Why A US Senator Just Said The Fed Should Buy Bitcoin [The Breakdown]

🎙️ Syndicate DAO on The Transforming The VC Landscape [Blockcrunch]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.