The Weekly #181

US inflation data supports Fed bets and drives mixed results for equities. DeFi continues to shine its light in an overall soft market.

Inflation Data Go BRRR..

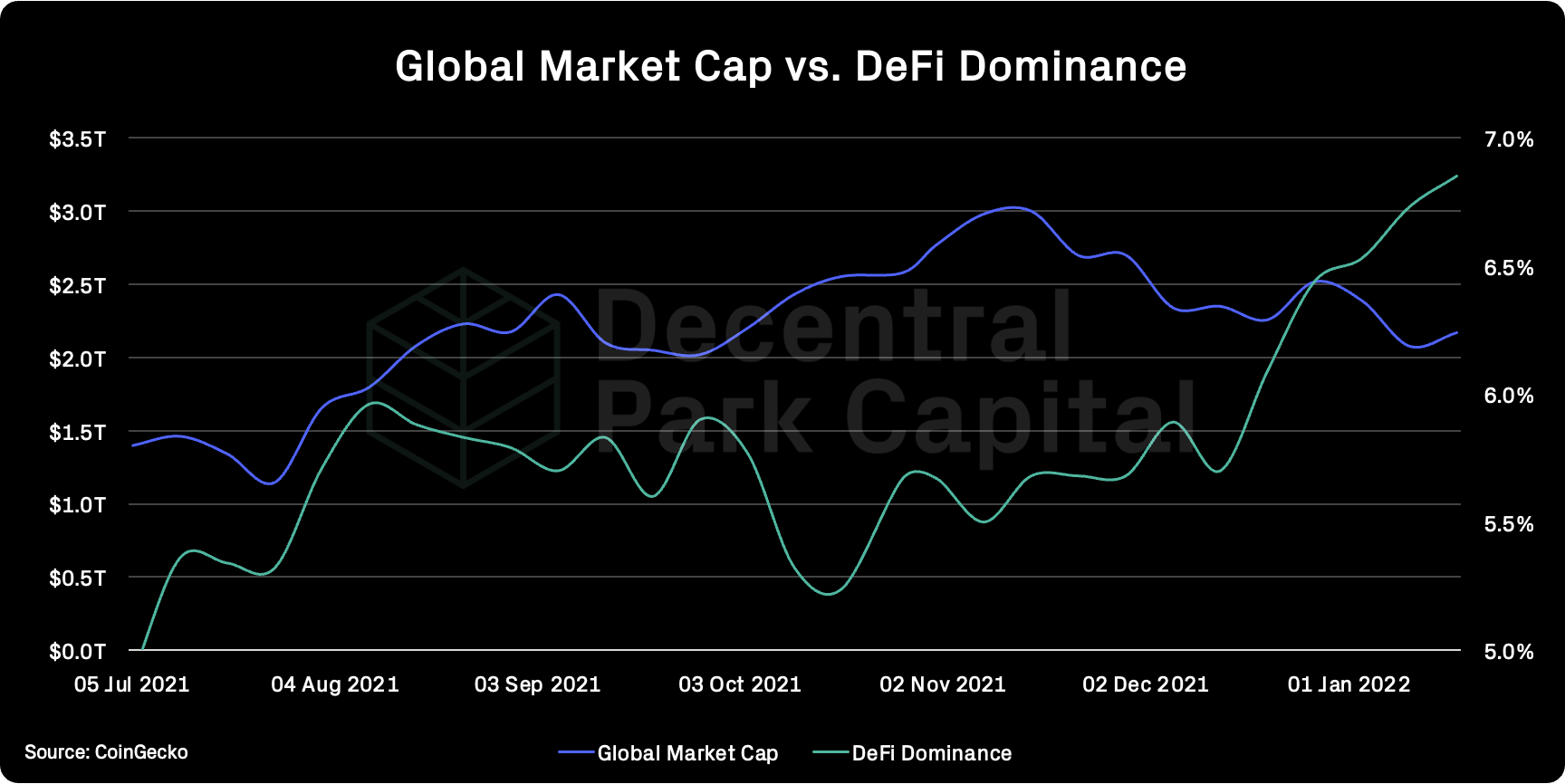

Crypto markets have rebounded slightly over the past week, increasing 4% and standing at $2.17T. BTC continues to hold support at $40k and ETH above $3k.

One of the main headlines last week was the US inflation print with CPI jumping 7% over the past year. This is the fastest 12-month pace in nearly 40 years and comes amid a shortage of goods and workers along with unprecedented cash in the US economy.

This CPI print will do little to change The Fed’s strengthening hawkish stance. According to CME’s FedWatch, markets are now pricing in an 80% chance for first-quarter-percentage point increase to occur in May. There is a 50% the Fed could enact four total hikes in 2022.

However, it may not rattle wider risk markets just yet. A 7% annual change in CPI was in line with wider expectations and equities were not shake dramatically. Equities were helped by longer-dated U.S. Treasury yields which had been weighing on growth sectors like Technology.

“It's a matter of riding that bull,” she said. “It's going to be a wild ride, and there will be people who are thrown off the bull and who's going to stay on the bull.”

Loreen Gilbert (WealthWise Financial, CEO)

Where does this say about crypto? As we’ve explored in previous editions of The Weekly - crypto as a whole has kept in line with wider equity trends. November and December being more challenging periods for crypto relative to equities as investors likely accelerated their profit taking for year end.

So far this year, the relationship between these two markets is strengthening positively and should not be wholly surprising. What weighs in on stocks weighs in on crypto.

Crypto Receiving The Cold Shoulder

Cryptoassets, which remains on the far end of the risk continuum for investors, continues to receive limited interest in the new year as the derivatives markets highlight.

Implied 1M volatility for BTC has fallen sharply to ATLs since October 2020 with overall demand for options keeping low.

Wider macro headwinds may be playing a core role in overall enthusiasm being curbed and negative impact on prices is a real possibility.

More positively, falling OI and funding rates kept neutral at 0.001% points to the market not becoming over-levered. Concerns around long-liquidations driving price cascade should be eased for now.

This is supported by the OI/MCAP ratio which continues to fall below 2% - a level that often coincides with significant margin flushes.

On-chain indicators focussing on short-term BTC holders signal bearish momentum medium-term. The STH-MVRV has yet to capitulate to its multi-year lows which has marked price BTC’s floor before momentum reversals.

Bitcoin’s STH-NUPL has also yet to reach its multi-year floor which has occurred every time the indicator flips negative (network moving into a state of loss). This would imply a more severe short-term shakeout before a sustained period of price recovery.

But Gilbert’s observation on the equity market will likely be true of the crypto markets too. There are 3 general planes in which investors can and will evaluate outperformance: Sectors, vertical in sectors, and assets within individual sectors. Let’s explore.

The Bright Spot - DeFi

After lagging for a number of months, one bright spot so far in 2022 has been DeFi where its sector dominance continues to climb until all-time-highs (6.9%).

Total-value committed to blockchains has kept relatively steady since the market highs in early November, falling ~8% while the wider market has declined by over 32%.

This value is becoming even more distributed across ecosystems. Ethereum’s TVL dominance has now fallen to 60% for the first time as alternative ecosystems continue to make strides.

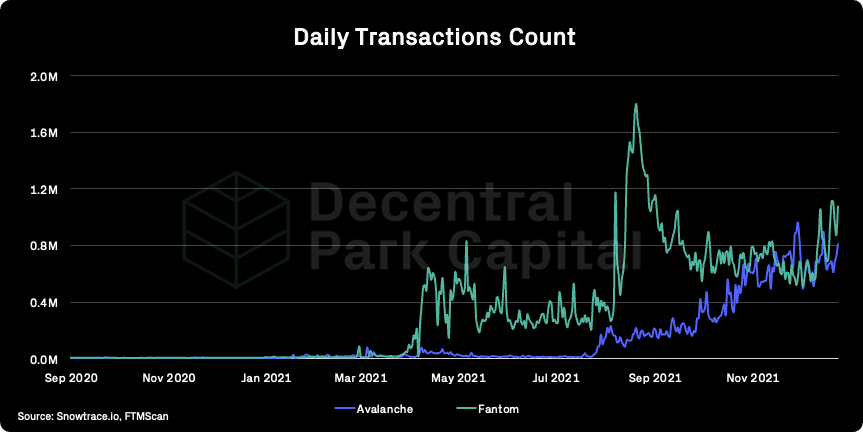

Fantom

Fantom has received growing interest from users and investors since Daniele Sestagalli and Andre Cronje disclosed a new AMM launching on the L1, ve(3,3).

The airdrop for ve(3,3) is anticipated to be released either this week or next. Up to 60% APR on stablecoins has also helped drive daily transactions to new highs since September 2020, firmly overtaking Avalanche’s count.

Osmosis

Osmosis has climbed to new ATHs and has been largely driven by 3 main factors:

1) Trading volumes surging to $100-$160m daily with OSMO being priced a lower multiple to its volume

2) TVL in Osmosis climbing to new ATHs ($1.43B) aided by ATOM/USD reaching new ATHs ($43)

3) Increased awareness around cross-chain bridges and IBC-enabled ERC-20s

Osmosis is now the 3rd most valuable DEX after Uniswap and Curve.

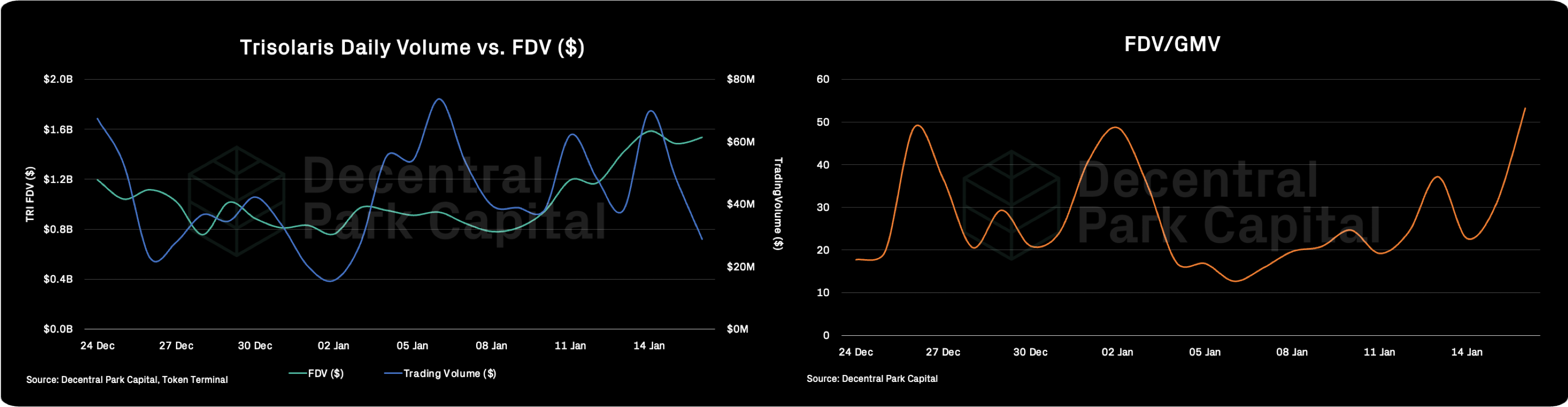

Trisolaris

Keeping on the DEX theme - Trisolaris, a native DEX deployed on NEAR, is already seeing daily trading volume hit above ~$40m and TVL climb 42% YTD ($583m).

TRI is trading 50x of its daily volume and trading 2.38x its TVL. What’s interesting here is that both data points are significantly lower than Osmosis (120x and 7.2x respectively). Either a premium is being placed on Osmosis and its future growth and/or a re-pricing may occur between these two emergent ecosystem DEXs.

Angle Protocol launched veANGLE, LPs can lock ANGLE tokens from 1 week to 4 years to receive their share of the interest generated by the protocol. Current APY is 400%.

Convex Finance launched pools for SPELL / ETH and T / ETH Curve LP tokens with 11.5% (proj. 40%) and 19.8% (prof. 120%) APY respectively. Alternatively, LPs can stake LP tokens for 20% and 23% APY in Curve Gauge.

A proposal to enable Fei Protocol's FEI to be used as collateral on Aave has 99% pro votes (ends Jan 19) and is likely to pass. Users already can borrow FEI on Aave for TRIBE rewards.

Tokemak launched GAMMA reactor (ex-VISR reactor). LPs can deposit GAMMA for 64% and TOKE for 18%.

Legislators force regulators to the middle. House and senate agriculture committees issue bipartisan call for CFTC guidance on crypto (CoinDesk).

Stablecoins are regulated by charter, creating a regulatory floor for mass adoption. OCC Chief: Bank regulation can put ‘stable’ in stablecoins (Decrypt). Hong Kong begins discussions to introduce stablecoin regulatory framework (Cointelegraph). Palau president talks stablecoin plans following island nation’s ‘digital residency’ rollout (CoinDesk).

US announces the covert development of a CBDC. Fed’s Lael Brainard invites congress to choose whether to compete with China’s digital yuan (Cointelegraph). Bill seeks to ban Fed from issuing digital currency to consumers (Decrypt). BIS, Swiss national bank, SIX exchange complete wholesale CBDC trial (CoinDesk). Visa offers test platform for central bank digital currencies (Bloomberg).

Global market cap: $2.17T; Global market cap has increased 4% over the past week.

DeFi: $152B; DeFi market cap has increased 5%. DeFi dominance now approaching 7% and an all-time-high.

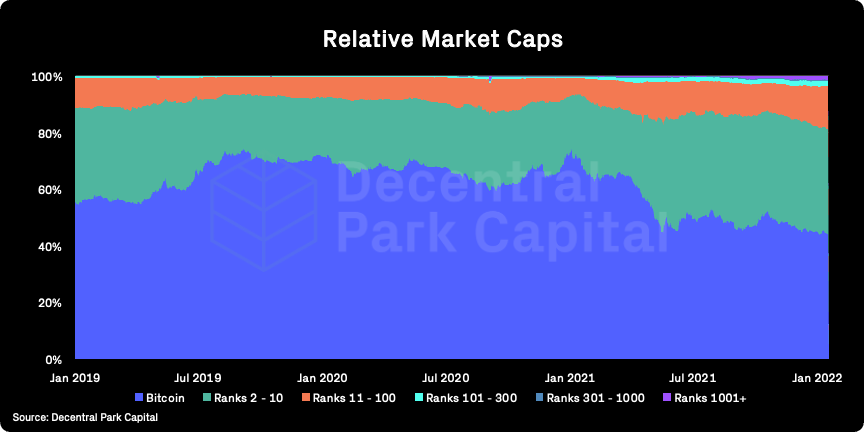

Market shares; Bitcoin dominance has kept flat over the past week and now standing at 47.5%.

BTC/USD

ETH/BTC

Price action; BTC still holding support at $40k and ETH at $3k with both assets rebounding from sub-30 daily RSIs but are still near oversold territory. Both assets kept below their 200d MA with ETH/BTC under pressure for the same trend.

Volatility (BTC & ETH); BTC and ETH 30D vol have fallen over the past week in line with implied volatility measures.

Combined order books; Order books look fairly even. Heavier resistance up to $44k (Source: Bitcoinity).

Crypto vs. SPX; Relationship between global crypto markets and equities strengthening to the positive since late December. Macro pressures on risk assets likely to carry over to crypto generally.

GBTC premium; New all-time-high for GBTC discount last week indicating low institutional demand for GBTC on secondary market. GBTC volumes up 11% YTD.

ETHE premium; ETHE discount/premium still showing descending channel also pointing to limited interest on secondary market. EHTE volumes down 3% YTD.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains relatively low indicating low network utilization.

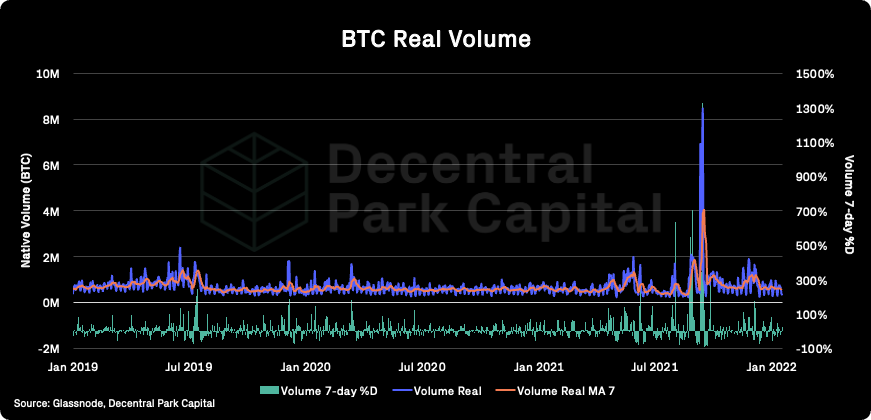

On-chain real (BTC) & off-chain volume; BTC on-chain volume has kept relatively flat over the past week. BTC and ETH spot volumes have fallen 17% and 22% respectively over the past week (7d MA).

Hashrate & Difficulty; Bitcoin hashrate jumps to new ATHs as jack Dorsey announces a project looking to build an “open Bitcoin mining system”.

Active addresses (BTC); Active addresses (30d MA) has fallen 1% over the past week and 4.5% YTD and, as a proxy measure, indicates lower overall network usage.

Trader positioning; Perpetual funding rates flipped negative for both BTC and ETH pointing to traders taking a predominantly bearish stance. Combined with falling OI, volume, and implied volatility indicates softening interest from investors.

Omenics Sentscore (BTC); Sentiment score around BTC continues to fall over the past week as the asset hovers above $40k.

Exchange inflow/outflow (BTC, ETH); Net flows for ETH and BTC remain positive. ETH net flows have fallen 66% from Jan highs ($3B/daily). BTC showing more stable USD-denominated net inflows to exchanges (~$200m).

📚 22 Regulatory Predictions For 2022 [@Leo Lucisano]

📚 Cross-chain visualized [@Timecopeland]

📚 Wu-Tang Project Lead [@PleasrDAO]

📚 MEV Report [Galaxy Digital]

📚 Egirl Capital 2022 Predictions [Egirl Capital]

🎙️ L1 Wars [Web3Vault]

🎙️ NFTX [Zima Red]

🎙️ Weekly Roundup [On The Brink]

🎙️ Apathy in DAOs [Block Crunch]

🎙️ Stablecoin Regulation [The Breakdown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.