The Weekly #173

Outlook remains largely bullish with turbulence expected around the upcoming US Fed meeting this week. Metaverse and meme-related assets start outperforming the market.

BTC Relief

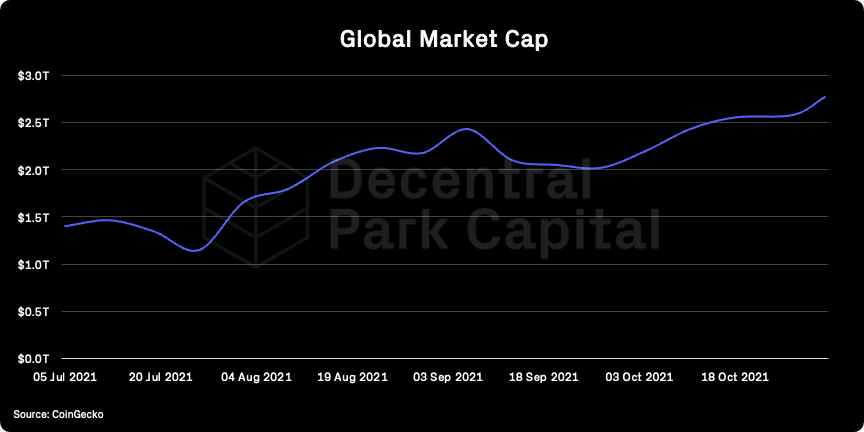

Bullish sentiment remained last week as the global crypto market cap printed new ATHs of $2.78T.

BTC fell to a weekly low of $56.4k before recovering strongly back above the key psychological level of $60k. BTC now trades at $62.3k at the time of writing.

Meanwhile, Ethereum printed new ATH of $4.46k. The more interesting data point was this came at a time when Facebook announced their rebranding to Meta - a strategic decision to pivot towards the Metaverse. Expect ongoing discussions for how Ethereum and Meta will diverge and also work together for this emergent digital world.

Other L1s have taken a breather this week with DeFi assets largely outperforming the market.One valuation lens of long-standing and emergent L1 chains is through Metcalfe’s Law.

L1 performance are becoming uncorrelated but the market appears to be valuing these ecosystems systematically according to their active user base. For example an FDV/Daily active addresses ratio for L1s shows two key things:

1) Ecosystems are valuing users more as those ecosystems become realized (ratio is increasing over time). This follows the S-curve model.

2) The difference between the highest and lowest ratios is narrowing. The market values active user bases equally across ecosystems regardless of their age.

One clear implication being that L1s should continue to become more valuable as their active user base grows.

DeFi

The global DeFi market cap printed new ATHs last week topping out at $154B. While directionally positive, DeFi’s dominance remains low at 1.8% and yet to break out above previous ATHs of 3%. The DEFIPERP/ETHUSD ratio has formed a bottom as the sector starts showing promising growth.

There are plenty of reasons to be optimistic. ‘Institutional DeFi’ narratives are building with the launch of institutional DeFi products. The recent example being Valour’s Uniswap ETP. As seen with other ETPs, these products can create a supply-side liquidity crisis for assets that are locked for 6-12 months.

DeFi fundamentals also remain strong with both aggregate exchange and lending volumes either printing or near ATH levels ($14B and $31B respectively).

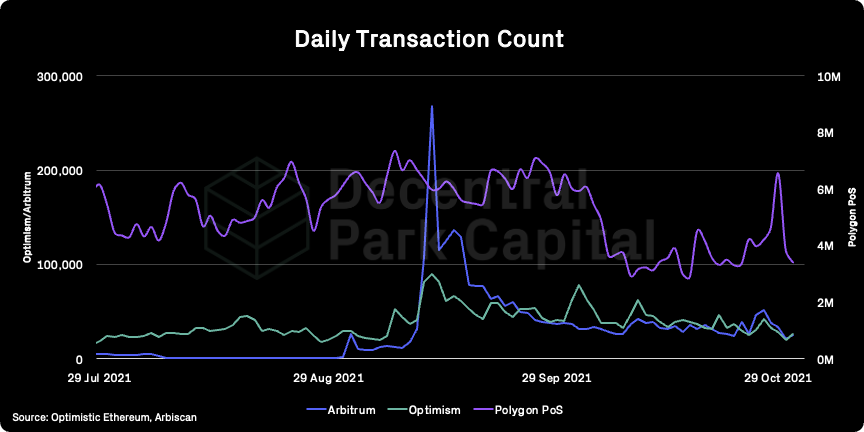

L2 Growth

Ethereum’s scaling ecosystem has seen continued growth over the past week in key metrics, including total-value-locked ($4.7B). L2 TVL growth is outpacing L1 TVL growth - with the L2/L1 TVL ratio at an ATH of 2.7%.

As highlighted last week, this growth comes at a time when both Arbitrum and Optimism are preparing for their own respective network upgrades.

As liquidity grows, these ecosystems become more useful and sticky for users with incentives continuing to play a key role in competing against one another.

Arbitrum maintains it top spot for TVL ($2.8B) but Optimism has see that largest weekly growth (+66%) over the past week, surpassing $450m.

However, transaction count for these ecosystems paints a different story. Both Arbitrum and Optimism have had declining TX count trend over October while sidechains like Polygon has seen an uptrend over the same period. While the scaling narrative is building, we are clearly still early with L2 adoption.

Top performing assets have fallen in either the Metaverse (following the Facebook news) or the meme coin camp. This points to a resurgence in retail-driven speculation.

Global:

Decentraland (+306%)

The Sandbox (+157%)

SafeMoon (+121%)

Shiba Inu (+98%)

Basic Attention Token (+54%)

DeFi:

Frax Share (+94)

Seedify.fund (+68%)

Loopring (+65%)

Convex Finance (+40%)

bZx Protocol (+34%)

AAVE (-58 U/O)

Aave’s TVL fell 21% over the weekend with the main driver being Justin Sun withdrawing $4.2B. The decision comes at a time when concerns about a potential Aave vulnerability were raised. As a result XSUSHI and DPI borrowing were disabled along with UNI/BAL liquidity pools.

AAVE still remains the largest lending protocol by TVL and undervalued by 58% by its APT ratio.

LDO (-58 U/O)

Lido’s aggregate TVL has surged to new ATH due to ETH price appreciation, now standing at $9.5B. A 100k ETH were staked via Lido over the month of October. This is a slower growth rate than previous months but was higher than all other staking platforms.

With TVL growth not translating to positive LDO price action, LDO is at an ATL on its U/O index.

wNXM (-70% NXM Discount)

The mutual has seen a 21% increase in active cover (+19k ETH) since October lows with recent catalysts being the C.R.E.A.M exploit where the mutual has started to approve claims.

The wNXM-NXM discount is at an ATH of 70% with wNXM continuing to underperform both ETH and the wider DeFi market. Nexus Mutual’s price-to-book ratio is at a new ATL (0.49). This comes at a time when the Nexus community is discussing approaches for solving the widening wNXM-NXM discount.

Alpha Homora V2, a leveraged yield farming protocol, has launched on Avalanche with 34% APY on AVAX.

TraderJoe, a DEX protocol on Avalanche, has launched MIM lending market, MIM can be deposited for total 19% APR. LPs can use Snowball to autocompound rewards and earn additional SNOB to boost APY up to 63%.

Curve has launched CRV rewards on Avalanche: 0.25% for Aave pool, 4.5% for ren and 3.20% for tricrypto.

Allbridge and Orca are bringing AVAX to Solana with AVAX / USDC trading pair. Rewards TBA.

Wormhole (Terra / Solana bridge) UST pool is live on Saber with 29% farm APY.

FATF crypto guidance looks to bring the industry in line with banks (Coindesk). After several years of draft papers and industry feedback since April 2021, the global anti-money laundering and terror financing watchdog issued guidance for people and projects that handle virtual assets.

SEC won’t approve leveraged bitcoin fund after epic BTC futures ETF (WSJ). Valkyrie Investments filed a leveraged BTC ETF application on Tuesday which was reportedly rebuked by the SEC and subsequently withdrawn at the end of the week (Blockworks).

FDIC is preparing guidance on banks and crypto (Bloomberg). The FDIC has been working with the OCC and Federal Reserve in signs of increasing federal agency coordination in order to develop and apply clear guidance to banks regarding crypto asset activities(Decrypt).

Stablecoins key part of CFPB probe into big tech (Bloomberg). CFPB Director Chopra indicated at a congressional hearing that his agency will research Big Tech plans to use native tokens and the risk of proliferation of stablecoins across social networks (read Facebook’s, ahem Meta, Diem project - WSJ).

Global market cap: $2.77T; Global market cap has increased 5% over the past week, reaching a new ATH as bullish sentiment is unwavering.

DeFi: $154B; DeFi market cap increased 2% over the past week with DeFi dominance falling 2% over the last week.

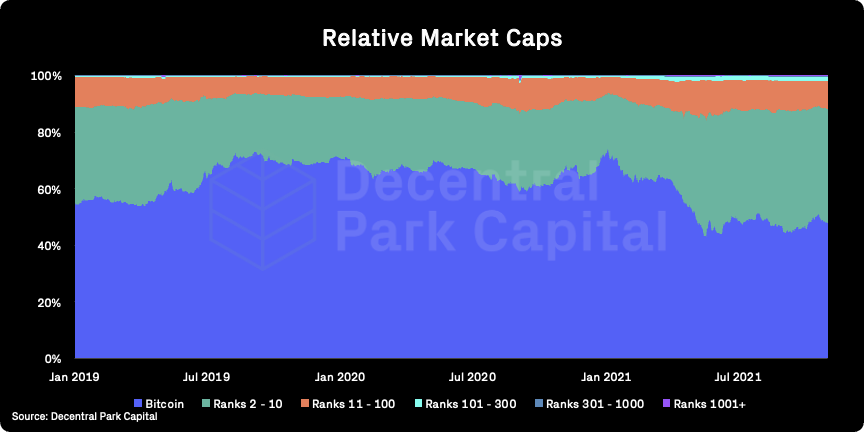

Market shares; Bitcoin dominance has fallen 1% over the past week (48%) as high cap names claw back market share.

BTC/USD

ETH/USD

ETH/BTC

Price action; BTC/USD back above $60k with $63.6 as next resistance level. Bullish ETH/BTC week (+6%) with next resistance at 0.701. ETH/USD near overbought levels but with bullish momentum slowing down (MACD).

Volatility (BTC & ETH); BTC and ETH vol has fallen over the past week. 1-month implied BTC volatility has fallen slightly from 83% to 81%.

Combined order books; Order books look slightly heavier on the ask side. Heavier resistance all the way up to $63.7k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC still largely correlated with equities. A key macro event this week will be the Federal Reserve’s policy meeting where it is expected to announce the start of its tapering of its $120B monthly bond purchases.

Expectations of sooner-than-expected rate increases continue to push short-term yields higher in recent days. Still, it is not expected that the Fed will raise interest rates until next year.

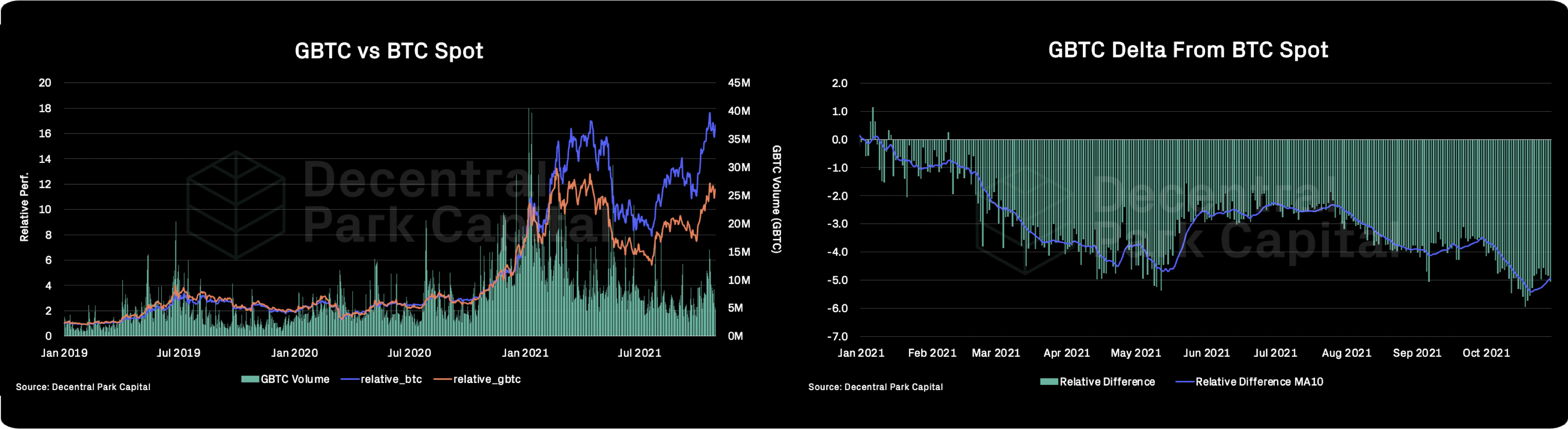

GBTC premium; GBTC outperforming vs. spot over the past week as the GBTC discount narrows from 20% to 13%. Renewed interest in GBTC likely still from DCG authorising the purchasing of up to $1B GBTC shares and speculation of the trust rotating into an ETF at some point in the future. Not clear if this represents a long-term reversal.

ETHE premium; Discount narrowed to -2.8% as ETH/USD climbed to new ATH levels. 0% discount may still be ceiling for growth with 30D ETHE secondary market volumes keeping flat over the past week (5.94M).

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains relatively low indicating low network utilization.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

On-chain real (BTC) & off-chain volume; BTC on-chain volume increased ~4% over the past week. BTC spot volumes have fallen 4% while ETH spot volumes has increased 7% for the same period (divergence).

Hashrate & Difficulty; 7D Hashrate has increased by 7% with overall miner commitment of resources is still looking healthy. Bitcoin underwent an 8% increase in mining difficulty, marking the 8th consecutive time the difficulty change has been positive.

Active addresses (BTC); Active addresses (30d MA) has increased by 1% over the past week and has been steadily increasing since late July 2021.

Trader positioning; Perpetual funding rates moderately positive for both BTC and ETH along with near ATH OI in the futures market. Risk of long liquidations still in play although Bitcoin being used as collateral has dropped from 70% to ~45%. The rise in meme coins (e.g. Shiba) may lead to growth in retail traders, adding to a near-term leverage flush out.

Omenics Sentscore (BTC); Sentiment score around BTC is kept highly positive.

Exchange inflow/outflow (BTC, ETH); Strong net outflows for BTC ($200m and $400m in net outflows respectively).Balance on exchanges has fallen by ~130k BTC and ~800k ETH since the start of October.

USD(b) supply; Total stablecoin supply has increased by 1B over the past week and now stands at over 123B. Growth for the week has been notably lower.

📚 DAO Biweekly [Paradigm]

📚 C.R.E.A.M. Exploit [BraveDeFi]

📚 Mars Protocol Deep Dive [Terra]

📚 Meme Investing [AVC]

📚 Orca Protocol Pod Primitive [OrcaProtocol]

🎙️ Skin Trader to NFT Expert [UCC]

🎙️ Blockchain Reliability [On The Brink]

🎙️ Mental Models For Web3 [Bankless]

🎙️ Sushi’s Community Raise [BlockCrunch]

🎙️ Inflation and Risk Assets [Between2Chains]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.