The Weekly #172

Leveraged traders add long liquidation risk to markets. ETH looks to take market share back from BTC with several tailwind narratives coming together near-term for the asset.

After reaching new all-time highs of $67k last week and the launch of the ProShares Bitcoin Strategy ETF, BTC has cooled off 11% dipping back below key support of $60k.

We may simply be seeing the ‘post-event’ selling by investors with concerns about the attractiveness of the ProShares ETF for retail investors and inability to track the price accurately gain momentum. More macro headwinds include a US Treasury granting the SEC authority to regulate stablecoins pegged 1:1 to fiat currency.

At the same time, ETH reached marginal ATHs of $4,361 with the asset holding up better than the orange coin for the past week (12% outperformance). As reported in previous weeklies, the launch of the BTC ETF came at a time when ETH/BTC was trading low on its RSI (~33).

Top performers in the market over the past week have continued to be L1 assets of emerging ecosystems, especially smaller cap names (+30-40%). However, if we take these L1s on their ETH ratios, we are starting to see weakness trickle in. Why? Narratives.

Ethereum now has a collection of potential narrative tailwinds in the coming weeks:

Prospects of a ETH ETF - growing demand for long-dated, OTM call options on ETH with much higher strike prices.

ETH2 Momentum - October release of the Altair upgrade to the Beacon Chain which brings several improvements for validator rewards and light clients.

Scaling - Aggregate TVL on L2 now at ATH ($4.1B) with scaling projects like Arbitrum and Optimism releasing major upgrades.

BTC’s Near-term Direction

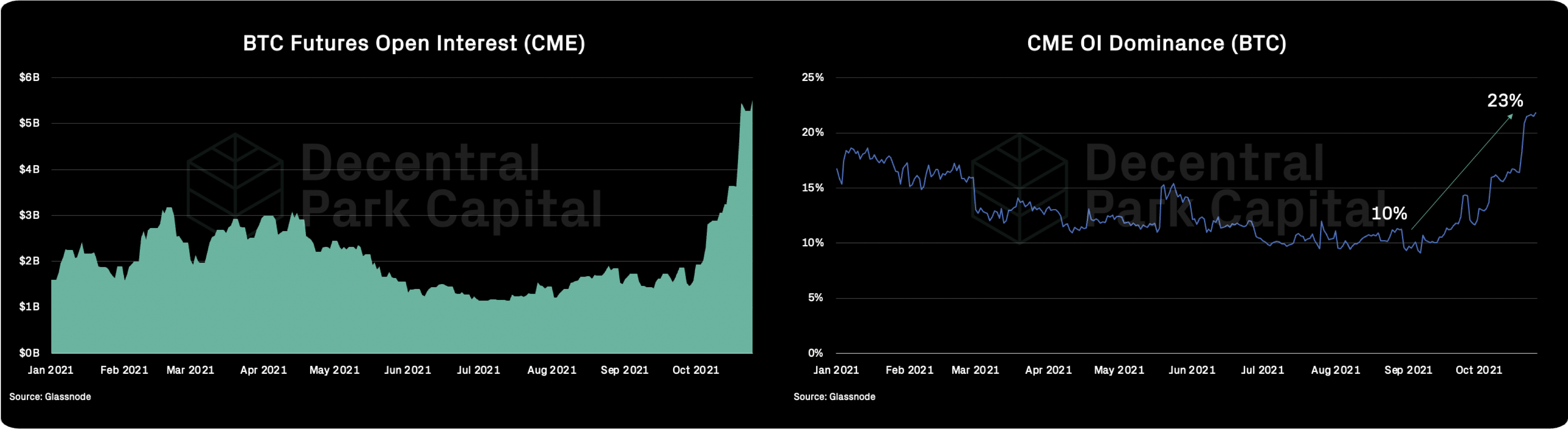

So what’s next for BTC in all of this? The futures market shows strong institutional interest with CME open interest reaching a new ATH of $5.4B. This is outpacing growth on other future exchanges with CME now accounting for over 23% of global OI (ATH).

CME volume also reached a new ATH of $7.6B - $500m more than the previous peak in Feb 2021.

Leverage longs continue to come into the market (keeping moderately positive) with levels similar to that seen in early May and September this year. At the same time, we have seen sustained periods of growing funding rates (Oct 2021 to Jan 21).

The key risk is that, with very large OI, we may see a flush out of leverage long positions risking further downside from cascading liquidations.

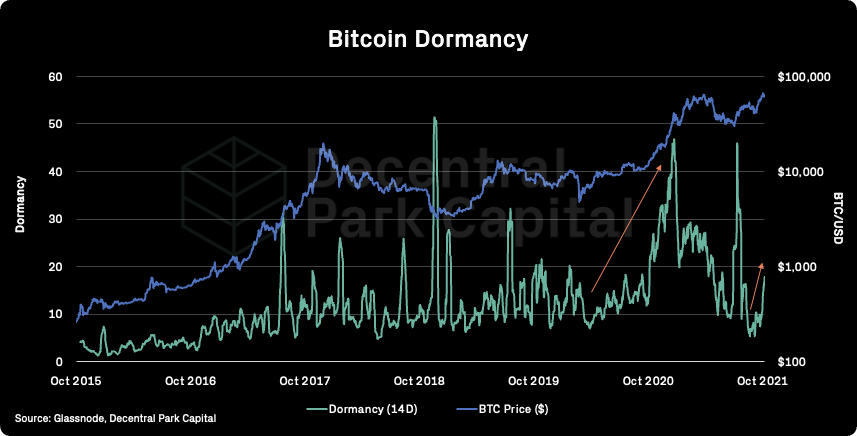

Looking on-chain paints a more bullish picture overall. Dormancy, which measures the lifespan destroyed per coin transacted has been increasing over the past week indicating older coins are being distributed. However, this appears to be only a modest increase relative to the growth seen in early 2021 as BTC topped out at $40.7k.

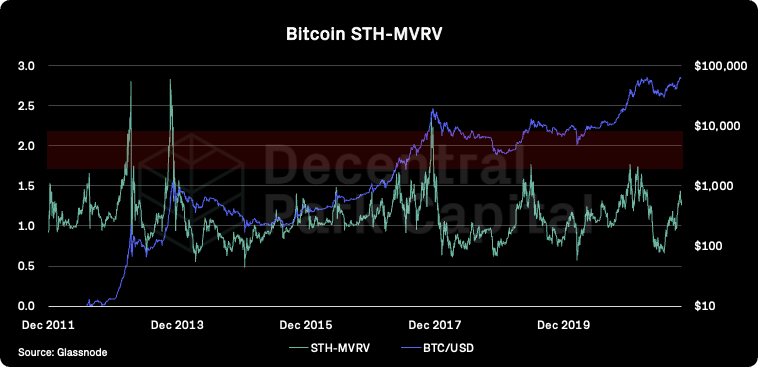

Other metrics assessing the behaviour of short-term holders like the STH-MVRV remain below levels (~1.7) that have often coincided with macro tops.

Switching over to DeFi and the market has reached new ATHs for sector market cap ($152.5B). This growth has outpaced large cap L1s like ETH (shortly after DEFIPERP/ETHUSD RSI was 30).

Key signals for sustained sector growth will be breaking above the 200d MA on the DEFIPERP/ETHUSD ratio plus DeFi dominance breaking above 3%.

Top performing assets been smaller cap L1 names and select DeFi names which have been largely catalyst/event-driven.

Global:

1inch (+100%)

Shiba Inu (+93%)

ThorChain (+78%)

Secret (+76%)

SafeMoon (60%)

DeFi:

1inch (+100%)

Frax Share (+85%)

ThorChain (+56%)

CurveDAO Token (+53%)

Aave (+40%)

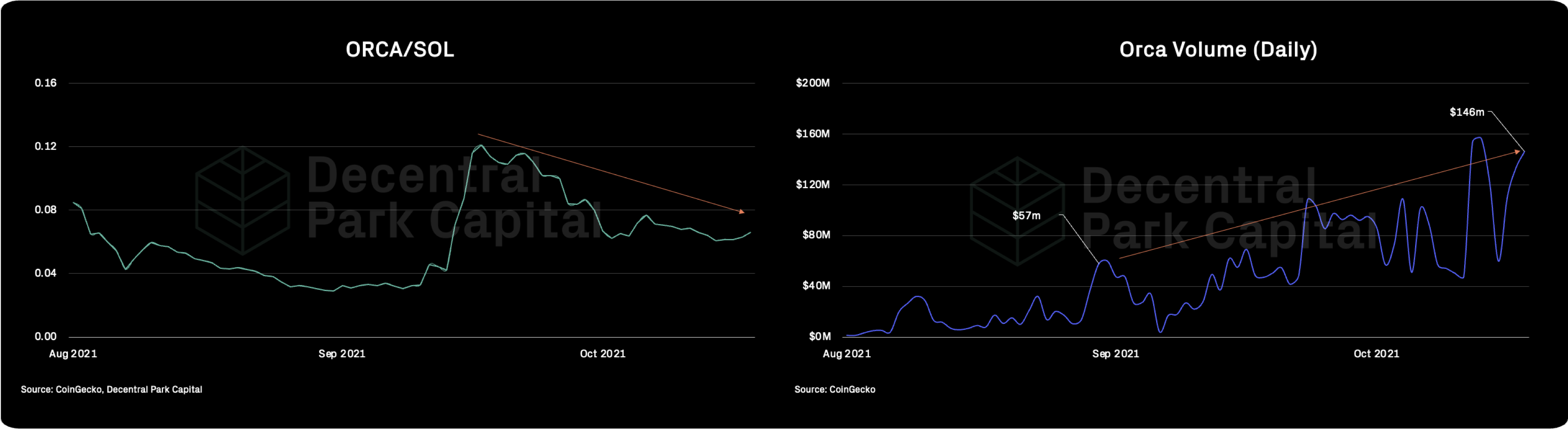

ORCA

ORCA continues to a leading AMM within the Solana ecosystem, valued 20% that of Raydium on an FDV basis. ORCA/SOL appears to be bottoming after the DEX asset lost steam relative to its L1 counterpart.

However, ORCA volume has seen consistent growth since inception rising from $50m in September to new ATHs $140M+.

FXS

The algorithmic stablecoin been an outperformer in the DeFi market with key drivers including the SEC regulating stablecoin issuers and FXS supply-side liquidity squeeze (27% of FXS supply locked for an average of 12 months).

FRAX overtook UST for the first time for its monetary supply growth (14D). FRAX had the largest percentage increase in supply relative to major issuers.

CRV

After underperforming the DeFi market throughout 2021, CRV is now in high demand due to the ongoing Curve wars. DeFi protocols are seeking to offer the highest yields for users by accumulating points in the form of veCRV (e.g. yearn, convext, stakeDAO).

This is translating to higher demand for CRV with lower liquidity on exchange (supply squeeze) with CRV exchange balance at an ATL since January 2021.

Curve's tricrypto (DAI / USDC / USDT / wBTC / WETH) pool is live on Harmony, APY with ONE LM rewards TBA.

Abracadabra now accepts SHIB as collateral to mint MIM with 6% interest and 70% LTV.

INDEX and SPELL pools are live on Bancor with single-token exposure and protection from impermanent loss. Possible BNT LM rewards TBA.

Penguin, the first layer 2 yield farm on Avalanche, joins Avalanche Rush LM program and will offer 2.5M in AVAX incentives for participating in selected liquidity pools.

Wormhole v2 (Terra - Solana bridge) UST is live on Saber with new UST / USDC pool with 31% farm APY.

Apricot Finance now supports mSOL, MNDE rewards soon to be announced.

Terra CEO served by SEC at Mainnet files lawsuit against SEC for ineffective service of process. CEO Do Kwon was served in the open by SEC enforcement attorneys, sending the crypto community abuzz during Mainnet NYC three weeks ago. The matter in question is the Mirror Protocol and synthetic stocks that reference registered securities.

NY Attorney General petitions two lending firms to shut down operations in New York state with focus on lenders continuing to escalate. Two firms were issued cease and desist orders to shut down in-state activities in 10 days as lending platforms continue to receive state and federal scrutiny.

Global financial watchdog will issue updated crypto regulatory proposals next week. The Financial Action Task Force (FATF) will issue new risk-based virtual asset guidance that will focus on the Travel Rule and exchange disclosures. Global regulatory regimes often adopt FATF recommendations as law, with the US traditionally not doing so but shifting its approach in recent months.

Global market cap: $2.58T; Global market cap has stayed flat over the past week.

DeFi: $145B; DeFi market cap increased 7% over the past week with DeFi dominance increasing 8% over the same period (1.85%).

Market shares; Bitcoin dominance has decrease by 6% over the past week (47.8%) as BTC sells off harder than other high cap names since its ATH.

BTC/USD

ETH/USD

ETH/BTC

Price action; BTC/USD cooling off from overbought levels (ATH) MACD crossing below signal line suggesting bearish momentum strengthening. ETH/BTC strengthening (MACD) with RSI still below overbought levels.

Volatility (BTC & ETH); BTC vol has stayed flat while ETH has fallen over the past week. ETH 3M implied vol has increased over the past week (115%).

Combined order books; Order books look slightly heavier on the bid side. Heavier resistance all the way up to $60k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC becoming more correlated to other risk-on markets like equities. Earnings season continue to fuel risk appetite with Tesla beating gross margin expectations, surpassing $900 for the first time. Yields on short-term government bonds rose to highest levels since March 2020, a sign of investors starting to bet about global rate hikes.

GBTC premium; GBTC still underperforming vs. spot. GBTC discount at 15.4%. Notable narrowing of discount likely due to increased demand from DCG purchasing $388m of GBTC shares and speculation of the trust rotating into an ETF at some point in the future.

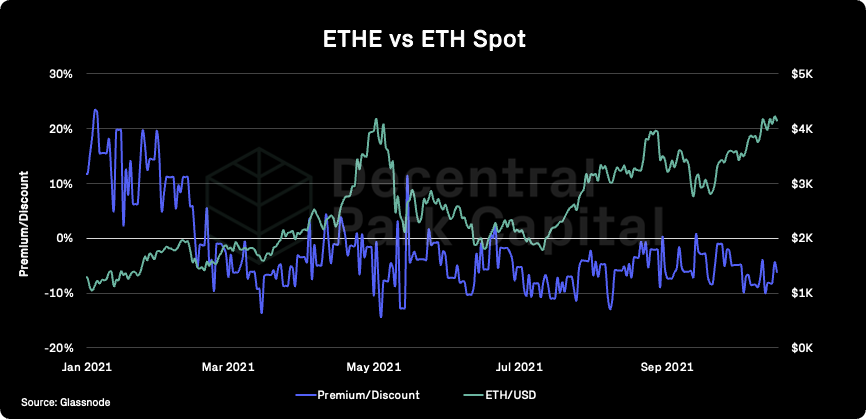

ETHE premium; Discount at -6%. Stronger evidence of ETHE discount floor at 10%. 30D ETHE secondary market volumes have been flat over the past week (5.94M).

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains relatively low indicating low network utilization.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

On-chain real (BTC) & off-chain volume; BTC on-chain volume decreased ~1% over the past week. BTC spot volumes have fallen 16% while ETH spot volumes has increased 8% for the same period (divergence).

Hashrate & Difficulty; 7D Hashrate has increased by 7% with overall miner commitment of resources is still looking healthy. Next difficulty adjustment estimate is +4% due to increase commitment.

Active addresses (BTC); Active addresses (30d MA) has increased by 2% over the past week but still ~18% lower than ATHs seen during Q1 2021.

Trader positioning; Perpetual funding rates moderately positive for both BTC and ETH with ATH levels of OI and volume. Flush out of leveraged longs still in play. Hedge funds continue to increase exposure ($2B) to arbitrage shorts with long-spot exposure being needed more to hedge risk maintain these positions.

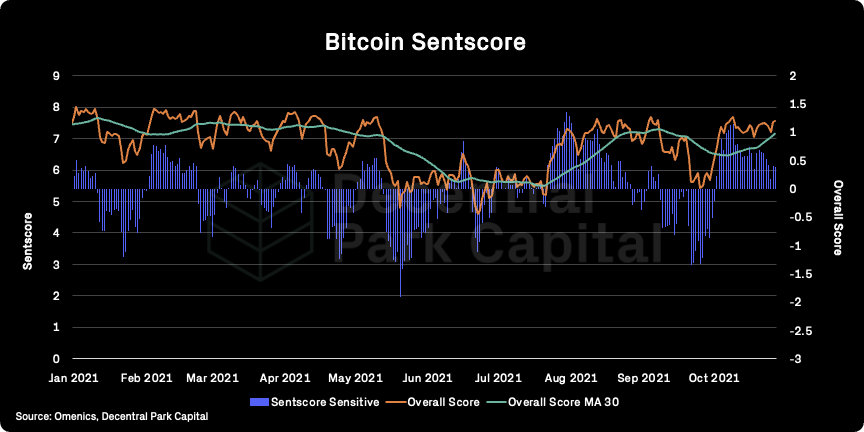

Omenics Sentscore (BTC); Sentiment score around BTC is kept highly positive although sensitive score has been falling in line with weakening price as the asset breaks below $60k.

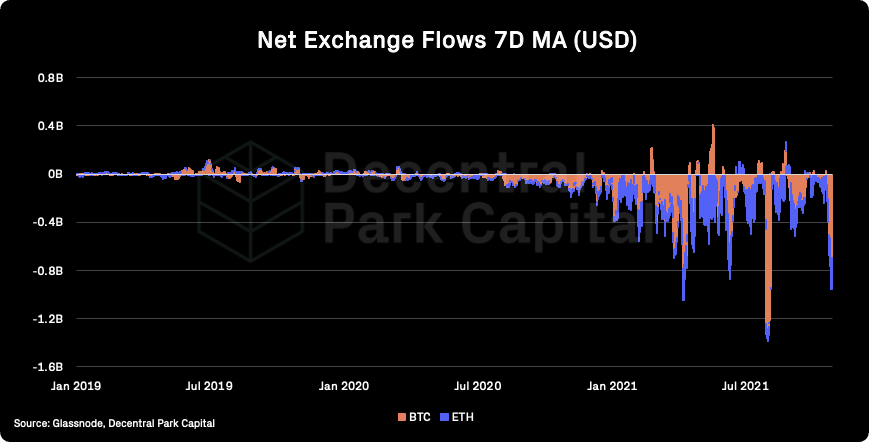

Exchange inflow/outflow (BTC, ETH); High net outflows for BTC (-50k) and ETH (-400k) over the past week potentially creating a potential supply liquidity crisis for buyers.

Balance on exchanges is at ATL since July 2018 and November 2018 for BTC and ETH respectively.

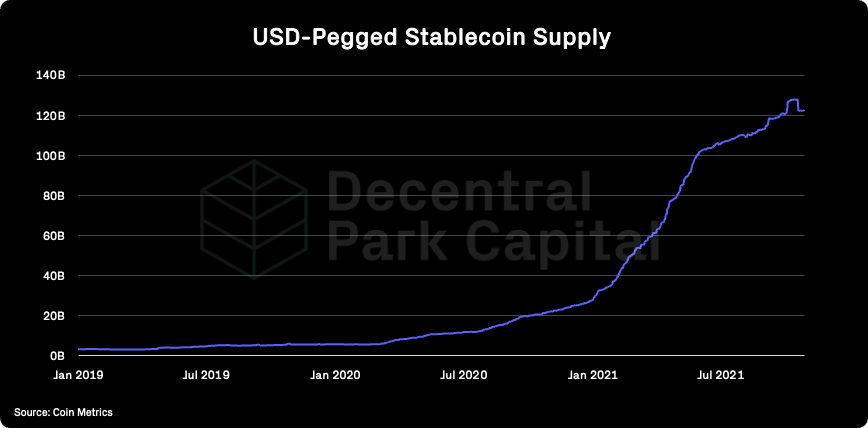

USD(b) supply; Total stablecoin supply has increased by 1B over the past week and now stands at over 123B. Growth for the week has been notably lower.

📚 Bitcoin Bankathon [CityAM]

📚 ETHLisbon Projects [Calvin Chu]

📚 Indexing The Creator Economy [Stripe]

📚 Orca Roadmap [Orca]

📚 OHM-ETH Bonds [ohmzeus]

🎙️ Stabilzing The Grid With Bitcoin Mining [On The Other Side]

🎙️ Index Funds, ETFs,& The Passive Investing Revolution [Hidden Forces]

🎙️ Ultra Scalable Ethereum [Bankless]

🎙️ Terra Autumns #5 [Delphi]

🎙️ Future of Decentralized Fundraising [Protocol 432]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.