The Weekly #171

The Weekly #171

Speculation around an imminent futures-based BTC ETF drives record high futures and options open interest. Technical indicators signal pullback while key on-chain metrics stay bullish.

All Hail The BTC ETF

The main headline in the crypto markets for the week was the upcoming launch of a futures-based Bitcoin exchange-traded fund in the U.S. ProShares’ Bitcoin Strategy ETF is expected to start trading tomorrow.

The prospect of a Bitcoin ETF launch has been priced in, with BTC climbing to a local high of $62.3k and managing to stay above the key $60k level for now. BTC is currently trading at $61.4k.

One of the more common takes for near-term price action is ‘buy the rumour, sell the news’. The market is heavily pricing in the launch but questions marks remain on the attractiveness of a futures-based ETF product given low retail understanding and inefficiencies (e.g. contango).

The technical signals align with this take with the daily RSI in clear overbought territory.

At the same time, a futures-based ETF can requally create a stronger demand for BTC spot with revived interest in the cash & carry trade.

The clear demand for BTC can be attributed to both spot and futures market. Daily spot volume has increased 50%+ over the past two weeks to $15.3B.

However, the leading source of price discovery is arguably the futures market, specifically institutions. Futures OI has increased to $10B since September lows (+100%) with CME seeing record highs in OI ($3.6B) signalling increased institutional participation.

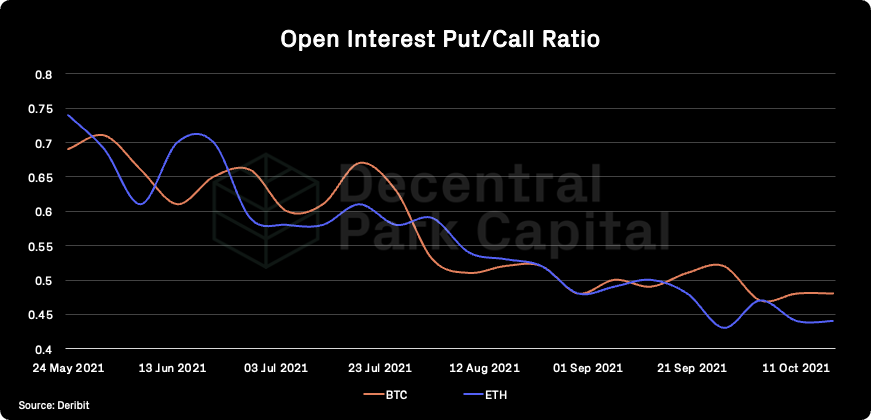

Similarly, Bitcoin options OI has surged to near ATHs, increasing $6B (+100%) since September lows. The last time we saw similar interest was when BTC was rallying to its ATH price. Options volume hit a high of $3.3B last week when a BTC ETF approval hit headlines.

This increase in demand is clearly from the bulls. For futures, the perpetual funding rate has hit 0.028% - bullish levels not seen since mid-May this year. Traders are also favouring options strike prices above $100k.

The risk here is increased volatility from long liquidations if BTC sells of as the ETF launches.

We can also look to on-chain to evaluate the potential price action near-term. BTC MVRV ratio, a good macro indicator for market tops and bottom, is still far below the ‘top’ zone of 7 and above. Every time the MVRV ratio passed 3, BTC has historically rallied for the subsequent 1-2 months.

Adjusting for short-term holders, and more likely sellers in the coming days, an ATH-MVRV also points to a bullish near-term outlook with the ratio still below 1.7 ‘top’ zone at 1.3 (but fast approaching those levels). Short-term holders are not at levels where they take profit.

The imminent launch of a spot-based ETF (without contango risk) could fuel this next run with the futures-based ETF being the first process of fuelling a “regulated market of signifiant size”.

DeFi

The focus of BTC and large cap names has been at the expense of the DeFi sector (once again). DeFi has been in a consolidation patter for a month but on a ETH/USD ratio is at a yearly low and remains an attractive capital rotation play.

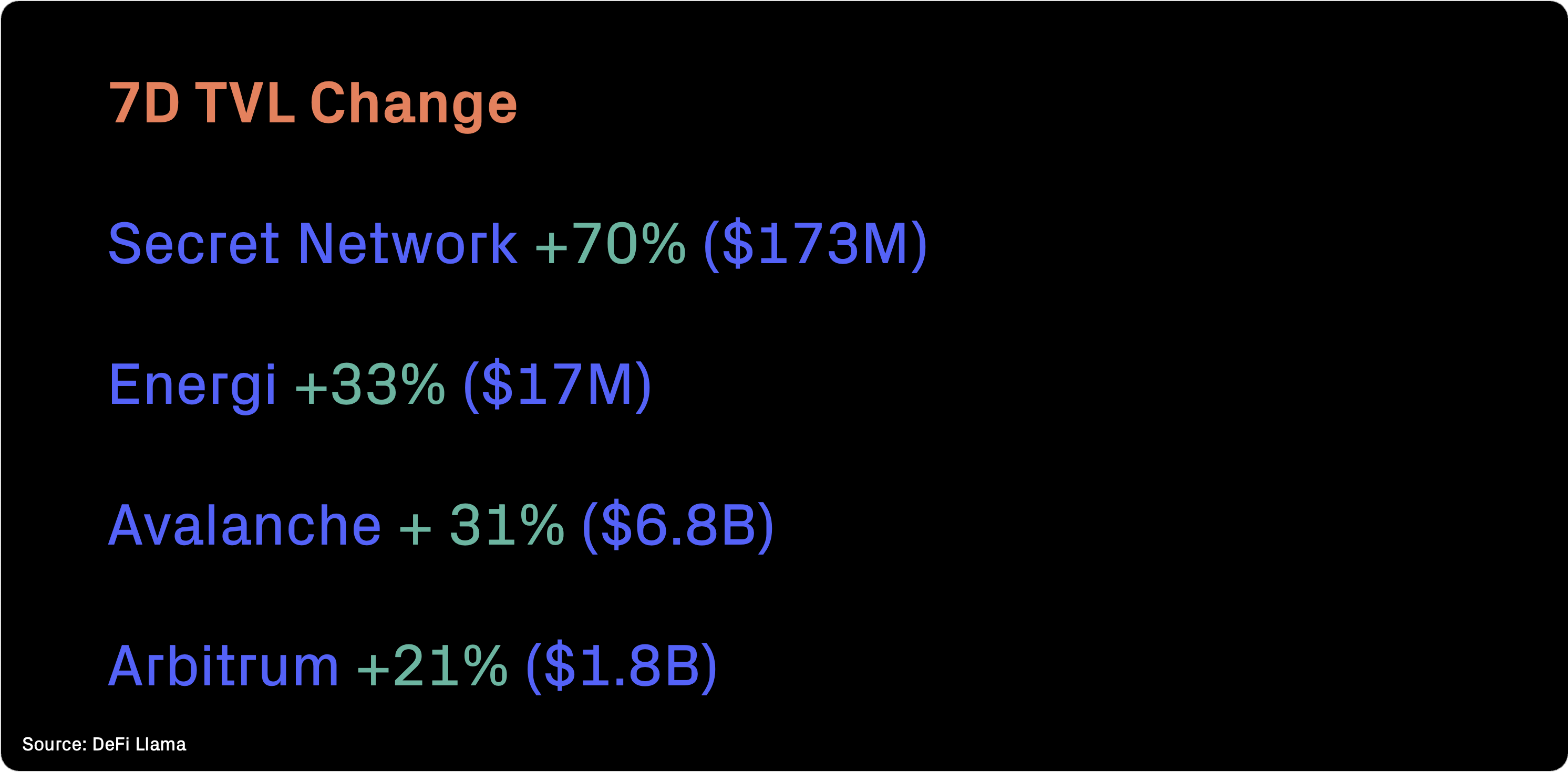

The sector continues to print new ATHs including overall TVL reaching $223B and TVL across L2s climbing to $3.8B. This growth has been the result of both asset appreciation and effective liquidity inventive programmes by alternative L1s/L2s to Ethereum.

The value of the sector also increases with higher asset prices and services like lending become more liquid and useful (reflexive).

Ecosystems that have seen notable percentage changes in their TVL have been a mixture of alternative L1s and Ethereum L2s. Avalanche leads by dollar amount, adding $1.5B thanks to its LM programmes for flagship projects like Trader Joe.

Algo Stablecoin On The Rise

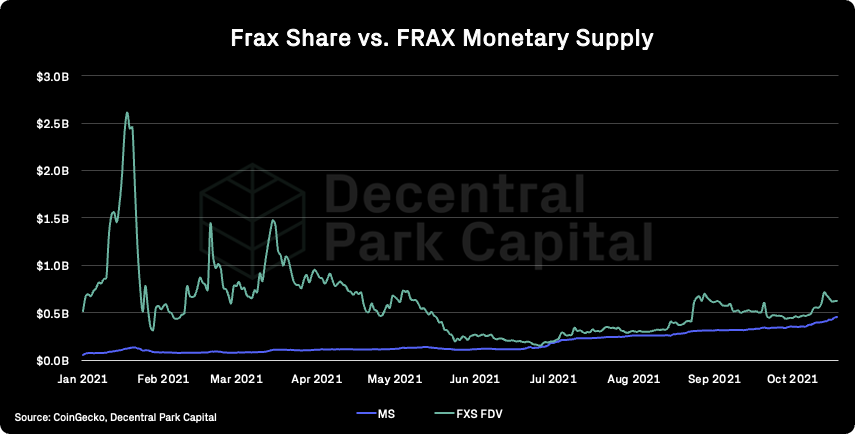

As centralized stablecoin issuers like Tether receive the heat from regulators, the market for algorithmic-based stablecoins is growing. UST and FRAX lead the pack with both seeing 2.5B and 400m YTD growth respectively.

FRAX, the partially collateralized stablecoin, has maintained a tighter peg than Terra’s UST over 2021.

The key thing here is that stablecoin growth informs the valuation of the governance assets (e.g. FRAX Shares). The monetary supply may act as a valuation floor for those assets with networks like Frax showing this relationship to date.

Top performing assets have been largely event-driven with highlights including Polkadot launching parachains, Binance’s ecosystem fund announcement, the imminent launch of Arbitrum Nitro, and Polygon’s Korean CEX listing.

Global:

Polkadot (+22%)

Polygon (+21%)

Stacks (+18%)

Dogecoin (+17%)

Binance Coin (16%)

DeFi:

Keep Network (+108%)

KeeperDAO (+80%)

MCDEX (+55%)

Planet Finance (+47%)

Alchemix (+43%)

REN (-37% U/O)

REN maintains its undervaluation level from last week with the assets yet to re-rate from its fundamentals. TVL for RenVM at ATH ($1.6B) with the network benefiting of the current BTC rally.

Near-term BTC sell off will impact fair value estimate unless the protocol sees significant inflows of BTC.

AAVE (-70% U/O)

AAVE is at a new ATL on its U/O index (oversold relative to fundamentals). Aave market size on Avalanche is now bigger than that of Polygon ($4.1B) showing how long-standing Ethereum dApps can potentially lead the market in alternative EVM ecosystems over new (natively-born) entrants.

Upcoming catalysts include Aave ARC, its permissioned pool product, which is slated to launch by month end.

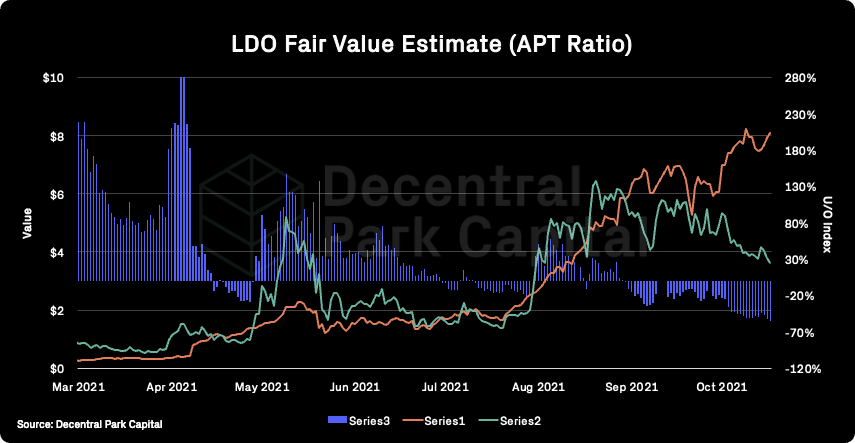

LDO (-55% U/O)

LDO continues to diverge away from strengthening fundamentals, printing a new ATL on its U/O index. A total of 1.3m ETH is now staked via Lido with TVL being boosted by $2.2B LUNA and $150m SOL staked on their respective network.

Balancer launched new Tracer's TCR / ETH pool on Arbitrum with 1000 BAL/week LM rewards. Current APY is 92%.

Futureswap V4 beta is live on Arbitrum, more details is here. LPs can add liquidity to ETH / USDC pools for 237% APY including FST rewards.

Curve is live on Harmony network with 3pool (DAI / USDC / USDT). Harmony is providing $2 million in ONE tokens as LM rewards, boosting current APY up to 11%.

Tesseract Finance, yield farming protocol originated from YFI Combinator, is live on Polygon with USDC, DAI, WBTC and WETH vaults (currently capped at 1M$).

Raydium launched several new Marinade Finance Fusion pools with MNDE rewards: BTC / mSOL, ETH / mSOL, mSOL / USDT and MNDE / mSOL. All MNDE reward options can be found here.

Stablecoin enforcement actions emerge as CFTC slaps Tether (and sibling Bitfinex) on the wrist with $42.5M in fines on allegations that its USDT stablecoin was not fully backed by reserves during 2016-2018 and that assets were commingled and not in cash.

Putin chimes in on the regulatory debate stating crypto “has the right to exist” in an interview with CNBC. Putin signals tolerance for crypto in recent comments: noting that cryptocurrency “has the right to exist and can be used as a means of payment” but is not yet ready for commodity trading as a reserve currency.

Coinbase and Andreessen Horowitz separately issue proposals for regulating crypto amid a major industry lobbying push. Coinbase CEO Brian Armstrong pens Wall Street Journal OpEd introducing the Digital Asset Policy Proposal: Safeguarding America’s Financial Leadership that calls for a crypto-specific regulator and new rules. Venture capital titan Andreessen Horowitz simultaneously issues a vision of regulation. Both are expected to continue strong lobbying efforts on Capitol Hill in coming weeks.

Decentralized finance protocols continue education efforts with federal lawmakers and regulators. Uniswap Labs hires a former Obama spokesman as communications chief. Other incumbents are ramping up lobbying efforts, with MakerDAO sending a delegate to lead the education charge with lawmakers.

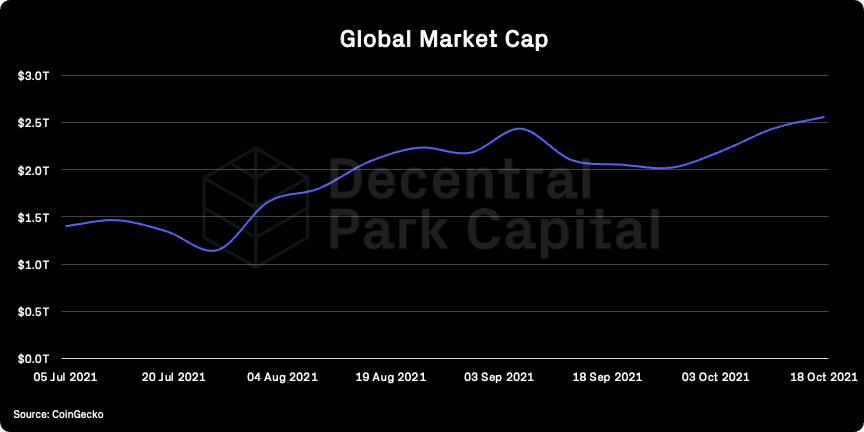

Global market cap: $2.54T; Global market cap has increased by 5% for the week.

DeFi: $135B; DeFi market cap increased 3% over the last week. DeFi dominance has stayed flat over the past week but at an ATL since January 2021.

Market shares; Bitcoin dominance has increased over the past week (50.1%) with the asset being an outperformer for the period.

BTC/USD

ETH/USD

ETH/BTC

Price action; Strong BTC/USD performance over past week with daily RSI in overbought territory and facing resistance at $63k. ETH/USD facing resistance at $4k. Bearish ETH/BTC price action with next support level at 0.0598 and daily RSI falling to oversold levels.

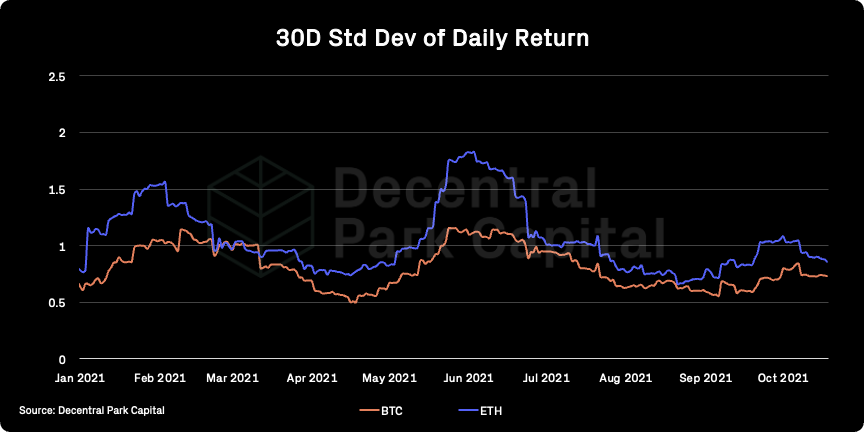

Volatility (BTC & ETH); ETH vol. has stayed flat in recent days while BTC vol. has increased slightly. 1M and 3M realized Ethereum-Bitcoin volatility spread dropped to yearly lows (15%), indicating Bitcoin having higher chance of moving faster through the charts.

Combined order books; Order books look heavier on the ask side. Heavier resistance all the way up to $65k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC and the wider crypto market becoming more correlated to other risk-on markets, such as equities (0.4). Banks posted better than expected results last week with JP Morgan seeing its profits increase 24% and the steepening of the yield curve boding well for US banks.

Disappointing US job growth will unlikely change the Fed’s tapering timeline but analysts predict that this additional uncertainty will bring further volatility over the coming weeks.

GBTC premium; GBTC still underperforming vs. spot. GBTC discount still widening overall. Futures-based ETF on the horizon reducing attractiveness for arbitragers to step in. Prospect of spot-based ETF will be the key catalyst for discount narrowing.

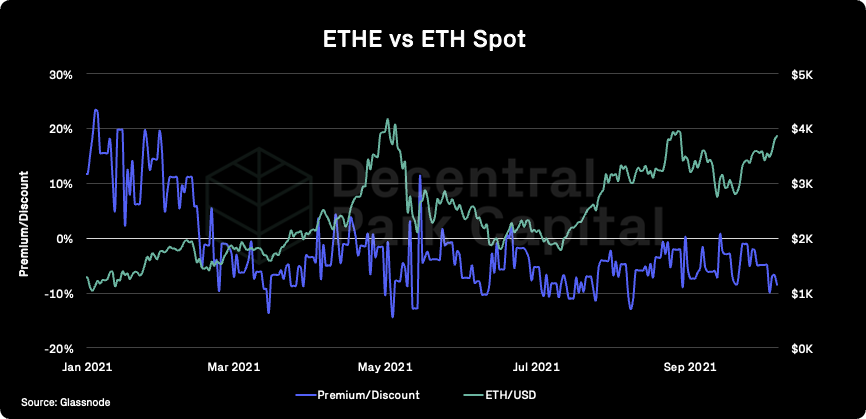

ETHE premium; Discount at -8%. ETHE discount widening along with GBTC despite spot also hovering close to ATH levels. 30D average ETHE volumes falling 10% over the last 2 weeks indicating weakening secondary market demand.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has fallen slightly over the past week indicating lower network utilization.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

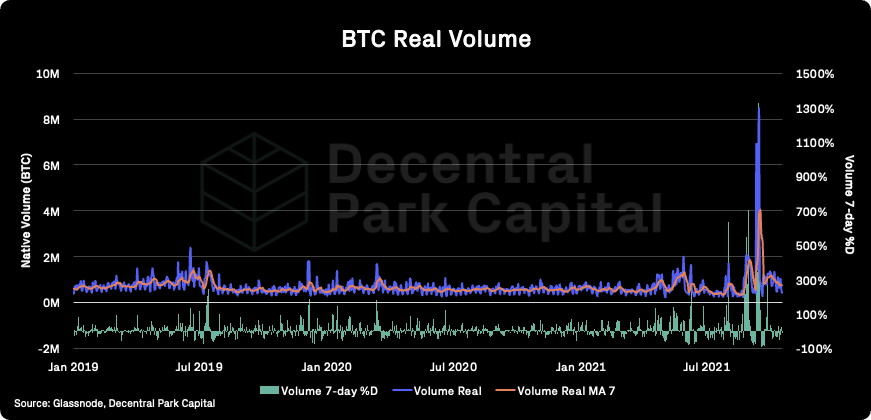

On-chain real (BTC) & off-chain volume; BTC on-chain volume decreased ~11% over the past week. BTC spot volumes have increased 35% while ETH spot volumes has increased 28% for the same period.

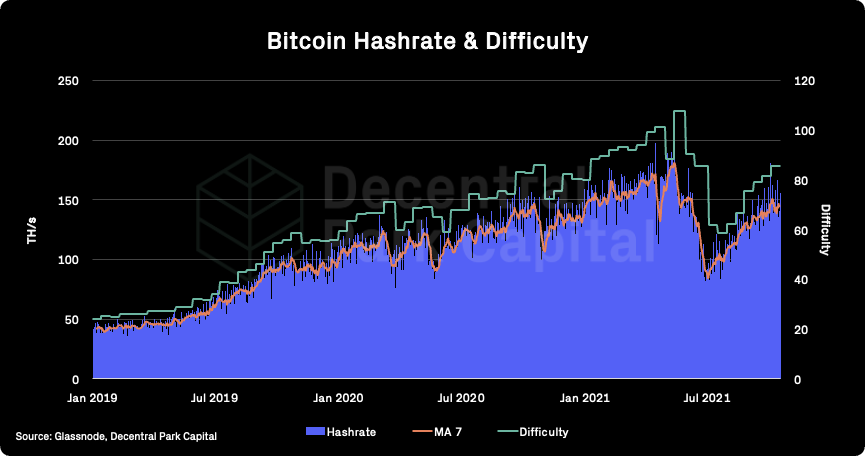

Hashrate & Difficulty; Hashrate has increased by 1% (7d MA) but overall miner commitment of resources is still looking healthy as reflected in Bitcoin having six consecutive upwards difficulty adjustments.

Active addresses (BTC); Active addresses (30d MA) has increased by 1% over the past week and is still ~20% lower than ATHs seen during Q1 2021 despite strong spot action.

Trader positioning; Perpetual funding rates increasing along with OI and volume for both BTC and ETH indicating bullish trader positioning and increased leverage in the market.

Hedge funds continue to increase exposure to arbitrage shorts with long-spot exposure being needed more to hedge risk maintain these positions.

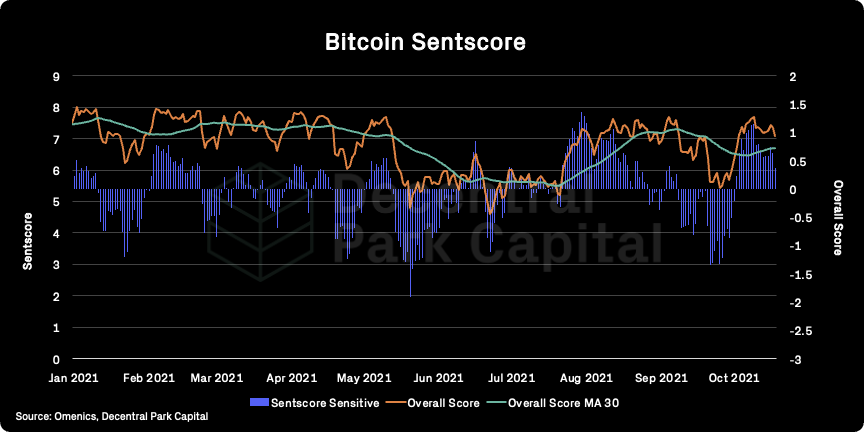

Omenics Sentscore (BTC); Unsurprisingly sentiment around BTC continues to be at yearly highs.

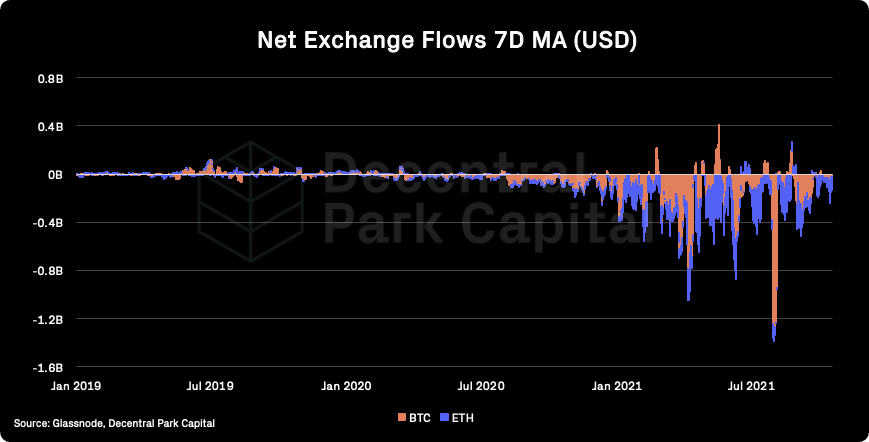

Exchange inflow/outflow (BTC, ETH); ETH continues to see minor net outflows from exchanges while BTC seeing equal amounts of inflows to outflows.

USD(b) supply; Total stablecoin supply has increased by 1B over the past week and now stands at over 128B. Growth for the week has been notably lower.

📚 Our Network #93 [Spencer Noon]

📚 Digital Asset Policy Proposal: Safeguarding America’s Financial Leadership [Coinbase]

📚 MakerDAO Incoporation and Taxes [The Defiant]

📚 Matter Labs AMA [Reddit]

📚 Governance Mining — liquidity mining for human capital [Jacob Phillips]

🎙️ DAO Social Dynamics [On The Other Side]

🎙️ On Maximalism, Decentralization, and Investing [UpOnly]

🎙️ Forward With Crypto | Andrew Yang [Bankless]

🎙️ Dan Tapiero On Crypto Unicorns [The Scoop]

🎙️ How The Crypto Industry Thinks It Should Be Regulated [The Breakdown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.