The Weekly #170

Several factors drive renewed interest in Bitcoin, pushing the asset into overbought territory. Ethereum will look to claw back its market share leading up to the Altair upgrade and ETH2 merge.

Bitcoin Leads The Charge

Crypto markets have started Q4 in true bullish fashion with the global market cap reaching 2.4T - up 6% over the week. Bitcoin performed strongly with the asset surpassing the $1T mark again while breaking key resistance of $50k.

One can point to a number of factors that have brought fresh momentum behind the orange coin. These include: the likely launch of BTC futures-based ETFs, the launch of Bitcoin ‘lite’ equity ETFs, potential bitcoin whale purchases, ATHs for lightning network metrics, rising inflation concerns, and fading regulatory worries.

What’s more impressive is Bitcoin’s correlation to the S&P 500 has also fallen to 0.12 - the lowest since late July 2021. This weakening relationship comes at a time when Bitcoin is strong while equities are relative weak. Stock futures point to a lower start on Wall Street.

The crypto market anticipated the start of “Uptober” and were no disappointed. Historically, September has been the worst months while October has been one of the strongest.

Looking on-chain, key macro market indicators like the MVRV ratio point to neutrality in exchange price relative to “fair value”. For example, the long-term MVRV (which only considers UTXOs of more than 155 days) is far below the red zone which has historically coincided with market tops, despite BTC looking to test new ATH in price.

Short-term MVRV paints a similar picture albeit with a shorter range - a move above ~1.4 could signal when we see pressure from short-term holders.

With so many tailwinds for Bitcoin, investors are wondering where the puck will go over the coming weeks. After impressive performance for alternative L1s, we are now seeing capital rotation back to ETH.

Ethereum continues to get fundamentally stronger for becoming a decentralized financial layer with 27.7% of the ETH supply now held in smart contracts (ATH).

Ethereum’s Q4 catalysts are clear:

L2 scaling - making Ethereum more performant relative to Alt L1s

The ETH2 merge - Altair upgrade (low stakes-warm) set to go live on October 27th (Epoch 74240). The merge is expected to occur by May 2022.

DeFi, NFTs, and gaming cryptoassets remain oversold relative to fundamentals, the beneficiaries of more performant foundations, and a good target for capital rotation. At the same time, emergent ecosystems seeing continued growth in TVL and dApp deployment will still stay very relevant heading into this quarter.

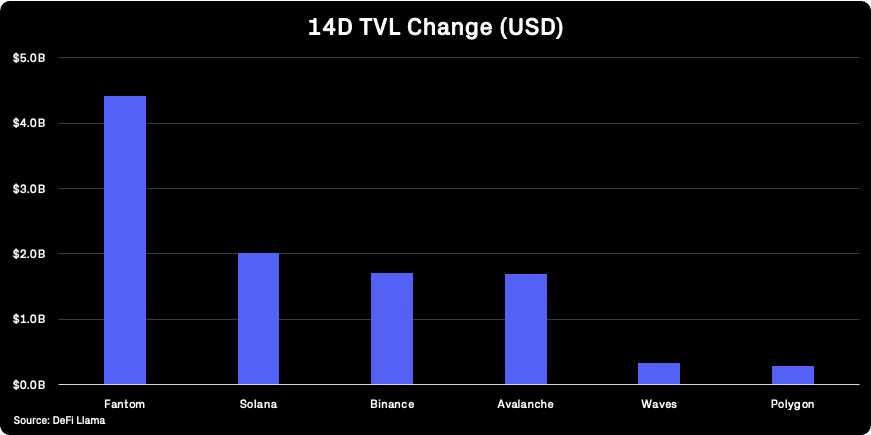

Analyzing the TVL growth of major blockchains and L2s, Fantom has been the fastest growing (+$4.3B). Key drivers of growth are incentives with Geist Finance (an Aave fork) giving away strong LP rewards.

More nascent alternative L1s like Avalanche continue to show a meteoric rise in nominal terms but the strongest growth here is still largely Ethereum-centric.

Long-established DeFi protocols are benefiting from more scalable foundations outside of Ethereum. An example is Aave which has its 2nd largest market on Avalanche overtaking Polygon’s ($3.6B).

We are also seeing native TVL growth on Ethereum L2s. Lyra, a decentralized options protocol built on Synthetix and Optimism has already reached $8m and has the highest TVL growth in percentage terms over the week (+1081%). Overall, the strongest growth in DeFi is still largely EVM-centric.

Top performing assets are in many cases fundamentally-driven (e.g. TVL growth). DeFi top performers are all low-cap names with coin ranks ranging anywhere from 24-98.

Global:

Shiba Inu (+221%)

Bitcoin Cash ABC (+71%)

Stacks (+57%)

Fantom (+44%)

Klaytn (42%)

DeFi:

SPELL (+205%)

ICE (+191%)

STP Network (+125%)

TIME (+87%)

AQUA (+80%)

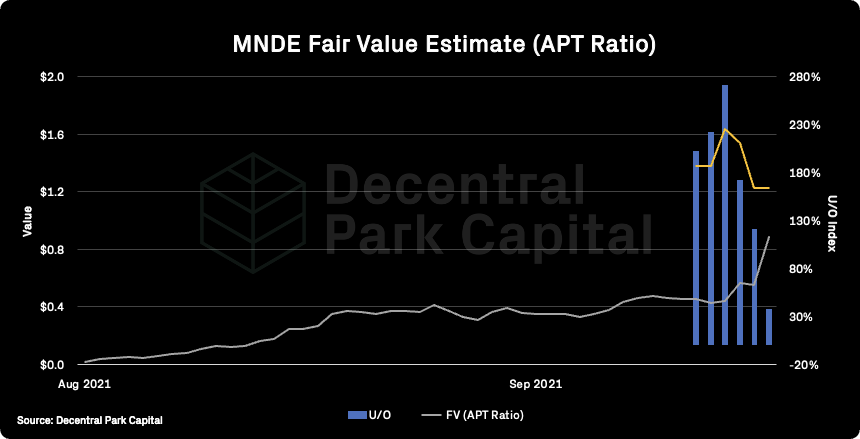

MNDE (30% U/O)

Marinade Finance now has over $890m in TVL with recent growth throttled by the launch of the MNDE token and its respective incentive programmes. Marinade still dominates over Lido for SOL staking, possibly due to Marinade being a Solana-native integration.

REN (-33% U/O)

With BTC’s strong performance, DeFi assets with large amounts of BTC supplied to them stand to benefit. An example is Ren which is printing new ATH for TVL ($1.5B) with REN yet to reflect this recent growth. renBTC supply growth is now outpacing WBTC as RenVM capitalizes on emerging chain markets.

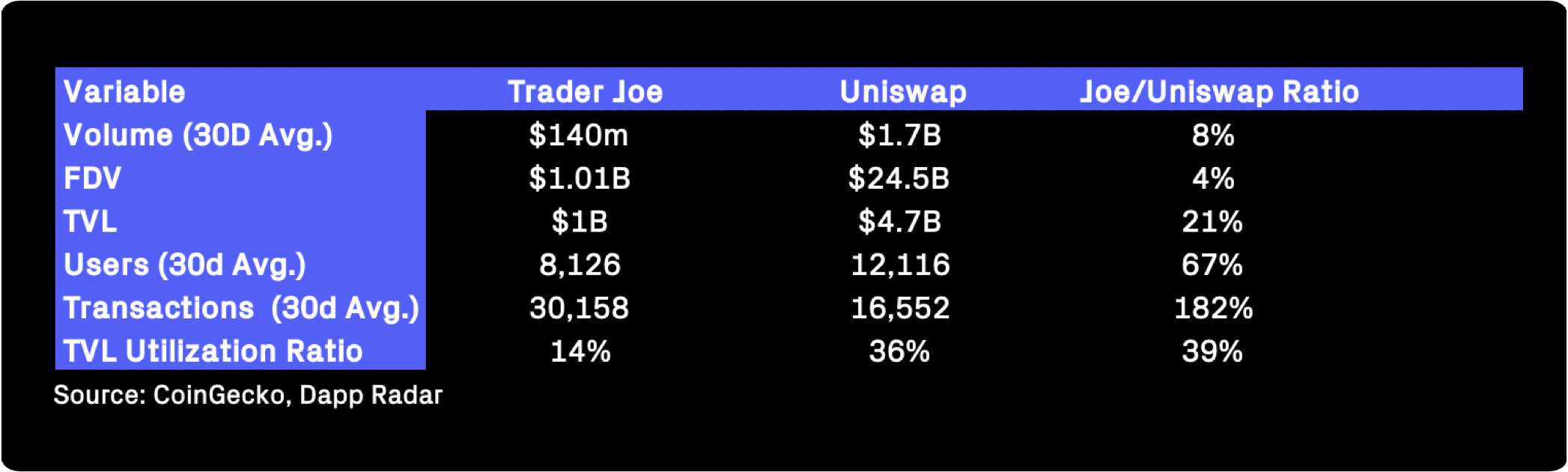

JOE

The Avalanche AMM continues to see daily trade volume above $200m. Trader Joe has seen impressive liquidity contribution to date with volumes now representing ~8% that of Uniswap. Trader does fall behind Uniswap for efficiency (TVL utilization).

ANC (-16%)

Anchor has benefited from LUNA price appreciation and bETH stakers on Lido. Nearly 95k ETH (stETH) is now bonded via Anchor protocol which has contributed to a further ~$340m in TVL.

Anchor’s stETH integration enables holders increased yield opportunities as well diversifies Anchor’s asset bucket, improving the protocol’s sustainability long-term.

Aave is live on Avalanche network, lenders and borrowers are rewarded with wAVAX tokens. Current APY for depositing ETH, USDT and BTC is 4.3%, 10.9% and 5.6% respectively.

BENQI, an algorithmic liquidity market protocol on Avalanche, has updated wAVAX incentives. APY for supplying ETH, USDT and BTC is 1.4%, 16.6% and 4.6% respectively

Jet Protocol is live on Solana, LPs can supply SOLs for 1.10%, rewards TBA.

Fei protocol updated to v2, see the list of changes here. LPs can stake Aave Variable Debt FEI for 19.8% APY.

Curve is live on Avalanche, APY for staking in aDAI / aUSDC/ aUSDT pool is 23% (mostly wAVAX rewards).

Marinade Finance's MNDE token is live, mSOL LPs (Orca, Raydium, Saber, Port, Larix pools) can participate in liquidity mining program.

FTX is rumored to be setting up the blockchain industry’s largest Political Action Committee (PAC) in the US in a show of force for the global crypto community. Sam Bankman-Fried is rumored to be hiring a political director for what will be the largest cryptocurrency focused PAC, larger than incumbent HODL Pac.

Ranking member of the US House Financial Services Committee introduces a bill that institutes safe harbor for token issuers. This week, Congressman Patrick McHenry introduced the Clarity for Digital Tokens Act of 2021 that would put into law pro-crypto SEC Commissioner Hester Peirce’s 3-year safe harbor for tokens and associated teams to decentralize and register as securities.

Bank of England: “Crypto asset markets continue to grow rapidly, but currently pose limited risk to UK financial stability.” In what is being interpreted as bullish sentiment, the Financial Policy Committee (FPC) of the Bank of England (BoE) takes a different tone to its sister organization in the US. This coincides with a warning from the FCA to social media platforms against advertisement tied to fraudulent crypto products as consumer protection rhetoric starts to mount.

Russian regulators aim to regulate and limit exchange of crypto assets as authorities focus on consumer protection. “A number of websites providing options to exchange, cash out, and transfer cryptocurrency using various payment methods may be blocked by Russia’s telecom regulator, Roskomnadzor, if their operators don’t delete the illegal web pages.

Global market cap: $2.4T; Global market cap has increased by 6% for the week.

DeFi: $130B; DeFi market cap increased 2% over the last week. DeFi dominance has fallen by 15% over the same period - the largest weekly decline since July 2021.

Market shares; Bitcoin dominance has increased over the past week (49%) with a number of L1 assets losing steam on their BTC ratios.

BTC/USD

ETH/USD

ETH/BTC

Price action; Strong BTC/USD performance over past week with RSI approaching overbought territory. Volume relatively low still. ETH/USD facing resistance at $3.6k ETH/BTC underperformance with support found on the 200d MA and RSI at 32.

Volatility (BTC & ETH); ETH vol. has stayed flat in recent days while BTC vol. has increased slightly.

Combined order books; Order books look heavier on the ask side. Heavier resistance all the way up to $57.9k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC and the wider crypto market diverging from other risk-on markets. Equity futures taking a hit as economic growth forecasts are cut.

Poor jobs report released last Friday showed only 194,000 jobs in September were added. However, it is perfectly possible there is enough recovery in the jobs market for the Fed’s tapering to start next month.

Analysts are estimating earnings growth rate of 27.6% for the S&P 500 in Q3 which would be the 3rd highest growth rate since 2010 and perhaps counteracts concerns of lower attractiveness of equities vs rising bond yields.

GBTC premium; GBTC still underperforming vs. spot. GBTC discount reached a near ATL of 18.6% last week as the prospect of futures-based BTC ETFs become more likely. BlockFi filed to offer a Bitcoin futures ETF last Friday.

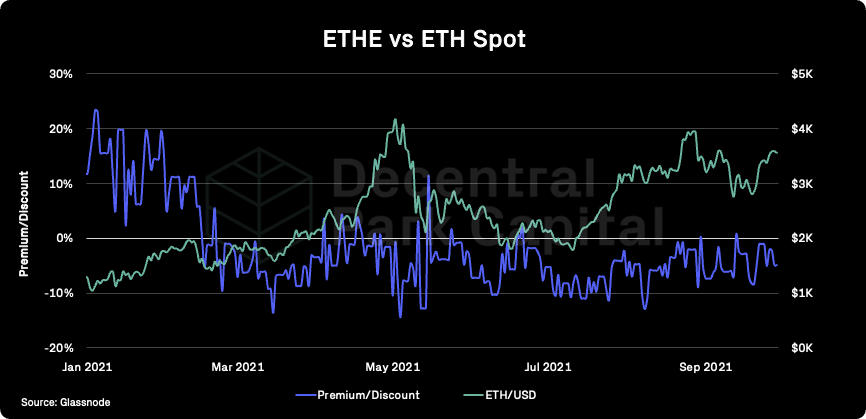

ETHE premium; Discount at -4.8%. ETHE has yet to print a sustained premium but has been posting higher lows since August 2021. ETHE 30D volume have kept flat over the past week indicating muted interest on the secondary market.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has increased moderately indicating higher network utilization.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

On-chain real (BTC) & off-chain volume; BTC on-chain volume decreased ~15% over the past week. BTC spot volumes have increased 14% while ETH spot volumes has fallen 5% for the same period (divergence).

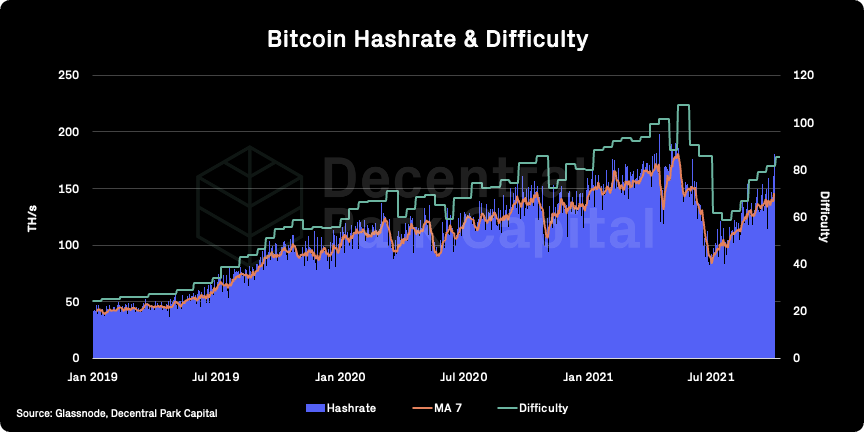

Hashrate & Difficulty; Hashrate has fallen by 3% (7d MA) but overall miner commitment of resources is still looking healthy. BTC difficulty set to increase by a further 1.4% next week.

Active addresses (BTC); Active addresses (30d MA) has increased by 3% over the past week but still 20% lower than ATHs seen during Q1 2021.

Trader positioning; Bitcoin futures OI climbed by over $5B in October with current OI standing at $18.4B. This is lower than total OI printed when BTC was last trading at $56k.

Hedge funds increasing exposure to arbitrage shorts with long-spot exposure being needed more to hedge risk maintain these positions.

Omenics Sentscore (BTC); Spike in positive sentiment around BTC as the asset edges closer to $60k.

Exchange inflow/outflow (BTC, ETH); ETH seeing minor net outflows from exchanges while BTC balance has kept flat over the past week.

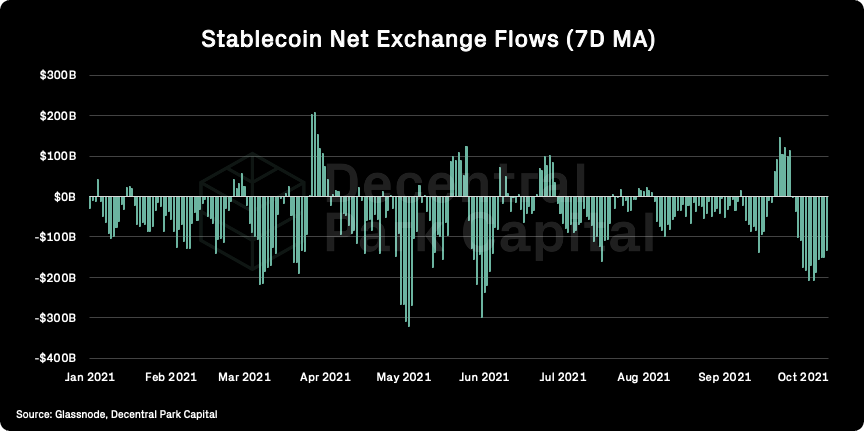

Exchange inflow/outflow (stablecoins); Strong net outflows of stablecoins from exchanges over the past week.

USD(b) supply; Total stablecoin supply has increased by 5B over the past week and now stands at over 126B. Stablecoin supply has 4.5x YTD.

📚 DeFi 2.0 [scupytrooples]

📚 This Week In Ethereum [CryptoGucci]

📚 Yearn [Wot_iS_Goin_On]

📚 Biden Administration Weighing An Executive Order On Crypto [Bloomberg]

📚 Incentives [Delphi]

🎙️ Power Law of Crypto Investing [UpOnly]

🎙️ Community-Run DEX Built by Ava Labs - Pangolin [Protocol 432]

🎙️ Digital Assets 4th Q Predictions [Between2Chains]

🎙️ The Future of MakerDAO [Bankless]

🎙️ DeFi Market Is Undervalued [The Scoop]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.