The Weekly #169

Crypto markets hold steady after returning bullish sentiment drives relief rally in crypto assets. Top performers are market cap agnostic with performance continuing to be largely event-driven.

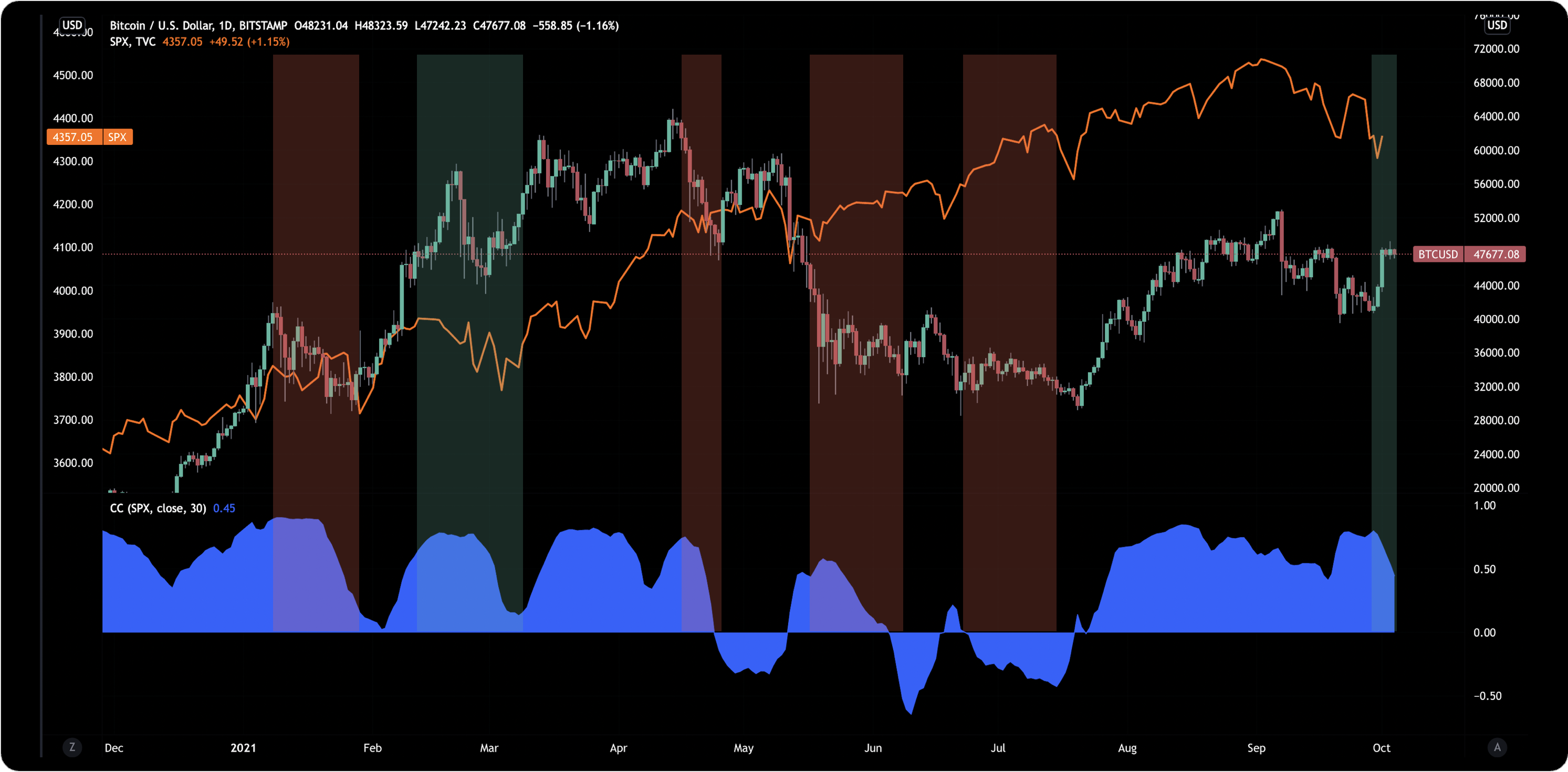

It was a strong week for crypto last week as bullish sentiment started to trickle back into the markets. Global market cap climbed 11% for the week to $2.2T. BTC also climbed 11% but has faced resistance at 48.4k. BTC is currently trading at $47,643 at the time of writing.

One of the more interesting market data points was crypto’s resilience against a brief risk-off action in the equities markets.

On the 30th September, BTC rallied 5.5% while the S&P 500 printed a 1.2% drawdown. A likely reason for this divergence was Jerome Powell’s comments about having “no intention” of banning cryptocurrencies, including stablecoins.

A reduced risk of strict regulatory clampdown perhaps represents a much-awaited bullish pivot after a prolonged period of negative news items. BTC is still largely positively correlated with risk-on assets but this relationship is now weakening.

Historically, falls in their correlation represent periods of BTC down, equities up. This is not the case today - where the opposite is now playing out. This is similar to dynamics in March where resilience in the crypto markets led to new ATH prices.

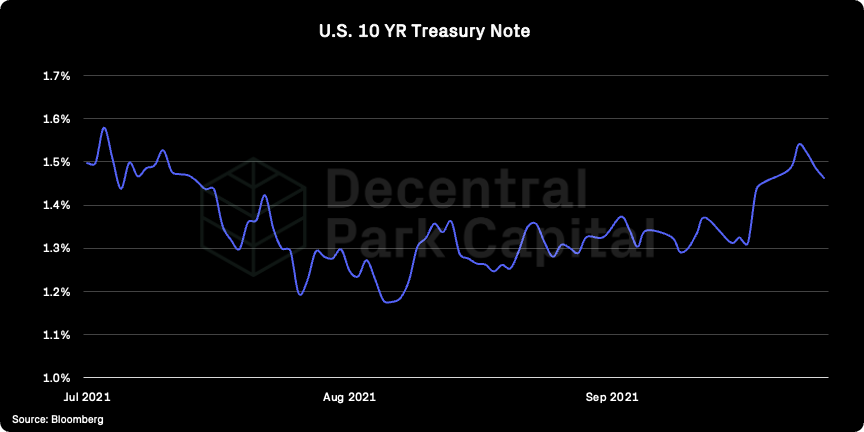

We may not be out of the woods quite yet. The Fed’s imminent tapering and rising inflation concerns may continue to push pressure on risk-on appetite in all global markets. Bond yields are hitting 3-month highs, reducing the relative attractiveness of equities. At the same time, rising earnings and normality in economies can offset this negative impact.

On-Chain

Core on-chain metrics for Bitcoin point to an under utilization of block space over the past few months. Entity-adjusted tx count is down 30% from February’s highs which may indicate low overall interest in the asset.

Bitcoin active entities paints a similar picture but we can see a trend reversal in play. Increases in active entities often coincides with bull market phases.

Dormacy, which measures the age of coins being released into circulation by holders, is plummeting. Dormacy trends up when large quantities of ‘old’ BTC is being ‘spent’ and falls during periods of accumulation.

Doramcy is at ATL levels since 2018 and indicates clear accumulation behaviour by holders. This historically occurs either at late phases of bear markets or early stages of bull markets.

Short-term BTC holders are now getting into profit. After a period of minor capitulation in September, there is now more BTC supply in profit than at a loss (ratio >1). With bullish sentiment trickling back in, it is possible short-term holders may be less likely to sell in the near-term given price is near their on-chain cost basis.

DeFi

DeFi TVL, standing at $194B, is just under ATH levels. Over the past week we have seen a further $21B in value across L1 blockchains.

Notable increases include Solana (+$3.5B) and Terra (+$2B). Saber, which has driven healthy growth on Solana has launched its first stable ETH liquidity pool where users can bridge ETH to Solana using either Allbridge.io or Wormhole.

Meanwhile, Terra saw its Columbus network upgrade go live last week which allows assets to be ported across IBC-enabled chains and refines the seigniorage mechanism behind its stablecoin, $UST.

TVL remains a key driver in chain value today. If we analyze an L1s ratio of TVL and MCAP to Ethereum’s we can make 3 observations:

1) Alternative L1 chains which have higher TVLs have a higher market value.

2) L1 MCAP ratios to ETH are always higher than their TVL ratios.

3) Tier 1 chains are valued much higher on a ratio basis to ETH than their TVL (e.g. Solana, Avalanche). The market is likely pricing in higher future TVL growth for these ecosystems.

Ethereum Scaling

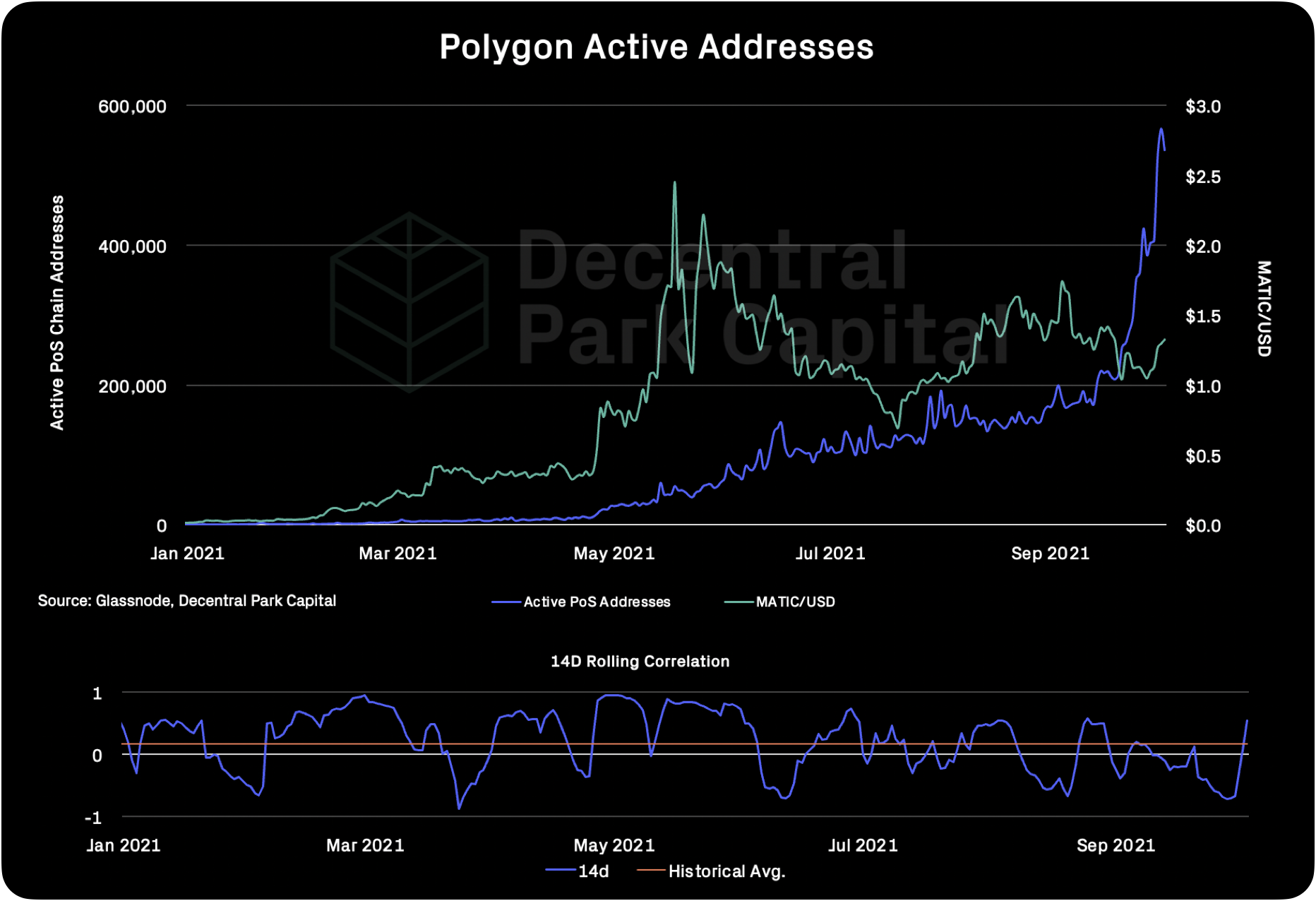

The limelight was not taken away from Ethereum completely. Polygon has seen a surge in active addresses for its PoS chain. NFT hype continues to be a key driver in activity with Polygon OpenSea trader count multiplying by 45x since July.

This has led some analysts to conclude this drives demand for the MATIC token, driving up price in the process. However, the relationship is not all too clear with the recent MATIC price movement looks to be sentiment-driven rather than utility-driven.

The battle between Arbitrum and Optimism intensifies too. Arbitrum leads for aggregate TVL but Optimism shows a more consistent upwards trend since July. Optimism is also getting more momentum for unique addresses and tx count in the lead up to Optimism 2.0.

At the same time, dYdX has been driving the zk-Rollup TVL growth over the past month. zk-Rollup TVL is now 42% that of optimistic rollups and we have yet to see the full launch of zkSync/zkPorter.

Top performing assets for the past week continue to be largely event-driven. AXS leads the market after announcing the launch of their DEX. OMG token holders are set to receive a one-to-one drop of $BOBA tokens next month.

Global:

AXS (+134%)

OMG Network (+96%)

Olympus (+50%)

QTUM (+46%)

OKB (37%)

DeFi:

Olympus (+50%)

dYdX (+34%)

DerivaDAO (+31%)

IDEX (+28%)

Coin98 (+26%)

LDO (-43% U/O)

LDO now trades below its fair market value (APT ratio) by the largest percentage since inception.

TVL is now at ATH ($7.4B) and Lido’s share of ETH2 deposits now stands at 17%. stETH is also becoming more popular with Nexus Mutual increasing its capital pool allocation to stETH and stETH looking to be listed in Aave markets.

dYdX

dYdX continues to lead the market despite being a high cap DeFi name (+34% 7D). dYdX now facilitates more trading volume daily than all other AMMs on Ethereum. Pereptual swap volume is orders of magnitude higher than spot and this could be the first time we see this be mirrored within DeFi.

dYdX is also becoming more capital efficient despite the increase in TVL.

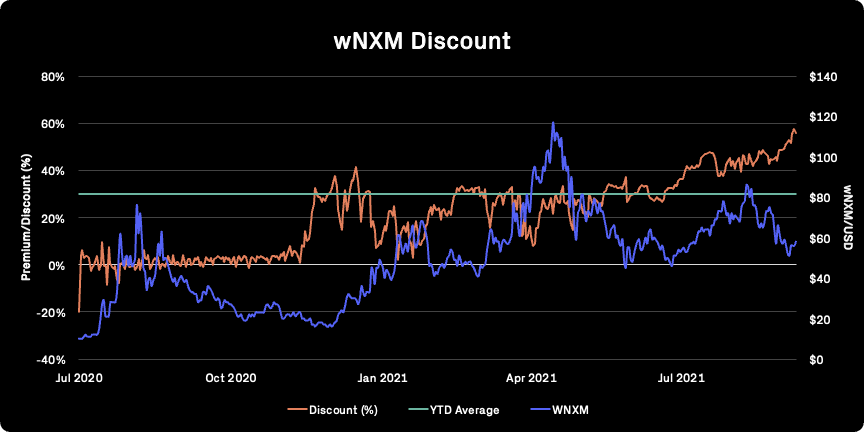

wNXM (55% discount)

wNXM discount to NXM is at ATH (55%) with price-to-book ratio at ATL (0.73) indicating the asset is oversold. MCR% still stands at 100% with arbitrage traders still unable to realize profit.

The mutual will now increase its capital pool allocation in stETH from 15k ETH to 30k ETH.

Compound's new COMP distribution contract contained a bug that allowed some users to receive far too much COMP. No supplied/borrowed funds are at risk, distribution is patched and resumed.

Visor upgraded existing VISR staking program allowing all Visor protocol fees from both Ethereum and L2s (Optimism and Arbitrum) to flow to VISR stakers who stake on Ethereum. APR increased from around 7% to . Learn more.

Polygon has provided Quickswap with $1 million in $MATIC to offer short-term dual farming rewards for select pairs: MATIC / ETH (19%), MATIC / USDC (42%), MATIC / USDT (38%) and MATIC / QUICK (36%).

Saber launches pUSDT / pUSDC pool with Port Finance with 35% farm APY. pUSDC / pUSDT is a pToken, a derivative token that corresponds to an underlying loan on Port Finance. Learn more.

Compound protocol bugs test the viability of DAO governance and smart contract mechanics as $160 million in rewards are leaked to token holders. Compound founder Rober Leshner referred to bugs in the Compound smart contracts as a “moral dilemma” after two exploits inappropriately distributed $160 million in rewards to COMP token holders.

Biden administration and the President’s Working Group are set to release findings on stablecoins, and propose regulating issuers through a special purpose bank charter. “While the report is likely to focus primarily on the risks posed by stablecoins and how to impose a bank-like framework around the firms that issue them, other key issues will likely remain unresolved, such as investor protections around the trading of stablecoins, distinct from the regulation of the companies that issue them.”

Deloitte and Credit Unions respond to federal RFI about how financial institutions will react to crypto, in a positive signal of support for regulatory clarity of digital assets and DeFi. Deloitte and two national associations of credit unions submitted comments to a federal RFI seeking dialogue regarding digital asset rule-making and strategies of financial institutions.

China's ban and crackdown on offshore exchanges presents a window of opportunity for the US to accelerate regulatory clarity, adoption, and infrastructure for digital assets. Senators Hassan and Ernst introduced a bill allowing the Treasury Department to study crypto mining to better understand China’s approach.

Global market cap: $2.2T; Global market cap has increased by 9% for the week.

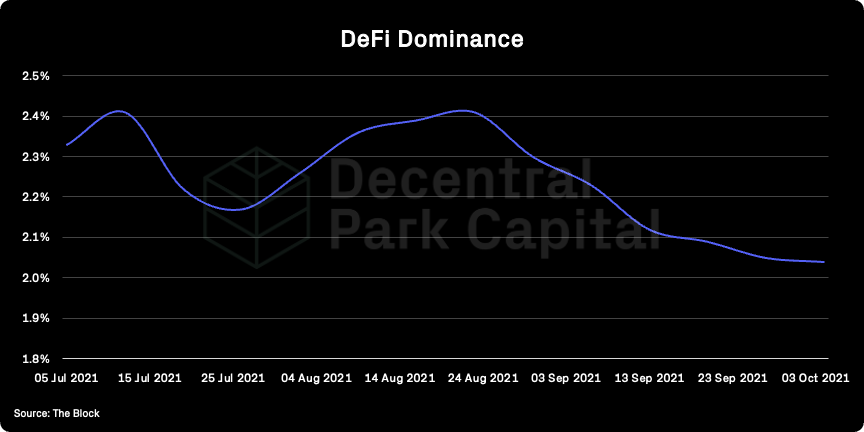

DeFi: $128B; DeFi market cap increased 4% over the last week. DeFi dominance has fallen slightly for the week..

Market shares; Bitcoin dominance has stayed flat over the past week (46%) with a number of L1 assets keeping relatively steady against their BTC ratios.

BTC/USD

ETH/USD

ETH/BTC

Price action; BTC/USD back above 200d MA with resistance at $48.4k. Lowish spot volumes and neutral daily RSI. ETH/BTC still kept range-bound between 0.066 and 0.071.

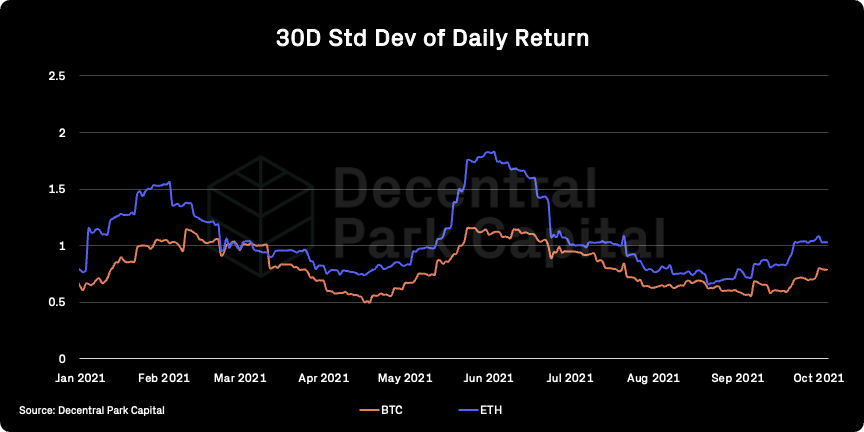

Volatility (BTC & ETH); ETH vol. has stayed flat in recent days while BTC vol. has increased slightly.

Combined order books; Order books look heavier on the bid side. Heavier resistance all the way up to $44.8k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC still perceived as a risk-on asset overall with BTC/SPX 30d rolling correlation increasing to 0.5. Relationship weakening over the past week with correlation falling 30%.

GBTC premium; GBTC still underperforming vs. spot. GBTC discount stands at 14%. The SEC has delayed its decision on BTC ETFs and analysts giving a 75% chance of a futures-based BTC ETF launching in October.

ETHE premium; Discount at -1%. ETHE discount/premium appears to be more sensitive to spot action likely due to ETH ETFs not being a factor for investors at present. ETHE volumes on the secondary market down 43% from May highs indicating relative low interest from investors.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains low indicating lower network utilization. This is conducive to the conclusions in the on-chain analysis above.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

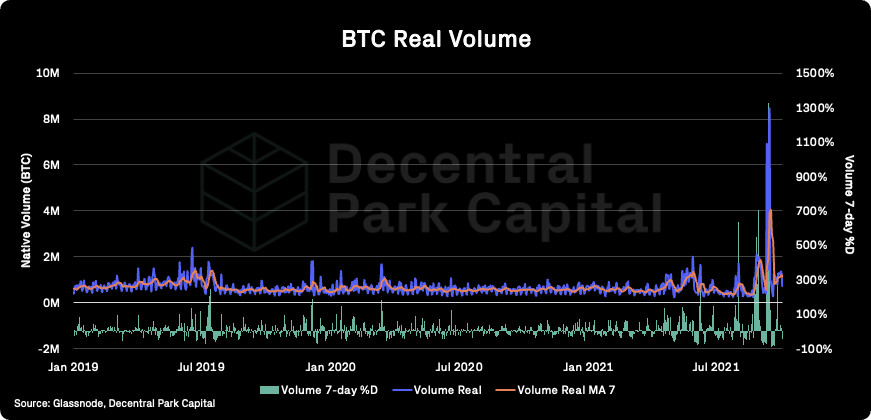

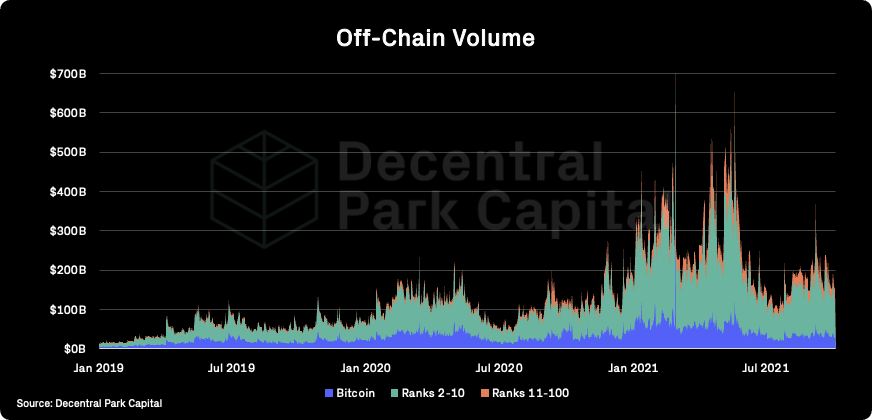

On-chain real (BTC) & off-chain volume; BTC on-chain volume increased ~3% over the past week. BTC and ETH spot volumes decreased 16% and 22% over the past week respectively.

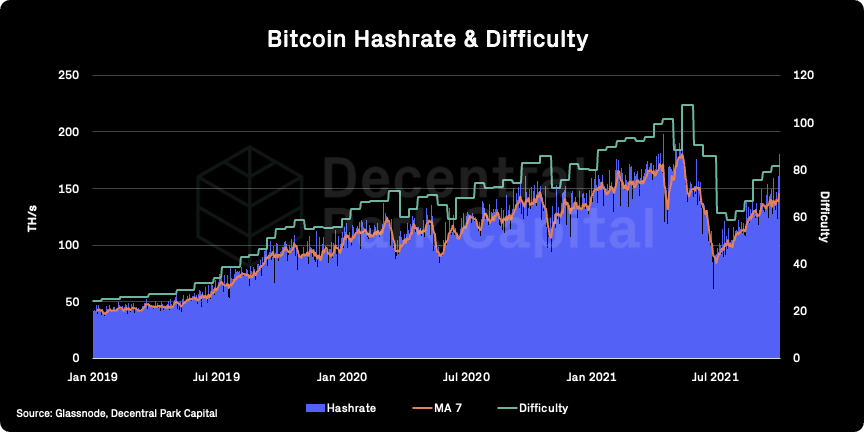

Hashrate & Difficulty; Hashrate has increased by 7% (7d MA) but overall miner commitment of resources looking healthy. BTC difficulty set to increase by a further 3% in the next day.

Active addresses (BTC); Active addresses (30d MA) has stayed flat over the past week.

Trader positioning; BTC and ETH funding rates have turned slightly positive indicating traders taking a predominantly bullish stance. This coincides with increased levels of OI for both assets over the past week. Convergence in put/call ratios for BTC and ETH.

Omenics Sentscore (BTC); Spike in positive sentiment around BTC after an overall bearish period for the month of September, following a slurry of headlines around hacks, exchange clampdowns.

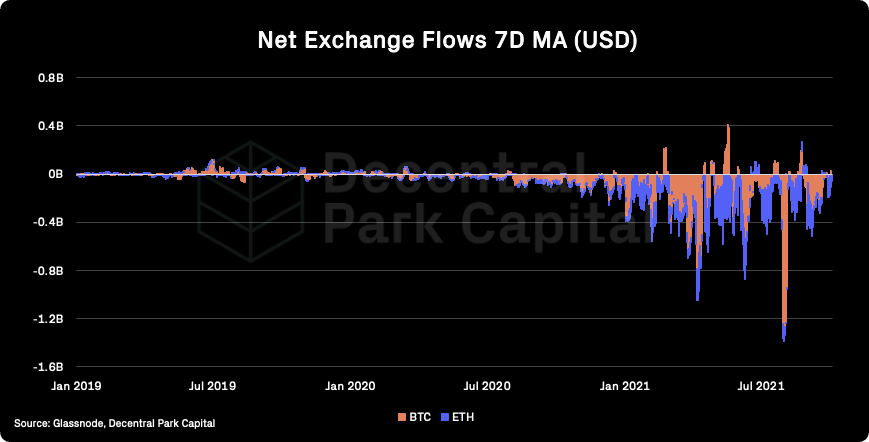

Exchange inflow/outflow (BTC, ETH); ETH seeing moderate net outflows from exchanges while BTC balance has kept flat over the past week.

Exchange inflow/outflow (stablecoins); Strong net outflows of stablecoins from exchanges over the past week.

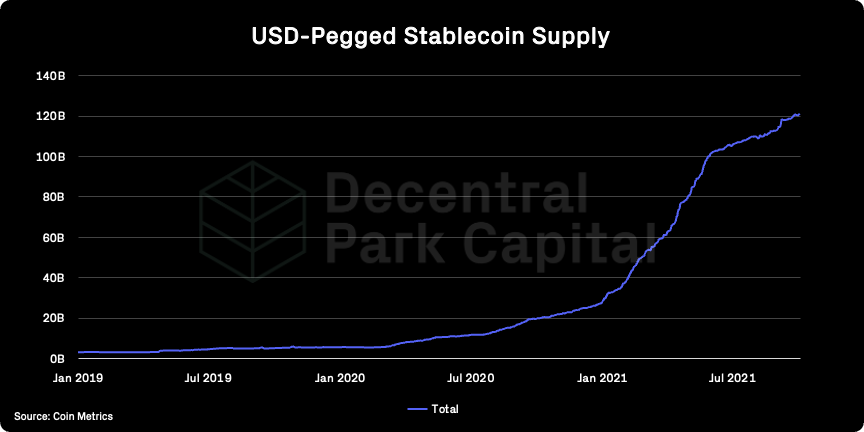

USD(b) supply; Total stablecoin supply has increased by 1B over the past week and now stands at 121B. Stablecoin supply has now increased 350% YTD.

📚 Narrative Distillation [John Zhao]

📚 The Web 3 Playbook [Chris Dixon]

📚 Breakdown of Terra’s Ecoystem [Smart Stake]

📚 Is RARI Undervalued? [Bankless]

📚 DeFi Weekly Report [Coin98]

🎙️ OpenSea & The Busines of NFTs [Bankless]

🎙️ Building Compound And Deep Diving DeFi [UpOnly]

🎙️ DeFi to MetaFi [The Metaverse Podcast]

🎙️ Wrapping Up A Crazy September in Digital Assets [Between2Chains]

🎙️ This Overlooked Crypto Tax Provision Would Be A Disaster [The Breakdown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.