The Weekly #168

Crypto markets hold steady against fresh regulatory headlines. Capital and activity move away from the centralized to the decentralized, driving significant performance for a number of DeFi assets.

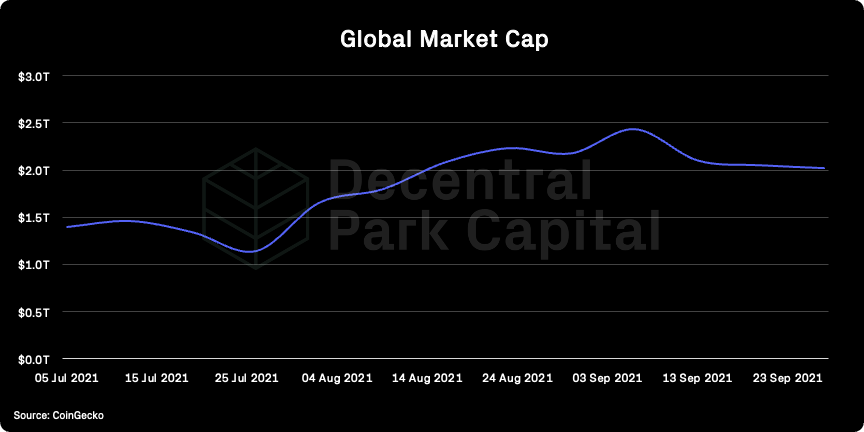

Global crypto market cap holds relatively steady at $2T as regulatory scrutiny and macro factors weigh in on the sector. One of the key headlines last week was China declaring all crypto activities ‘illegal’ (again). These announcements are a bit of déjà vu but unlike previous times, providers like exchanges are starting to be more pragmatic.

Centralized exchanges have started cutting off Chinese users with a number of venues looking to already comply with emerging regulations. There are two key data points here:

1) Exchange tokens with strong Chinese ties have underperformed significantly against both non-Chinese CEX tokens, DeFi, and the crypto market more generally.

2) DEX tokens like UNI have outperformed DeFi with this news with aggressive bans leading people to focus on all things decentralized.

The conflicting part of course being the recent SEC investigations into DEXs Foundations like Uniswap.

While regulatory scrutiny is a key factor for investor positioning, a key short-term threat for crypto are the equity markets. Bitcoin corrections in 2021 have correlated with 2%+ drawdowns in the S&P500.

Last week, The Fed announced it would start paring its $120B monthly asset purchases “soon” and end them by the middle of 2022. Rate-hike expectations are now more hawkish than last year’s FOMC and we may start seeing investors start reducing their gross exposure.

In other words, it is possible we now see investor sentiment switching over to the risk-off camp sooner than anticipated. Crypto is still largely perceived as a risk-on market and further institutionalization of the sector will likely cement this perception.

On-chain

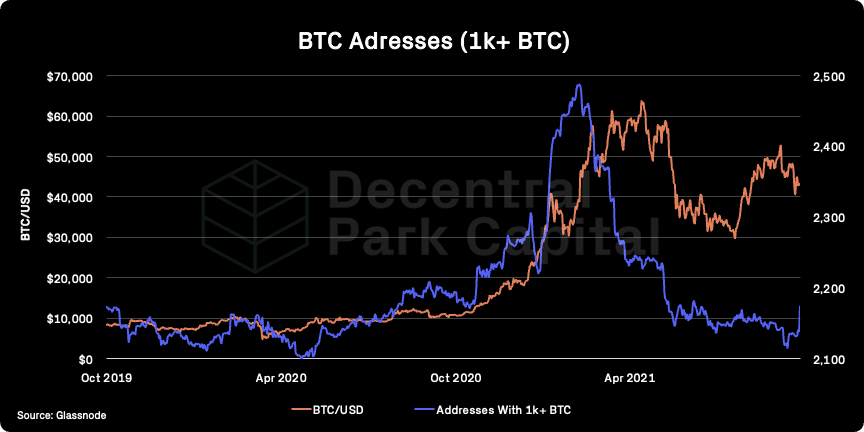

We’ve seen a sharp uptick in the number of BTC addresses holding more than 1k BTC since Friday (+33). This metric historically trends up before we see BTC/USD rallies and this recent uptick may indicate large entities expecting significant price rise for the asset in the near future.

Lightning Network

The payment network for Bitcoin has seen new all-time-highs on a number of key metrics. The Lightning Network’s capacity is up over 160% YTD (2.9k BTC) with over 72k channels. The number of LN nodes is just under ATH (15.6k) - up 88% YTD.

Continued growth here and we may start seeing an emerging narrative centred around Bitcoin and its use as a medium of exchange. This comes at a time when BTC is building deeper roots in developing countries.

Alternative L1 Ecosystems

Smart contract platforms outside of Ethereum have been amongst the top performers in recent weeks. User growth, dApp deployments, and liquidity provisioned to these networks have all contributed to higher valuations.

In terms of aggregate market cap, emerging L1 ecosystems printed new ATHs in early September but has since cooled off by 10%. However, their market cap share with Ethereum continues to trend up with Ethereum now standing at ~70%.

Alternative L1s are seeing impressive WoW growth in TVL with some ecosystems seeing higher nominal growth than Ethereum (e.g. Terra, Avalanche). What’s even more interesting is that TVL market shares seem to mirror MCAP shares to a close degree.

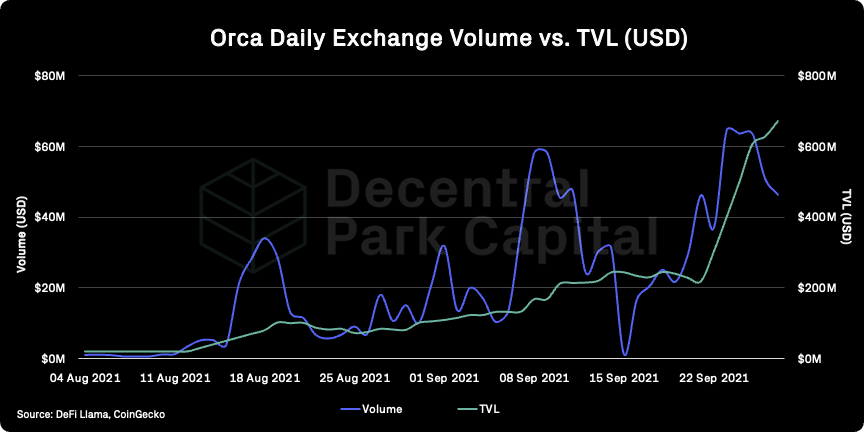

Top performing assets have been largely event-driven. Orca has seen over $600m in liquidity contributed to its network while dYdX has likely benefited from new Chinese traders moving from CEXs.

Global:

Orca (+117%)

Decentralized Social (+53%)

dYdX (+53%)

Terra (+9%)

Celo (+7%)

DeFi:

Orca (+117%)

dYdX (+53%)

Rari Governance Token (+26%)

Perpetual Protocol (+23%)

Enzyme (+23%)

DYDX has been a top performing and with good reason. dYdX daily trading volume has surged to new ATHs ($500m). P/S ratio has fallen 50% since December meaning volume increases have outpaced market value. dYdX protocol revenue totalled $10M last week ($120m annualized).

Number of active traders is down 43% from ATH and indicates fewer traders are trading larger sums of volumes on the platform. However, lower active trader count seems at odds with the narrative of Chinese traders looking to decentralized platforms already.

Lido (-25% U/O)

LDO continues to trade below its APT ratio fair value estimate. Rate of ETH staked via Lido has slowed in recent week but Lido’s share of ETH2 staking has stayed the same at 16%.

Lido now has ~20% market share (610k SLOL) against Marinade for Solana liquid staking.

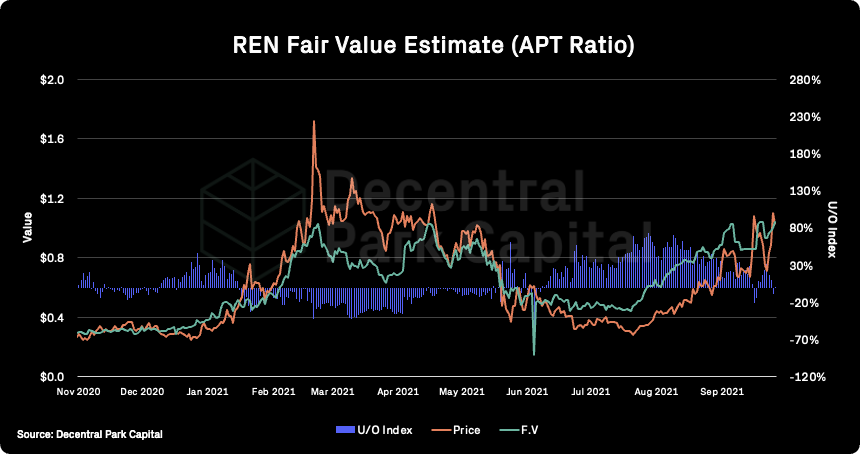

REN (+1% U/O)

REN market value has now caught up with its fair value estimate. Over $30m of value has now been minted on Ethereum L2 solution, Arbitrum. RenVM soon to launch renDAI for Arbitrum.

ORCA (1% U/O)

The Solana AMM has seen a 117% increase in TVL over the past week with trading volume printing new ATHs ($650m). While impressive, Uniswap V3 is 6-10x more capital efficient as an AMM than Orca today.

BarnBridge's SMART Alpha has been deployed on Polygon, LPs can deposit in ETH/USD, BTC/USD, MATIC/USD, ETH/BTC pools to manage their exposure to these assets.

Mercurial Finance with Wormhole bridge set up Solana's first 4Pool for wrapped wormhole tokens (wUSDC, wUSDT, wDAI + native USDC), current APY is 22%. For more info check this guide.

Saber has upgraded Wormhole farms to v2. Additionally, pools/farms have been added for Wormhole Ethereum USDC (23%) and USDT (25%).

Orca announced Orca Fall Festival with doubled ORCA LM rewards and new Double-Dip pools with additional rewards. Learn more.

Lido and 1inch have collaborated to provide LPs with double rewards on the stETH/DAI pool (200,000 LDO and 200,000 1INCH for the first month). APY is 43%, additional info here.

Scrutiny over stablecoins is accelerating as the Biden administration takes aim and the Federal Reserve prepares to issue findings. The Federal Reserve is set to lay out its views, as early as this week, that will espouse a “blueprint on the ‘the future of money, including stablecoins.”

Senator Toomey, Chair of the Senate Committee on Banking, sends concerns to SEC Chair Gensler after hearing. On friday, Senator Toomey (R - PA) sent a letter to Gensler followed up with harsh language for Gensler regarding the SEC’s approach of regulation by enforcement. Toomey seems to be echoing support for broad based clarity, similar to Representative Beyer’s approach in the House with the proposed Digital Asset Market Structure and Investor Protection Act.

Biden nominates anti-big bank and crypto skeptic for OCC Chair, as acting Chair compares crypto to toxic securities leading up to the Global Financial Crisis. Biden nominated Cornell law professor Saule Omarova as chief of the Office of the Comptroller of the Currency in what is being viewed as a partisan candidate who is skeptical of big banks and focused on consumer protection. Acting OCC Chief Hsu used language comparing crypto to the exotic assets that contributed to the Great Financial Crisis of the 2000s.

CBDCs are gaining steam across the West as a central bank policy tool against stablecoin proliferation, with Cleveland Fed President expressing an open mind. US regulators have been fairly unsupportive of broader CBDC proliferation, a stance that China and even Europe have eschewed by implementing the digital yuan and a UK study into the matter. Now Federal Reserve Bank President Mester and Fed Chair Jerome Powell are acknowledging the competitiveness of a CBDC as an effective policy tool.

Global market cap: $2T; Global market cap has decreased by 1% for the week.

DeFi: $123B; DeFi market cap increased 5% over the last week. DeFi dominance has increase 1% over the same period.

Market shares; Bitcoin dominance has stayed flat over the past week (46%) with a number of L1 assets keeping relatively steady against their BTC ratios.

BTC/USD

ETH/USD

ETH/BTC

Price action; BTC/USD remains below 200d MA, finding initial support at $40.7k. Relatively low spot volume. ETH/BTC finding resistance at 0.0712. Daily RSIs all in neutral territory.

Volatility (BTC & ETH); ETH volatility has stayed flat in recent days for both BTC and ETH.

Combined order books; Order books look heavier on the bid side. Heavier resistance all the way up to $44.8k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC still perceived as a risk-on asset with BTC/SPX 30d rolling correlation increasing to 0.71 since last week.

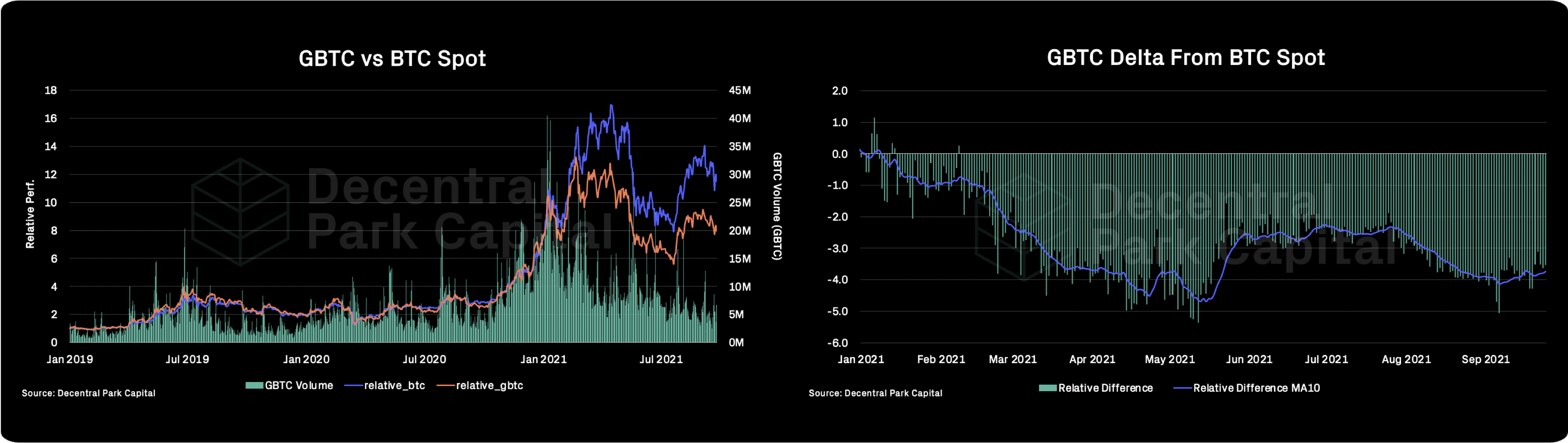

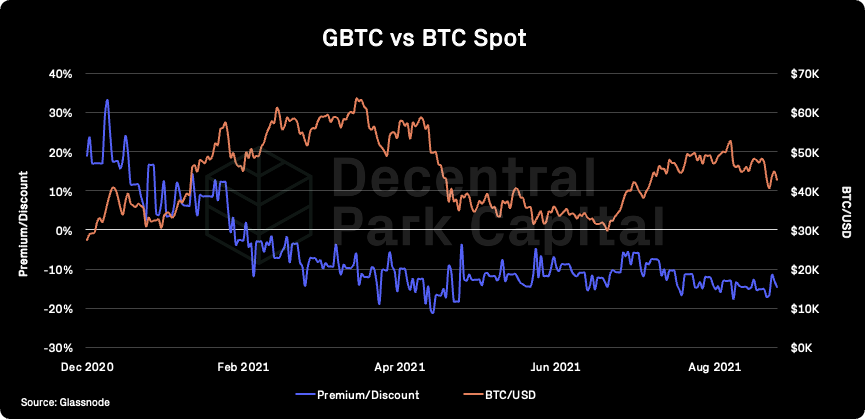

GBTC premium; GBTC still underperforming vs. spot. GBTC discount widened to 15%. With overall discount trending down, it looks more likely the market is placing a higher likelihood of BTC Futures ETFs to be approved in October.

ETHE premium; Discount at 6%. ETHE briefly printed 0.7% premium on September 22nd as ETH dipped to $2.75k indicating opportunistic ETHE buying on the secondary market. Still unclear about long-term premium being sustained but frequency of premium prints and higher lows are positive data points.

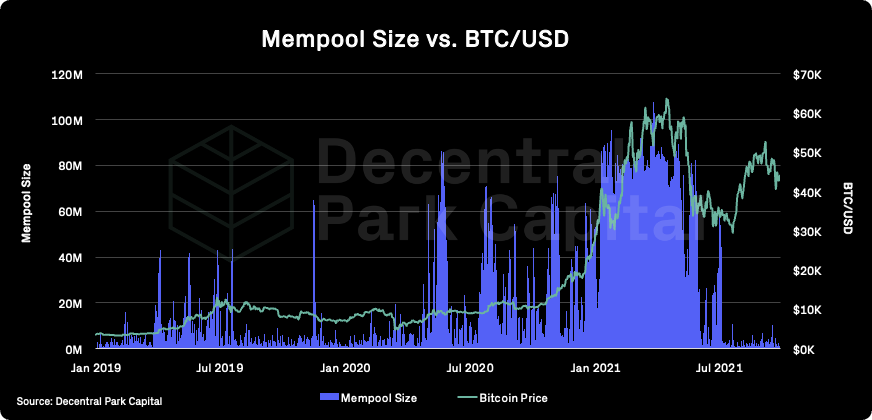

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains low indicating low network congestion.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

On-chain real (BTC) & off-chain volume; BTC on-chain volume increased ~20% over the past week. BTC and ETH spot volumes increased 27% and 44% over the past week respectively.

Hashrate & Difficulty; Hashrate has decreased by 2% (7d MA) but overall miner commitment of resources looking healthy. BTC difficulty increased 3% on the 21st of September.

Active addresses (BTC); Active addresses (30d MA) has decreased by 1% over the past week.

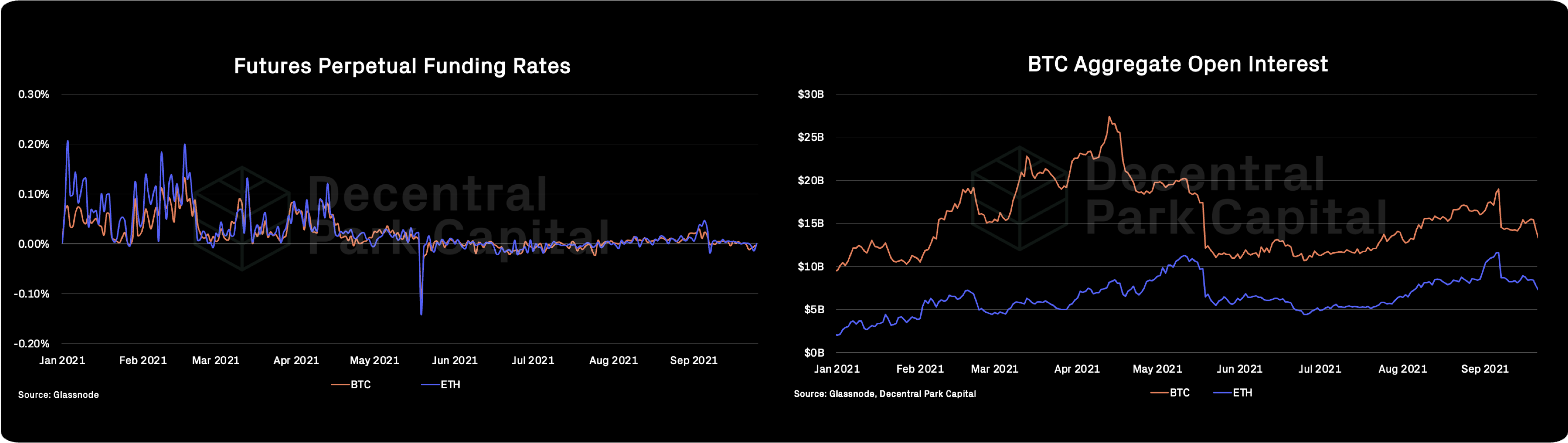

Trader positioning; BTC and ETH funding rates turned negative last week but are now neutral with OI falling for both assets. Divergence forming for BTC and ETH put/call ratios.

Omenics Sentscore (BTC); Sentiment around BTC turning negative over the past week with the Chinese crackdown being a key driver.

Exchange inflow/outflow (BTC, ETH); Net outflows turned to very minor net inflows last week. ETH now printing net outflows while BTC still shows net inflows on the 7d MA.

Exchange inflow/outflow (stablecoins); Strong net inflows for stablecoins (DAI, USDT, USDC) potentially indicating opportunistic buying by traders (i.e. moving out of stability).

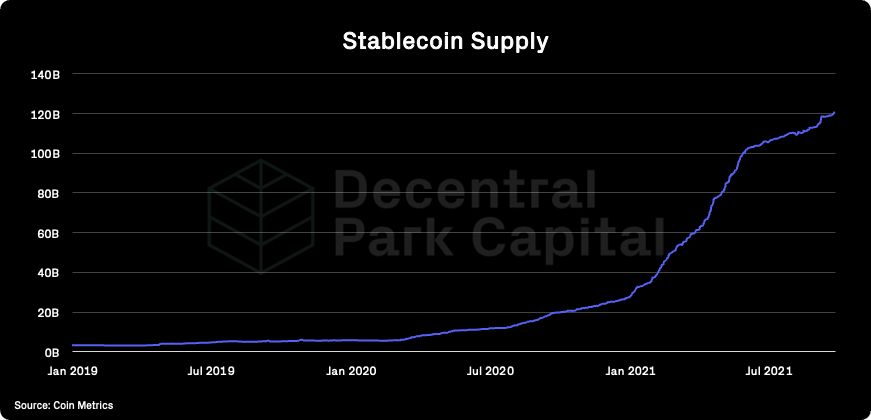

USD(b) supply; Total stablecoin supply is printing new ATHs (120B+).

📚 Mercurial Finance on Solana [CoinDesk]

📚 Why Web3 Matters [Chris Dixon]

📚 MakerDAO Concerns [Adam Cochran]

📚 Hasu Notes On UpOnly [CMS Intern]

📚 Web3 will be driven by crypto’s networked collaboration [Coinbase]

🎙️ Why Regualtors Should Embrace The Openness Of The Blockchain [The Scoop]

🎙️ Hop Protocol: A Trustless Protocol To Quickly Transfer Tokens From One Rollup/Sidechain To Another [Delphi]

🎙️ Digital Assets: Where Are We In The Cycle? [Between2Chains]

🎙️ Is Crypto At A Social-Regulatory Inflection Point? [The Breakdown]

🎙️ Scaling Ethereum: Starkware [Blockcrunch]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.