The Weekly #167

Crypto feels the heat as global markets become increasingly turbulent.

Macro Turbulence

Over the last week, the global crypto market cap has fallen 7%, retreating back to the $2T mark once again. A market wide sell-off appears to be in the works with BTC opening the week 7% down, trading at $43.8k

BTC/USD appears to have found initial support at $42.4k for now, falling slightly less than other high cap names.

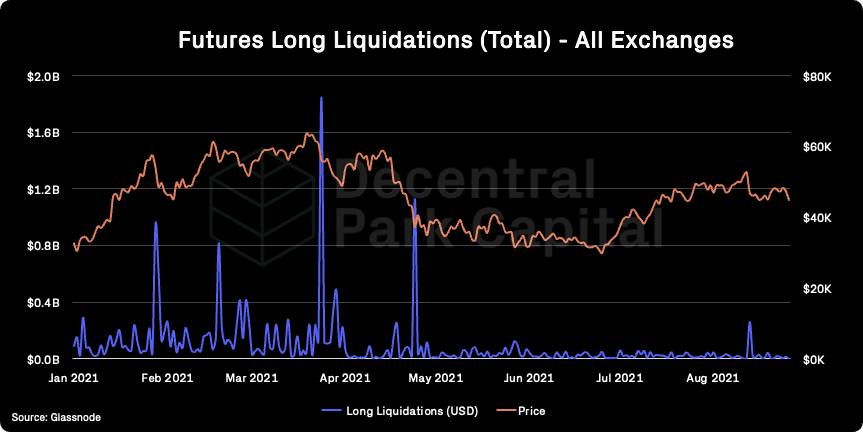

Just two weeks ago, it appeared the markets was in a similar state of correction. Analyzing long liquidations in the futures market shows that the initial negative price action was unlikely to be futures-based.

In the last 24 hours, ~$800m positions have been liquidated of which over $212m have occurred in the last 4 hours. Long squeeze may exacerbate short-term drawdowns but it appears other factors likely at play.

A key unfolding macro story this week has been the embattled Chinese property company Evergrande which has seen its shares plunge 12% in afternoon trade in Hong Kong. In short, Evergrande has $300B in liabilities with link to several banks where payments due are causing a potential liquidity crisis and cross defaults in the wider financial sector.

There is evidence for this already with Hong Kong’s Hang Sang Index dropping to a 52-week low (-7%) and U.S. stock futures also declining with Dow Jones futures falling 300 points.

BTC continues to be traded as a risk-on asset. BTC’s 30D Pearson correlation with SP500 is moderately positive at 0.58. Any weakness in the US equity markets from Chinese leveraged developers will likely also be carried over to the crypto markets.

At the same time, not all believe there will be material impact on crypto. It is possible that Evergrande’s $4B market cap is not a systemic risk to crypto and we have seen plenty of crypto bull runs against an existing property selldown in China.

However, these crypto bull runs have coincided with performant US equity markets which have so far shrugged off Evergrande contagion risk which may no longer be the case.

Regulation

Stablecoins

The New York Times publishing an explainer article for options that regulators could use at their disposal which many have taken as a clear signal that regulation is imminent. Stablecoin supply has grown 4x over 2021, climbing to ATH (120B).

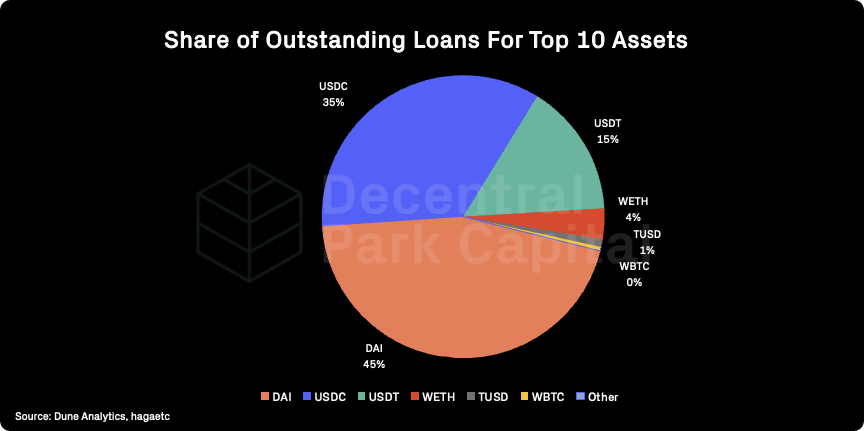

Regulatory tightening will have a material impact on crypto as it stands today. For example, over 95% of outstanding loans Lending protocols in DeFi are stablecoin-denominated.

A key question is how crypto-collateral stablecoins (e.g. DAI) will be treated relative to their USD-collateral peers (USDT, USDC) in light of tightening regulation. To make things murkier, Over 53% of DAI in circulation has been generated using USDC.

Crypto Lending

US states have filed notice seeking a hearing to determine whether to issue a cease and desist order against Celsius over unregistered securities.

Celsius (~$24B AUM) is larger than any one DeFi protocol by TVL. Celsius’ active deployment in DeFi to offer high rates may be directly impacted depending on the outcome of the recent state orders.

Insider Trading

Insider trading took place on the largest NFT marketplace with these types of activities likely contributing to the call for regulation. As regulation look closely to DeFi, the financialization of NFTs will likely lead regulators to apply a similar level of scrutiny.

Total performing assets over the last week have been largely smaller cap names with performance still being predominantly event-driven than momentum-driven.

Global:

ECOMI (+39%)

Olympus (+19%)

Cosmos (+17%)

Audius (+14%)

Curve DAO Token (+8%)

DeFi:

Joe (+49%)

Olympus (+19%)

Rari Governance Token (+19%)

dYdX (18%)

Rocket Pool (17%)

dYdX

dYdX has been a top weekly performer with TVL reaching new ATHs ($600m) and daily gross merchandise volume (USD) surpassing $1.5B. Despite the recent rally, volumes have been increasing at a faster rate than FDV with the market pricing volume lower than its competitor, Perpetual Protocol.

LDO (-13% U/O)

LDO’s market value remains below its fair value estimate (APT ratio) but the two are starting to converge (i.e. U/O index falling). Over 570k SOL are now staked via Lido (adding ~$80m to TVL).

JOE

The Avalanche ‘DeFi Hub’ JOE trading volume has increased to $200m daily with $800m TVL. JOE now facilitates 18% of Uniswap’s volume yet its FDV is 6% that of Uniswap’s. JOE also has a lower TVL utilization ratio (25%) compared to Uniswap V3 (~62%) with the latter more competitive from a capital efficiency perspective.

REN (-14% U/O)

Ren has reached new ATH in TVL ($1.04B) with Ren launching a new stable pool on Arbitrum. Total value ($380m) and number of BTC minted (8k) on alternative L1s has surged in recent weeks as more L1s become integrated with RenVM. Nearly $300m has been minted on Solana alone.

Recent demand has increased fair value above price once again.

Curve Tricrypto pool (USDT/BTC/ETH) is live on Fantom, CRV and FTM rewards TBA. Meanwhile, CRV rewards are live on Arbitrum with 19% APY for Tricrypto.

Saber launches new BUSD / USDC pool with Allbridge – LPs can stake abBUSD bridge asset for 21% APY in pool's farm.

Marinade Finance, a liquid staking protocol for Solana, announced retroactive 5,000,000 MNDE rewards for Marinade users.

Orca launched aquafarms for Parrot assets, LPs can now deposit into pSOL-USDC (29%) and ORCA-PAI (118%) pools to earn dual rewards in ORCA and PRT.

Global market cap: $2T; Global market cap has decreased by 7% for the week as crypto assets prices continue to cool off.

DeFi: $129B; DeFi market cap declined 9% over the last week. DeFi dominance fallen 1% over the last week with the sector market cap declining at a faster rate than the wider market.

Market shares; Bitcoin dominance has increased over the past week (46%) as high cap names experience sharper drawdowns.

BTC/USD

ETH/USD

ETH/BTC

Price action; BTC/USD remains below 200d MA, finding initial support at $42.4k. Relatively low spot volume. Second week of ETH/BTC weakness, falling 3%.

Volatility (BTC & ETH); ETH volatility has stayed flat over the past week while the BTC 30d volatility has fallen slightly over the same period.

Combined order books; Order books look heavier on the bid side. Heavier resistance all the way up to $45k (Source: Bitcoinity).

BTC vs. SPX and Gold; BTC still perceived as a risk-on asset with BTC/SPX 30d rolling correlation at 0.58.

Key macro event this week with the Fed’s FOMC meeting 21-22nd September where a formal signal on tapering may be given. Wider investor sentiment will likely carry over to BTC and the wider crypto market more generally.

GBTC premium; GBTC still underperforming vs. spot. GBTC discount widened to 15%. Possible the market places higher likelihood of BTC Futures ETFs to be approved in October. No narrowing of discount may mean unlikely to see Grayscale GBTC roll over into an ETF in the near-term.

ETHE premium; Discount at 6%. ETHE 30d average volume increased to 7m shares but is starting to decline once again signalling waning interest on the secondary market.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network remains low indicating low network congestion.

Mempool Size is the aggregate size of transactions waiting to be confirmed on the Bitcoin network. The more low value transactions are stuck in the Mempool, the more network resources are being expended by higher value transactions.

On-chain real (BTC) & off-chain volume; BTC on-chain volume decreased ~30% over the past week. BTC and ETH spot volumes fallen 22% and 27% over the past week, respectively.

Hashrate & Difficulty; Hashrate has increased by 4% (7d MA) with miner commitment of resources looking healthy. BTC difficulty estimated to increase by 3% in 1 day due to strengthening resource commitment.

Active addresses (BTC); Active addresses (30d MA) has increased 2% over the past week.

Trader positioning; BTC and ETH funding rates remain low along with open interest. Investors seem cautious overall with low levels of leverage in market. Slight increase in put/call ratio for BTC.

Omenics Sentscore (BTC); Sentiment around BTC remains relatively high but has been decreasing in line with spot action.

Exchange inflow/outflow (BTC, ETH); Moderate net outflows continue for BTC and ETH (7d MA). We are now seeing an ATL (2.45m) for BTC on centralized exchanges since August 2018.

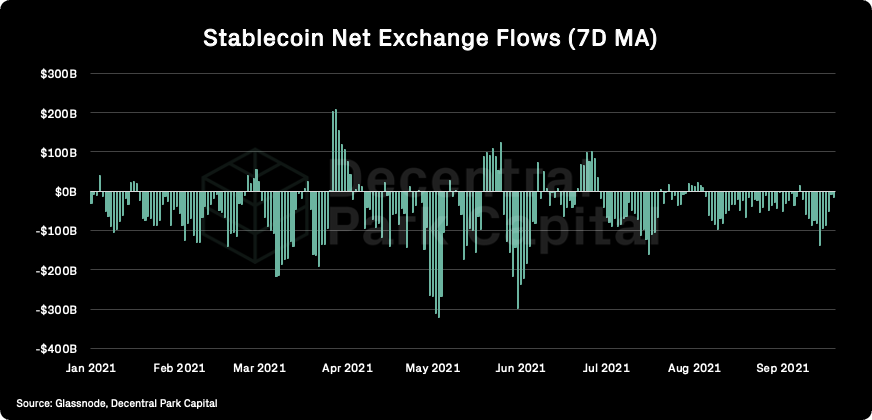

Exchange inflow/outflow (stablecoins); Declining net outflows of USDT, USDC, and DAI from centralized exchanges over the past week (7d MA) possibly indicating opportunistic buying by traders or traders covering their USD denominated margin accounts.

USD(b) supply; Total stablecoin supply reached new ATH (120B) last week.

📚 NFT Tracking Tools [ColeThereum]

📚 A Dive Into Matter Labs [The Block]

📚 A League Of Parachains [XRP Arrington Capital]

📚 Jake Chervinsky Round Table Summary [Joe Pettibone]

📚 Upcoming Terra Updates and Protocols [Fastgamecrypto]

🎙️ On Solana’s Outage [Unchained]

🎙️ On Building DeFi Protocol [UpOnly]

🎙️ Art for DeFi with PleasrDAO [The Metaverse Podcast]

🎙️ Free Markets vs. Investor Protections [The Breakdown]

🎙️ Beyond Coin Voting Governance | Vitalik Buterin [Bankless]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.