The Weekly #206

Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below.

How Far Is Far Enough?

The cryptoasset market jumped 4% last week on what was an overall bullish period for risk assets. Cryptoassets have now recovered 40% from June lows with eyes now on the market breaking through $1.127T resistance.

These levels marked the January 2021 and June 2021 lows where a convincing break above here may signal strong momentum to the upside from here on in. However, note the declining momentum since 2021’s highs with the daily RSI rolling over at the resistance line.

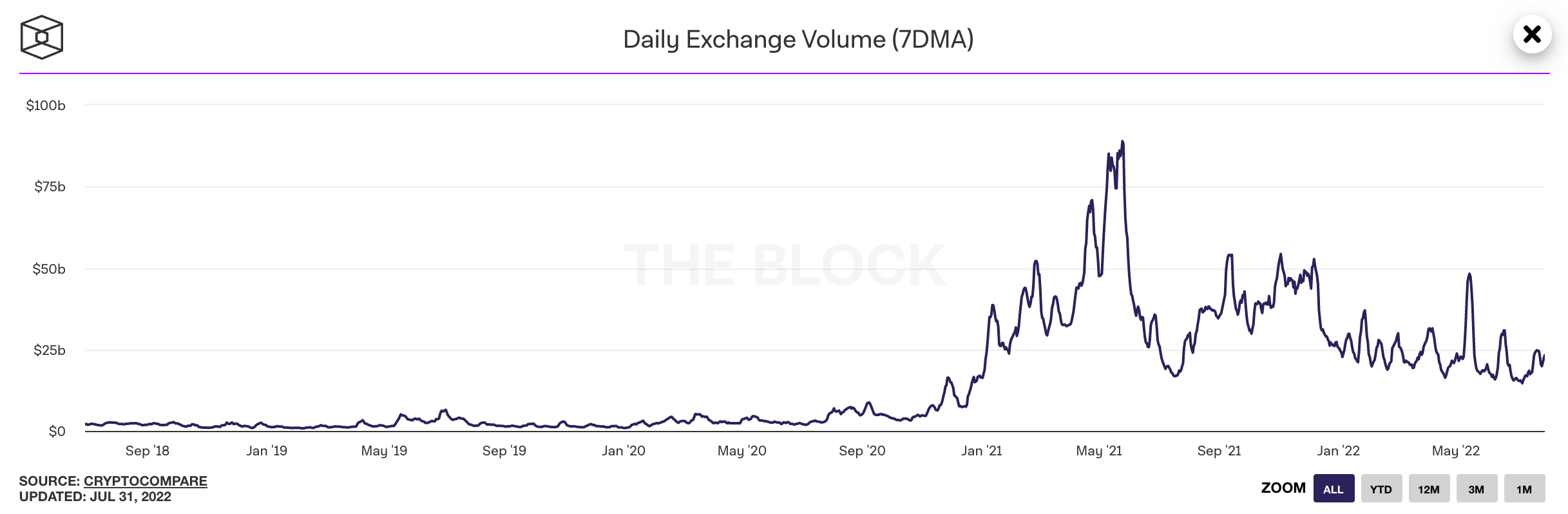

Basic measures of market participation such as daily exchange volume illustrate why we should remain cautious with lower peaks and lower lows being the key trend so far in 2022.

However, the key driver in price action remains the macro. Last week, the Federal Reserve increased rates by 75 BPS (in line with market expectations) taking its benchmark rate to a range of 2.25-2.5%.

The initial reaction by markets was bullishness perhaps signalling a dovish interpretation of Jerome Powell’s comments. Specifically, the Fed paving a potential path to pausing or cutting even rates citing recession risks and slow growth. More cynically, Powell’s comments allowed him optionality for future meeting decisions based on new data.

In any case, the Fed has fallen short of giving the strong signals to the market. It seems likely that prices, are likely to remain central banks’ north star for now.

Therefore, it seems markets (forward looking) are taking the recession camp while central banks are taking the inflation camp (backwards looking). One side will blink over the coming months.

We see this trend globally too with traders now pricing in a lower rate hike increases from the BoE’s meeting this week. The problem central banks have is if there’s a pivot from price to growth, they run the risk of letting price run higher - a trend within the US from the 60’s up until the early 80’s.

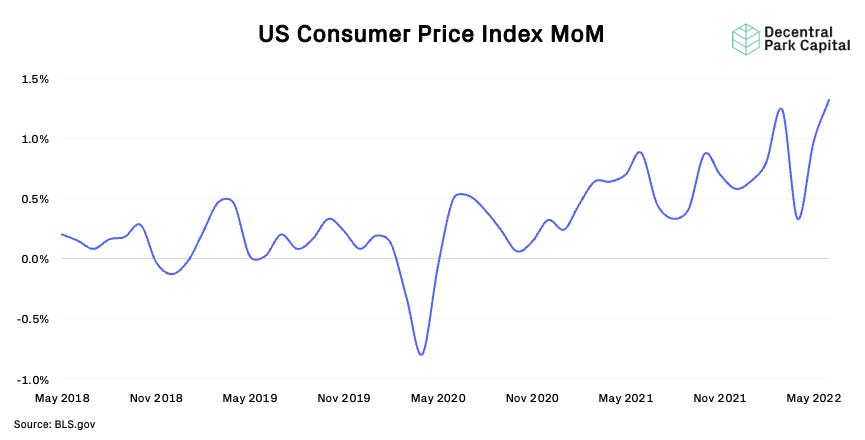

Within the US, the Fed will need CPI to come right down to the ~0.2-0.3% MoM range to get close to their target - a far decline from the recent 1.4% print in July.

CPI remains higher than the FF target rate too. With Powell suggesting the FF is in range of neutral, there appears to be widespread confusion for how this was to be interpreted. During periods of high inflation, the Fed would typically raise rates above prevailing levels of inflation to kill it.

This is leading some to believe that the FF needs to extend higher closer to 4% if CPI was to retreat slightly over the coming quarters. This FF TR extension is likely not priced in by the market today.

The risk for traders here is a mis-interpretation of potential credit ease by an unclear Fed ultimately determined to tighten financial conditions to any necessary levels in order to bring down price.

A challenge here is that prices may not be coming down at the rate central banks are looking for. Last week, the YoY change in the personal consumption expenditures index reached the highest level in January 1982. In other words, it may be that peak inflation is not yet in as core inflation drivers are signalling a re-acceleration.

Over in Europe, an energy crisis is unraveling with the EU becoming increasingly concerned with the reduction in available natural gas supply with flows being limited more than previously expected. German baseload power is trading closer to a new top and will likely remain elevated is supply constraints persist.

Raised rates in Europe will likely also been driven by consideration around currency stability and relative strength to the dollar. After all, a weakening currency may make the problem of rising prices even worse for central banks. The battle for leading rate hikes is well underway.

Where does this leave is? Well the market is clearly not pricing in an extension in the FF target rate with the focus being on growth, not price.

The US 10Yr yield has now broken down below support suggesting an expectation in growth and price collapse. The dollar weakness is also signifying less aggressive Fed. However, prices are unlikely to rollover unless commodities also rollover but with ongoing supply constraints poses significant challenges unless the demand side of the equation collapses.

The prospect overall therefore being prices remaining structurally high for the foreseeable future. Expecting a Fed pivot in the near term? Dream on.

Crypto In Harmony

Risk assets like equity are in bear market territory but not yet recession territory. There’s a lot more that risk assets can do in order to tighten financial conditions that can bring down price substantially.

This informs cryptoassets indirectly so long as the nascent market remains tightly coupled with equities.

It’s not just the prospect of another equity drawdown that should send alarm bells to cryptoasset traders but the reduction in broader market liquidity.

Whether the Fed has the ability to reduce its balance sheet below the $8T mark or not, the Fed is targeting a $500B run off by year end (-6% of current liabilities) with bank reserves falling to $2.1T during the Q1 2023 (-$900B).

Over the past week, ETH has marginally outperformed BTC (5.7% vs. 3.4%) with the marge and scaling headlines driving the majority if this ecosystem-specific momentum.

The DeFi MACAP/Total MCAP ratio has kept in a descending channel since September 2022 but could be at an inflection point. A convincing break above the top channel line may signal renewed risk appetite but the bias remains to the downside given the macro outlook.

Ethereum’s merge could be the catalyst for a break out with high beta plays related to ecosystem momentum (ETH2 = $LDO; Scaling = $MATIC) driving performance for the sector as a whole.

As we highlighted in the last week’s edition of The Weekly, DeFi/Total is also positively correlated to key measures of liquidity conditions such as the Fed balance sheet.

That said, there are several indicators suggesting a cooling off of Ethereum momentum. Technicals show ETH/BTC bearish RSI divergence (D) over the past 2 weeks with spot volumes declining since mid-June.

Bitcoin dominance has been declining sharply since June 2022 with momentum divergences indicating a potential reversal may occur.

Here is NDX/ETH where the ratio appears to be in a wider uptrend for now (limited relative deployment of risk down continuum).

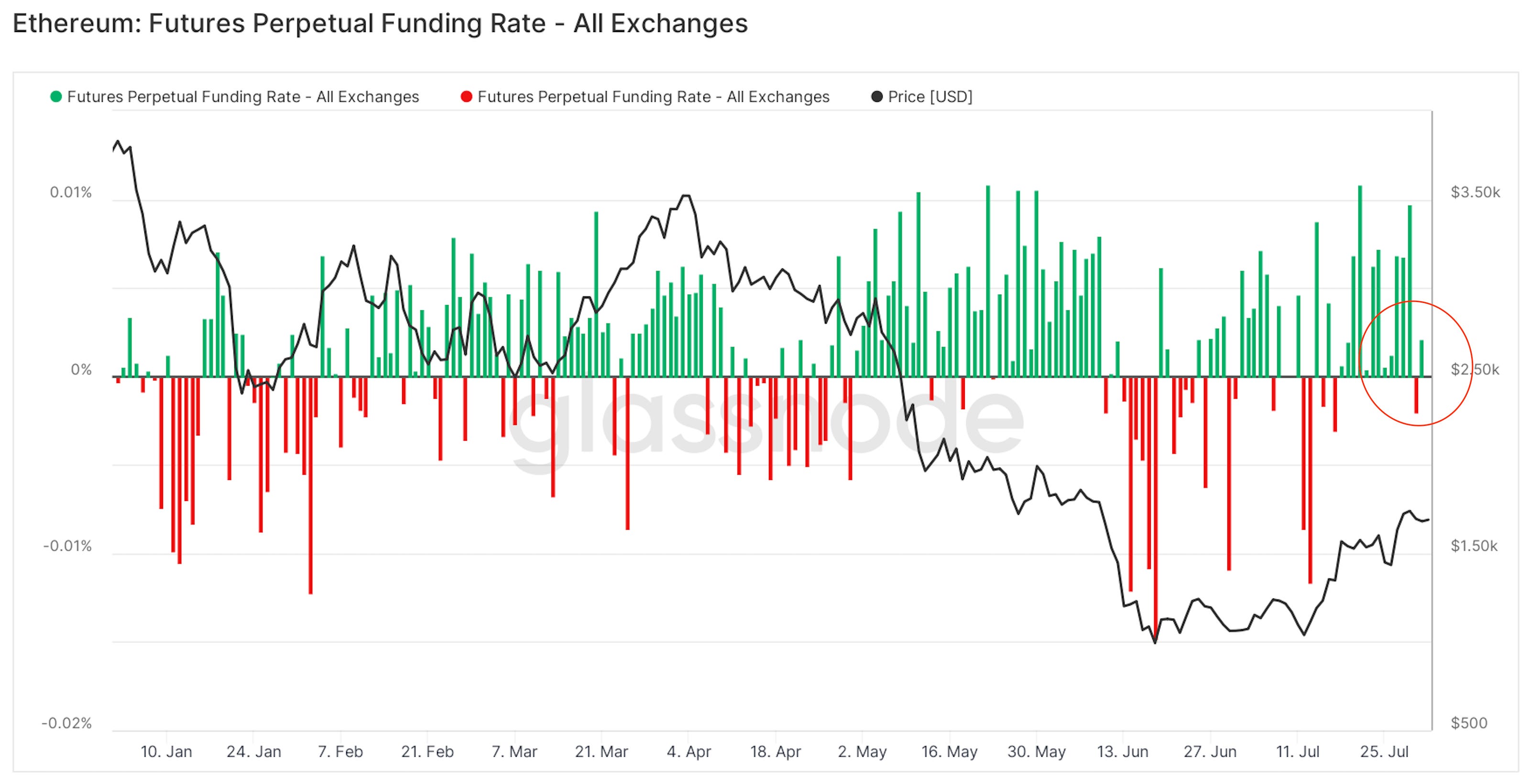

Perpetual futures markets show funding rate now only being marginally positive indicating momentum is declining alongside spot.

On-chain valuation models show some evidence of growing economic activity across a growing number of users as underpinning price over the past few weeks. However, this appears to be rolling over over the past 48 hours.

Looking ahead, all eyes are on playing the merge through certain ETHPOW trades (sell ETHPOW DeFi apps to ETHPOW, sell ETHPOW upon CEX listing to other assets).

This ‘ETH milkshake theory’ may end up driving demand eventually back to the ETH2 driving outperformance on a relative basis to competing ETH forks and potentially other beta names more broadly.

A number of top performing assets over the past week have been fork-related (Bitcoin Gold and Ethereum classic) with merge-related assets and Ethereum blue chip names also printing strong gains.

Top 100 (7d %):

Filecoin (+76.2%)

Ethereum Classic (+43.6%)

Bitcoin Gold (+33.5%)

Lido DAO (+31.6%)

Internet Computer (+28.1%)

DeFi Top 100 MCAPs (7d %):

yearn.finance (+65.3%)

GMX (+45.2%)

Ellipsis (+42.5%)

Flamingo Finance (+38.8%)

Seedify.fund (+34.2%)

Curve deployed new Aave pool on Avalanche, it is integrated with Aave v3 and includes USDC, USDT and DAI. Current APR is 3.5%, CRV gauge rewards TBD.

Stake DAO implemented Time Weighted Average Voting power (TWAVP) mechanism for CRV, ANGLE and FXS liquid lockers. This mechanism prevents governance attacks by increasing the voting power of staked sdTOKENs over a 30 day period after deposit.

Lido is bringing stETH to DeFi on Layer 2, users will be able to stake ETH directly on L2s, and use received wstETH (wrapped, non-rebasing version of stETH) across multiple DeFi protocols. Details coming soon.

Maker DAO plans to reduce stETH stability fee for WSTETH-A and WSTETH-B to 2.25% and 0% respectively. Decision is driven by impoved conditions of stETH liquidity and upcoming merge. Stability fee is paid by users willing to borrow DAI against stETH collateral.

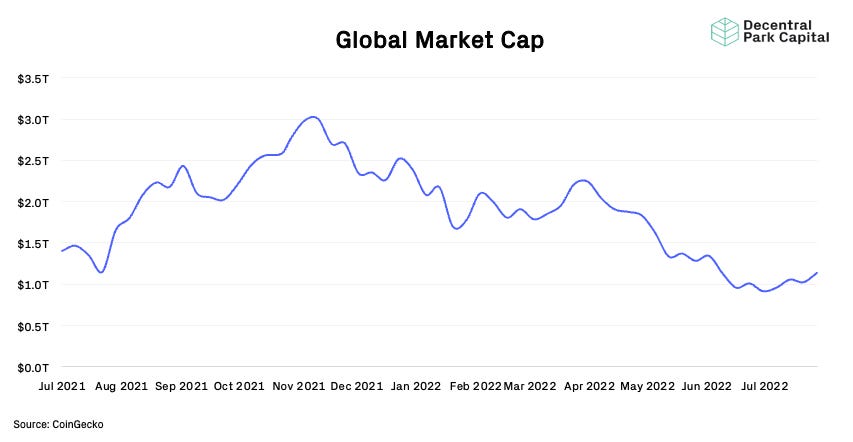

Global Market Cap

$1.13T; Global market cap has grown 11% over the past week.

$50B; DeFi market cap has increased by 4% over the past week while DeFi dominance increased 5% indicating DeFi outperformance against the broader market.

Bitcoin Dominance

Bitcoin dominance continues to fall closer to 41% as ETH and other assets down the risk continuum outperform. Possible reversal set up as indicated by momentum signals on the daily.

BTC/USD and ETH/USD

BTC/USD facing resistance at $25k while ETH/USD challenged at $1.8k. Both daily RSIs are hovering near overbought levels but are not in extreme territory.

ETH/BTC

ETH/BTC challenged at 0.075 with declining spot volumes. Momentum indicators signalling overbought levels (RSI D 68) with bearish divergence set up. Possible weakness this coming week with positive headlines likely needed to maintain current momentum trajectory.

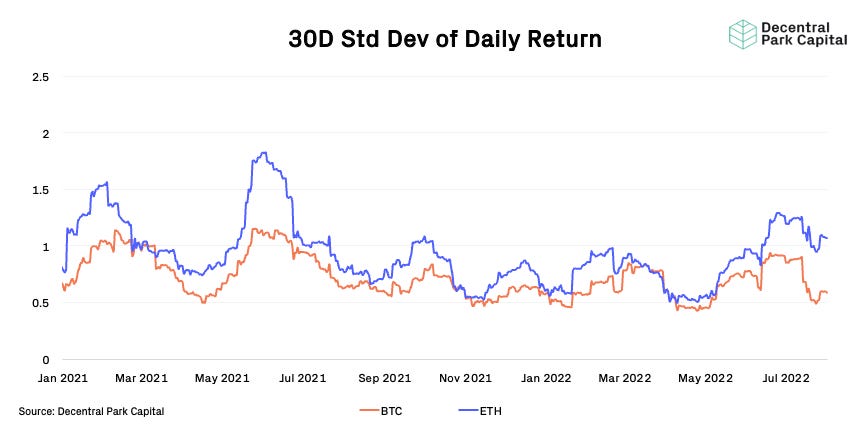

Volatility

Realized volatility for both BTC and ETH falling below July highs. Expectation is for higher volatility over coming months driven by the macro piece. Implied vols were largely sold off on the generally range-bound price action.

Paradigm note an increase in short-dates tied up call in size last Friday and could indicate relative bullishness of BTC vs. ETH (underperformed by 40% past month) or more constructive macro outlook.

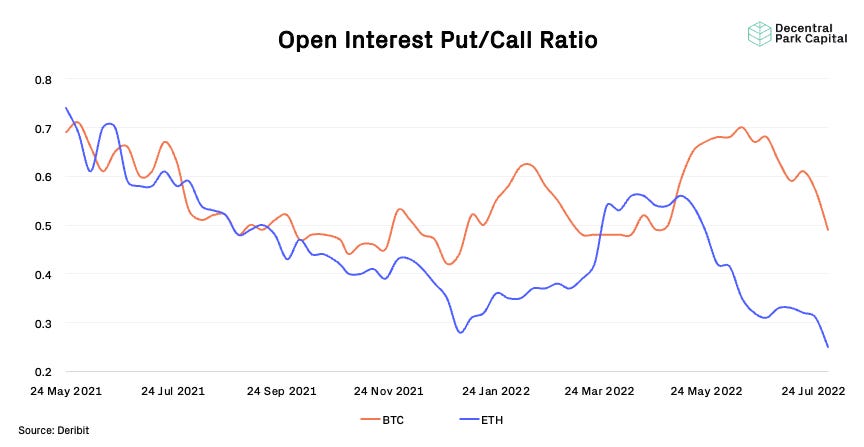

Trader Positioning

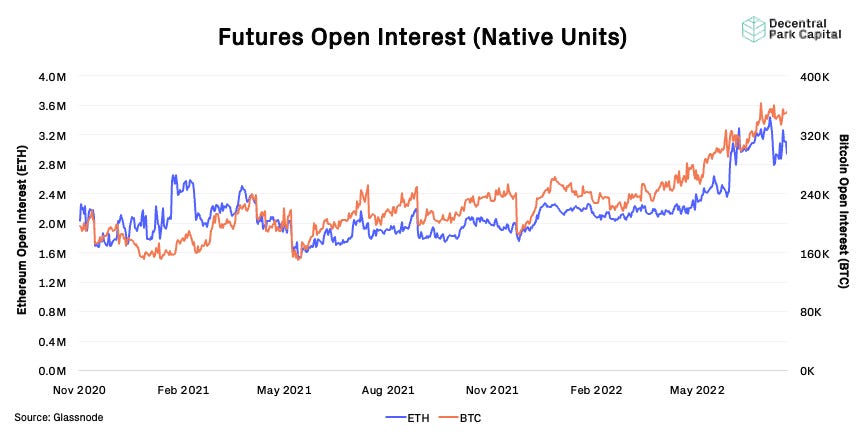

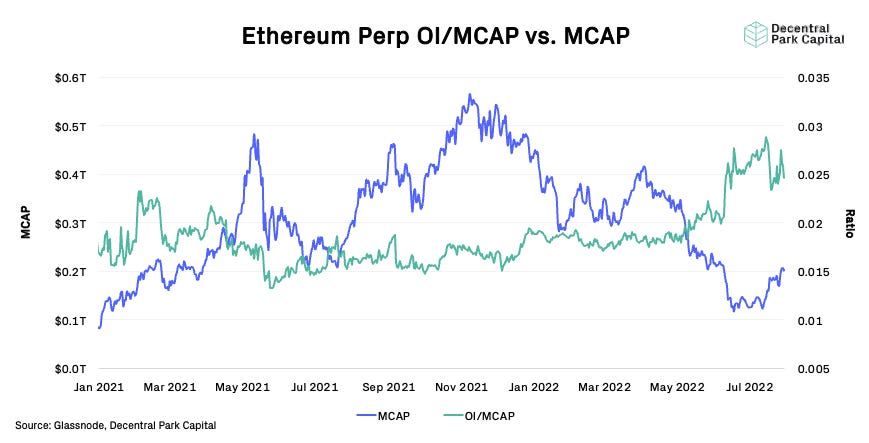

Market seeing a decline in put/call ratio for both BTC and ETH. Positions favouring calls over puts could sign renewed positive sentiment for the cryptoasset market (proxy for bullish momentum). Futures open interest (native units) taking a breather for both both markets too (529k BTC and 3.87m for ETH respectively). ETH OI/MCAP retreating from ATHs as perp speculation outpaced MCAP growth but the ratio still remains elevated.

Combined Order Books

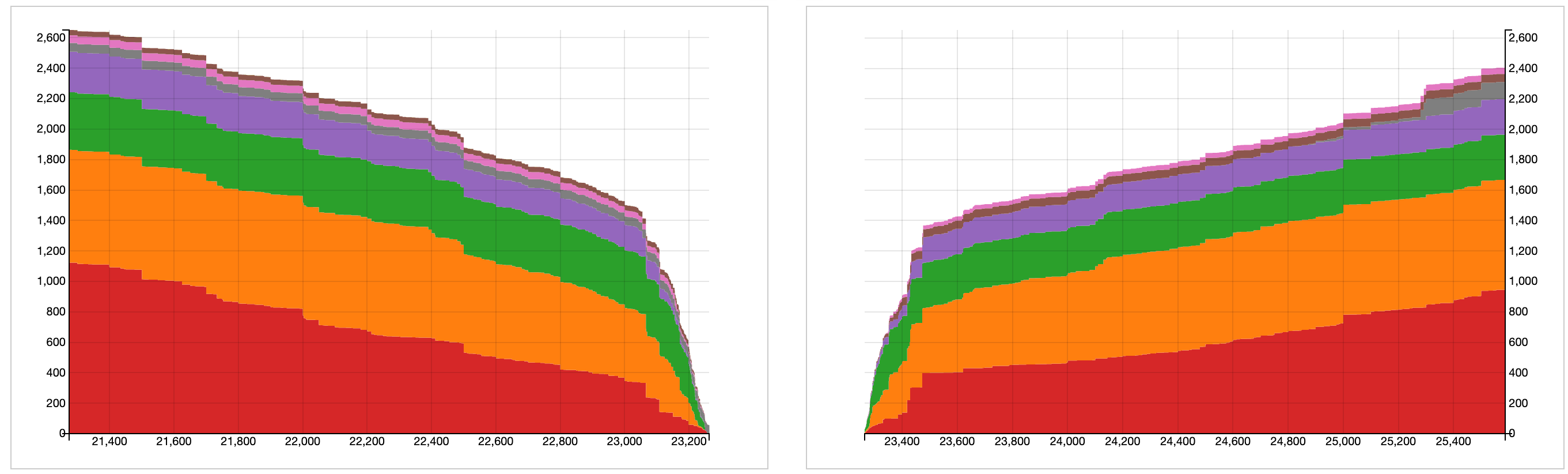

Order books look slightly heavier on the bid side. Heavier resistance up to ~$22.2k.

Macro Correlations

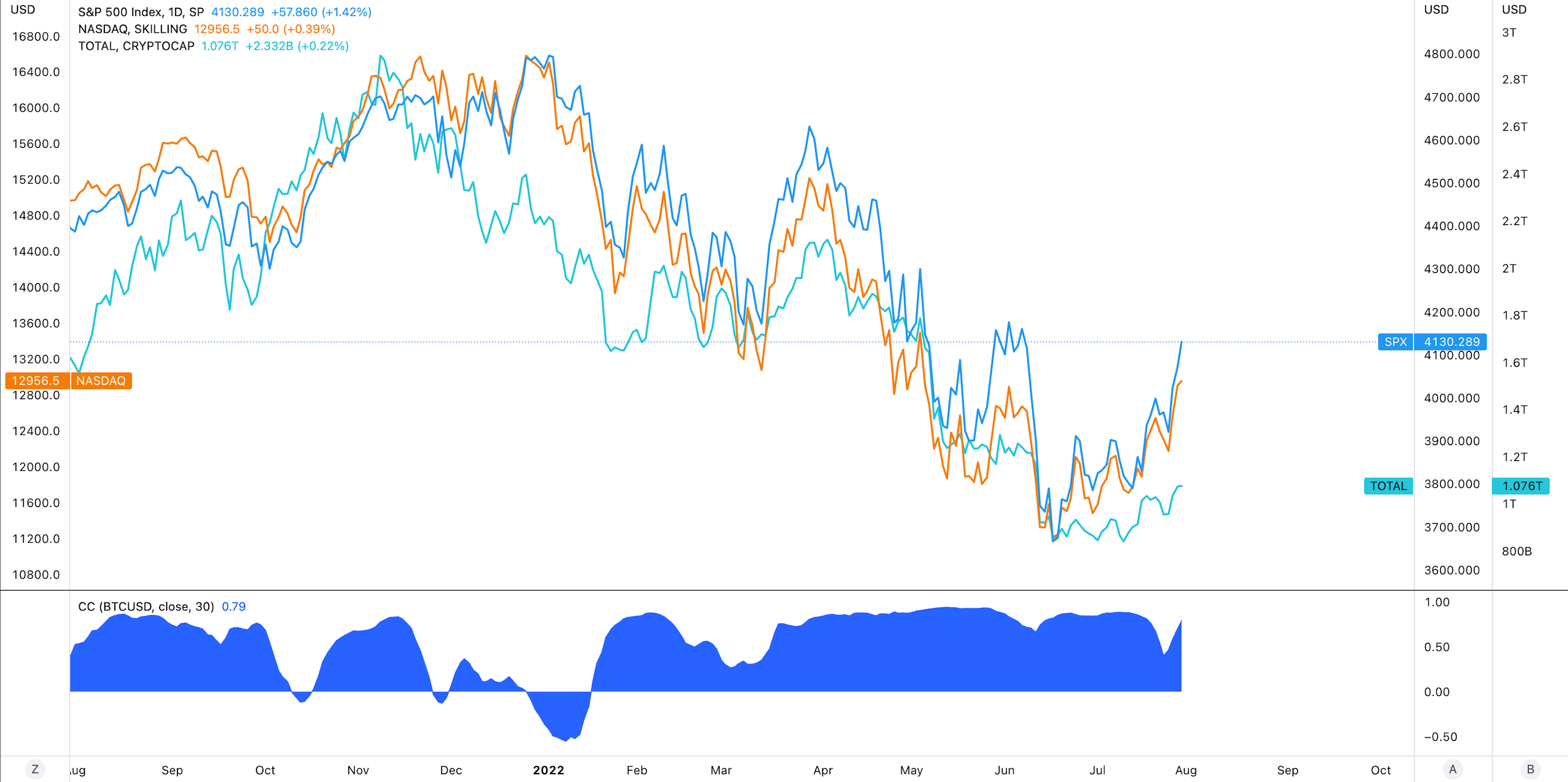

Crypto vs. Equities vs. Gold vs DXY; Cryptoasset correlations with broader risk markets kept high (~0.88). Higher volatility in SPX and NASDAQ from FOMC decisions trickled over into the cryptoasset market over the past week. NASDAQ futures down 25 BPS to open the week as market assess recession risk.

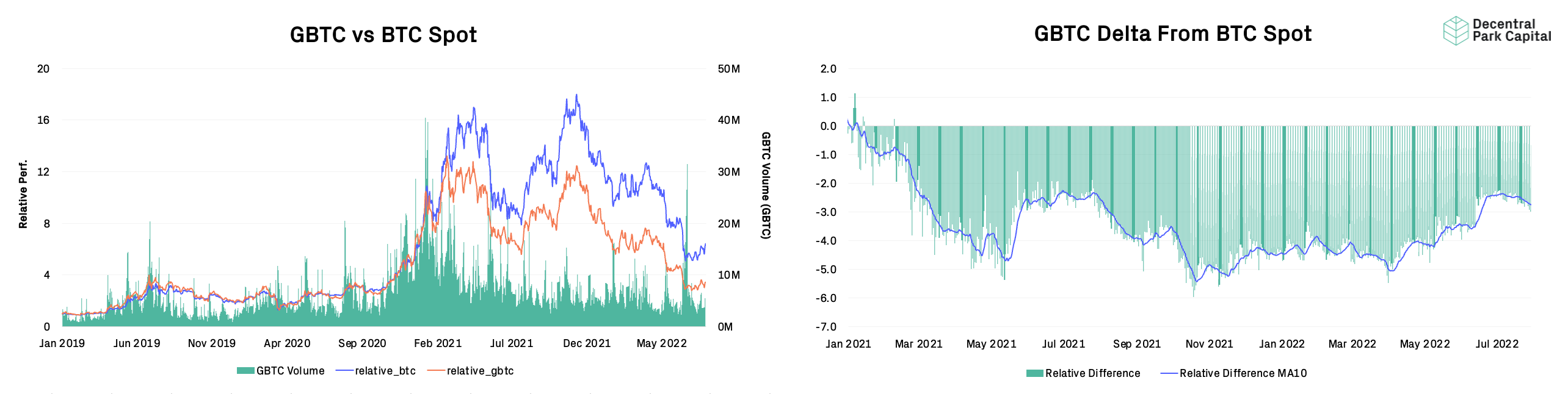

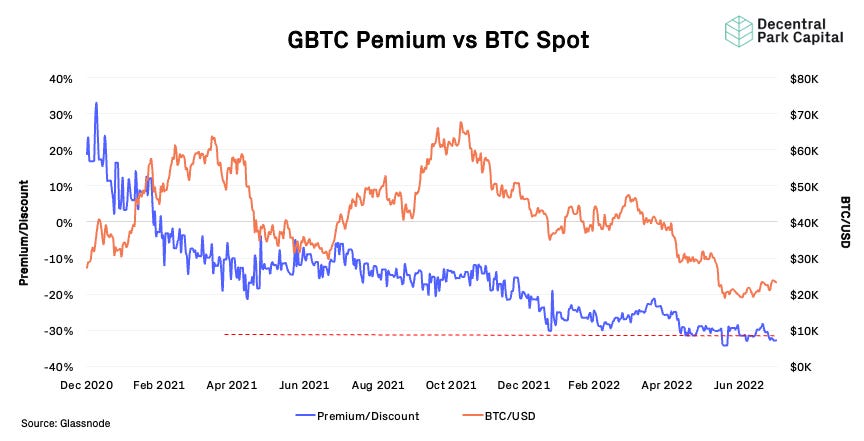

Trusts

GBTC; GBTC discount widening and broken recent support line (31.3%). GBTC 30D volumes are starting to fall off a cliff (6.7M) falling 10% from last week.

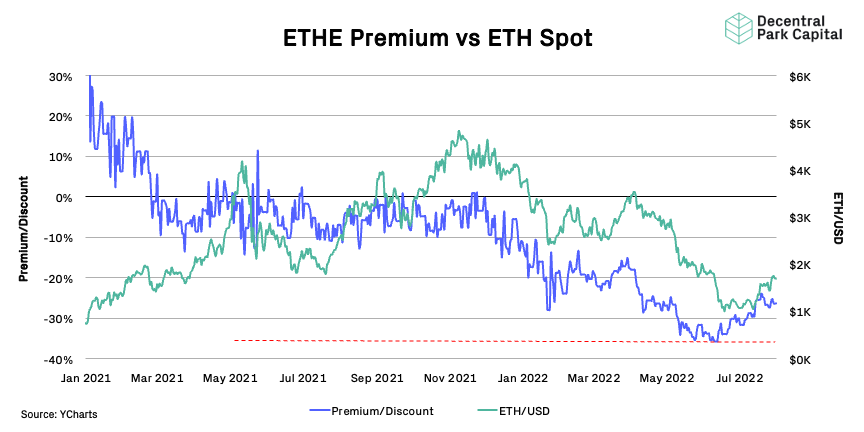

ETHE; ETHE discount narrowing in line with spot indicating stronger demand as the merge narrative picks up. ETHE 30D volumes are also starting to fall (4.6m).

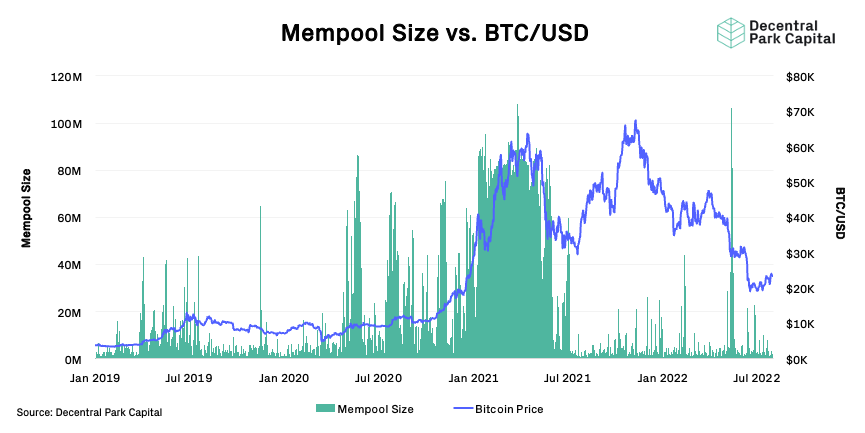

Mempool Size

No notable increase in mempool size meaning demand for block space is relatively low.

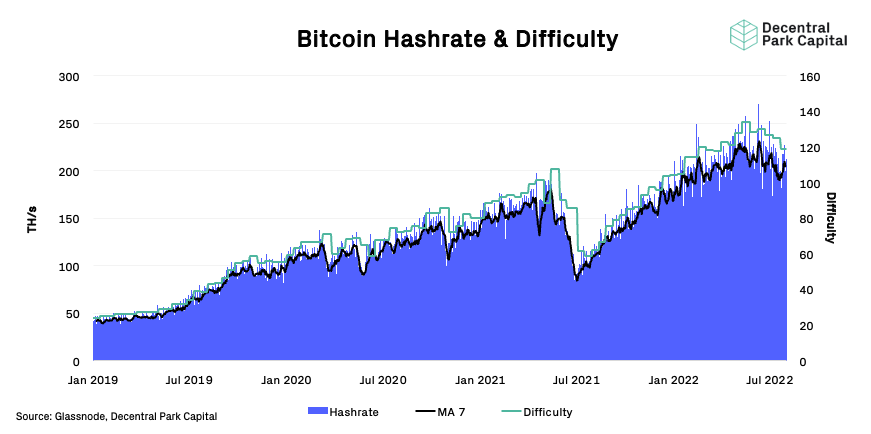

Bitcoin Mining

The Bitcoin hashrate trend has recovered over the past week (7D MA) but not convincingly broken out of its wider downtrend. Bitcoin difficulty is expected to adjust +0.5% in ~3 days. The hashrate recovery has not yet been strong enough to drive a ‘buy’ signal for the hash ribbons valuation metric for Bitcoin.

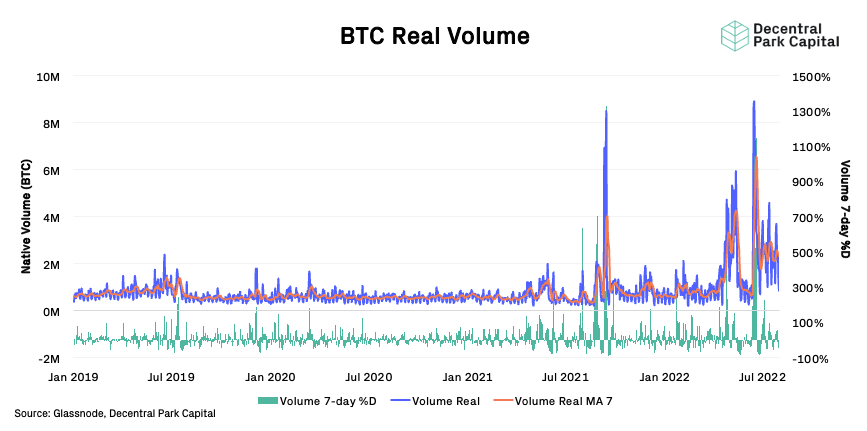

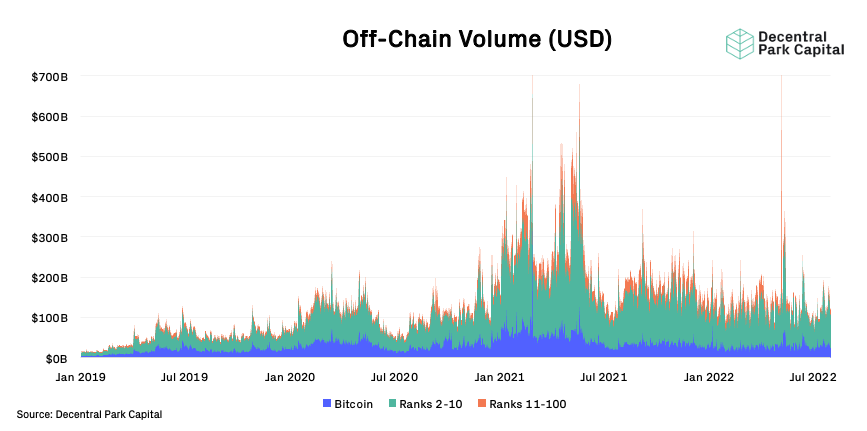

Volumes

On-chain real (BTC) & off-chain volume; On-chain volume has increased 4.5% while off-chain volume has been flat over the past week. BTC and ETH showing similar volume patterns over the past six months.

Exchange Flows

Bitcoin exchange flows have remained net negative with more units being withdrawn than deposited in aggregate. It remains unclear if this indicator will flip positive and how sustained this pattern would be if this was to occur.

📚 A16z Weekly [A16z]

📚 On Pivots [MacroAlf]

📚 Paradigm LP Letter Excert [Matt Huang]

📚 The Future of MEV [0xfbifemboy]

📚 Dimension of Web2 vs. Web3 [Antoniogm]

🎙️ On The Mania That Was Even Bigger Than Meme Stocks [Odd Lots]

🎙️ Zooko On Privacy And Crypto History [Up Only]

🎙️ Why The Inflation Is Over Rally Will Fall [Real Vision]

🎙️ E:89 GDP growth negative in Q2, layoffs [All-In]

🎙️ The Chopping Block: A Network State in 10 Years? [Unchained]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.