The Weekly #203

Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below.

Staring Down The Barrel Of The Macro Gun

We can see that US households are dipping into savings after they stockpiled $2.7T since the start of the COVID-19 pandemic.

To counter the income problem from an economic shutdown, households has a level of reliance on stimulus checks and child tax credits. The issue now is that the concern has now reversed with record inflation, high costs, and wages failing to keep up with those higher costs.

Personal saving has plummeted to 5.4% - the lowest level since 2009.

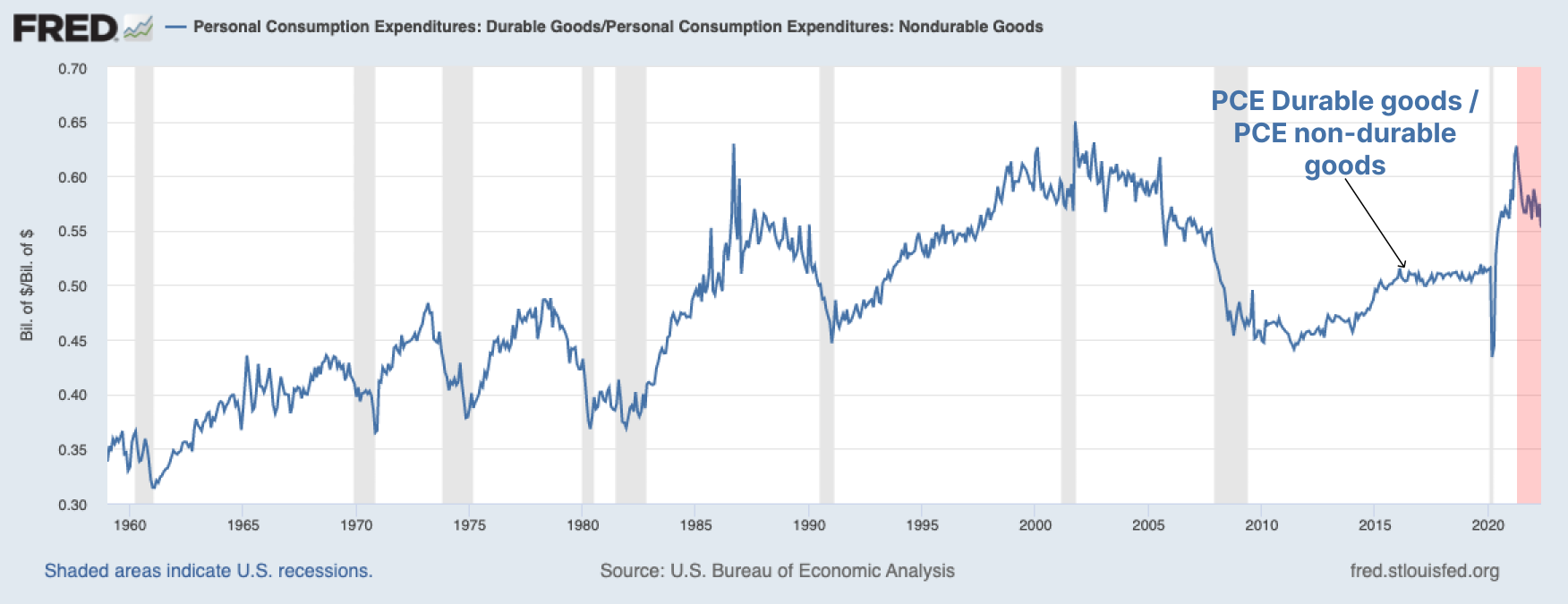

The rate of change of disposable income highlights the problem even clearer. There are now signs that retail sales are now rolling over with individuals perhaps being more selective in what they choose to purchase (e.g. durable goods and in size).

{kind=link}

We are already seeing the potential effects on GDP. Earlier in July, U.S. GDP shrank 1.6% during the first quarter of 2022 amid softening personal consumption expenditures.

ISM also dropped to 53 in June, from 56.1 indicating a clear slowdown in the goods producing sector and a signal of the looming recession down the road. Shortly after the release of the ISM data, U.S. treasury rates took a turn to the downside and, while taking a breather, bond yields are looking for higher ground.

There are signs of commodities like Oil (key inflation driver) rolling over but not everyone is convinced a retreat back to $60/barrel in on the card near-term.

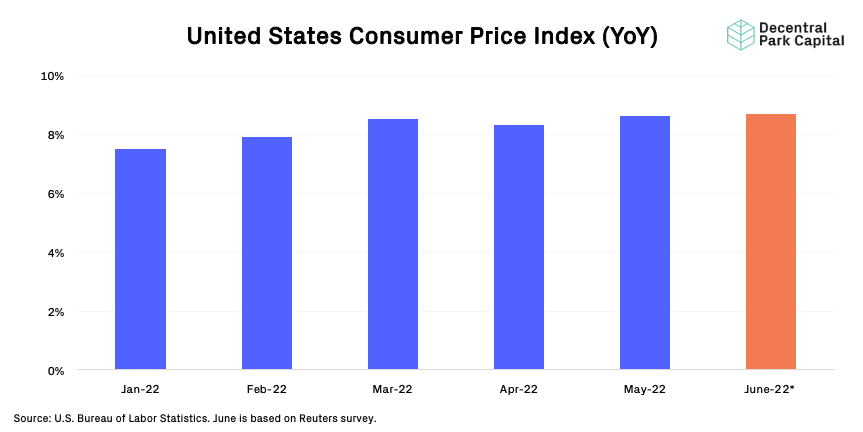

This week is a crucial week for the macro calendar too. US inflation data is expected to be released on Wednesday with Reuters survey indicating a 8.7% YoY change, up from 8.6% in the previous month. A higher-than-expected print may be the driver for higher bond yields and stronger dollar.

In the words of James Knightley (Chief Economist at ING Financial Markets):

“Inflation is likely to move even further above target this coming week as gasoline, food, shelter and airline fares continue to rise apace,” said James Knightley, chief international economist at ING Financial Markets.”

Inflation was “projected” to peak in March but what is becoming clearer is that inflation is here to stay and The Fed’s path for ‘demand destruction’ will be a long one.

So as a high percentage of households are at risk of financial distress heading into Winter, the expectation of large speculative investing down the risk curve over the coming months seems misguided.

This may be the case for the arguably the most speculative market sector of them all - NFTs - which saw a boost shortly after the rate of disposable income spiked and subsequently fell when savings became squeezed.

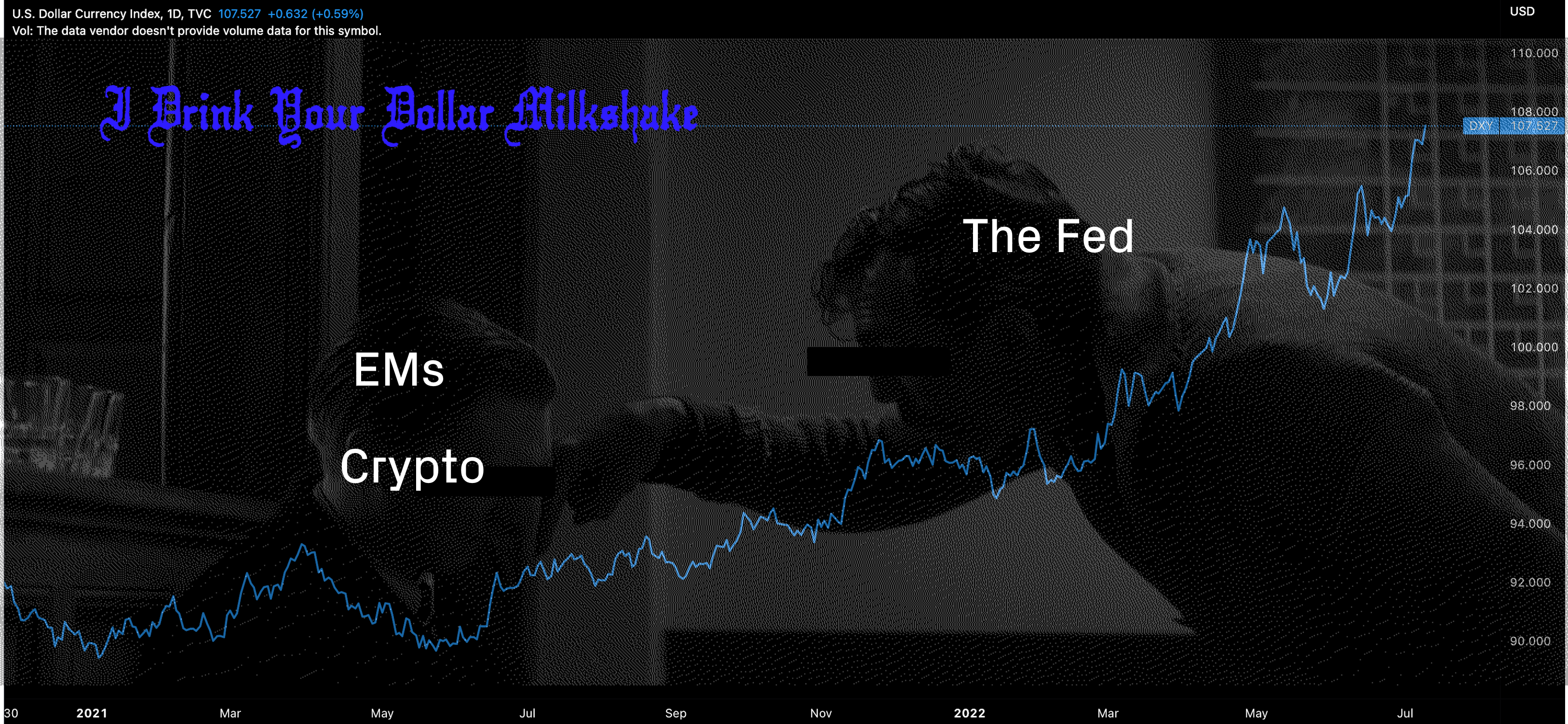

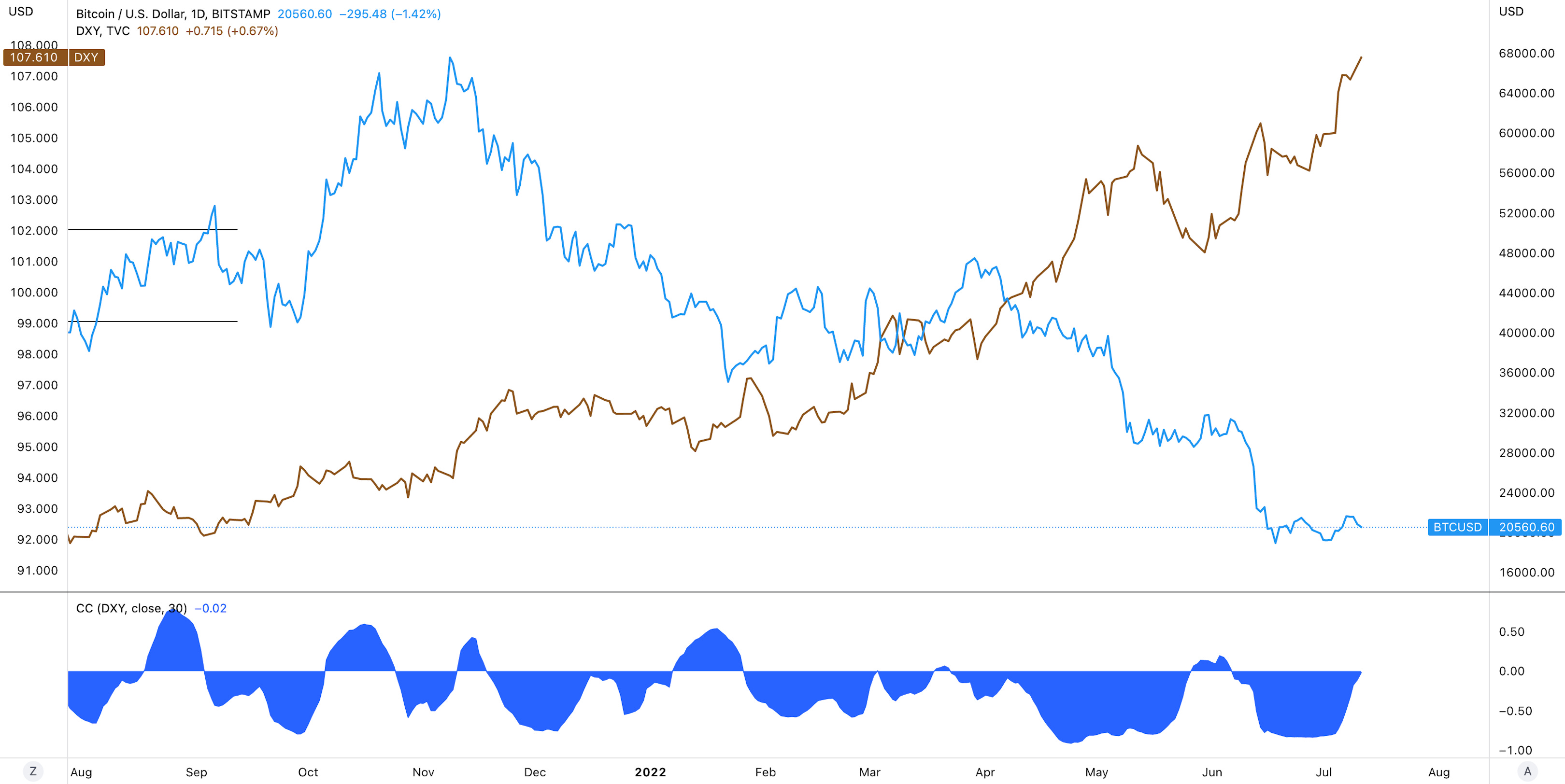

Crypto has other challenges too. The dollar is also getting stronger due to a number of factors including global debt market dynamics, global liquidity reduction, rate speculation, and QT. Its impact is painful for both emerging markets and cryptoassets, albeit for different reasons.

MSCI’s index of emerging market (EM) currencies slipped 0.2% and further rate hikes in the US and runoff on the balance sheet could worsen the outlook for already battered EM assets.

The DXY has printed a new 20 year high and shows little sign of slowing down near-term. As we’ve stated in previous editions of The Weekly, the path to a strong dollar was a key, ongoing risk to cryptoassets which are predominantly denominated in the greenback.

The ‘Dollar Milkshake’ is being drunk and the Fed is thirsty.

Price Action

Majors like BTC have oscillated just above key levels ($20k) with the 20d MA around $20.4k. Realized volatility has been lowered as a result and macro catalysts like CPI prints may re-introduce volatility back into the picture. Add earnings season on top and we have a turbulent flight ahead.

Recent profit warnings of large companies have investors worried about wide price downgrades driven by high energy costs, reduced consumer spending and exports.

Crypto maintains its strong positive correlation to US equities with this week’s opening price action for crypto being driven by the broader risk markets once again (e.g. ES1!).

Several indicators including Hash Ribbons have yet to signal ‘BUY’ after Bitcoin miners experienced a prolonged period of capitulation. We would need to see signals of stronger upwards price momentum which seems challenging given the market and macro set up.

Even crypto money managers are unclear on where things stand - we all want to believe the bottom is here but the reality is the macro storm is taking us into uncharted territory.

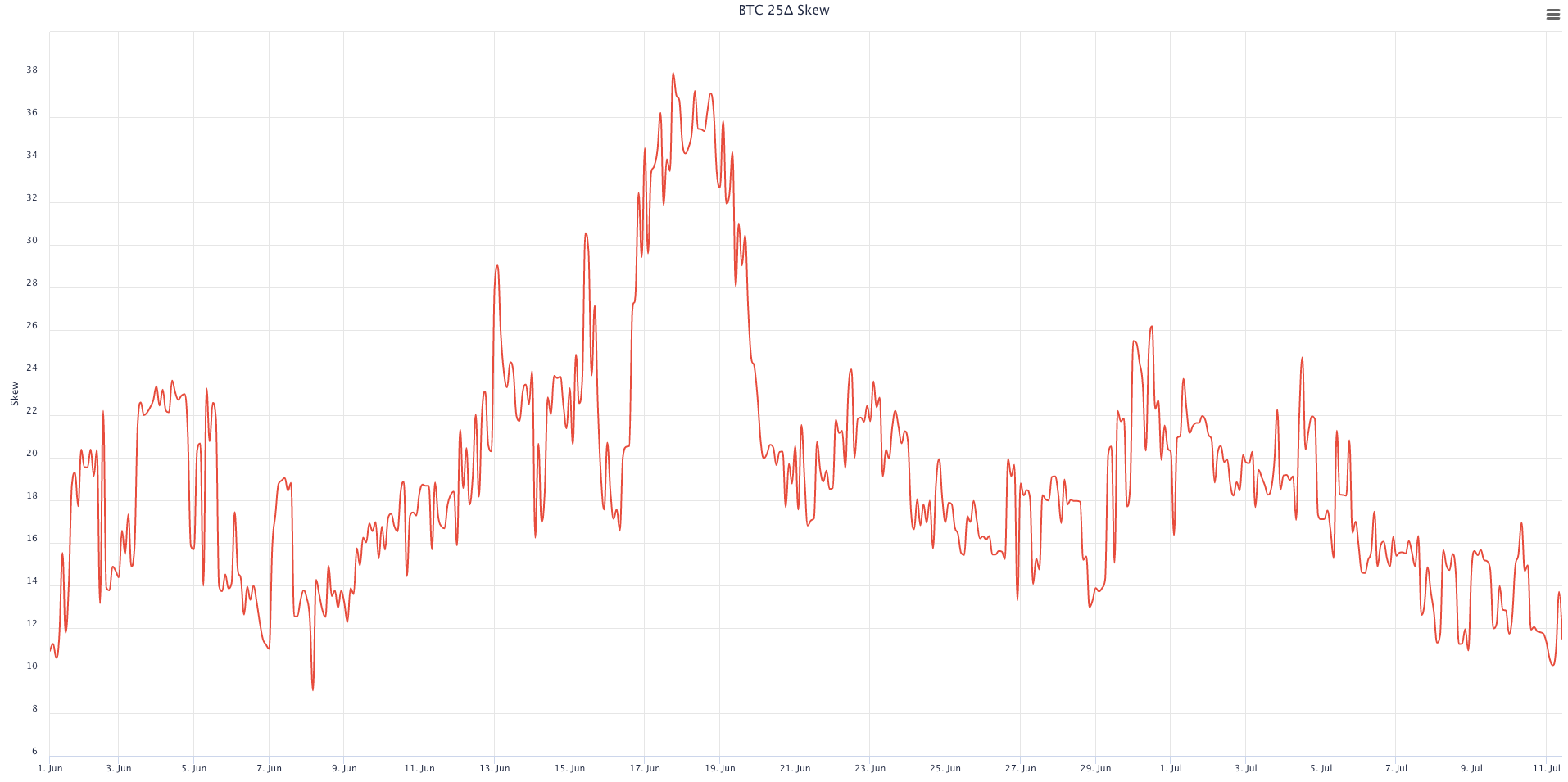

The Bitcoin options market signals a level of reluctance. Bitcoin’s 30-day options 25% delta skew has been falling since June 18th peak when traders were particularly bearish. Still, current skew at 12.6% indicates some trepidation.

You could also argue that closure of on-chain debt positions within DeFi has alleviated some concern in the broader market. Celsius has now reclaimed $440m of collateral after fully repaying their MakerDAO loan. So far, DeFi protocols have worked the way they were intended to.

Still, DeFi activity also shows a level of inertia. The DEX/CEX ratio has fallen to 10.6% down from its annual highs of 16.4% as on-chain exchanges are used less relative to their centralized counterparts.

Given the macro is still weighing heavily on speculative activity, on-chain usage within DeFi will likely continue to cool off.

Top performing assets have often been event-driven including Aave’s release of GHO stablecoin and Messari’s release of the State of Uniswap Q2 2022.

Top 100 (7d %):

Quant (+38.5%)

Aave (+33.3%)

Internet Computer (+27.7%)

Uniswap (+25.8%)

Polygon (+20.8%)

DeFi Top 100 MCAPs (7d %):

Convex Finance (+41.6%)

GMX (+36.2%)

Aave (+33.3%)

Neutrino System Base (+28.2%)

Lido DAO (+26.1%)

Aztec Connect, a zero-knowledge network with native smart contract privacy, is live on mainnet. LPs can use Aztec to privately stake DAI in ElementFi (3.65%) or ETH in Lido (4.4%), more native integrations on the way.

Aave is launching a new decentralized, collateral-backed stablecoin called GHO. Users will be able to generate it after supplying collateral, AAVE stakers are promised a discount on launch.

Aura announced retroactive airdrop for users that staked AURA into vlAURA before June 30th, they are rewarded 3.61% of their staked amount.

Stake DAO updated their ETH Covered Call Strategy with 25% projected APR and added 17 new strategies for the Liquid Lockers covering almost all the Curve pairs.

Global Market Cap

$955B; Global market cap has gained 5% over the past week.

DeFi MCAP And Dominance

$39B; DeFi market cap has increased by 2% over the past week while DeFi dominance has increased 1% over the same period.

Bitcoin Dominance

Bitcoin dominance has fallen another percentage point over the past week to 43.4%.

BTC/USD and ETH/USD

Majors consolidating just above key levels (BTC $20k and ETH $1.1k). Daily RSIs firmly in neutral territory. No clear direction with what feels as a headline-driven market. No significant outperformance of ETH relative to BTC in lead up to potential merge in August.

Volatility

BTC & ETH; Flat realized vol for both BTC and ETH as price consolidate. Possible uptick in vol around CPI print later this week. No notable uptick in BTC ATM IV (7D).

Trader Positioning

Diverging trends in put/call ratio for BTC and ETH. Traders taking an increasingly bullish stance for BTC while little change for ETH. Funding rate have flipped negative over the past day after being moderately positive. For options, $25k strike was most active BTC strike on Paradigm last week (outrights and call spreads).

Combined Order Books

Order books look slightly heavier on the bid side. Heavier resistance up to ~$20.7k.

Macro Correlations

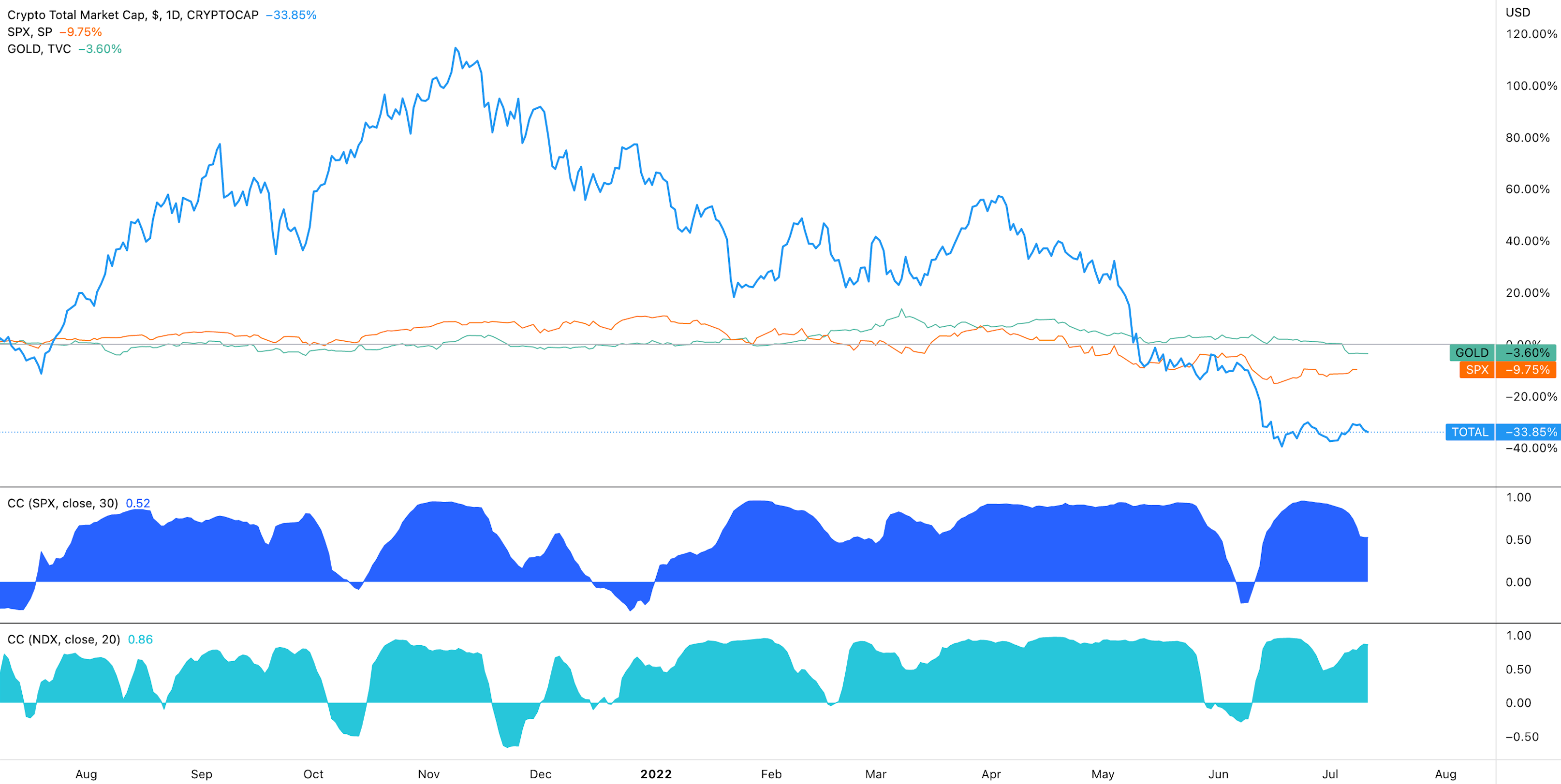

Crypto vs. Equities vs. Gold vs DXY; Cryptoassets remaining positively correlated to equity indices like SPX and NDX. Crypto’s correlation to DXY has reduced which has historically lasted briefly before returning to a strongly negative relationship. Either crypto is holding up well despite a stronger greenback or we have yet to see knock-on effect trickle down to the market.

Trusts

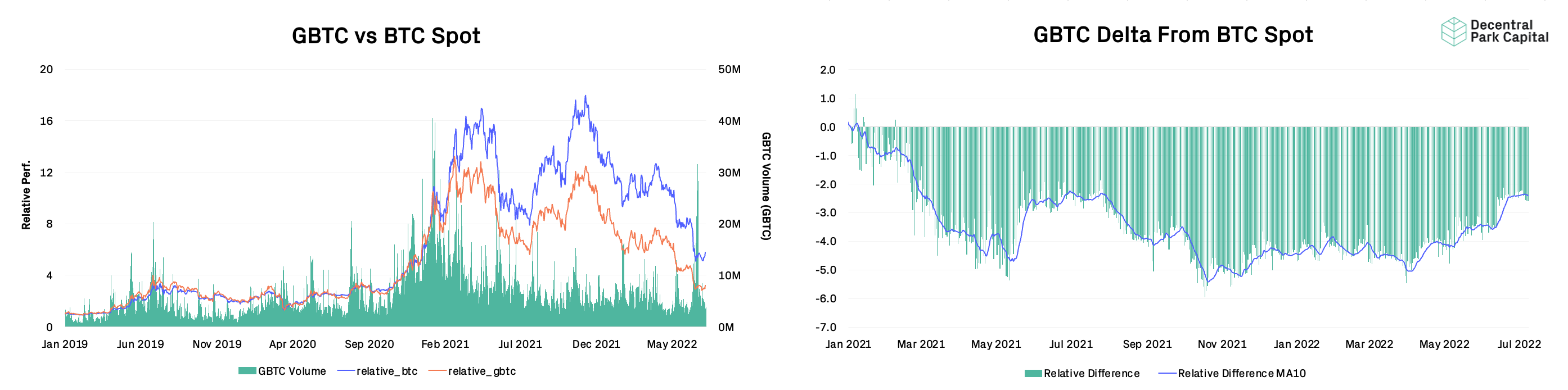

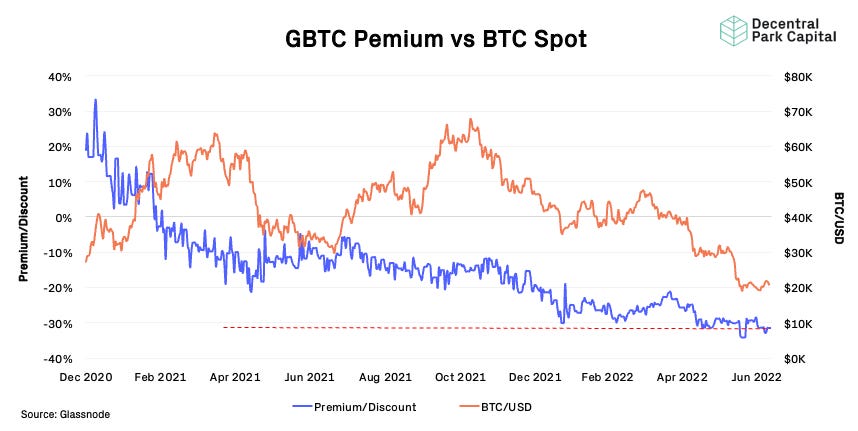

Grayscale GBTC

GBTC; GBTC discount still persisting (30%) and hovering around historical floor. GBTC volumes are up 80% since from its April/Annual lows (7.2M).

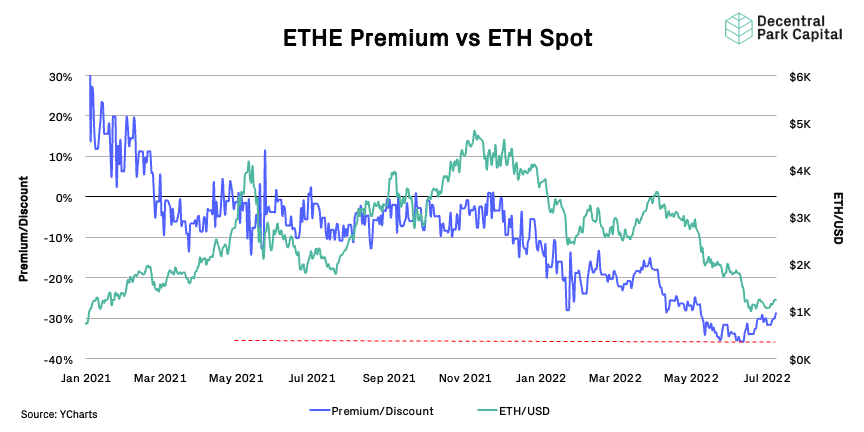

Grayscale ETHE

ETHE; ETHE discount is narrowing, back below 30% indicating renewed demand for ETHE shares in the lead up to the potential merge. ETHE 30D volumes are up >100% since April/Annual lows (4.9M).

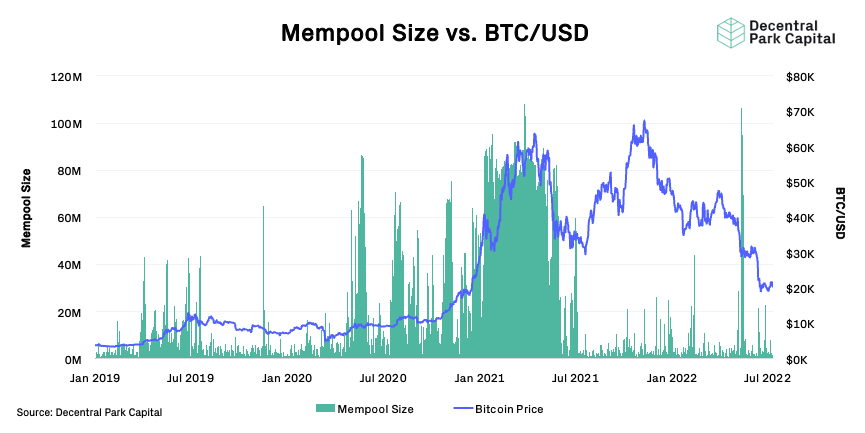

Mempool Size

Moderate uptick in mempool size as larger transactions force a growing number of smaller transactions to the pool.

Bitcoin Hashrate

Bitcoin hashrate has now dropped more than 11% from its ATH as miners start capitulating. Network difficulty has dropped 1.4% in response to falling commitment of hash power. The aggregate cost of minting 1 BTC has fallen to about $15k from $20k creating a new potential local floor in BTC price.

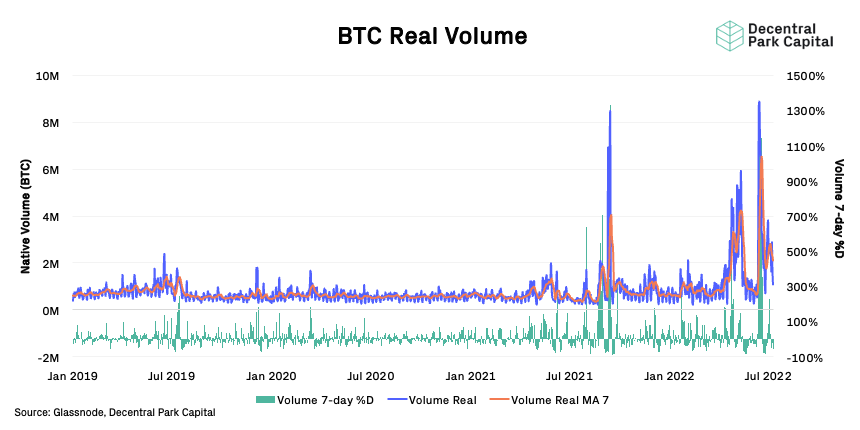

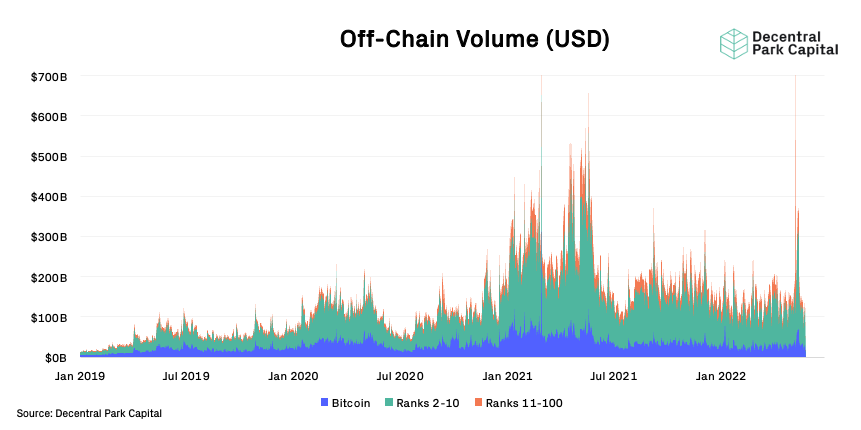

Volumes

On-chain real (BTC) & off-chain volume; On-chain volume has fallen 21% after previous on-chain liquidations occurred on-chain. Off-chain volume is up 2% over the week but still down 40% YTD.

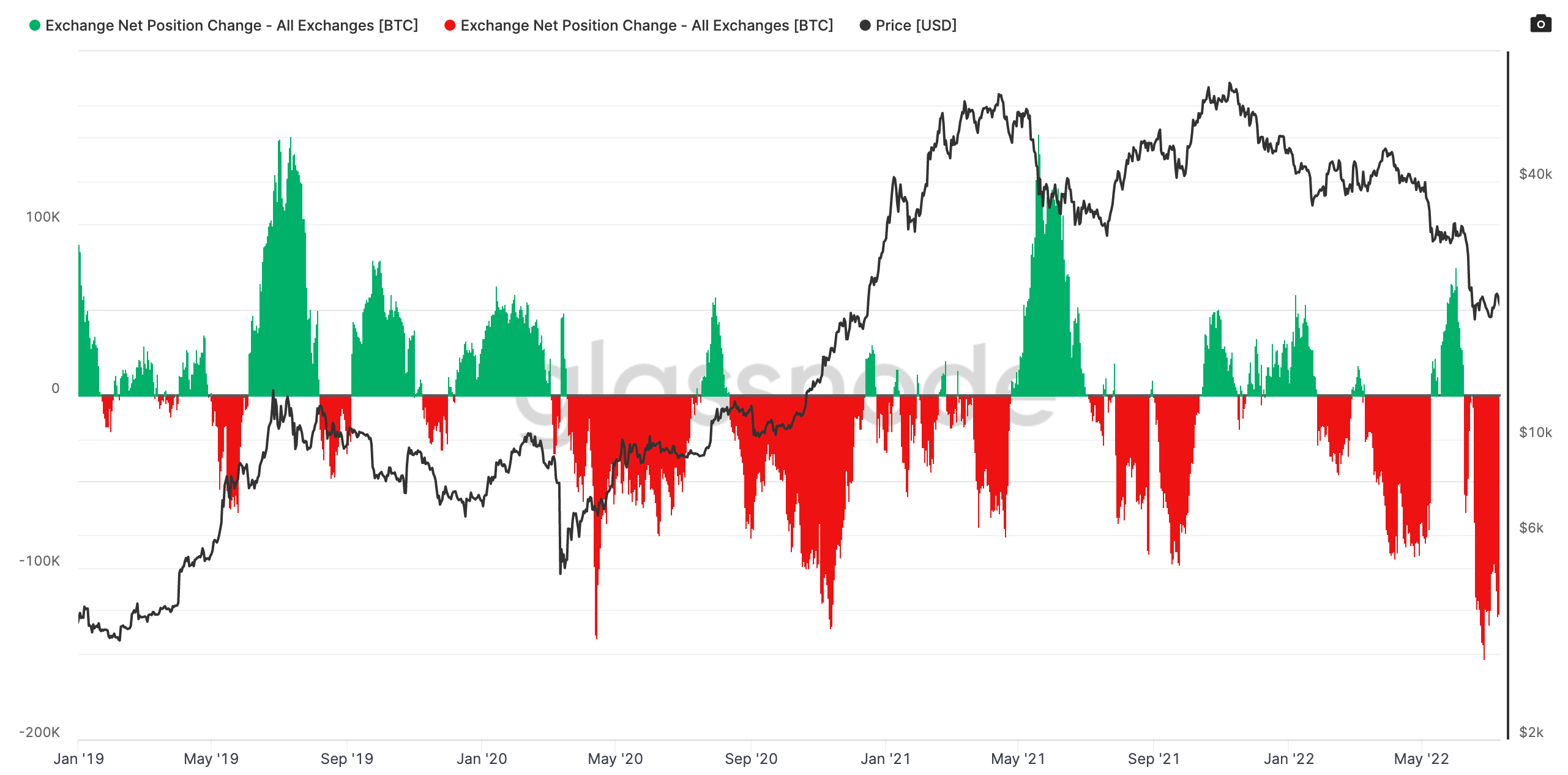

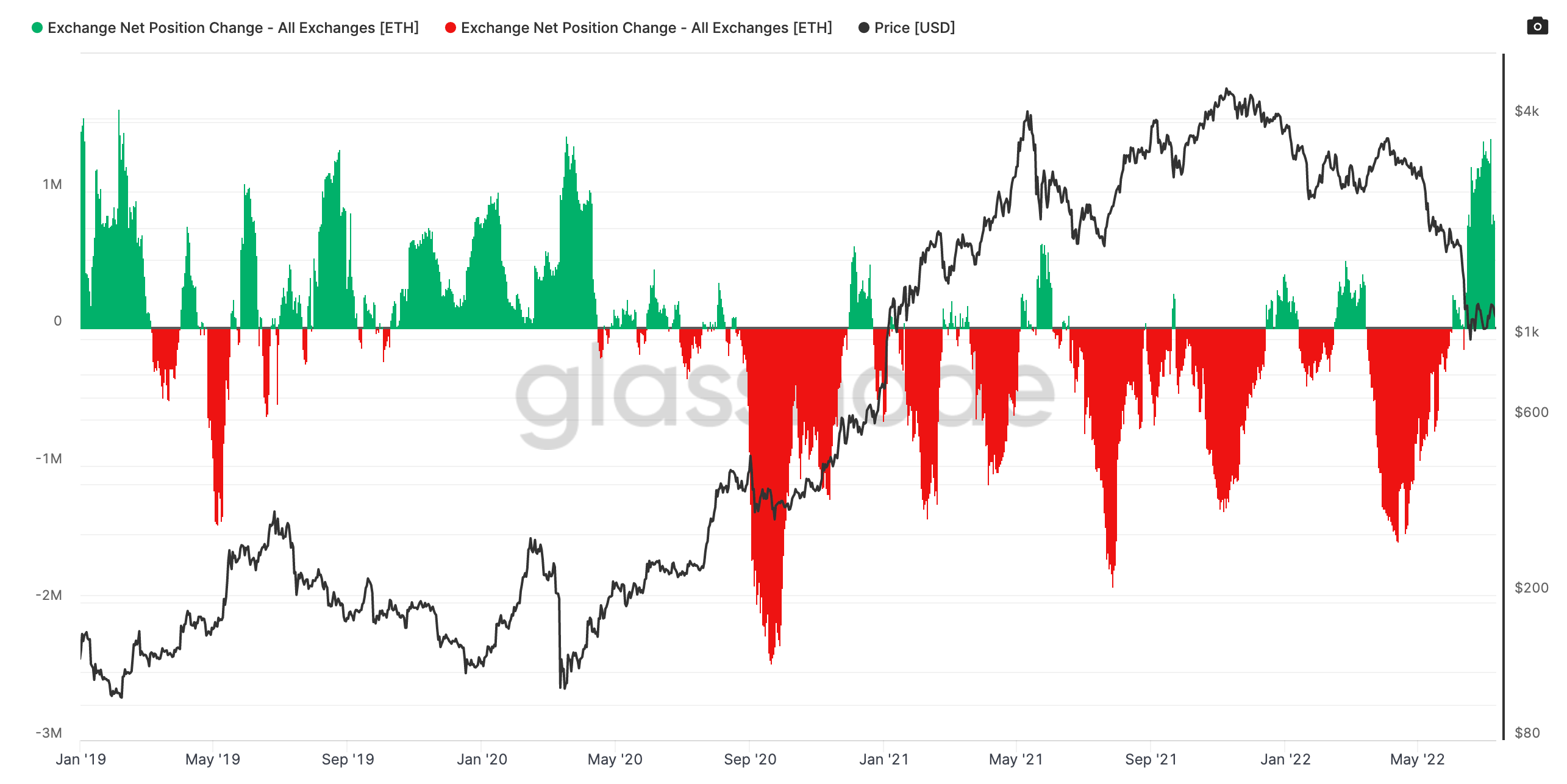

Exchange Flows

Net outflows from exchanges for BTC still strong. Opposite trend for ETH where exchanges are continuing to see strong net inflows of ETH. Divergence in exchange flows has yet to translate into signifiant divergence in spot price action.

📚 Mixed Messaging in Crypto [Chris Burniske]

📚 Financial Trouble in the UK [Bloomberg]

📚 The Case Against Oil Drop [Lyn Alden]

📚 Summer Reads [A16z]

📚 L1 Rotation Thesis [ChainLinkGod]

🎙️ WSJ Calls Out SEC Chairman Over Crypto [The Breakdown]

🎙️ Is This The End? [Bankless]

🎙️ Weekly Roundup Ep 333 [On The Brink]

🎙️ Macro Outlook [All-In]

🎙️ Why The Bond Market Has Been So Volatile [Odd Lots]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.