The Weekly #202

Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below.

In The Eye Of The Storm

Market expectations for a break down in BTC below $20k was short-lived as the cryptoasset found strength heading into the $2.25B options expiry last week.

The vast majority of the open interest was kept between $20-$30k. If Bitcoin’s price was below $21k, only ~2% of the call options would have been valued. While difficult to say whether the bears were the sole driver of BTC’s price action, it is reasonable to think BTC traded range bound around key levels like $20k once June 24th options were finalized.

BTC still trades below its 200W MA but has been edging higher in recent days. It remains to be seen how long this momentum can continue against an increasingly uncertain macro backdrop. For now, recent price action seem to be as-expected relief from the intense sell-off the week before last.

Market moves like this serve as a reminder that fundamental macro headwinds are still very much at play.

Last week, Jerome Powell testified before the Senate Banking Committee on policy and made it clear their path to 2% inflation was ‘unconditional’ but potential pain would be associated with that path, albeit not guaranteed:

“There will be expeditious progress towards higher rates”

“Recession likelihood is not elevated”

“Strongly committed to taming inflation”

“We want the housing market back on a sustainable path”

There are signals that the market believes recessions will drive central banks to reverse course swiftly. DXY (Dollar index) has fallen 1.81% from its annual highs which has largely been driven by a stronger Euro relative to the greenback (+1.7% since mid-June).

St Louis Federal Reserve President James Bullard took a more extreme view stating that recession fears are exaggerated and that the US economy was fine.

The market Brent (Crude) and US bonds appeared to follow a similar pattern. However, demand for the former seems to be sustained relative to supply while bond were sold off once again. Over in the UK, gas prices continue to reach new all-time-highs.

We have therefore yet to see a clear rollover in both commodities and bond yields with traders continuing to assess higher rates hikes and the risk it posses on the global economy.

While crypto remains challenged by this deteriorating market climate, we can still leverage a number of indicators involving key market participants that can point to the likelihood of a more sustained relief rally before a continuation of potential future drawdowns.

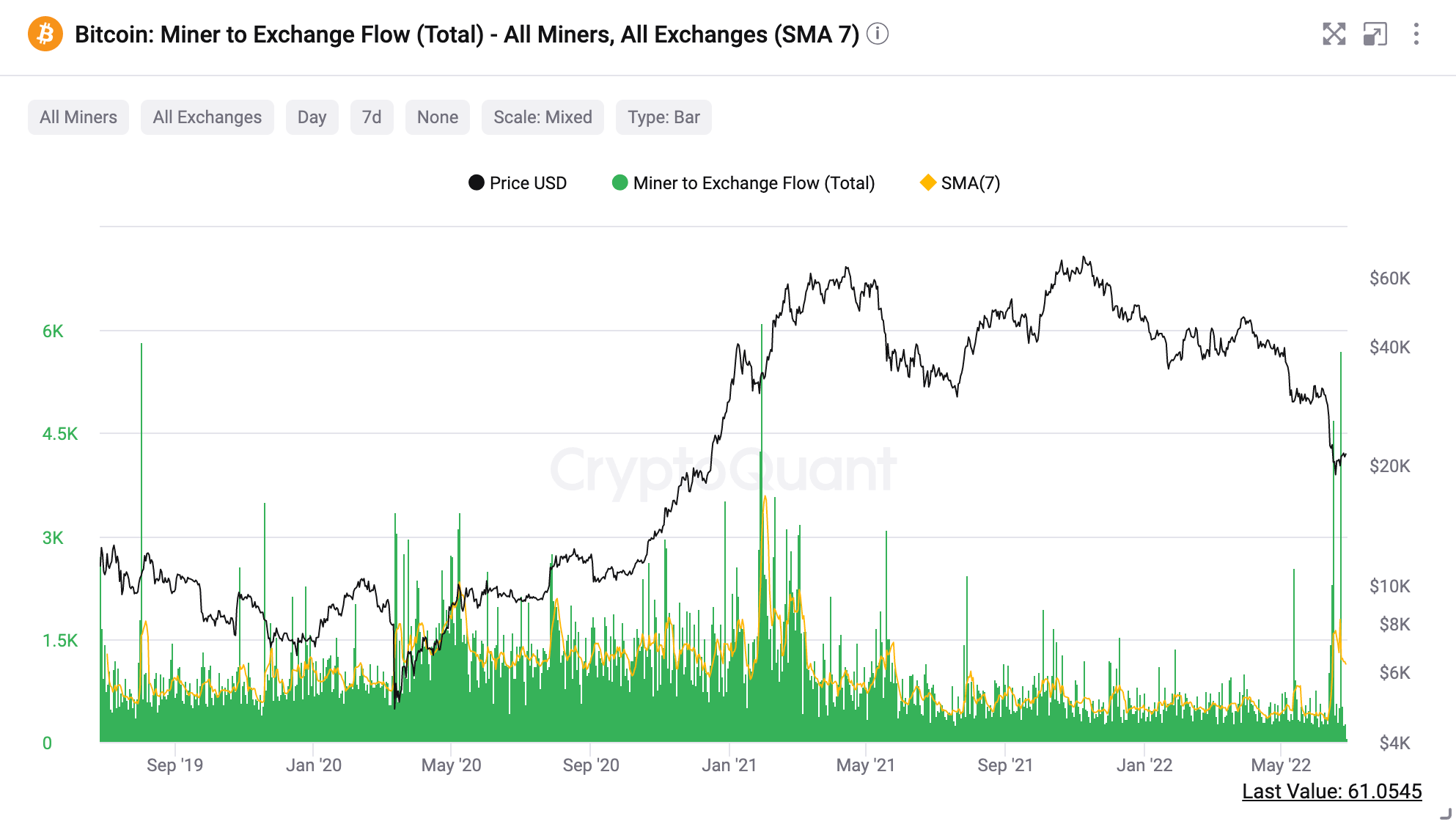

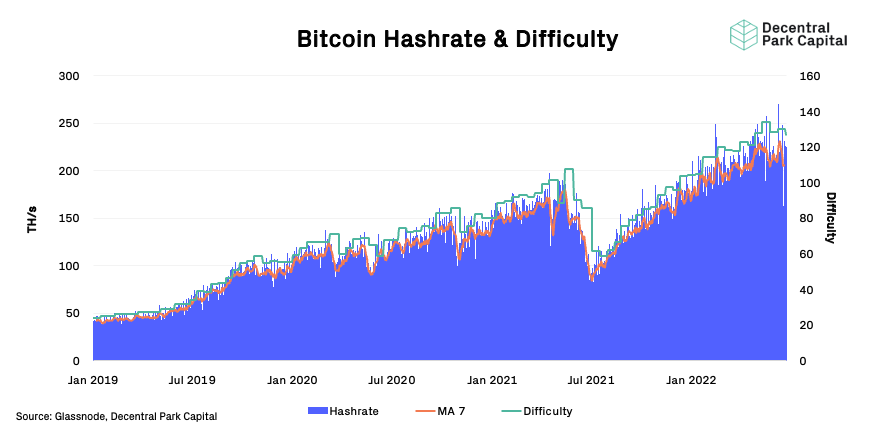

One is hash ribbons which has shown that miners (significant holders of BTC) are capitulating - defined by a bearish momentum of the network’s hash rate.

We may reasonably expect a more sustained spot rally to coincide with hashrate strength - as the involvement of miners as market participants mean things can become quite reflexive.

The average Bitcoin production cost is ~$20-$18k meaning that miners need BTC to trade close to this zone to break-even. It seems we are at an inflection point with miners clearly in distress. Miners have sold ~30% of their monthly production to the market.

More recently, we can see miners stepping up their selling as Bitcoin hash rate rolls over from its ATHs mid-June 2022.

Never have we also seen Bitcoin’s production cost remain so elevated while both hashrate and price are declining from their ATHs.

It seems something has to give.

Certain companies like Marathon are doubling down on buying BTC while not selling any minted BTC. A forced-selling scenario where BTC trades closer or below their production cost may mean miner dynamics gets worse before it gets better.

So it seems that the current environment is more challenging than supportive for miners unless we see spot demand that creates breathing room for them.

Identifying Ecosystem Risks

Liquidations

Distressed funds and companies have meant that large collateral positions were liquidated leading to BTC and ETH’s underperformance against the wider market.

In mid-June, forced selling of beta assets meant DeFi held up well on a relative performance basis. For the last week, DeFi continues to outperform beta but for different reasons.

We see a broad relief rally in crypto markets today where cryptoassets down the risk curve tend to outperform large cap names - business as usual. The net effect has been a continuation of a DeFi/BTC pair trade (+48% from annual lows).

A reversal in course remains a possibility in sharp, event-driven market correction but liquidations for beta assets can reverse the reversal.

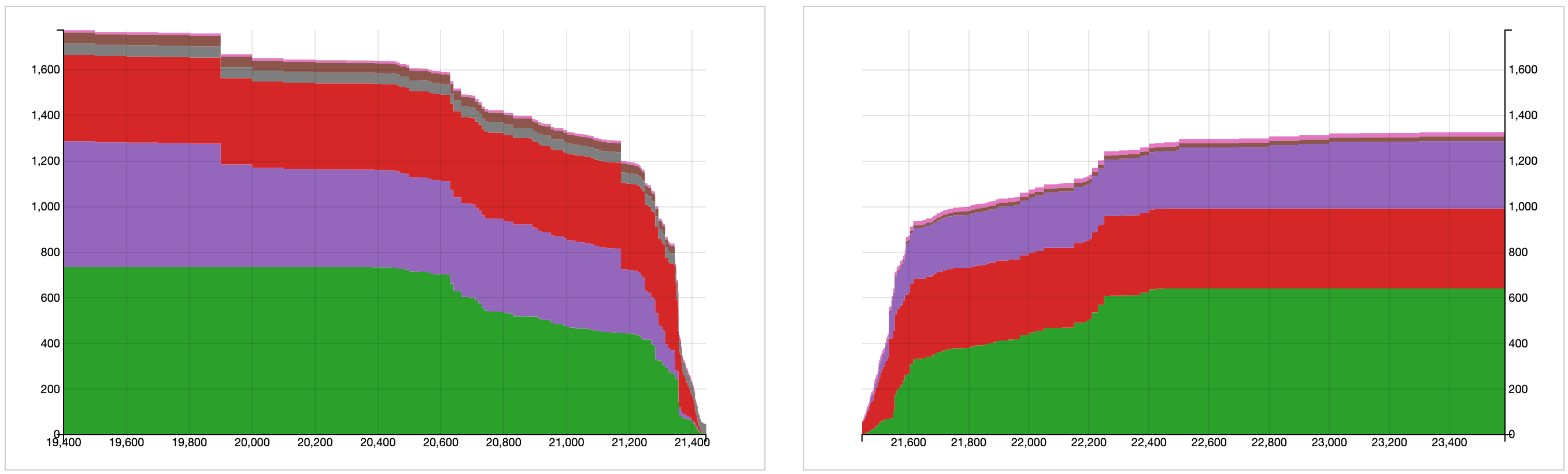

For now, the risk appears low with WBTC and ETH liquidation levels starting to become significant at 35% and 30% below current levels respectively.

But other risks remain in the wider ecosystem including stablecoin infrastructure where contagion could get us to those more extreme price levels.

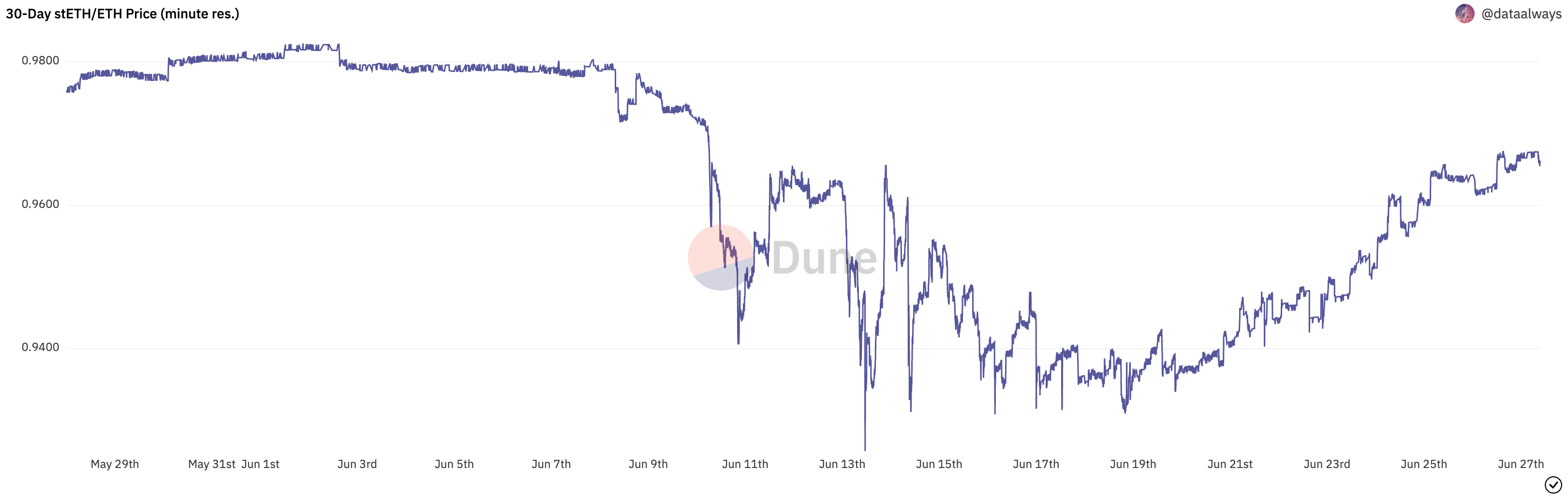

stETH

stETH/ETH has recovered well from its mid-June lows but it remains to be seen how much of the 3AC and Celsius fallout may reverse this trend down the line.

Curve’s ETH/stETH pool is more balanced with over 155k ETH now in the pool vs. 464 stETH. For now, contagion risk of a stETH/ETH ratio breakdown appears to have been lowered.

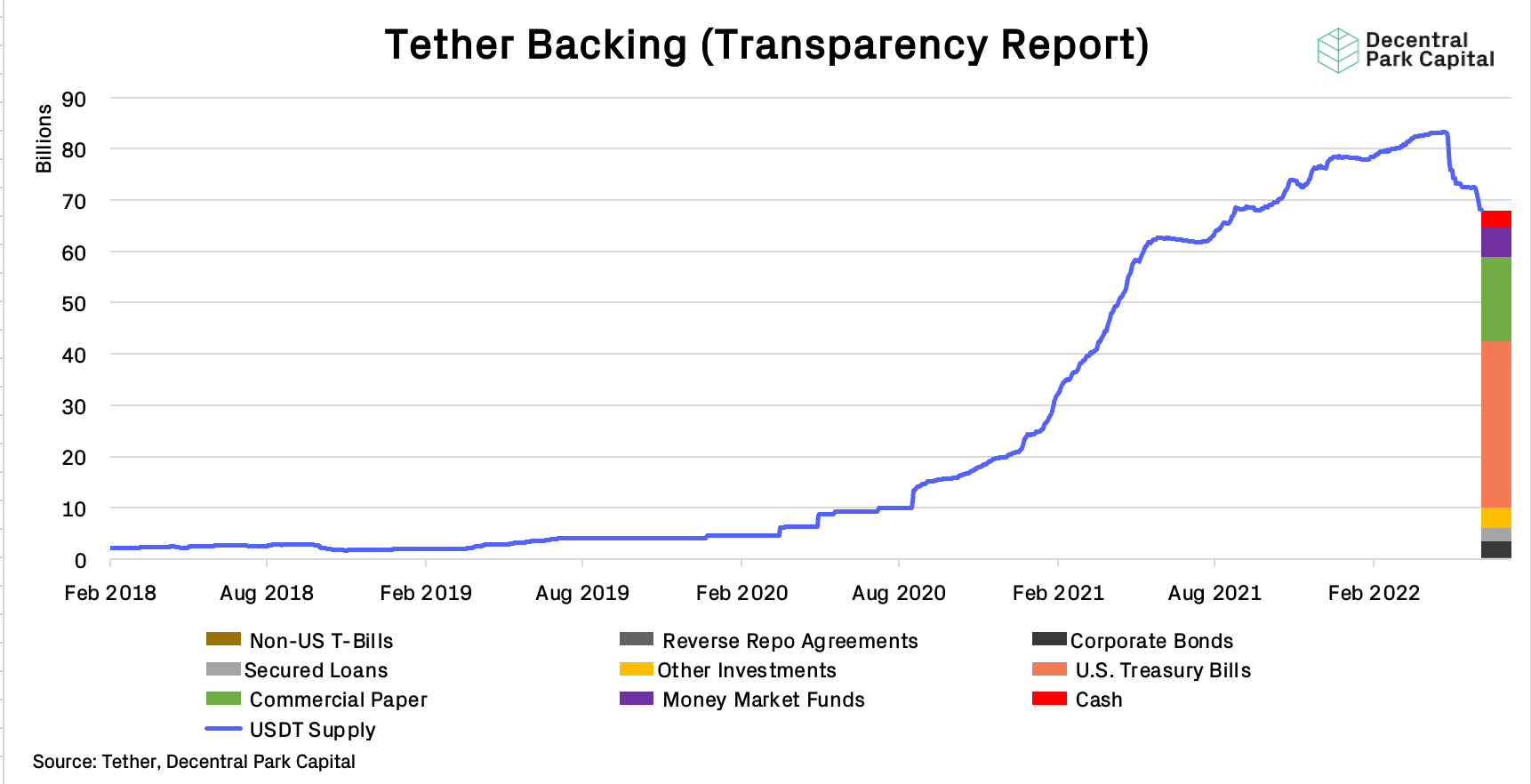

Tether

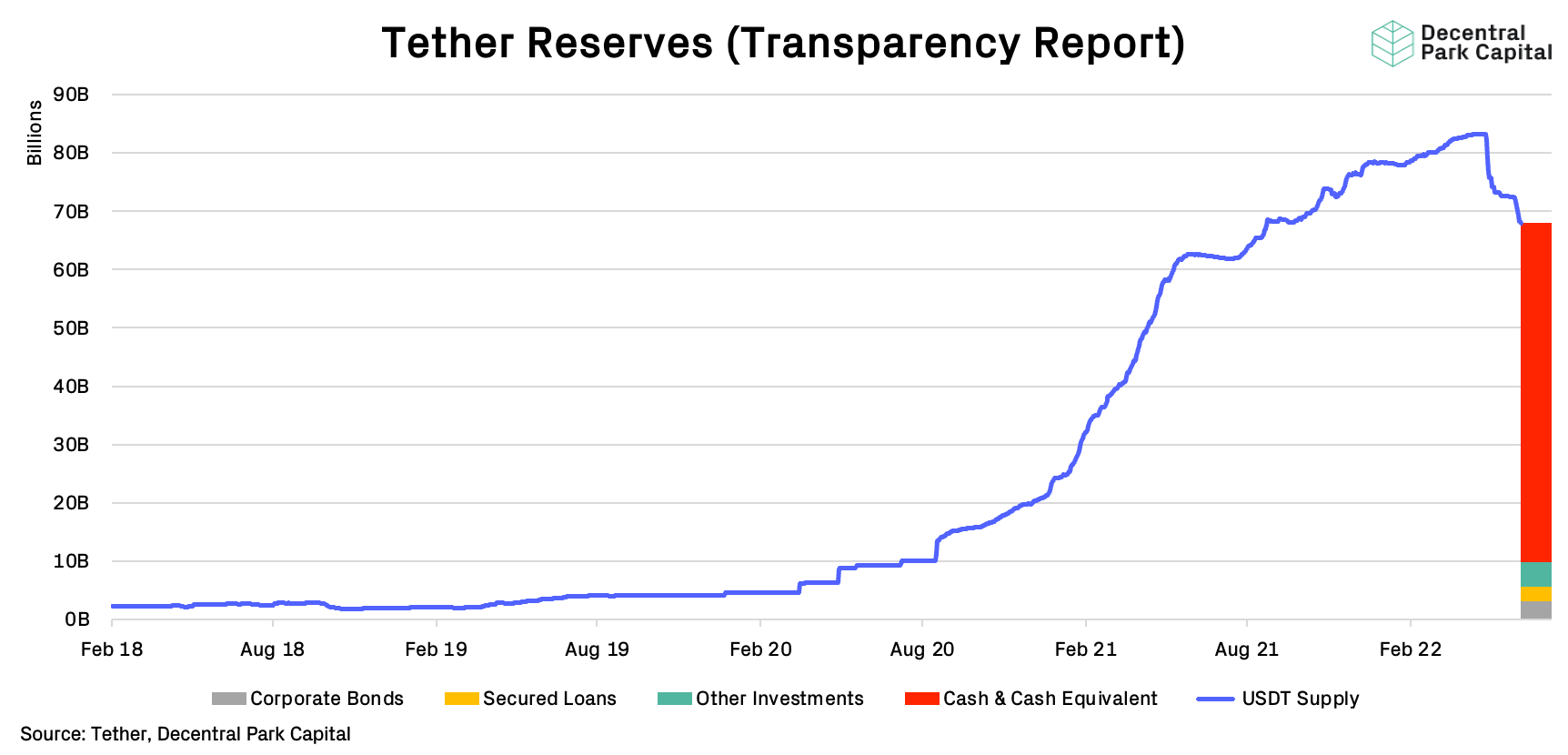

Tether’s supply has now fallen 20% from its ATH of 66.84B in May 2022. Tether claims a ‘coordinated conspiracy’ is trying to take it down and while that remains pure speculation the fact remains that the system is being stress-tested via its redemption mechanism.

Tether’s peg has recovered from its mid-June lows of 0.9975 and currently trading at 0.9937 indicating growing demand/trust in the stablecoin.

The risks remains largely around its reserves. According to their reserve report, the vast majority (86%) of USDT is backed by cash & cash equivalents. On the surface, this would give ~55B of redemptions before more other reserves are tapped into.

Within the cash & cash equivalents bucket, cash give only ~5B in redemptions before commercial paper, MM funds, and T-bills exits are required to keep the system running.

Assuming we see the rate of redemptions continue, the challenge for Tether will be the ability to exit these positions to keep trust in the system intact.

The profit Tether makes on its reserves is presumably significant but again it remains unclear how much runway this provides them. Neither should a fiat-backed system truly rely on the profits that system makes to facilitate redemptions at 100%.

Traders appear to be sector agnostic with a number of the top 100 performers being strong retail assets. DeFi blue chip names are leading the charge over the past week on an absolute and relative basis.

Top 100 (7d %):

Polygon (+53.8%)

The Sandbox (+47%)

Stacks (+42.8%)

Shiba Inu (+40%)

Uniswap (+39.7%)

DeFi Top 100 MCAPs (7d %):

DFI.money (+166%)

Compound (+64.7%)

Wrapped NXM (+46.2%)

yearn.finance (+41.9%)

JOE (+41.1%)

Arbitrum launched The Arbitrum Odyssey, an 8-week onboarding program where users can complete weekly tasks and get NFT rewards as well as potential Arbitrum token airdrop in the future.

Beethoven, an approved fork of Balancer v2 DEX, is live on Optimism with 5 incentivized pools including stable FRAX/USDC/MAI pool with 30% current APR.

DNS for Convex UI was hijacked, prompting users to approve malicious contracts for some interactions on the site. Funds are unaffected, but users are advised to review and revoke their approvals.

Atomic swaps from Synthetix on Curve and 1inch are live on Optimisim, trading fees from synth swaps are distributed to SNX stakers with 70% current APR.

Global Market Cap

$1T; Global market cap has gained 5% over the past week.

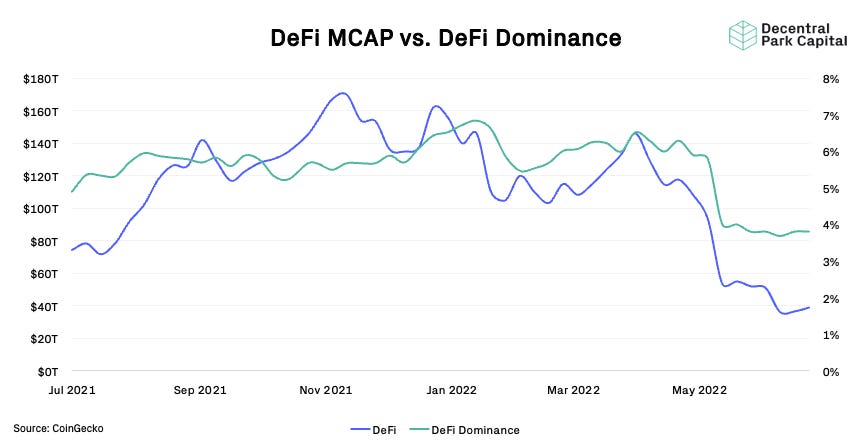

DeFi MCAP And Dominance

$40B; DeFi market cap has increased by 1% over the past week while DeFi dominance has stayed relatively flat and yet to break out above the 4% mark.

Bitcoin Dominance

Bitcoin dominance has fallen another percentage point over the past week to 43.4%.

BTC/USD and ETH/USD

BTC/USD and ETHUSD holding firm above key levels ($21.4k and $1.2k respectively) but with falling spot volume. BTC/USD still below 200W MA while ETH/USD trades claws back above it. Possible resistance at $23k BTC/USD. Daily RSIs no longer oversold and in more neutral territory.

Volatility

BTC & ETH; Elevated realized vol for both BTC and ETH. BTC vols significantly compressing as beta rallies over the past few days. Most BTC ATMs trading in high 70’s with front-end sloping (~77-80).

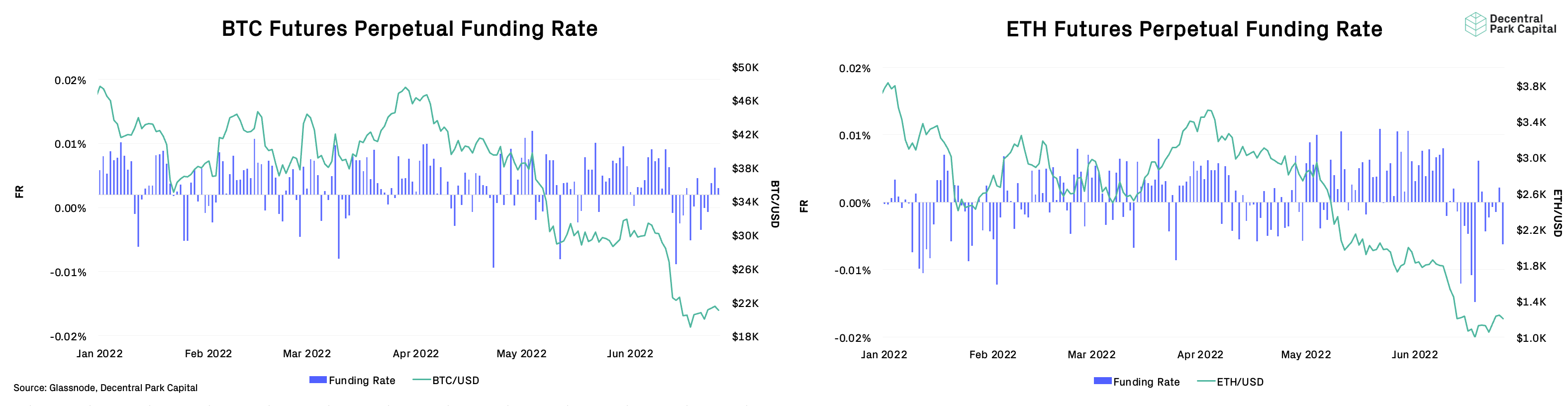

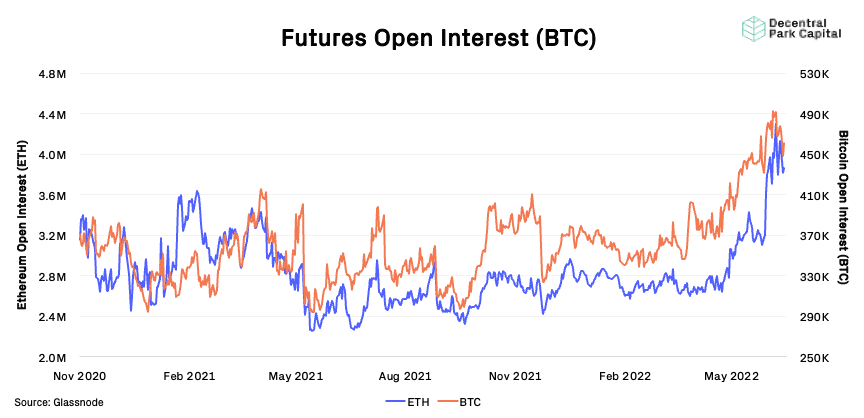

Trader Positioning

Diverging trends in put/call ratio for BTC and ETH. Traders taking an increasingly bullish stance. Futures painting a more bearish picture with funding rate turning negative (0.006%). Futures OI falling in both native denomination and USD indicating a level of waning interest.

Combined Order Books

Order books look slightly heavier on the bid side. Heavier resistance up to ~$21.6k.

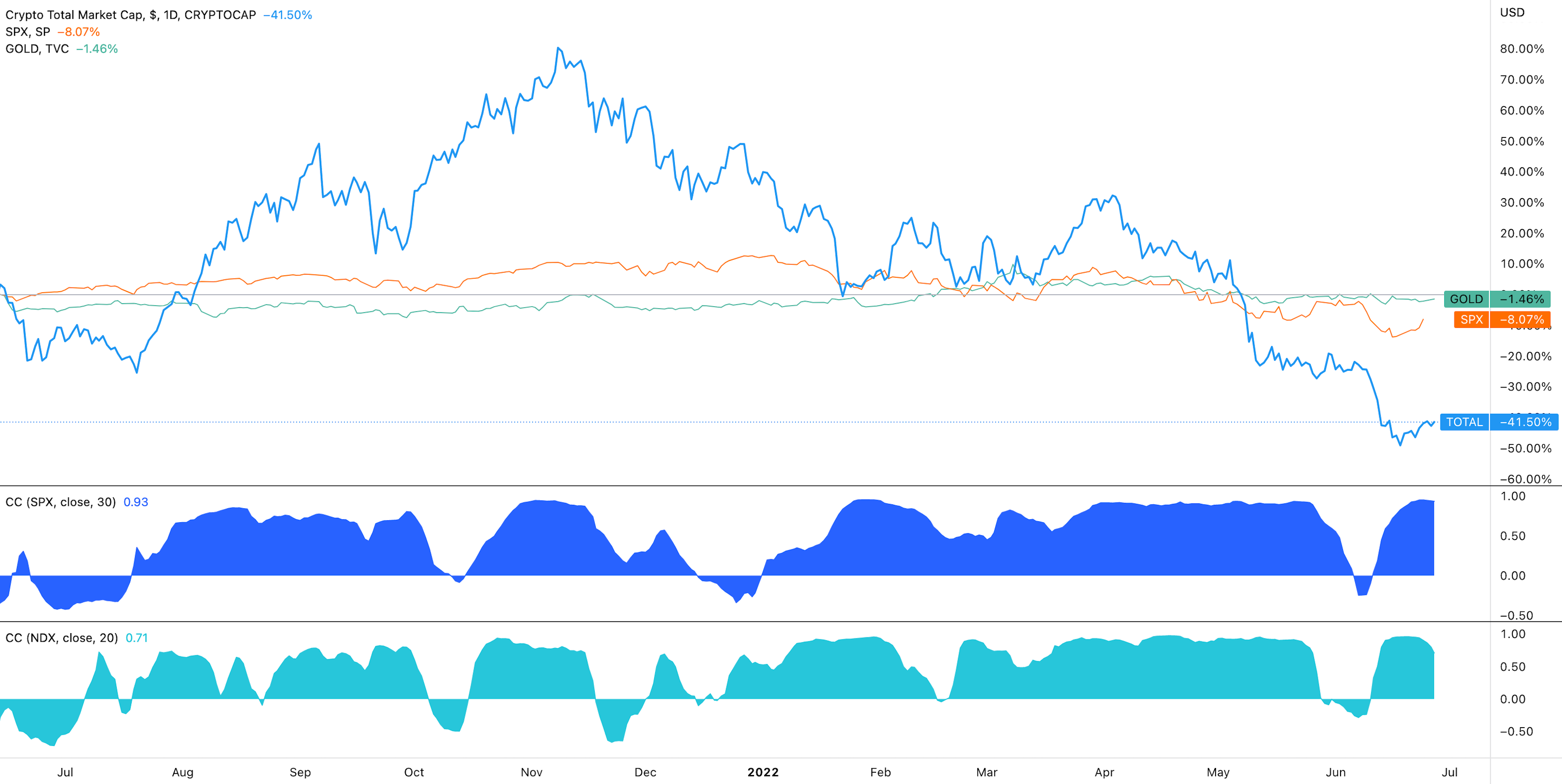

Crypto vs. Equities vs. Gold vs DXY; Cryptoassets remaining positively correlated to equity indices like SPX and NDX - no real change here. Implications being that deteriorating macroeconomic climate weighing on cryptoassets further if relationship persists.

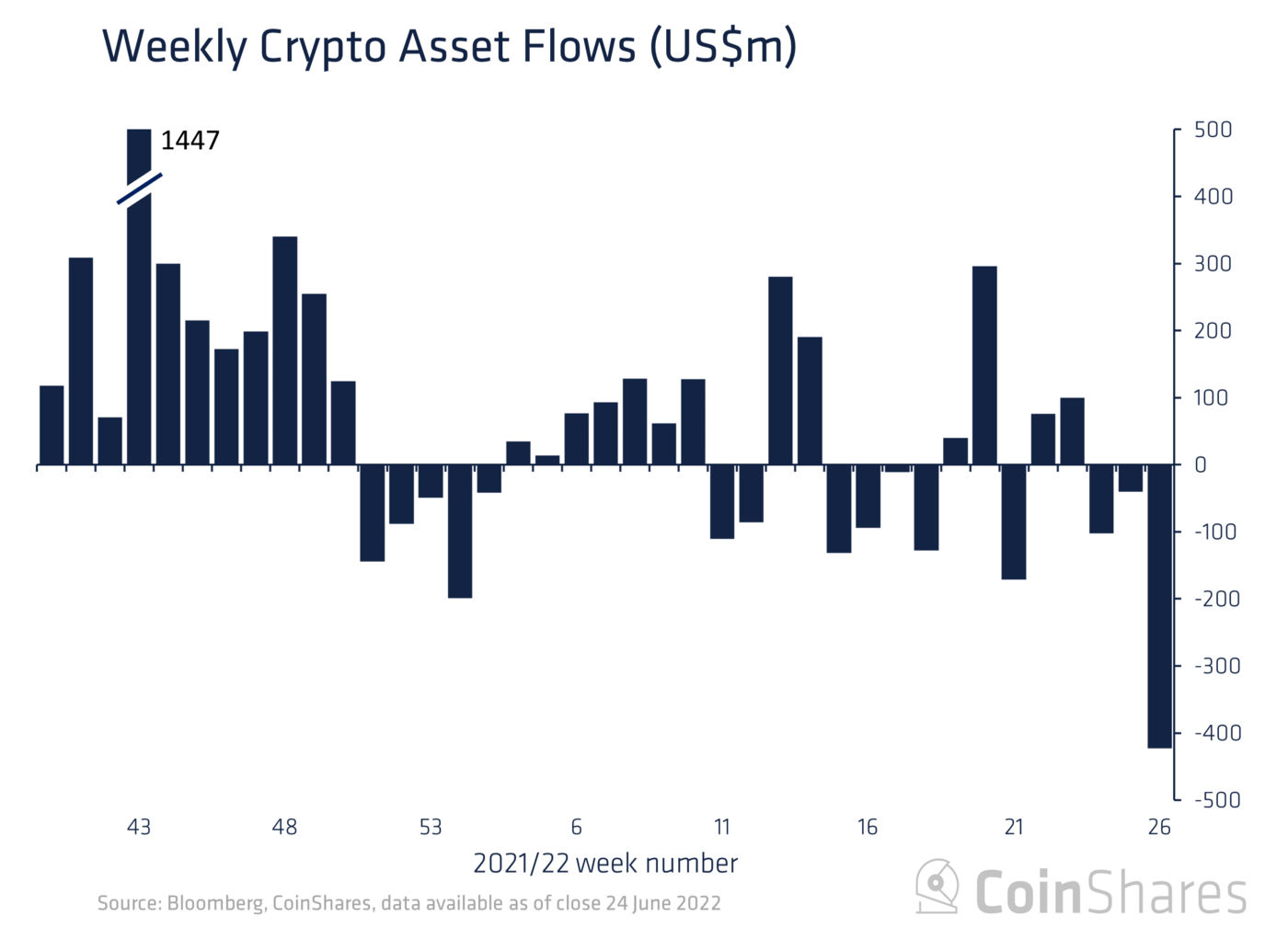

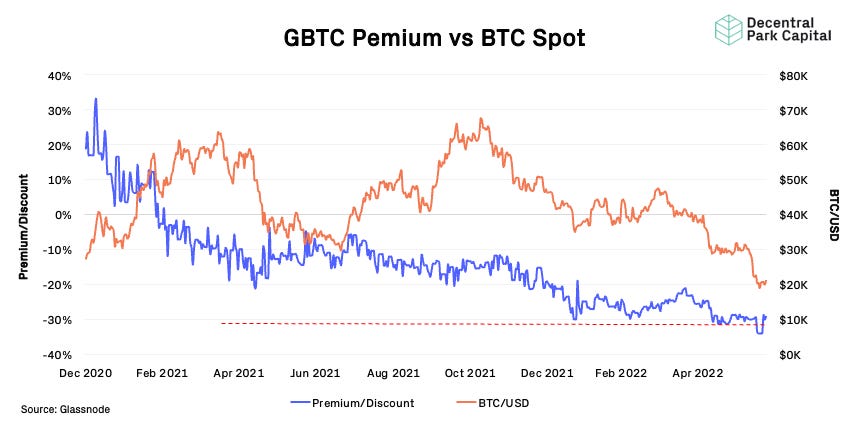

Trusts

Record $423 net outflows last week with majority stemming from Purpose (~490m).

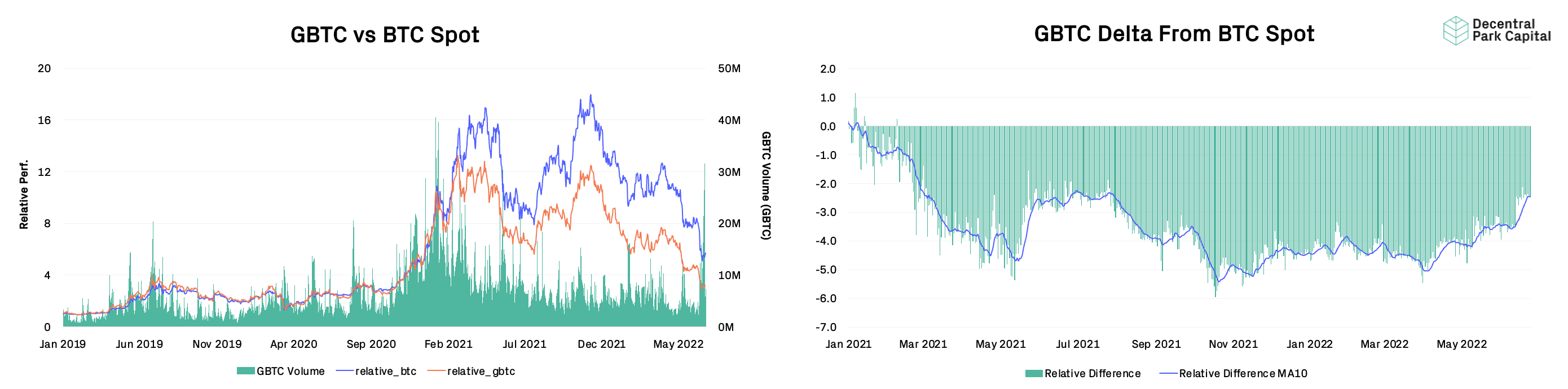

Grayscale GBTC

GBTC; GBTC discount still persisting (30%). GBTC volumes have spiked with volumes occurring after hours despite incurring high slippage but it is unknown if this seller is BlockFi. Large sellers would drive up the discount all else equal providing a more attractive long-term trade for traders with long-term time horizons.

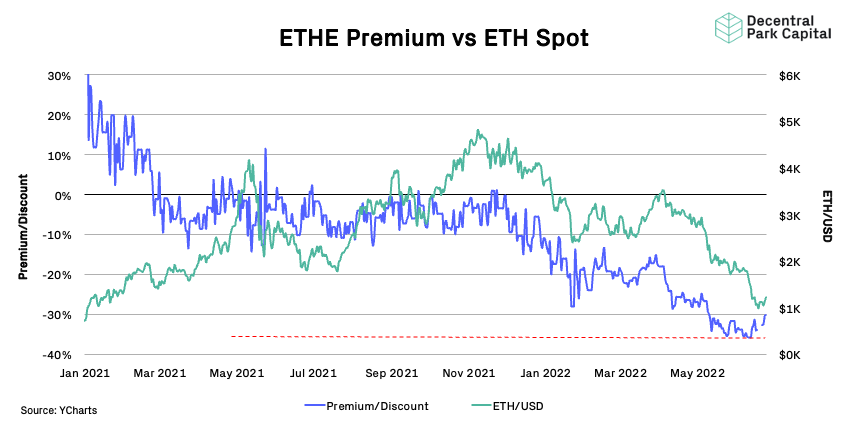

ETHE Grayscale Trust

ETHE; ETHE discount narrowing over the past week (30.17%) as ETH holds support above $1k. Not clear if this is a temporary or longer-term reversal. Secondary market volumes at ~5m daily, up from 3m in May 2022.

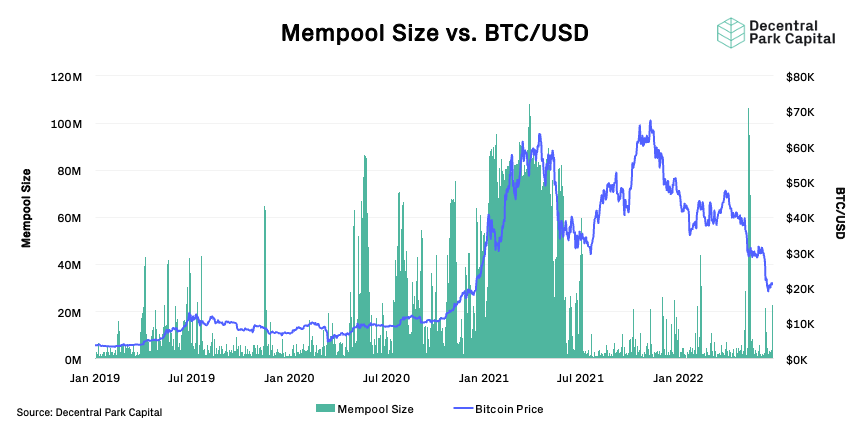

Mempool Size

Moderate uptick in mempool size as larger transactions force a growing number of smaller transactions to the pool.

Bitcoin Hashrate

Bitcoin hashrate has now dropped more than 13% from its ATH as miners start capitulating. Network difficulty has dropped 2.35% last week in response to the falling hash power committed.

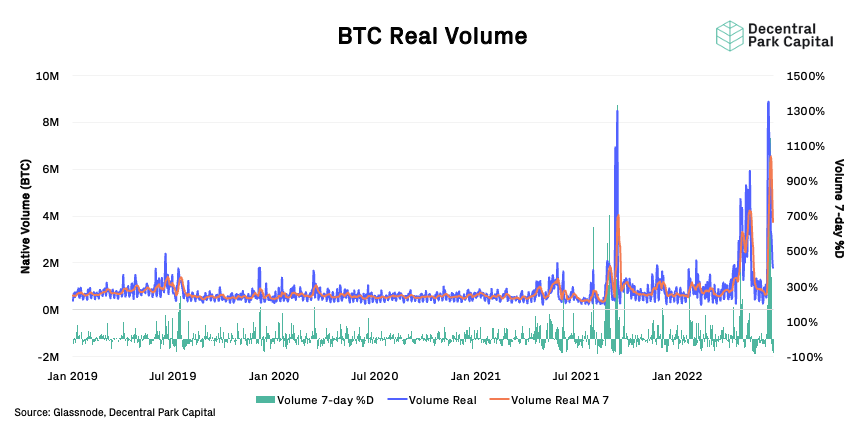

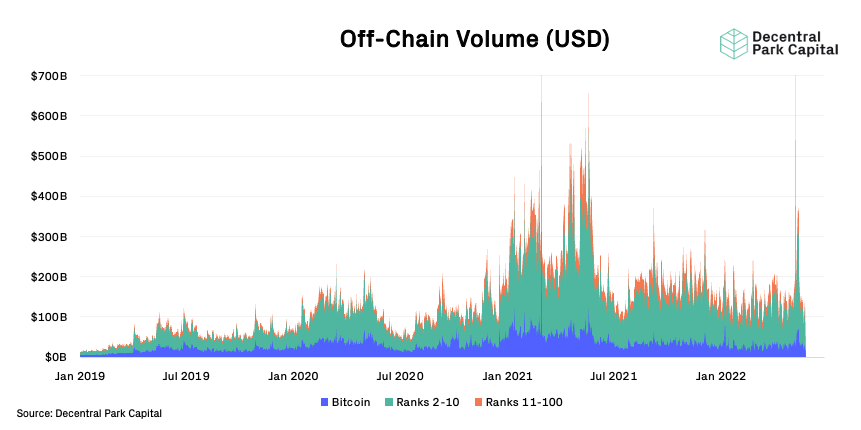

Volumes

On-chain real (BTC) & off-chain volume; On-chain volume spiked as liquidations took BTC to $20k. Off-chain volume now down 50% from its mid-June highs of $30B.

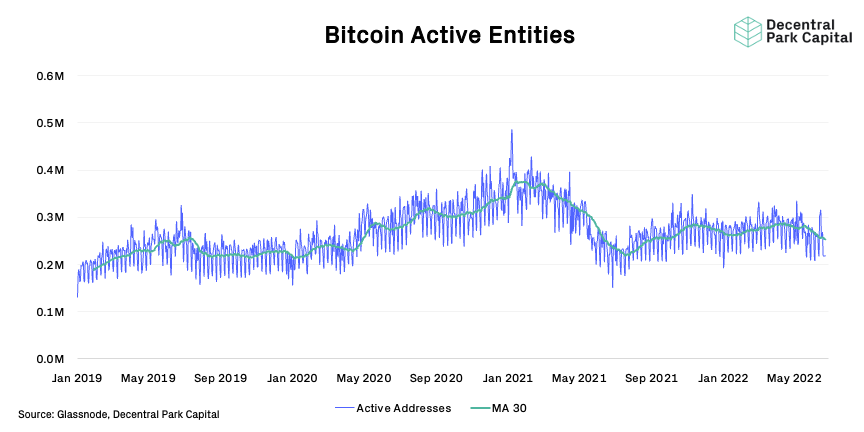

Active User Base

BTC; The Bitcoin network is seeing a less active user based. Active entities has fallen 1% over the past week.

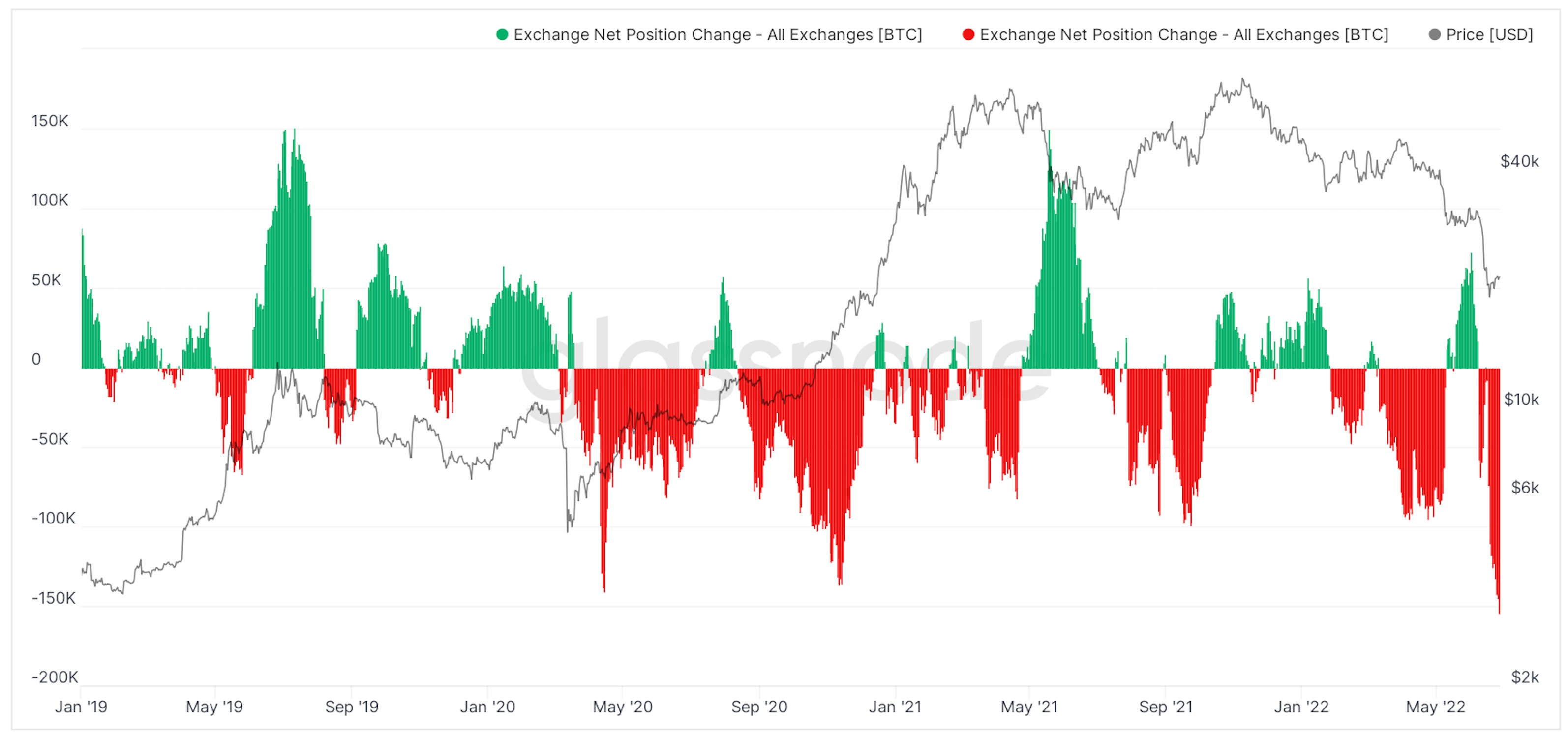

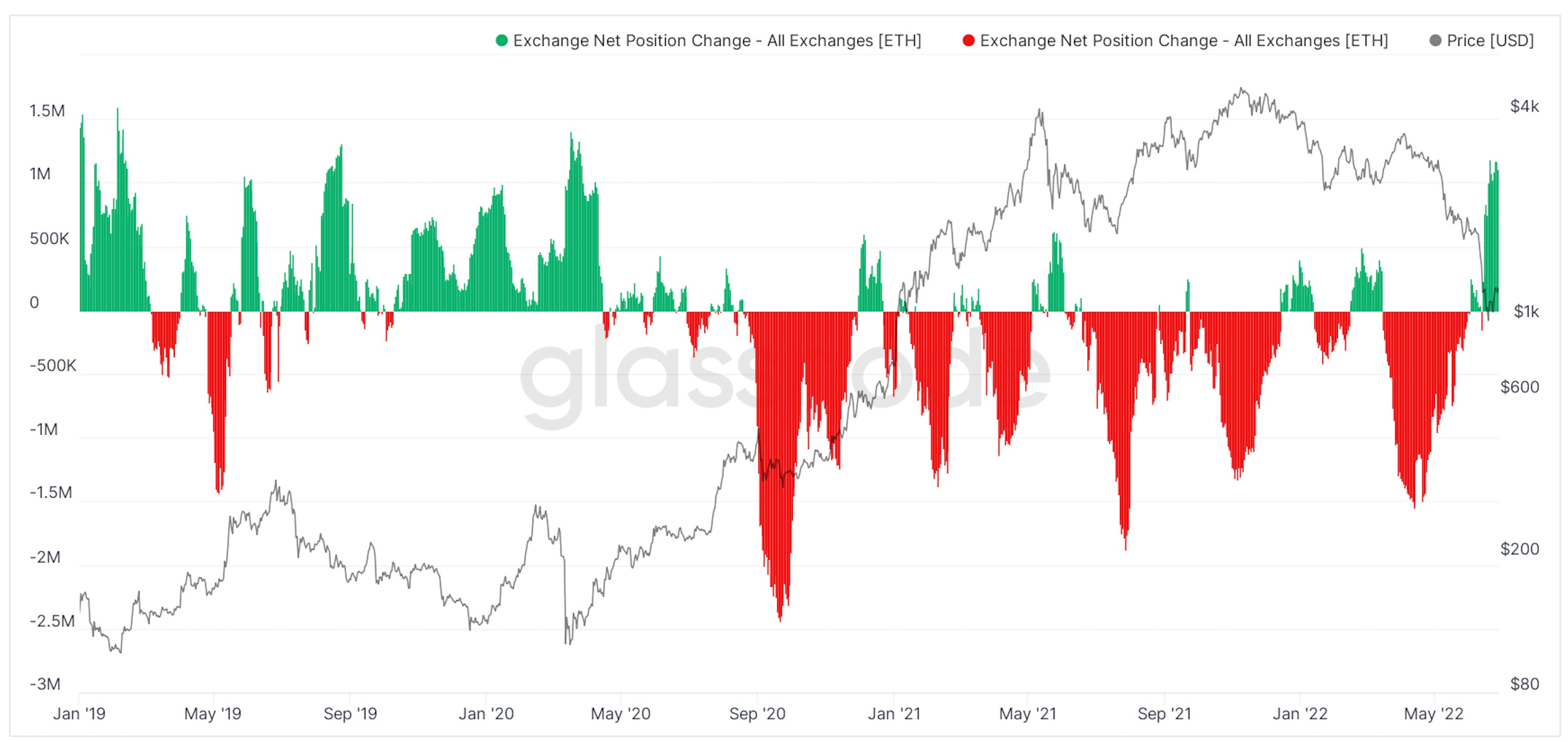

Exchange Flows

Net outflows from exchanges for BTC is gaining momentum. Opposite trend for ETH while prices rally but it is unclear if we see asymmetric selling for ETH relative to BTC.

📚 Liquidation Distributions [Messari]

📚 Short Bitcoin ETFs As A Market Bottom [Eric Balchunas]

📚 Liquidation Report Card [Mark Jeffrey]

📚 Gucci Buys Into SuperRare DAO [The Block]

📚 Why P/E Are Broken [DeFi Education]

🎙️ Jay Newman On The Coming Crisis For Emerging Markets [Odd Lots]

🎙️ E84: Markets Update, Turmoil and Endgame [All In]

🎙️ Zac Prince (BlockFi) On Navigating Through The Storm [On The Brink]

🎙️ Weekly Roundup 24th June [On The Brink]

🎙️ Inside Crypto’s ‘Biggest Deleveraging Event’ [The Scoop]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.