The Weekly #187

The Weekly #187

Crypto markets rally amid growing uncertainty around The Ukraine-Russia conflict. Positive sentiment and direct capital flows to cryptoassets are likely key drivers of recent price action.

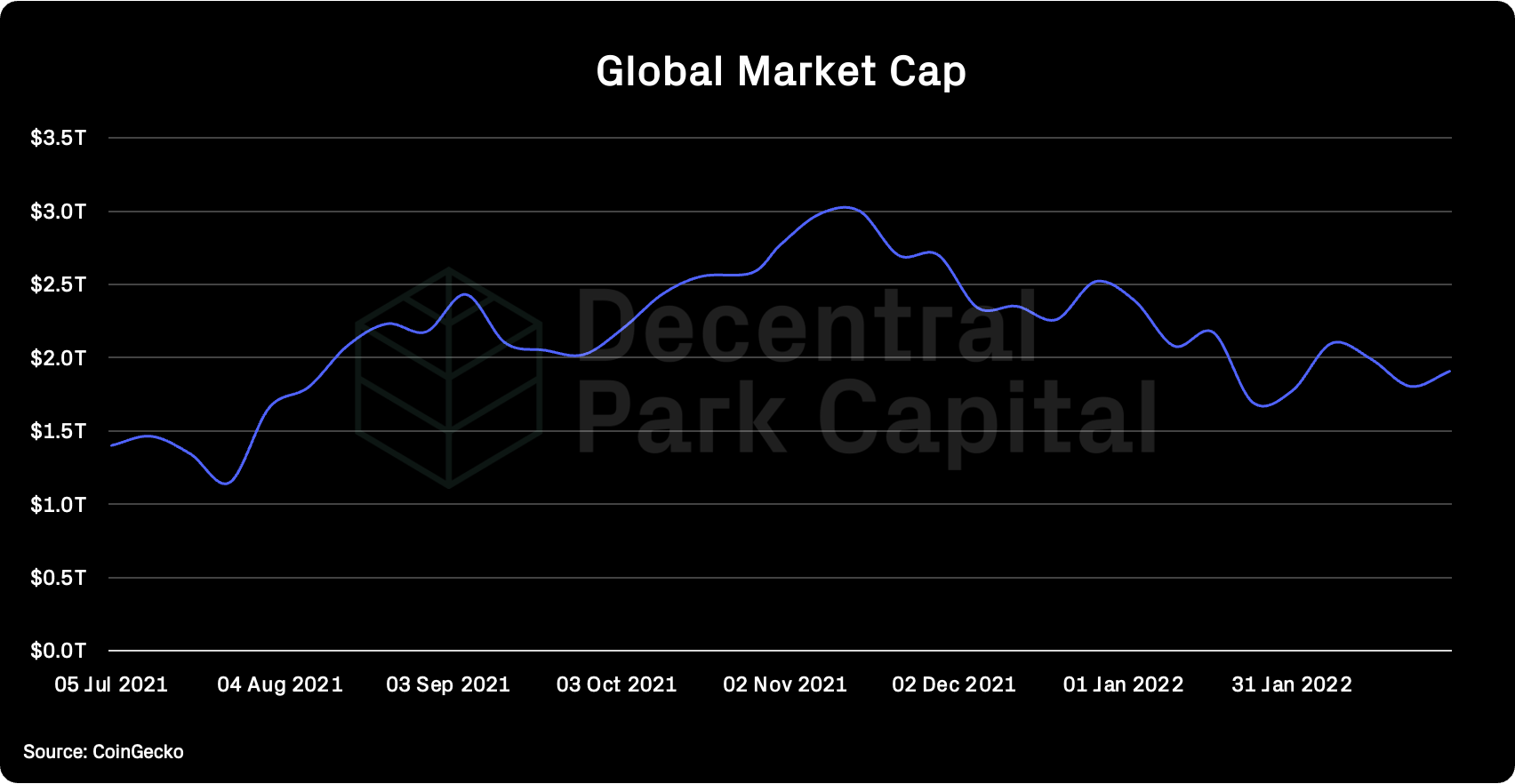

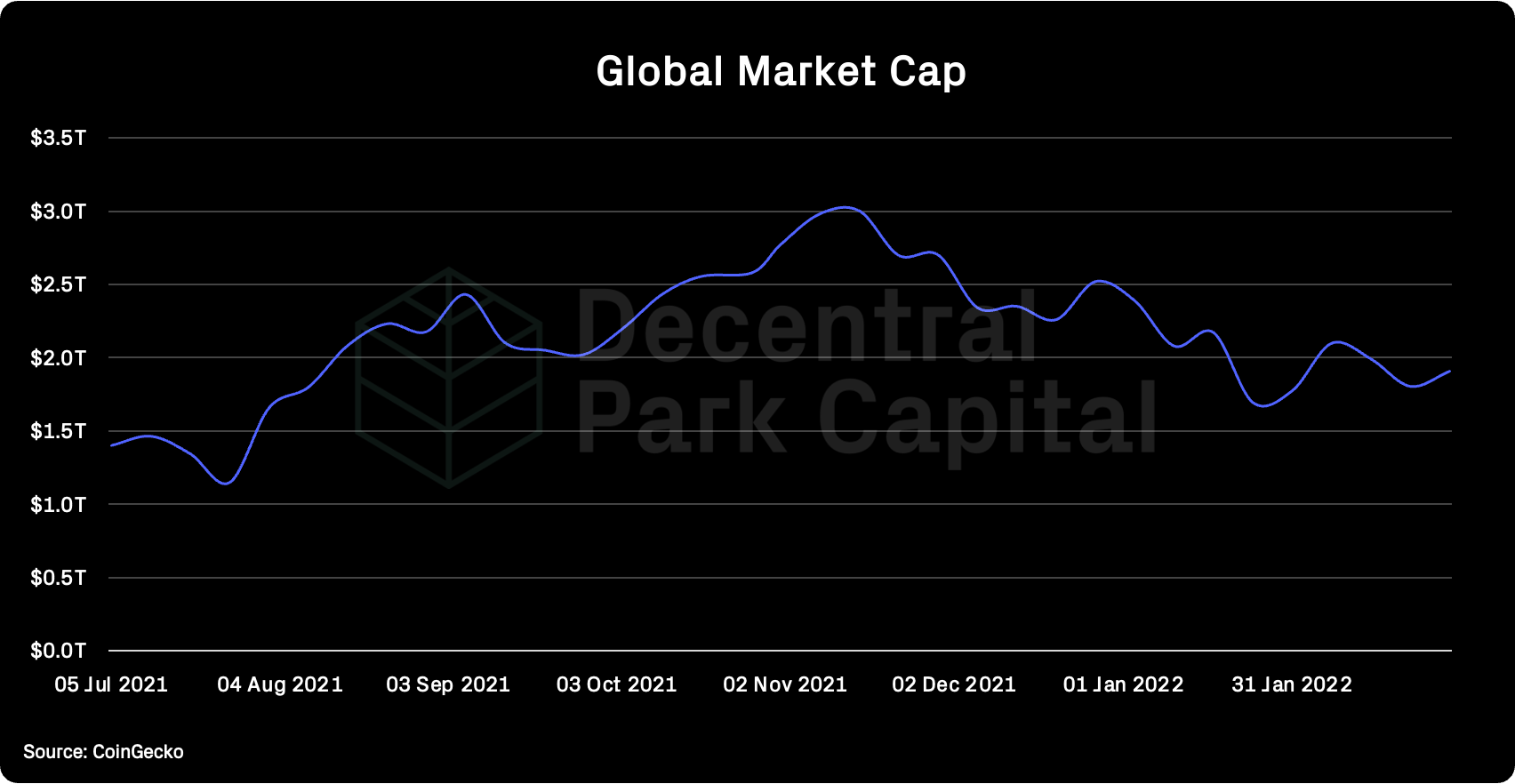

Global market capitalization has kept steady at $1.9T during what has been an eventful week on all fronts.

Russia continues to pursue its agenda in Ukraine with the West imposing severe sanctions on both Russian individuals and companies.

Some of the key sanctions included sanctions on the Russian central bank and the removal of lenders from the Swift global payment system.

As for the crypto markets, cryptoasset prices have kept relatively considering that $ES and $NQ had their largest gap downs since the March 2020 - the move coming clearly driven by continued conflict in Europe.

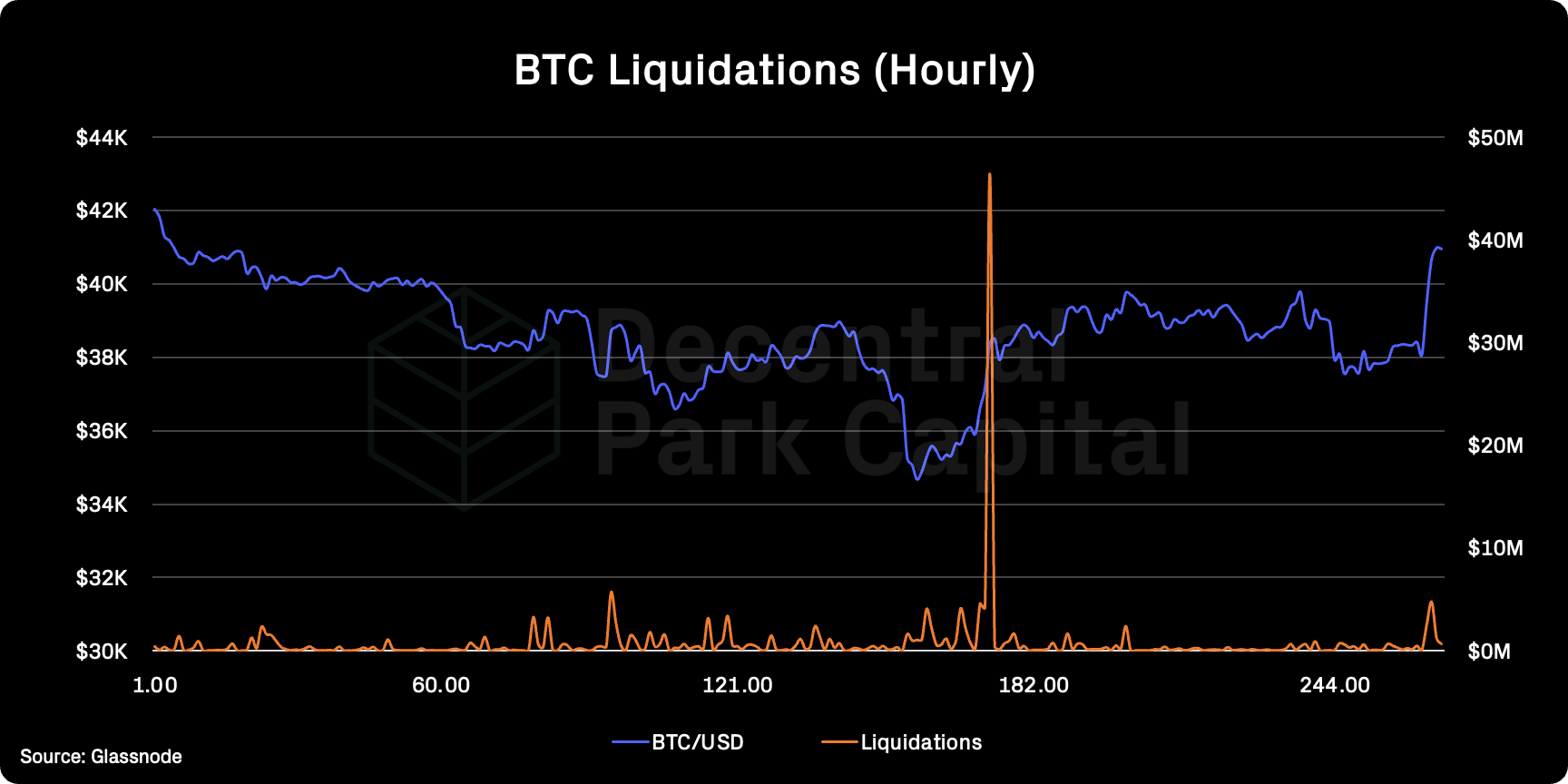

Meanwhile in crypto, BTC is looking to close above key support of $40k and the 50d EMA (+9.6% D) with the ETHBTC falling 3.8% in the past 2 days.

Cryptoassets have typically mirrored the broader risk-on markets like stocks which have been hammered. As Raymond James strategist Tavis McCourt highlights:

“War is fundamentally a ‘risk off’ environment for risky assets as global investors move into sovereign bonds and other ‘safe havens’ until some kind of conclusion/new normal becomes priced in. ... Everything about this is unprecedented, so about the only rational thing to say about equities is to expect volatility to continue pending a resolution.”

The potential future divergence between the equity markets and crypto could be driven by renewed positive sentiment and/or new flows to the ecosystem.

Today’s impressive price action does not appear to be driven by short liquidations - rather overall increased spot demand. Unlike on February 24th, short BTC liquidations have totalled <$10m. So the next question is what is driving this demand?

The rouble dropped to almost 118 against the US dollar in offshore trading on Monday after Russia was effectively cut off from the global financial system. Russia’s central bank more than doubled interest rates from 9.5% to 20% to steady the wider markets.

The fear, though, is runaway inflation - a vicious circle sets in where devaluation turns manageable foreign liability into systematic insolvencies. Russia companies have some $330Bn in external debt. Meanwhile, the dollar index is up 0.95% for the week.

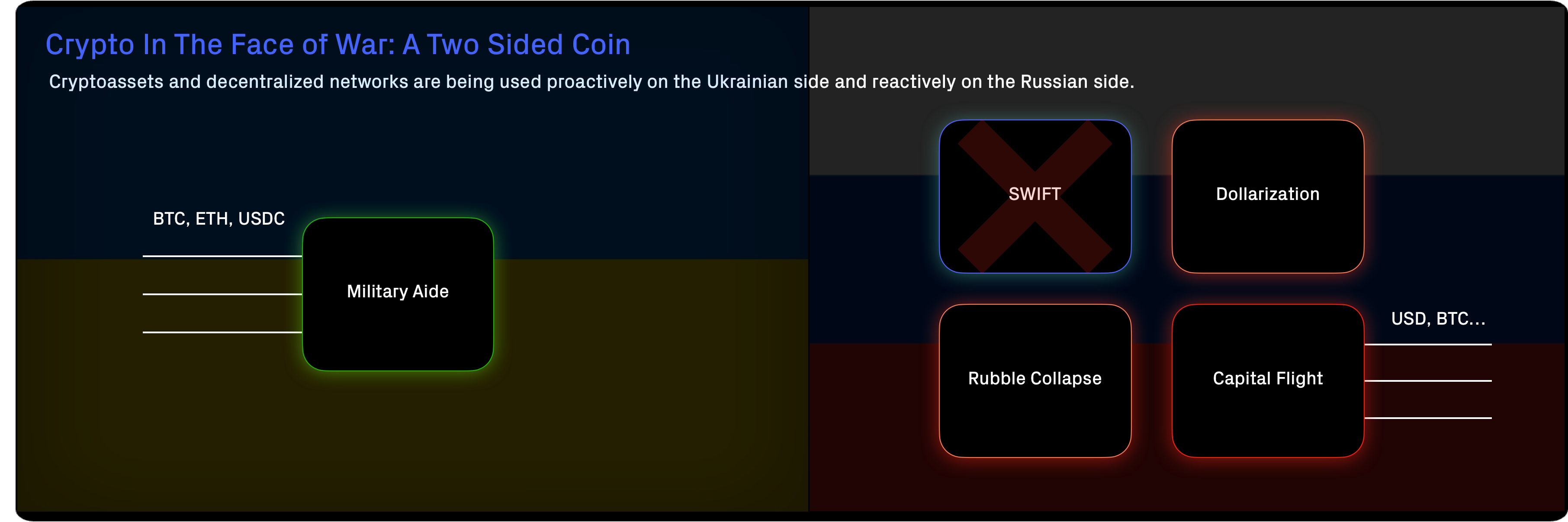

The buoyed sentiment for cryptoassets can stem from both sides of the conflict:

For Ukraine, the community has donated over $11m in Bitcoin donations with Binance alone donating $10m to the country in parallel.

For Russia, the blocking of SWIFT has led to rapid dollarisation as the currency demands a premium on the streets. Russians are reportedly withdrawing USD at more than a 30% premium. Flight to crypto to move assets outside of the country or liquidate positions is a possibility for Russians.

The risk for the west here is the Russian government or oligarchs mitigating the pain of sanctions by using ‘crypto rails’. While the west has used crypto to as secure aide to Ukraine, Russia can just as easily demonize the technology too.

It’s clearly not a complete solution though. Cryptoassets can be traced on-chain so it would be theoretically much harder to launder funds.

It is no coincidence that the Biden administration is calling on exchanges to enhance KYC/AML checks in light of recent Russian sanctions.

But we are clearly not out of the woods. A potential black swan event could be if Ukraine loses control of Kyiv. The market will be closely watching Belarus and its decision to send its troops into Ukraine.

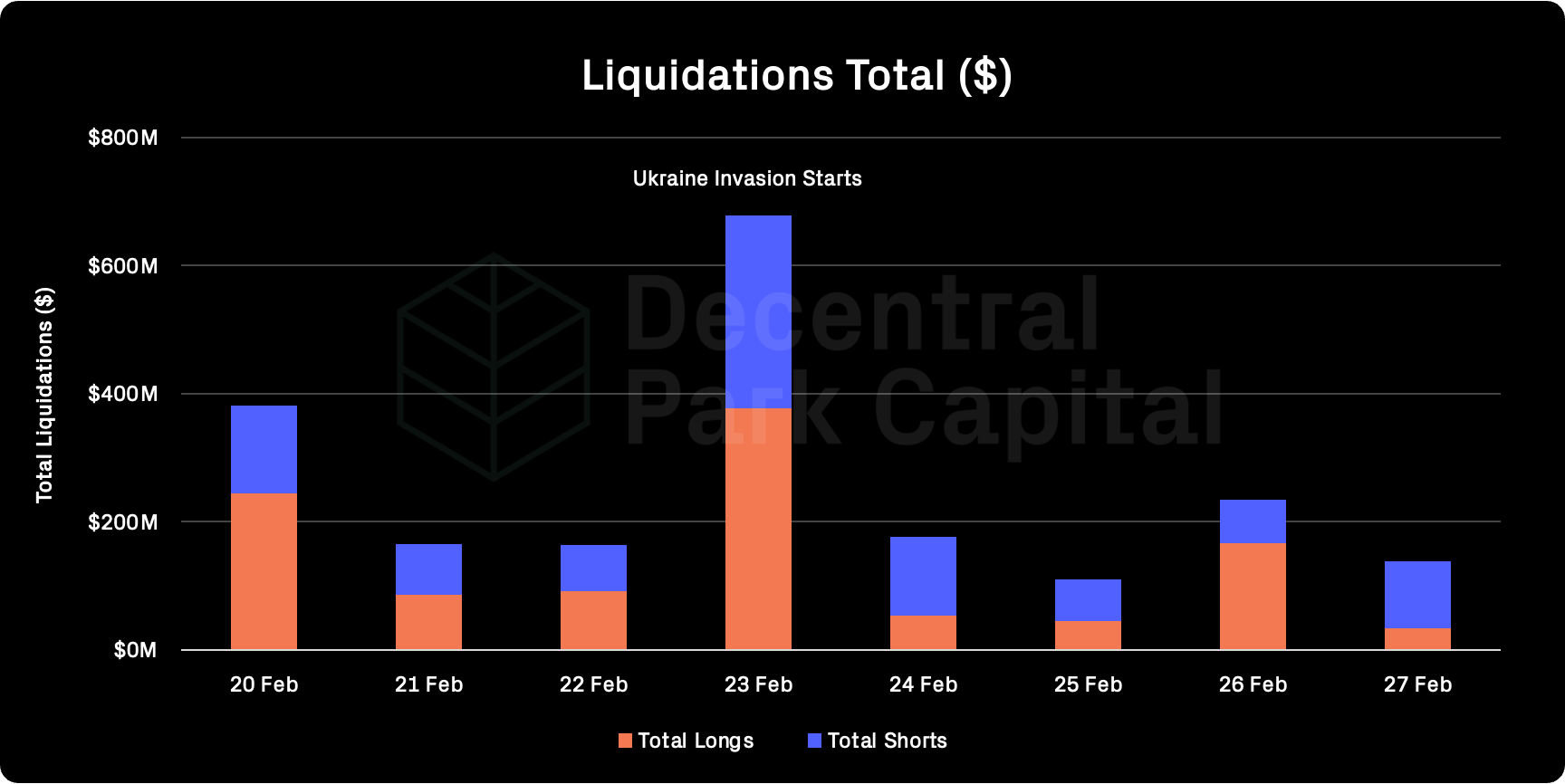

This potential black swan event does not mean necessarily mean bearish price action. Just last week as Russia invaded Ukraine, we saw over $300m long and short liquidations (balanced). Net, crypto markets moved +1.28% on the day.

So some traders may look at the current price action and deem it short-lived amid the wider geopolitical uncertainty while others see this price action simply reflecting an accelerated path to adoption beyond pure speculation.

Regardless of which conclusion you come to, expect volatility as the world watches the events unfold in real-time.

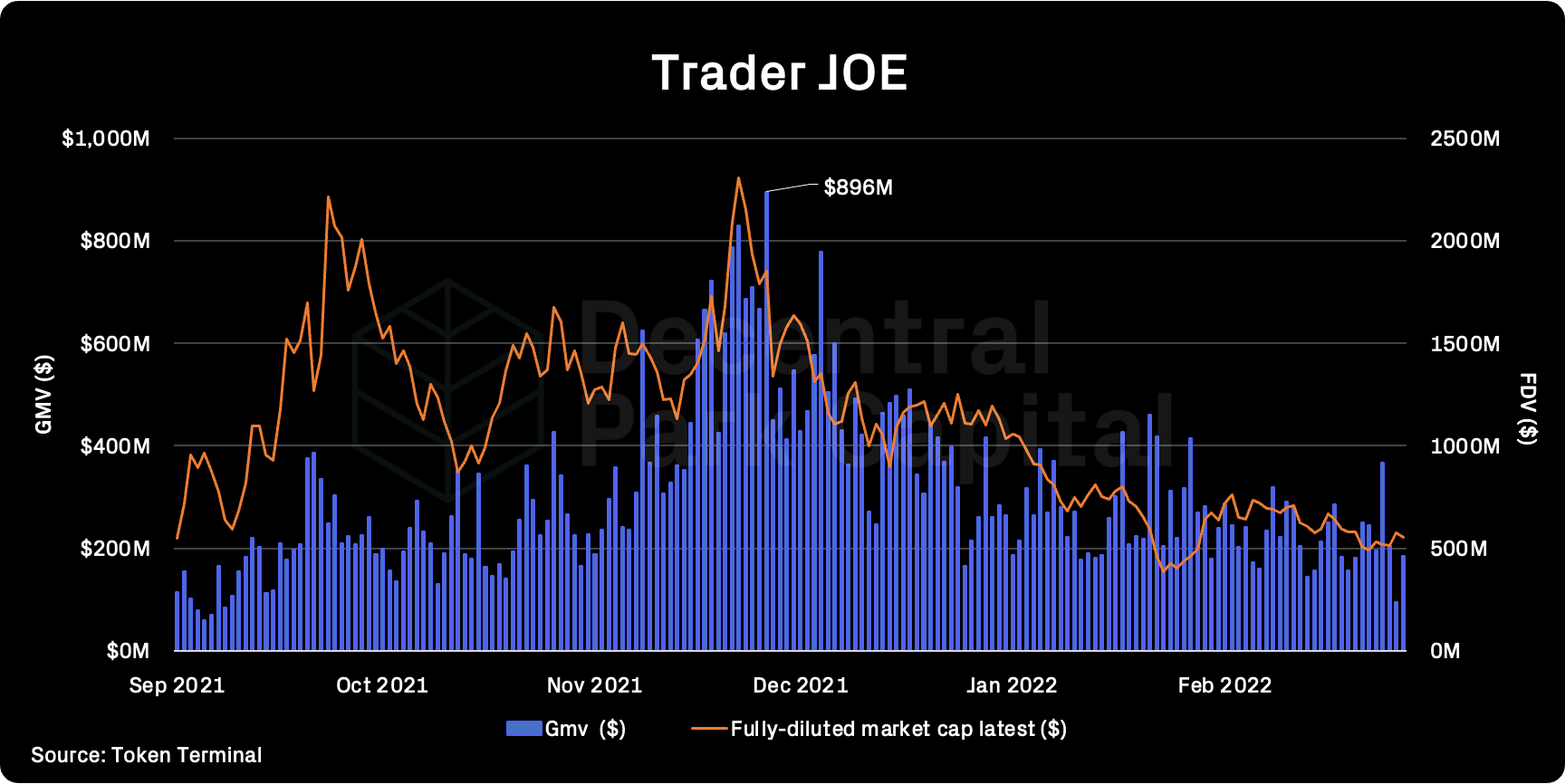

JOE

JOE has been a top performing asset this week with performance driven by the launch of sJOE today. Users are now able to stake JOE into sJOR and receive daily USDC rewards.

Trading volume continues to trend down from ATH levels in November ($896m), now dipping below $200m.

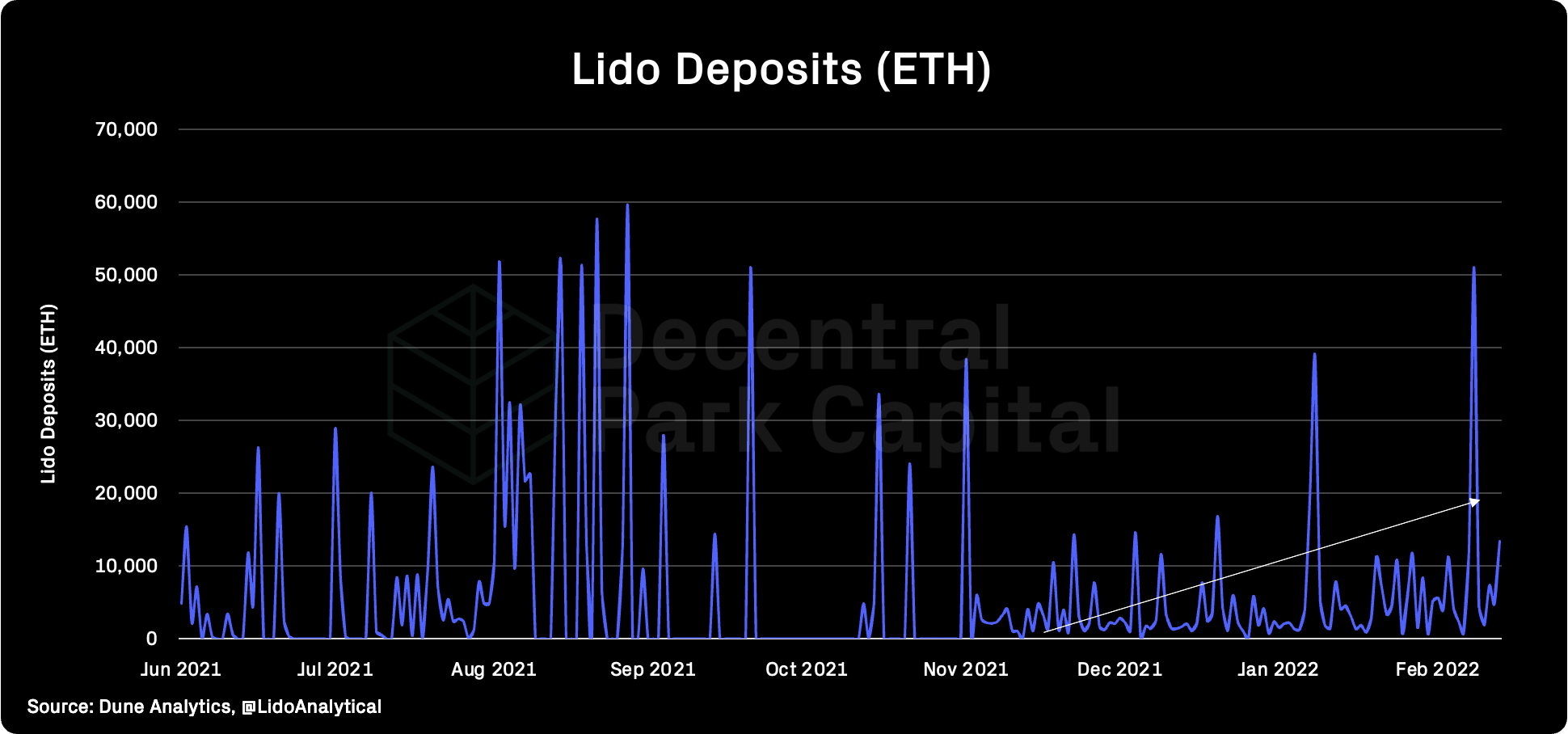

Lido

Lido continues to see a growing number of ETH deposited to its ETH2 validators which is now consistently >10k ETH daily.

Lido’s ETH2 deposit market share has climbed above 20% for the first time. stETH liquidity on Anchor Protocol is also growing with $750m of collateral value deposited in the protocol.

Top performing assets out of the gate this week can be found down the risk curve. Lido Finance leads the pack at 16.8%.

Global (24hr %):

Terra (+11%)

Solana (17%)

Zcash (+8%)

Kadena (+7%)

Waves (+6.8%)

DeFi (24hr %):

Lido DAO (+16.8%)

JOE (+12.5%)

Bounce (12%)

Terra (+11%)

API3 (+7.4%)

Convex launched cvxFXS / FXS pool on Curve with CVX rand FXS rewards. Current APR is 135%.

Tokemak announced that Cycle Zero is concluded. TOKE stakers will have a week to migrate to the new Liquidity Director contract. TOKE stakers can earn 30-40% APR based on their votes.

Solidly launched on Fantom followed by Solidex yield optimizer offering 18% APY for USDC/MIM pair and 16% for USDC/FRAX pair.

Ribbon launched veRBN (ve tokenomics pioneered by Curve), RBN holders can lock their tokens to receive a share of protocol fees.

Sanctions Summary - Last 48hrs:

Several primary Russian banks will be removed from messaging and access to SWIFT

Germany reverses course and commits to cash and arms

UK targets 100+ oilgarchs with sanctions to include mandatory offshore reporting and transparency

UK will prevent ALL Russian nationals from holding UK deposits above a small cap

US' OFAC targets Sberbank, effectively shutting off access to 80% of its daily $40B in non-Russia US denominated holdings

Ukraine crypto community in concert with cabinet is hunting crypto wallets of Russian politicos

Global market cap: $1.9T; Global market cap has increased by 6% over the past week.

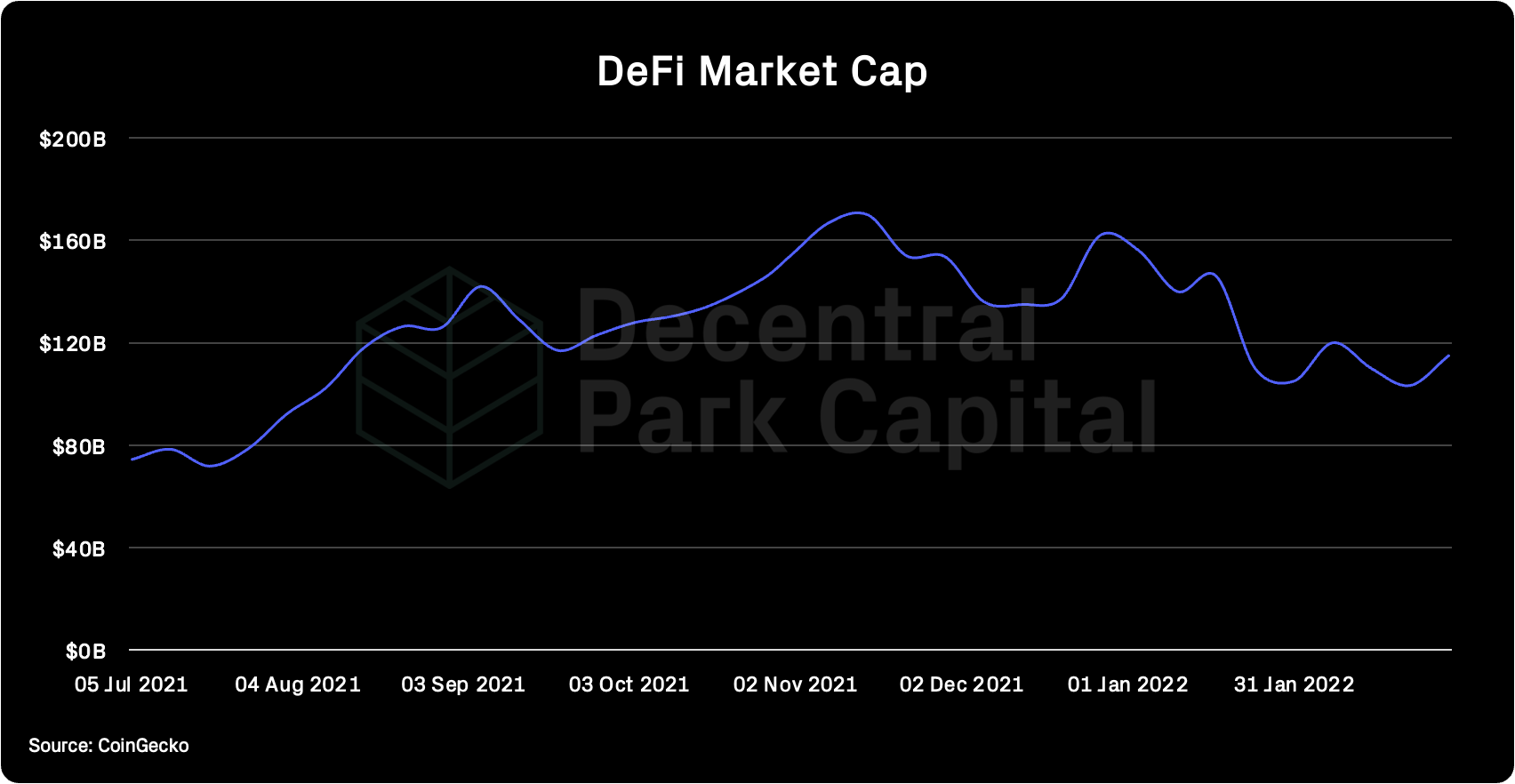

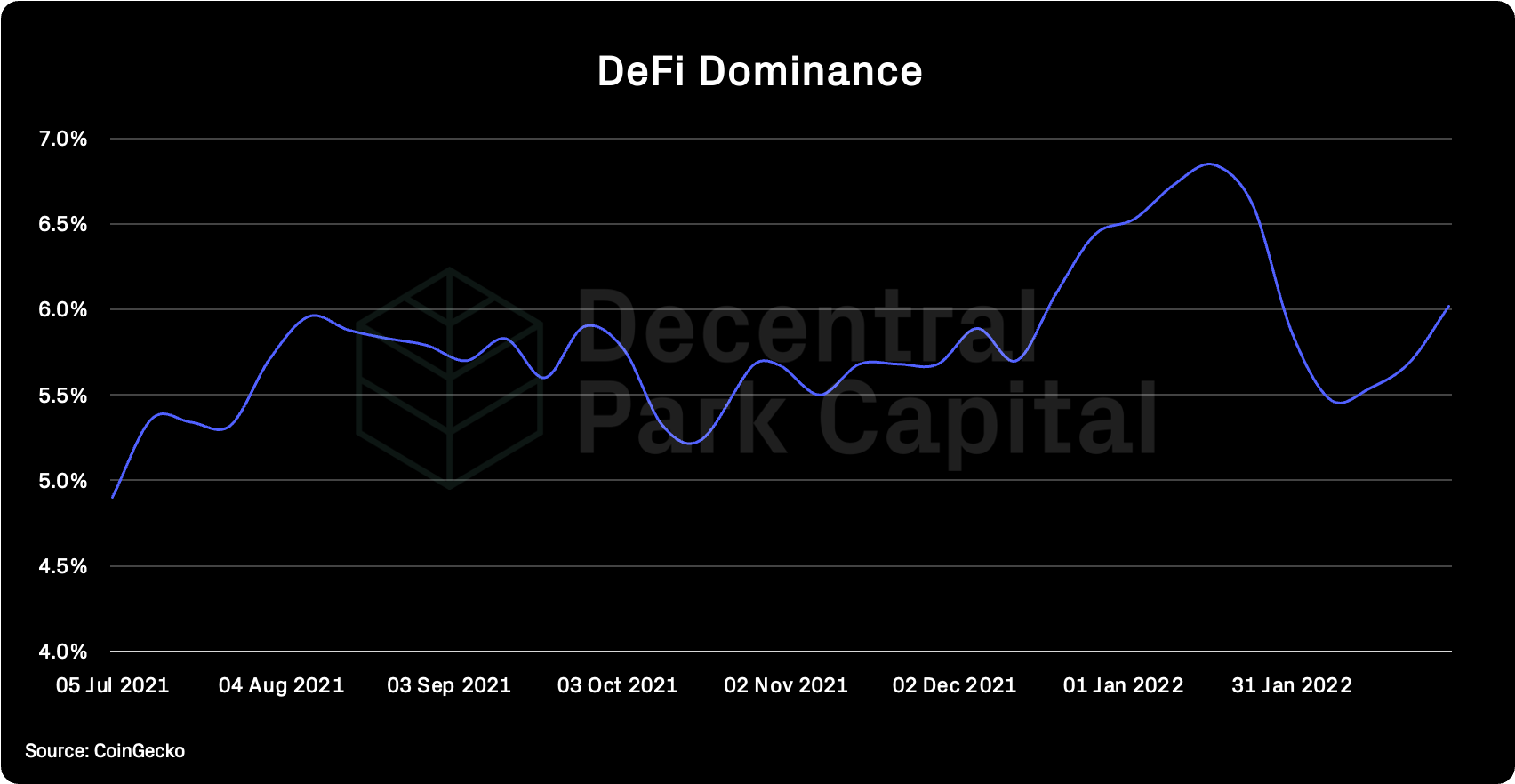

DeFi: $110B; DeFi market cap has increased 11%, slightly more than global MCAP. DeFi dominance has therefore picked up over the week (+6%).

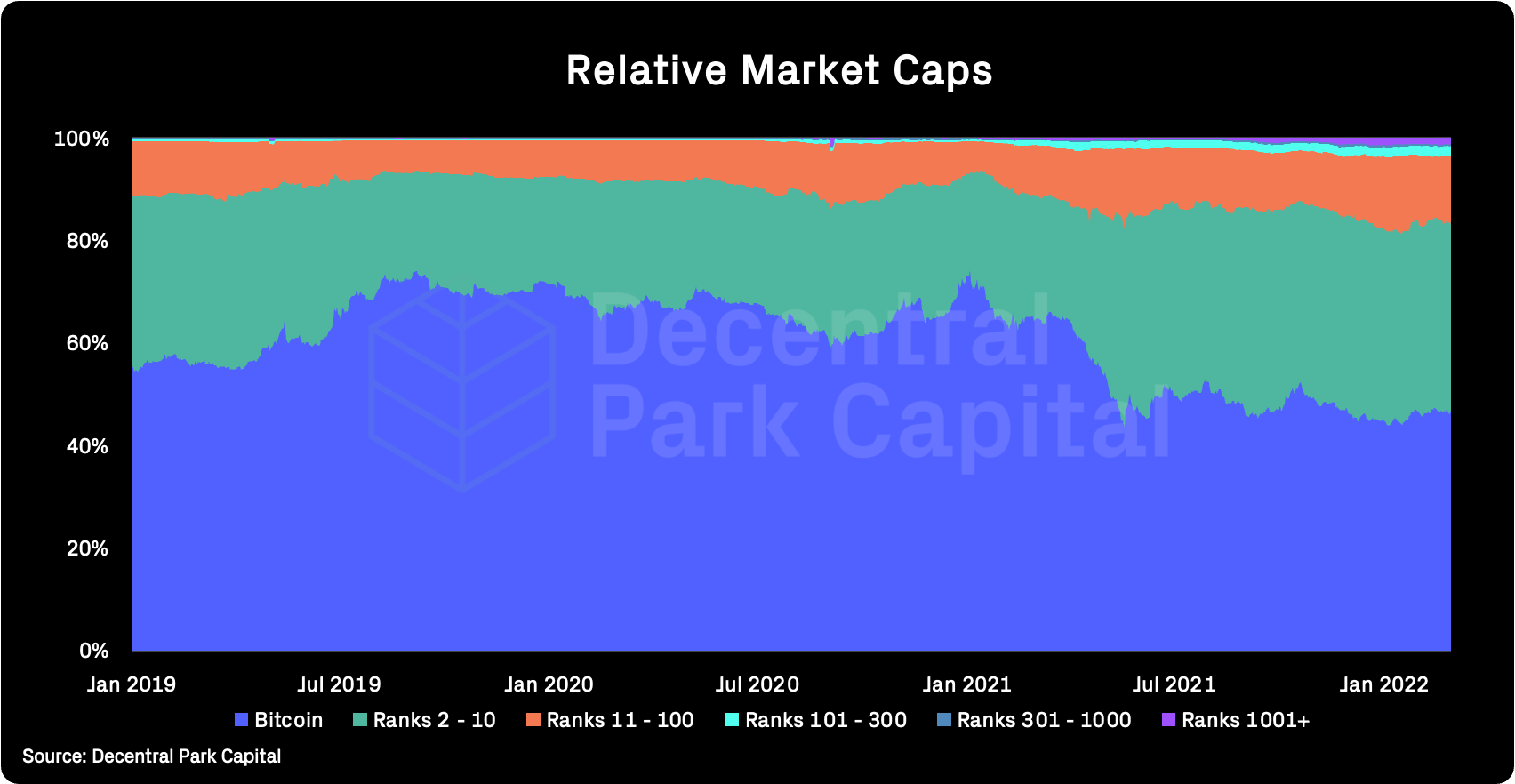

Market shares; Bitcoin dominance has kept its dominance at 47%.

BTC/USD and ETH/USD

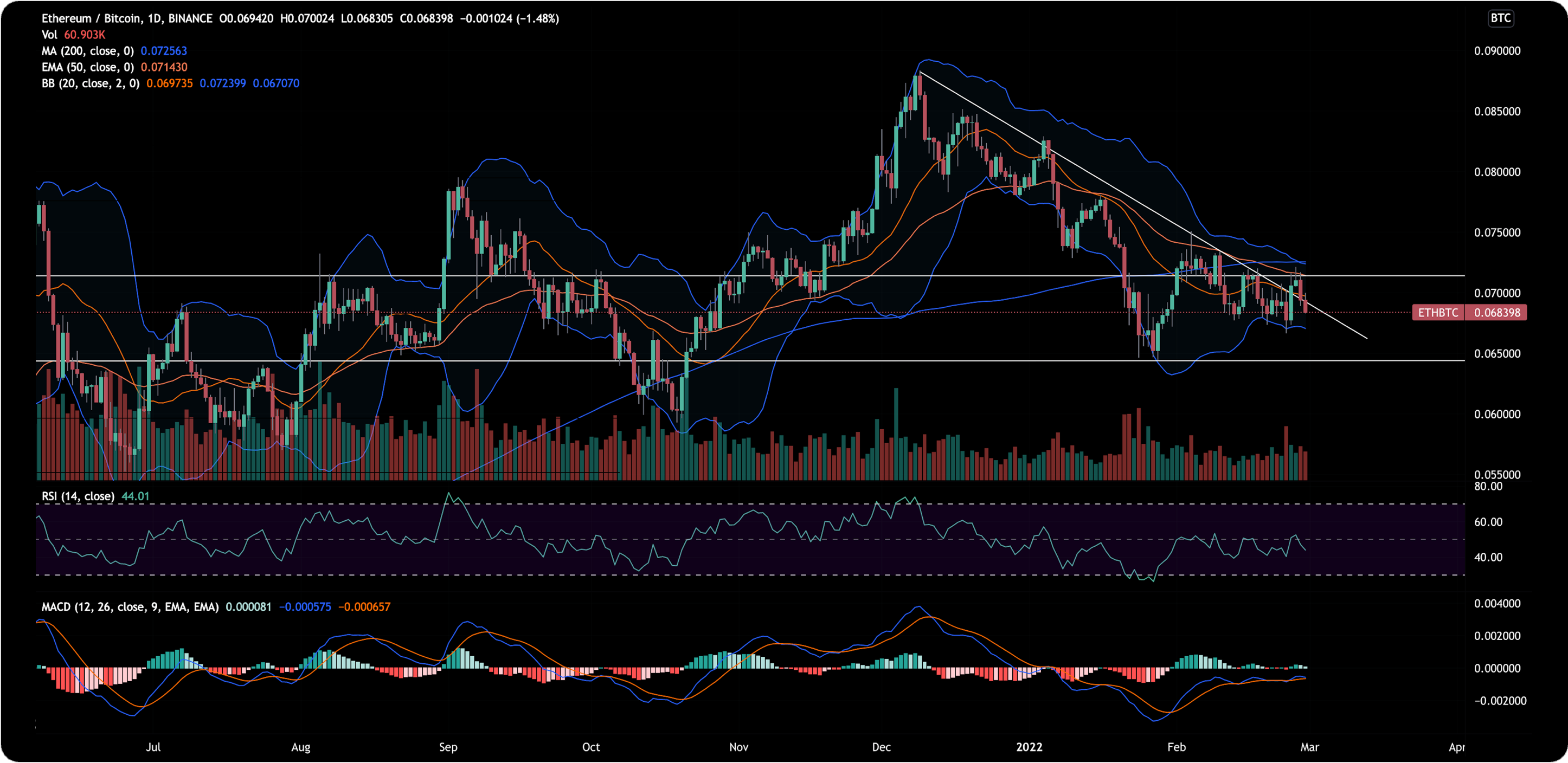

ETH/BTC

Price action; BTC/USD back above key resistance line of $40k. ETH/USD facing resistance at $2.85k. Daily RSIs still in neutral ground. ETH/BTC down 5% over the past 2 days and back below the descending channel.

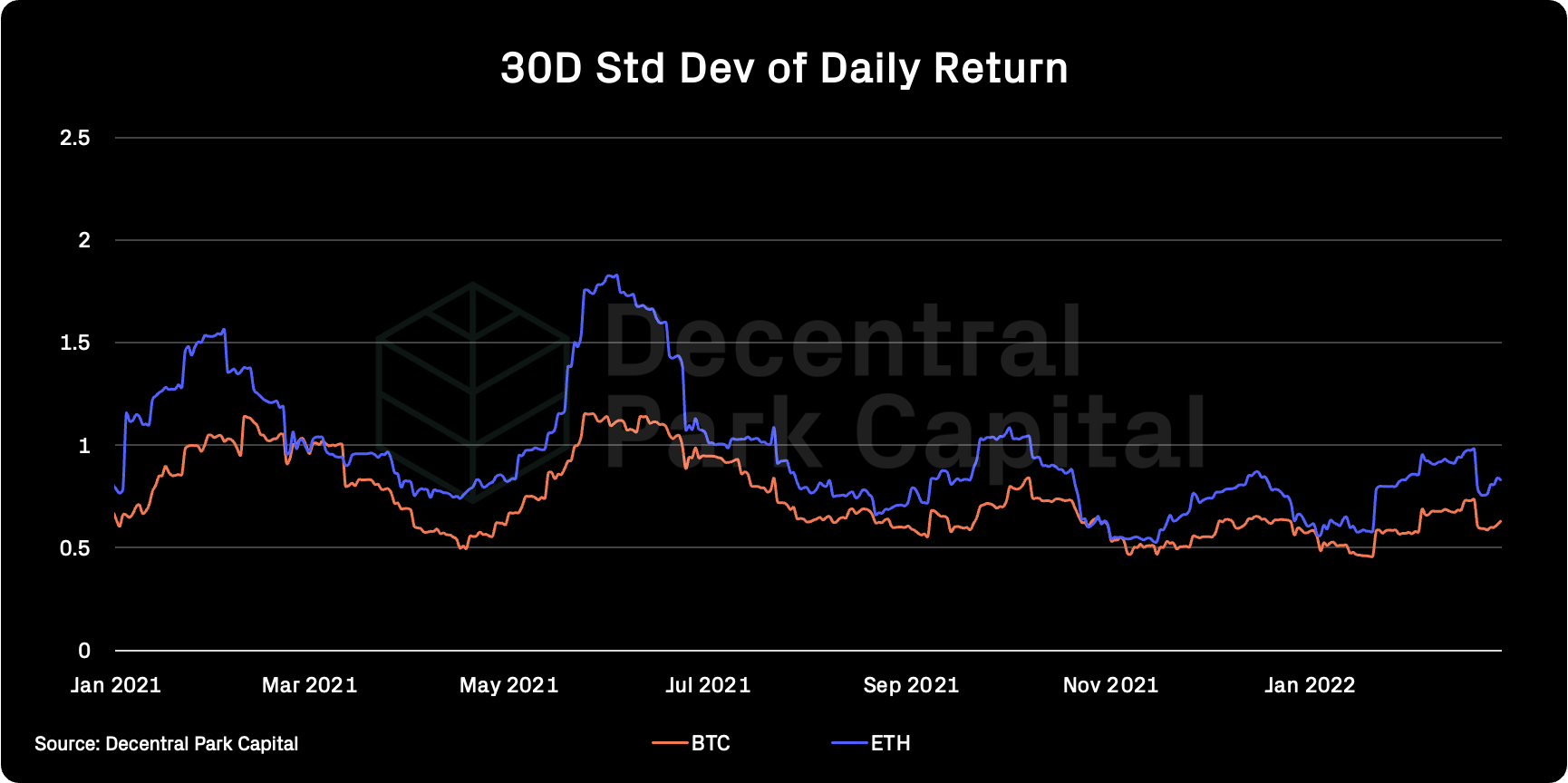

Volatility (BTC & ETH); BTC and ETH 30D vol has increased slightly. Implied 1M vol for BTC and ETH 59.72% and 69% respectively.

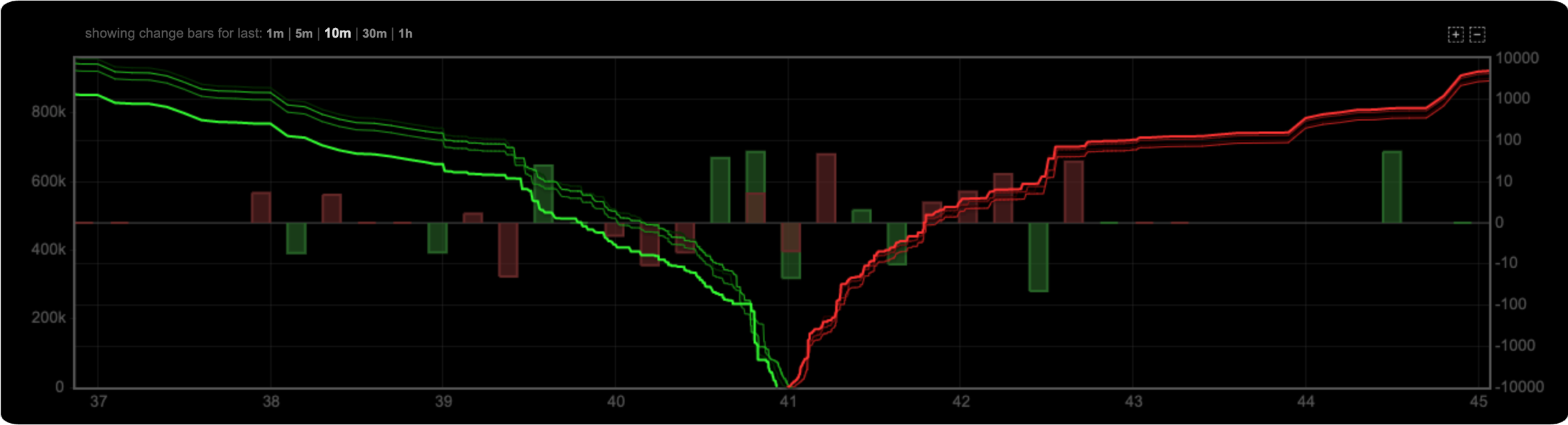

Combined order books; Order books look fairly even on both sides. Heavier resistance up to $42.5k (Source: Bitcoinity).

Crypto vs. SPX; Correlations between crypto and equities still remain moderately positive (0.52). Gold has seen higher volatility on further safe-haven demand.

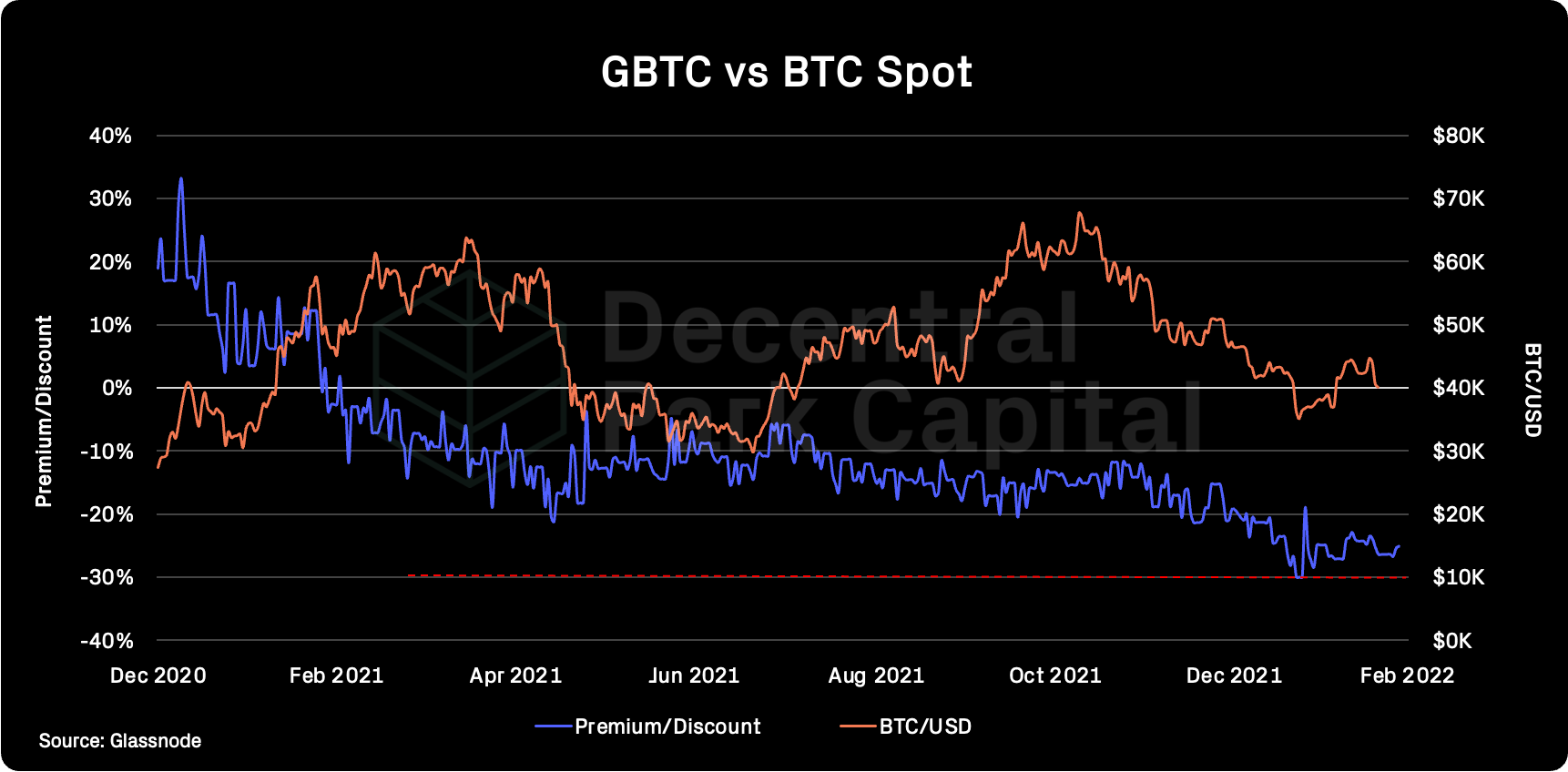

GBTC premium; GBTC discount falling to near ATHs (-25%). 30D volumes have kept flat over the past week (~7m).

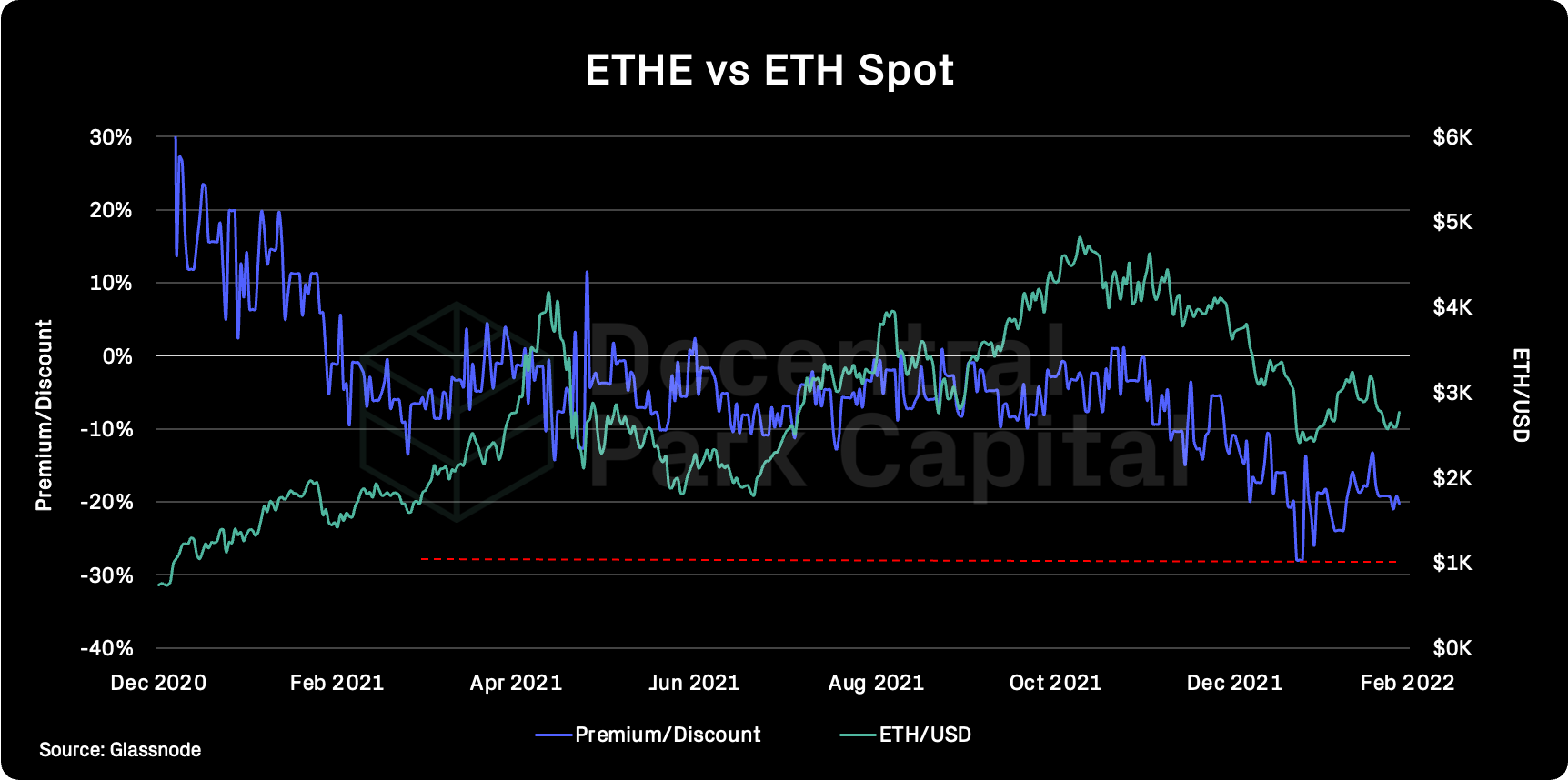

ETHE premium; ETHE discount to NAV has kept steady at 20% which appears to be the oscillation level. Secondary market volumes for ETHE has fallen 5% WoW.

Bitcoin Mempool activity (Size in MB); The mempool size for the Bitcoin network has fallen back to low levels indicating on-chain activity being fairly low.

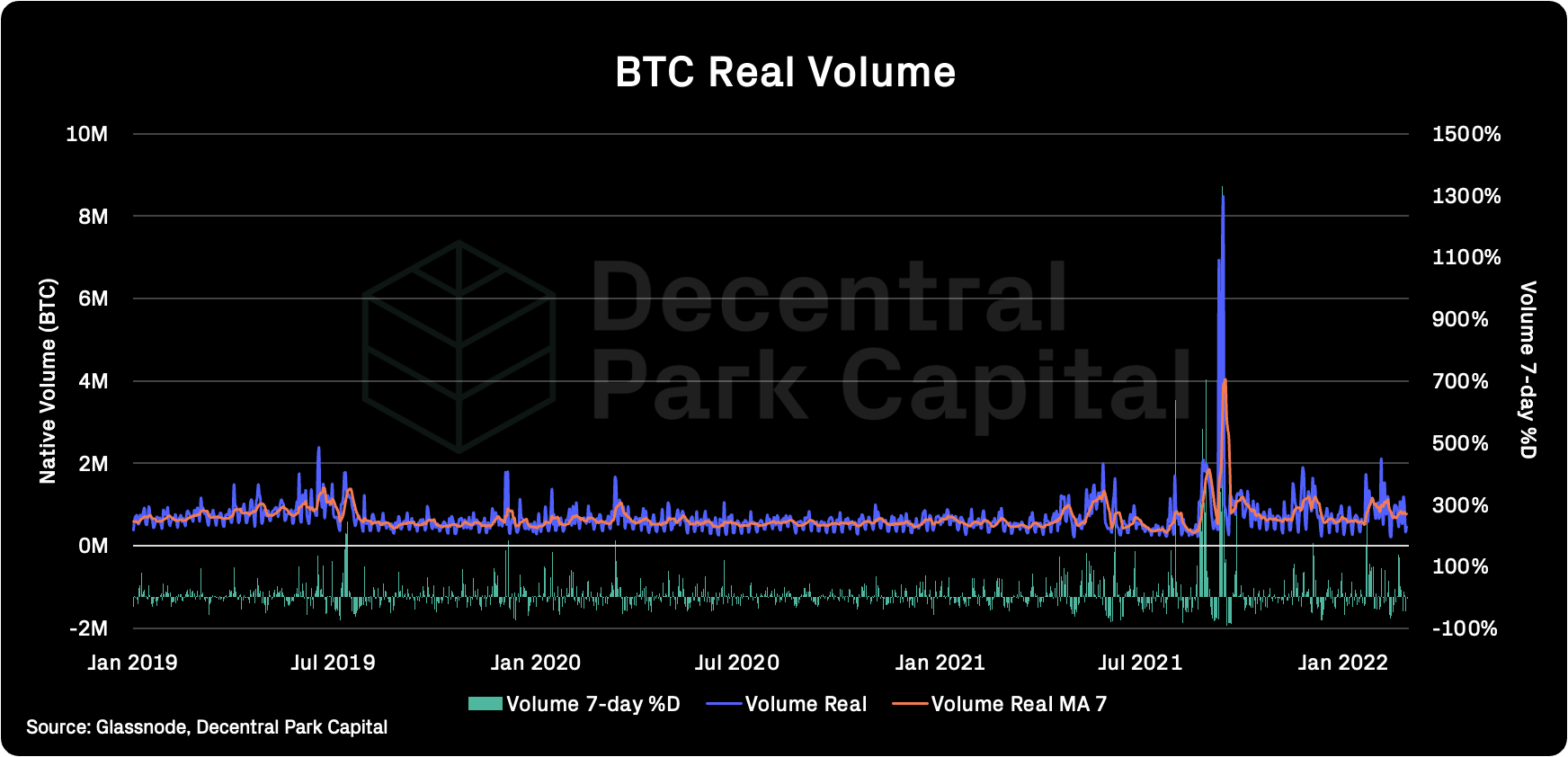

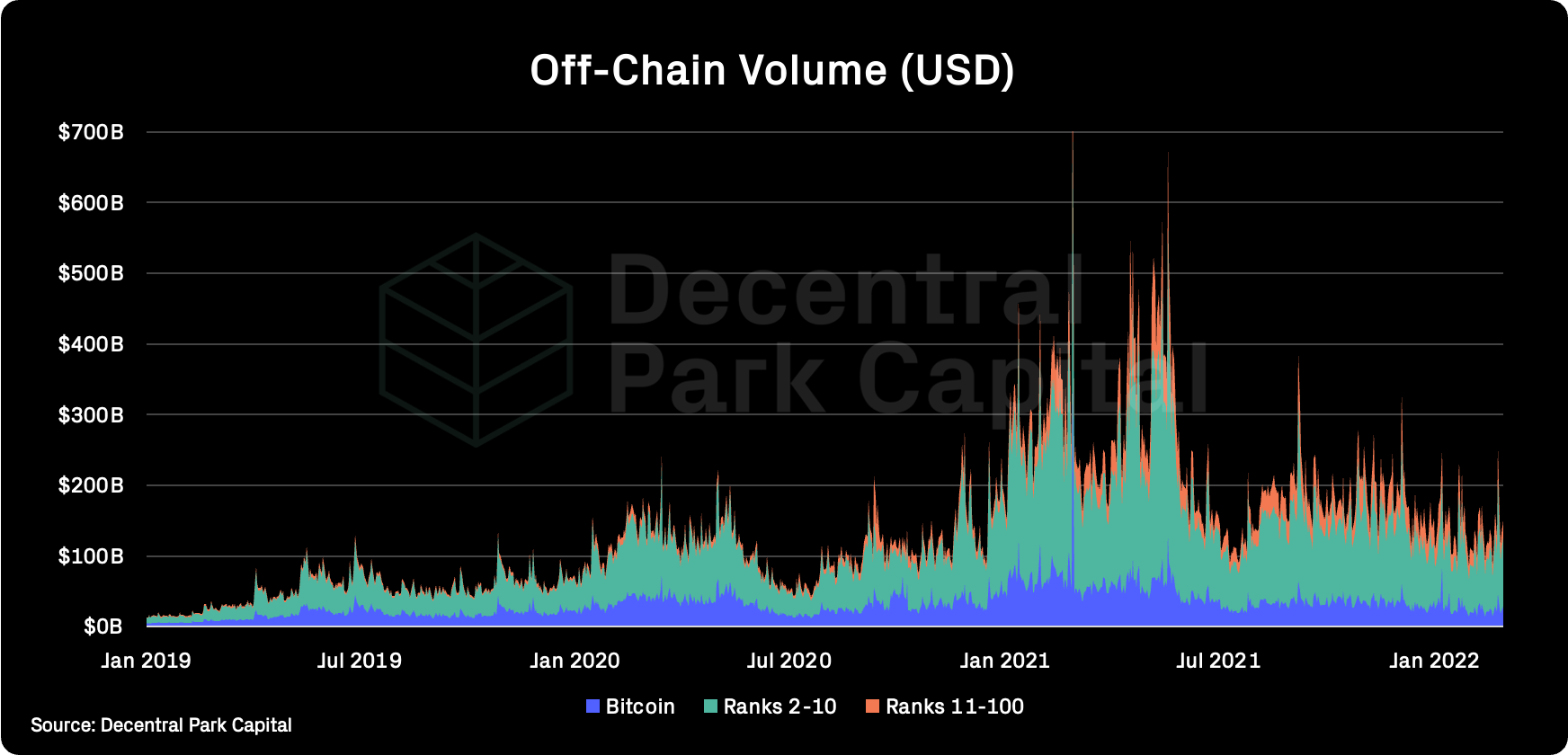

On-chain real (BTC) & off-chain volume; BTC on-chain volume has fallen ~13% over the past week. BTC spot volumes has picked up significantly, increasing 50% and 51% for BTC an ETH respectively over the past week (7d MA).

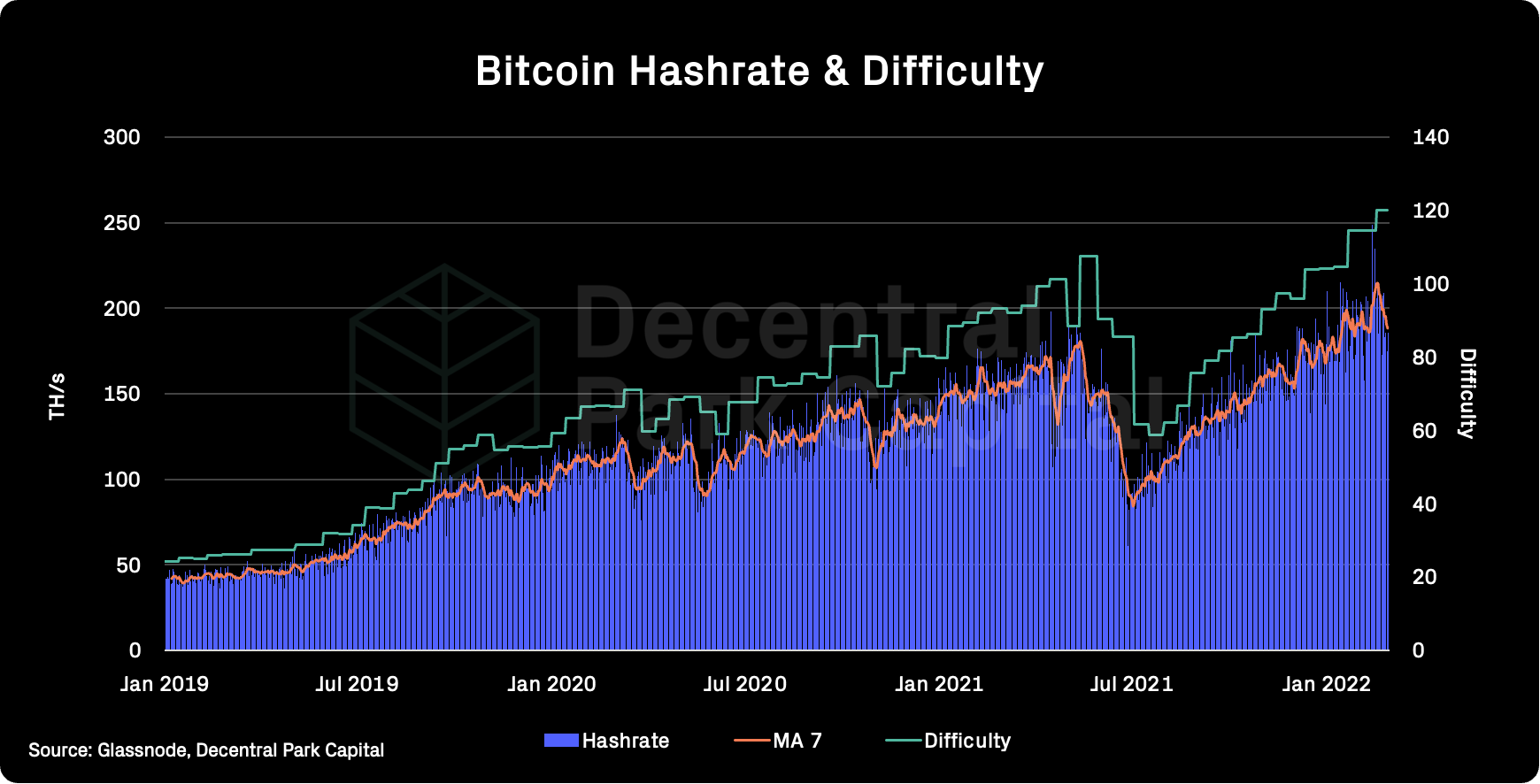

Hashrate & Difficulty; Bitcoin hashrate has fallen 3% from its ATH (199 TH/s; 7d MA). Bitcoin mining difficulty expected to fall 0.97% as a result of the hashrate drop.

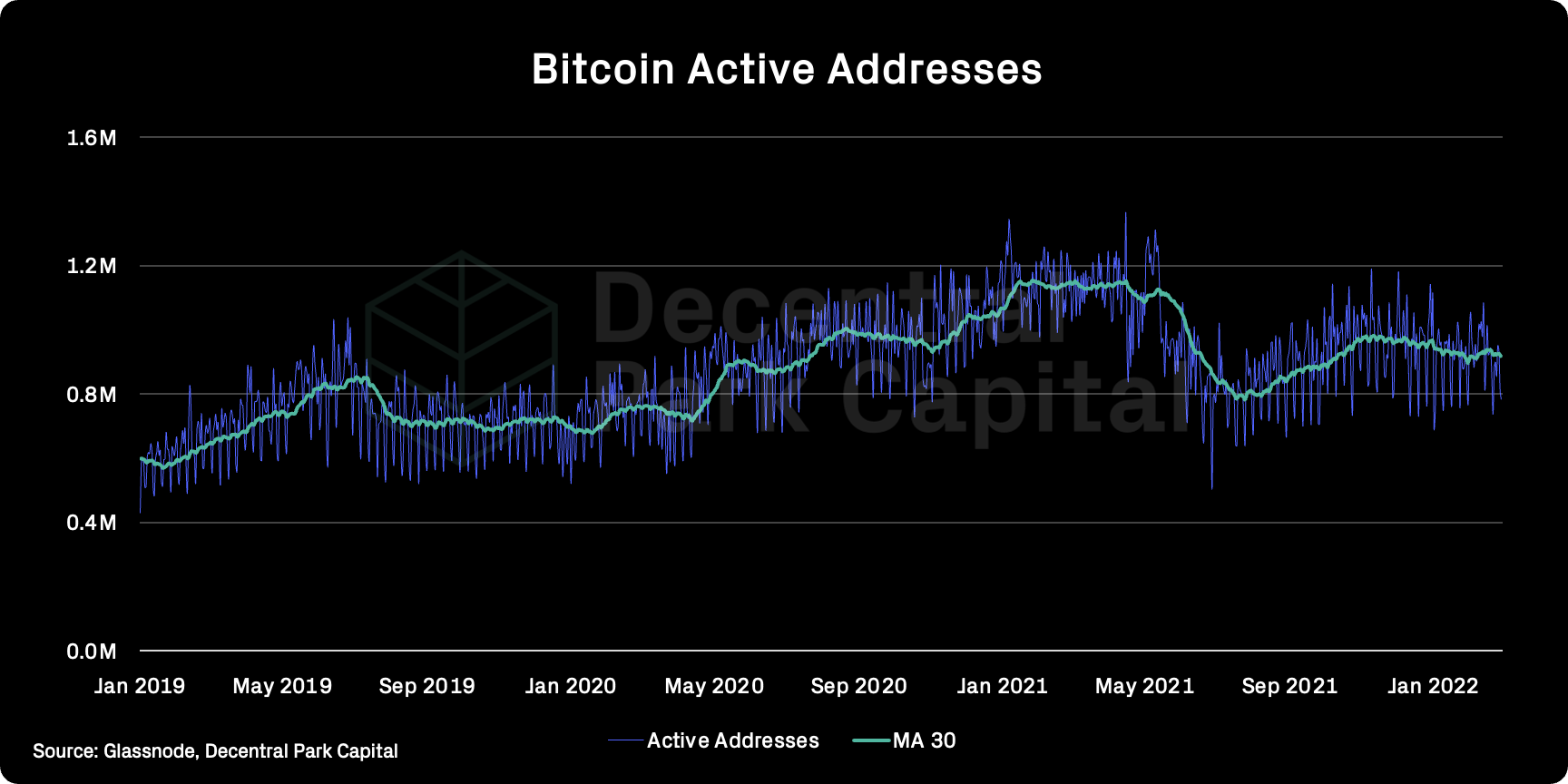

Active addresses (BTC); Active addresses (30d MA) has fallen 1% over the past week breaking its gradual trend higher YTD.

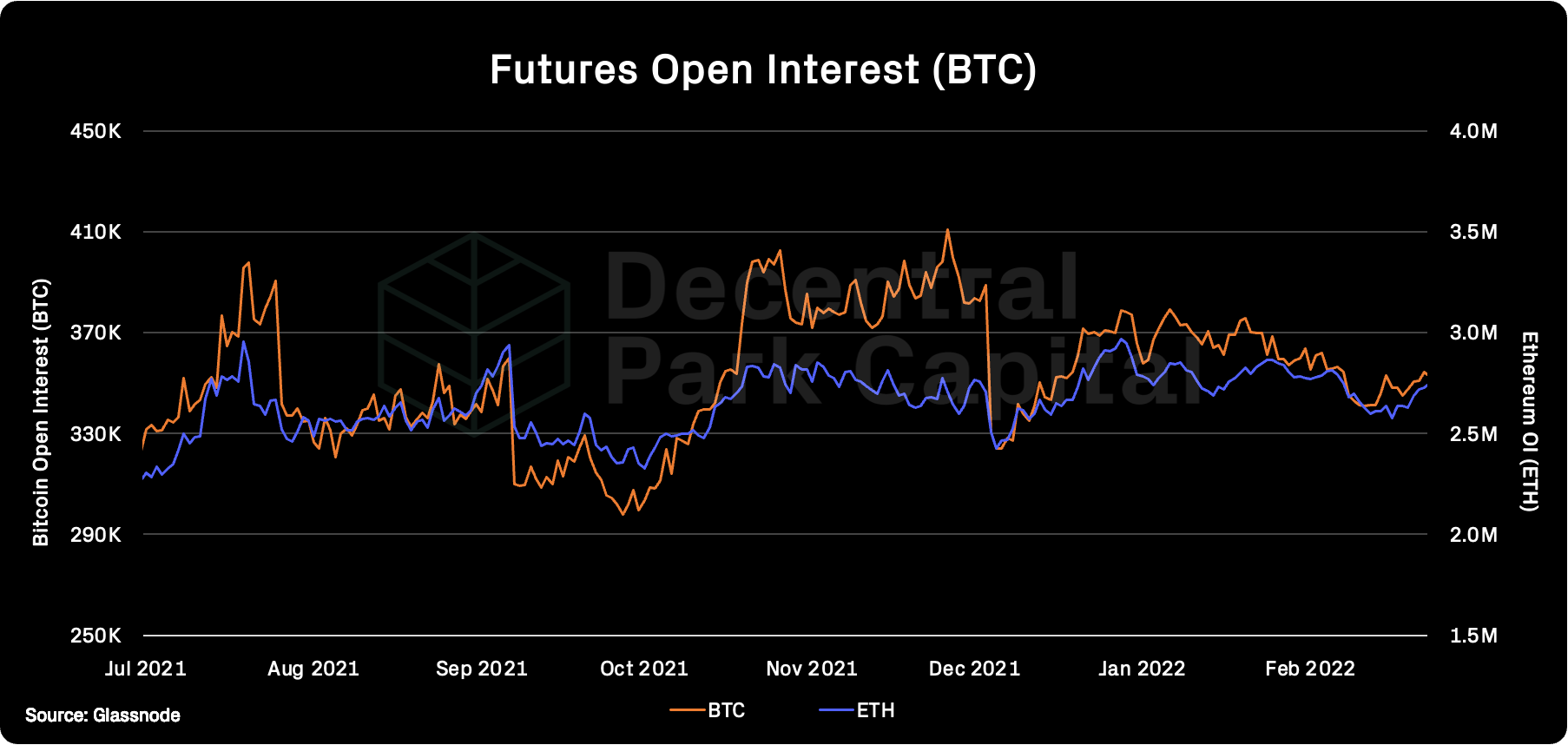

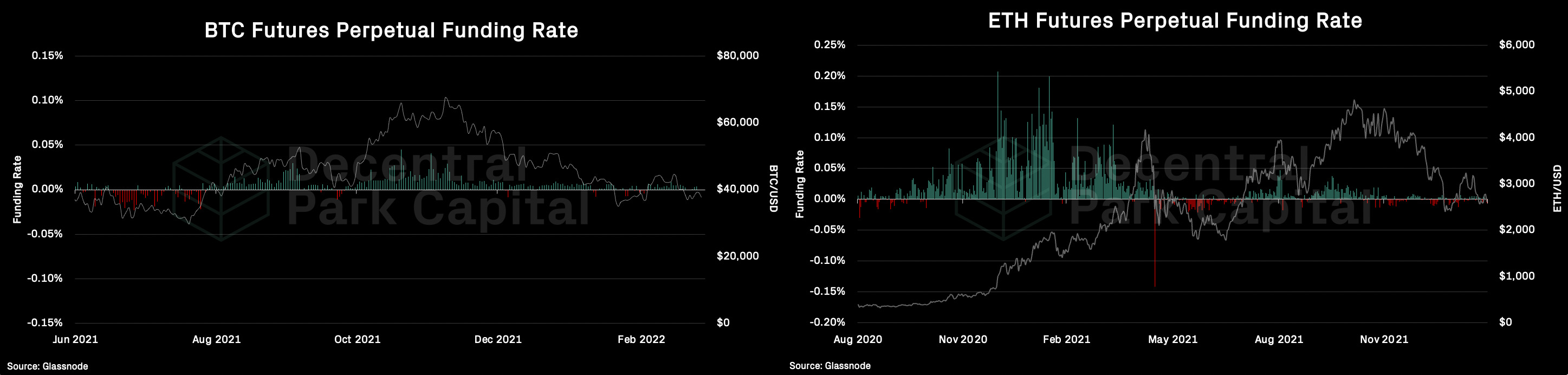

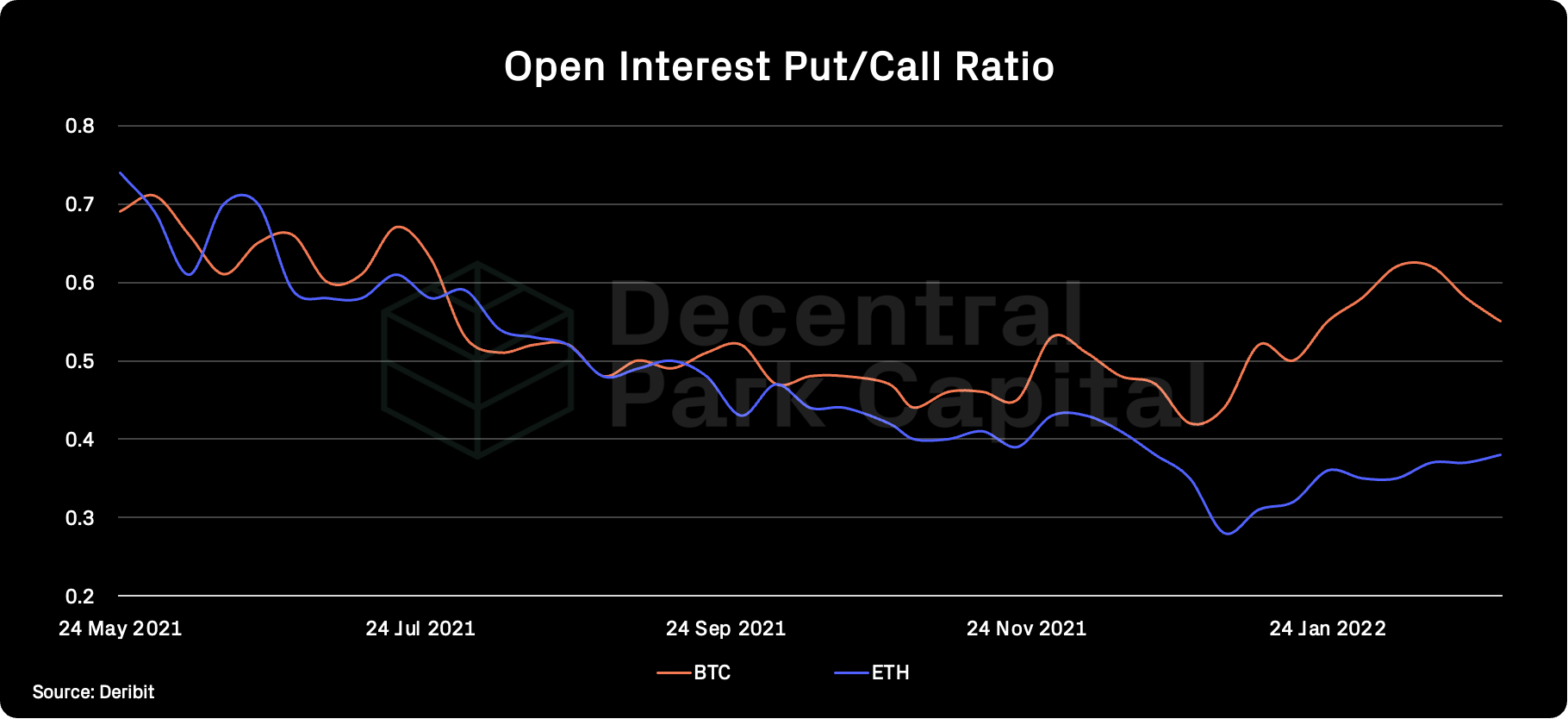

Trader positioning; Putt/Call ratio for BTC and ETH converging with BTC seeing relative growth in calls. Aggregate funding rates became moderately negative for BTC and ETH. Bitcoin futures OI has increased to 343k (+1%) BTC while Ethereum futures 2.6M ETH (+1%).

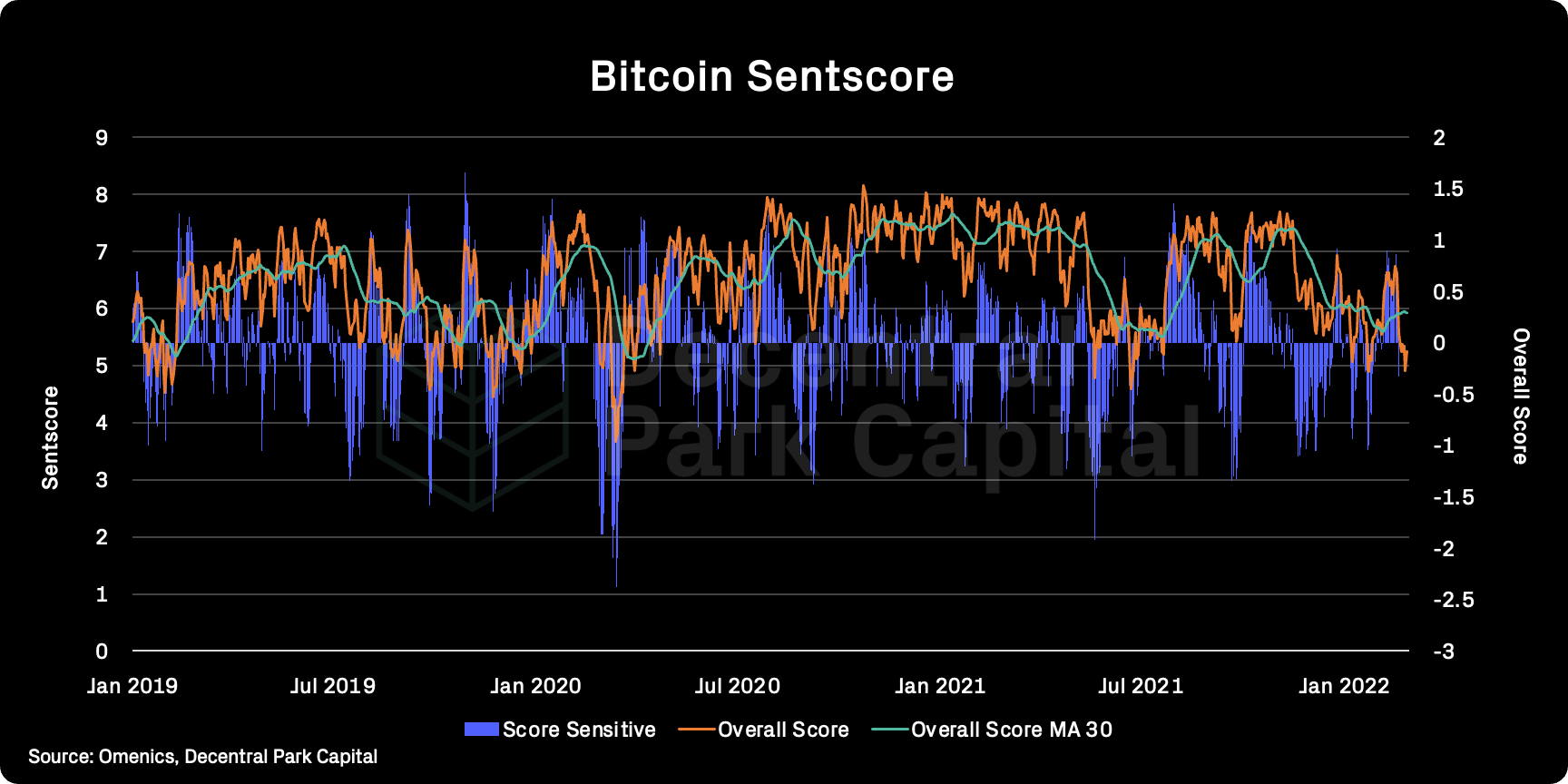

Omenics Sentscore (BTC); Sentiment score around BTC dropped over the past few days amid growing uncertainty around the Ukraine conflict. Crypto fear & greed index is 20.

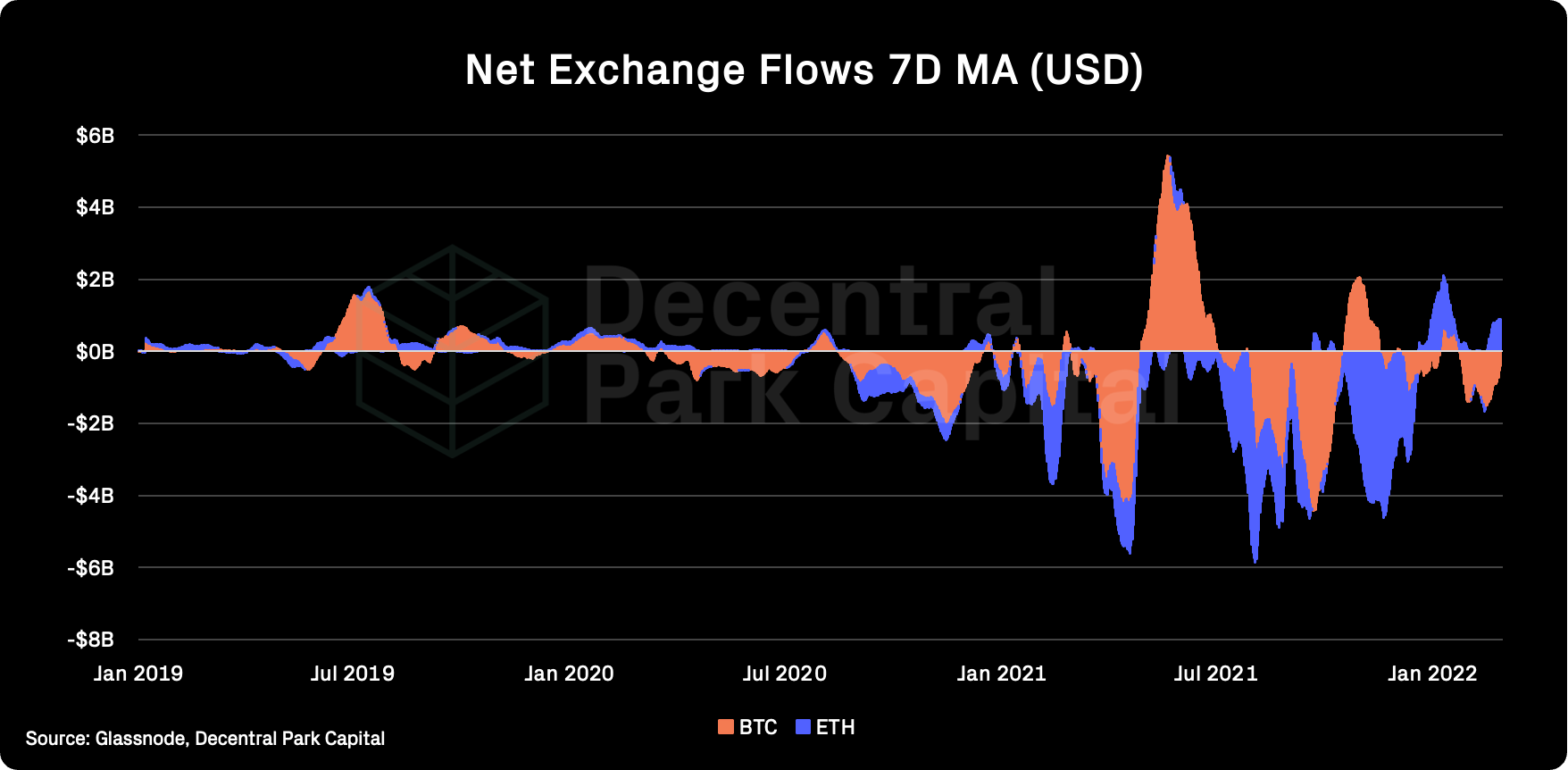

Exchange inflow/outflow (BTC, ETH); Divergence between BTC and ETH with regards to net exchange flows continued but this may be changing. Exchanges are seeing ~$477 net inflows of BTC to exchanges while exchanges are seeing $1b net inflows of ETH to exchanges.

📚 On Freezing Russian Accounts [Jesse Powell]

📚 Balaji On Outcomes [@balajis]

📚 Crypto As A Risky Asset [@Messari]

📚 Starknet Updates [@swagitmus]

📚 Options Markets With Evolving Ukraine Situation [@DeribitInsights]

🎙️ Leo Lucisano (Decentral Park Capital) on Regulatory Predictions for 2022 [Castle Island Ventures]

🎙️ Scaling Ethereum With Polygon [Zero Knowledge]

🎙️ What’s Real About Crypto Gaming [Bankless]

🎙️ Building Bitcoin DeFi [The Defiant]

🎙️ Can Bitcoin Stay Bipartisan? [The BreakDown]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.