The Weekly 295

The Market

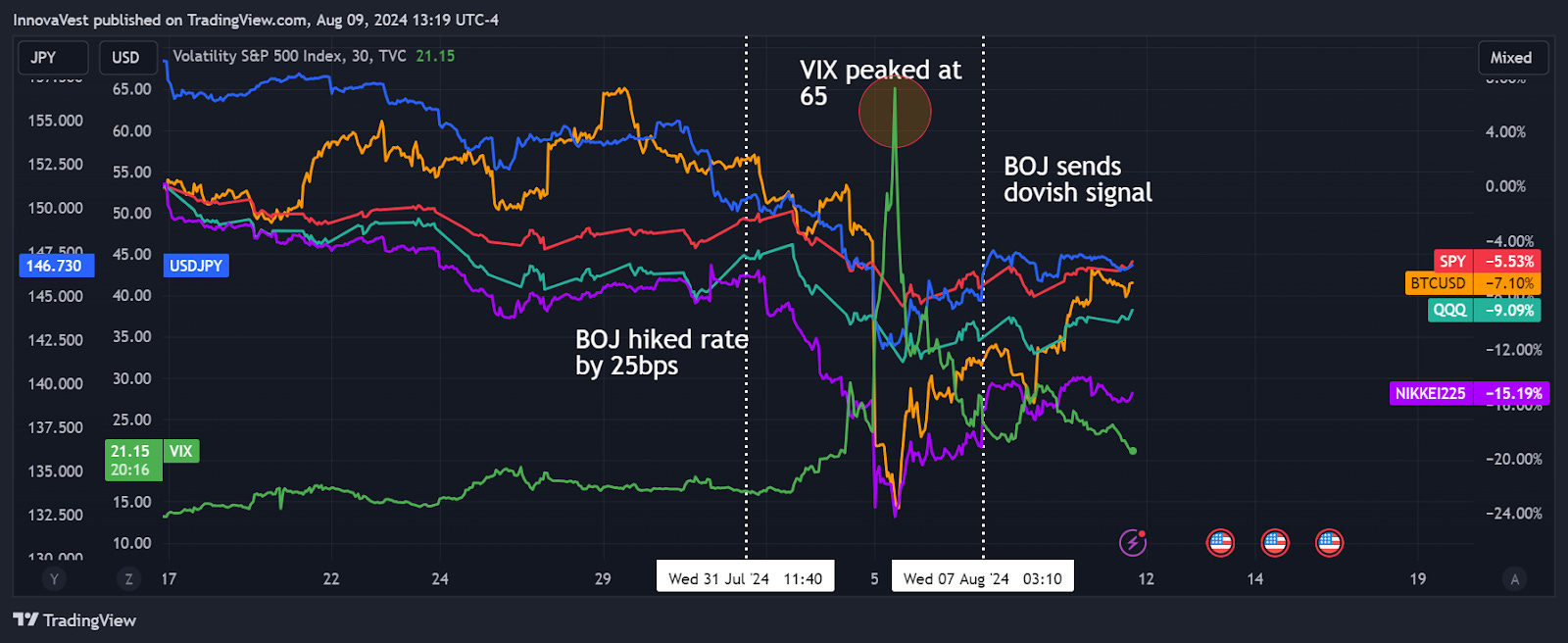

The market went through a whirlpool last week as the BOJ rate hike and disappointing US jobs data triggered a global selloff in risk assets. The VIX index briefly rose to 65, a level last seen during covid, and the Nikkei index sold off by as much as 10% during the week. However, the market stabilized as the BOJ quickly issued dovish signals, indicating no further rate cut in the near term. The VIX came back down to below 25, and both the equities market and the USD/JPY exchange rate ended the week slightly higher.

The crypto market followed a similar pattern but with greater volatility. BTC experienced a drawdown of ~18% over the weekend but bounced back along with other risk assets, ending the week flat. Solana bounced back more strongly, closing the week up 7.17%. ETH, however, fared worse, ending the week down more than 10% due to large liquidations by Jump crypto over the past week.

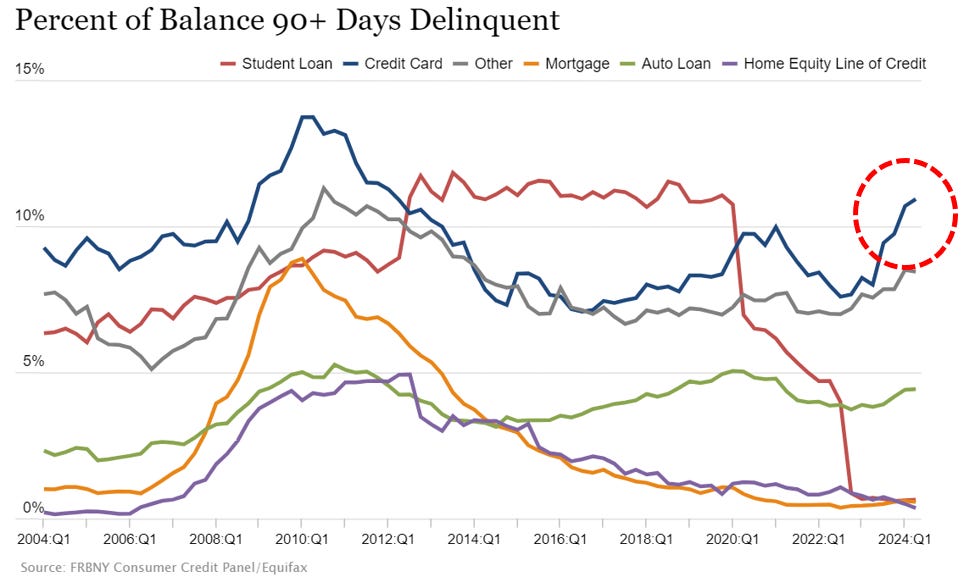

With BOJ signaling no more hikes in the near term and the tension in the Middle East abating - both developments achieved under significant US influence - we expect domestic affairs to have a greater impact on near-term risk sentiment. The Fed is facing a dilemma on how much and how quickly to cut rates. On one hand, the weakness in the labor market has sparked concerns of a potential recession; on the other hand, inflation remains above the Fed’s target level despite signs of cooling. An alarming trend to watch is the rise in the credit card and auto loan delinquency rates, with the former surpassing levels last seen during the covid lockdown. Inflation is hitting lower-income families harder, while the affluent enjoy a booming stock market and low mortgage rates locked down for the long term. This bifurcated U.S. economy is deepening political divisions, likely to play a significant role in the upcoming election.

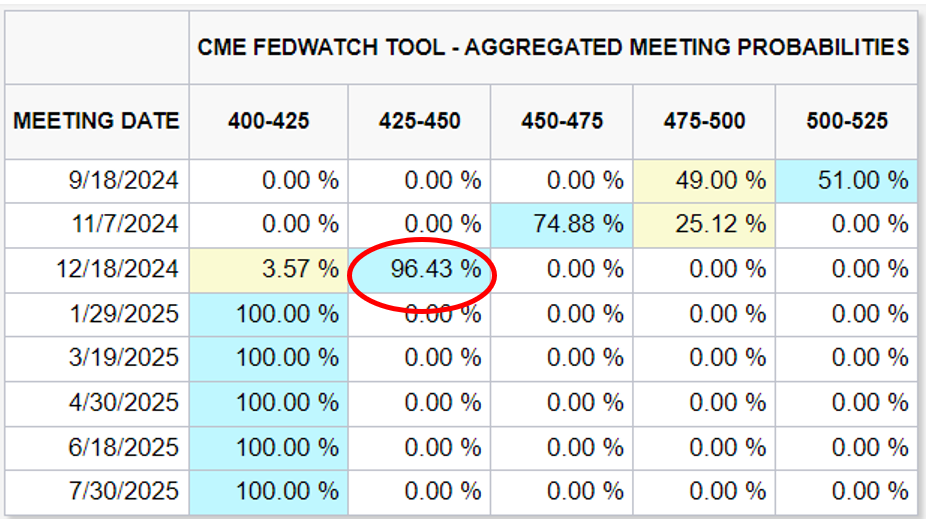

The market is pricing in at least one rate cut in September and a 96.43% chance of a full percent cut by the end of this year.

Source: CBOE FedWatch. 8/11/2024

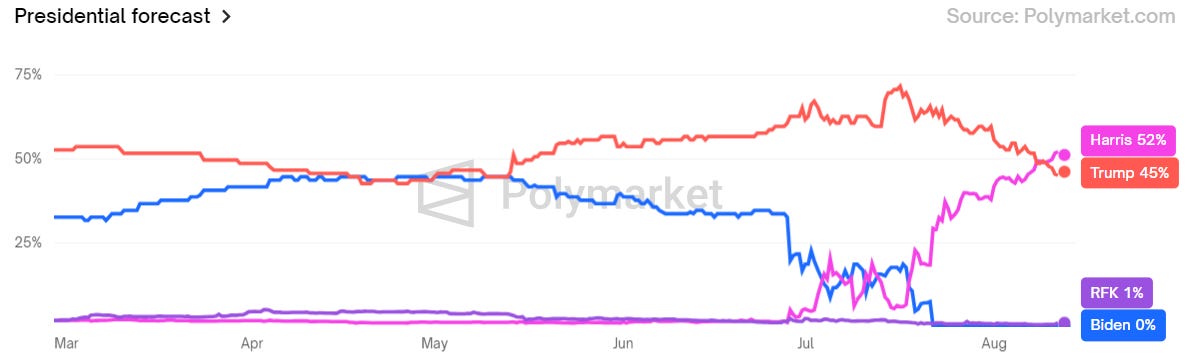

The prediction market is now pricing in higher odds for the Democrats to win the election as Kamala announced her choice of VP, who could counterbalance JD Vance’s appeal to the blue-collar working class. While we believe the election outcome will not significantly impact the long-term direction of the crypto industry, given that the Democrats have not yet made a clear stance on their crypto policy, we expect more short-term volatility.

Given how quickly the risk market has bounced back, we do not expect a system-wide catastrophic drawdown to continue in the near term. Encouragingly, there is an increase in stablecoin net supply, indicating fresh money is willing to enter the crypto market. We believe the Fed’s rate decision in September could remove some uncertainty and shore up investor’s confidence in Q4. Until then, we expect continued volatility as more economic data emerges and the election odds fluctuate.

DeFi Update

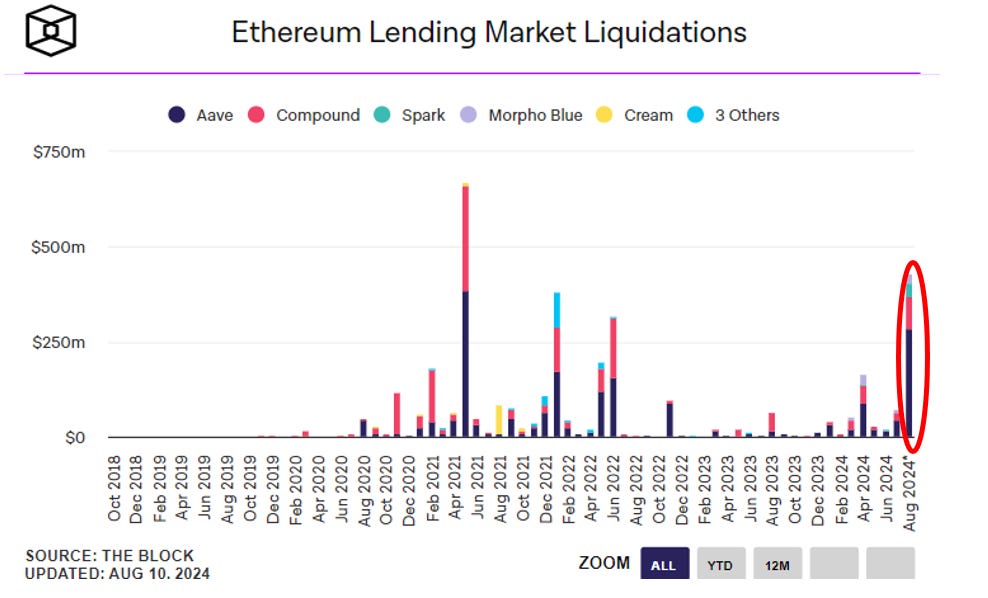

Last week’s selloff provided another stress test opportunity for the DeFi ecosystem. The Ethereum lending market processed over $400M in liquidations, the second largest since the crypto winter in May 2021.

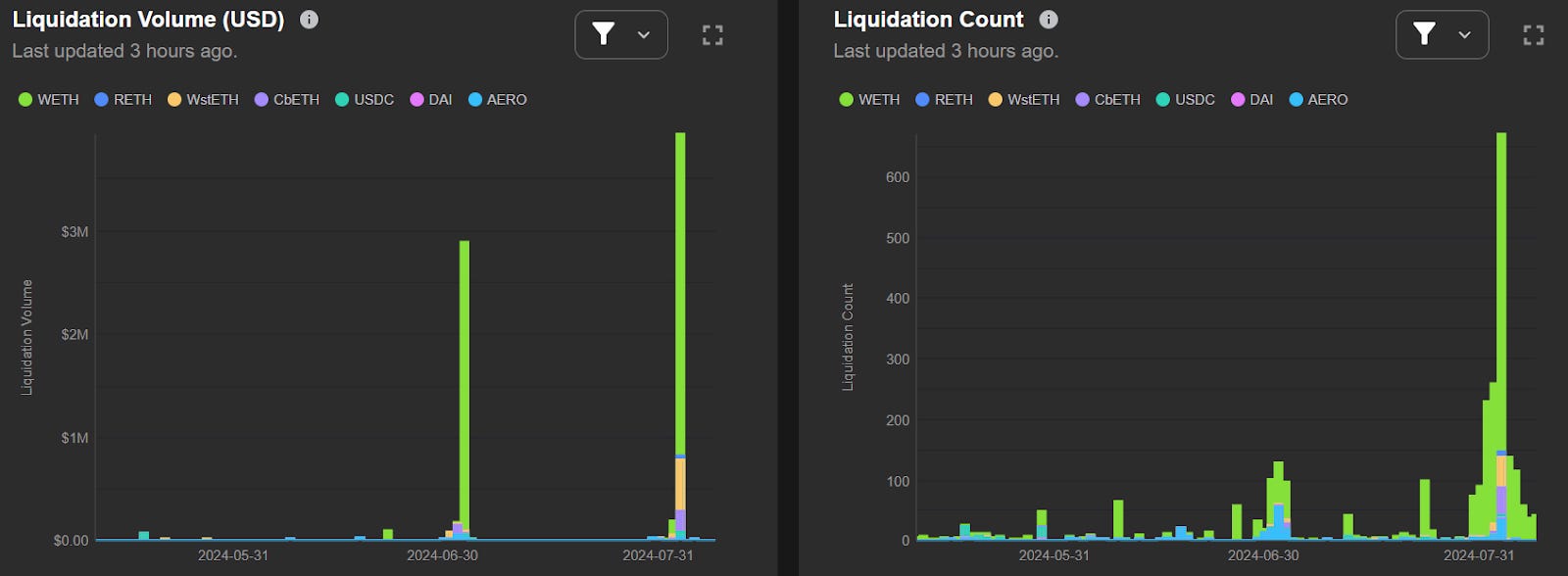

Aave alone has processed $300M liquidations with no bad debt and generated $2.1M daily revenue from the liquidation proceeds. Newer players also posted solid results. Moonwell, the largest lending protocol by revenue on the Base network, handled close to $5M in liquidations last week. Kamino, the largest lending protocol on Solana, also managed $4M liquidations with no bad debt.

Source: Gauntlet, Moonwell. 8/11/2024

Although DeFi trading volume has recovered to levels last seen during DeFi summer, borrowing and lending activity is still about half of the peak level. In the Solana ecosystem in particular, while trading volume has reached an all-time-high, borrowing amounts are only half of their peak. As the Solana ecosystem continues to grow, we see more room for the lending activities to expand.

Source: DeFiLlama. 8/11/2024. TVL only includes borrowing.

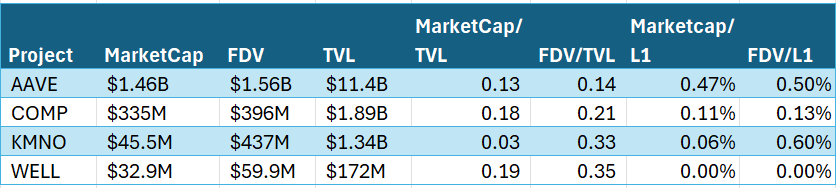

From a valuation perspective, Kamino’s MarketCap to TVL ratio is lower than other lending protocols on Ethereum. As the top lending protocol on Solana, its market cap is only 0.06% of SOL, compared to AAVE’s 0.47% of ETH. Although only about 10% of KMNO tokens are currently in circulation, the same metrics applied to FDV still do not appear expensive. In fact, after a brief 30% selloff last Sunday, KMNO price more than doubled through the course of the week, making it the top performer in the Solana ecosystem last week.

Source: Messari. 8/11/2024

Top 100 MCAP Winners

SUI (+45.56%)

ZCash (+28.63%)

Helium (+26.84%)

Bittensor (+18.18%)

Akash Network (+14.15%)

Top 100 MCAP Losers

Lido DAO (-20.81%)

Maker (-14.06%)

Aave (-13.72%)

Gala (-12.13%)

Artificial Superintelligence Alliance (-11.57%)

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.

About the Author

Kelly is Portfolio Manager and Head of Research at Decentral Park Capital. Investing across sectors with a thesis driven, deep research approach.

Prior to this, Kelly has led research and product efforts at CoinDesk Indices and Fidelity Digital Asset Management. Kelly has been a TradFi investor for 15 years before joining the crypto space.

You can follow Kelly on Twitter and LinkedIn for more frequent analysis and updates.